UNIT - Uniti Group: The Trap Of High Dividend Yield

2023-05-20 00:13:17 ET

Summary

- Despite impaired financial results in the first quarter of 2023, the company’s Board of Directors managed to declare a 1Q 2023 cash dividend of $0.15 per share.

- Also, for the second quarter of 2023, the Board of Directors declared a cash dividend of $0.15 per share.

- However, the company is not sourcing these cash payments through its cash provided by operating activities.

- Due to high interest rates, I expect UNIT’s interest expenses to remain high in the upcoming quarters.

- Also, due to its customer concentration, the company may not be able to benefit from the strong market outlook as much as its peers.

With a fiber route of about 137 thousand miles, Uniti Group ( UNIT ) is the eighth-largest fiber provider in the United States. Hiked interest rates negatively affected the company's cash position in 1Q 2023 and 4Q 2022 significantly. Uniti Group reported 1Q 2023 FFO, and AFFO of $0.15, and $0.39 per diluted share, respectively, compared with $0.40, and $0.43 in 1Q 2022. Despite unsatisfactory financial results, the company managed to pay 1Q 2023 cash dividend of $0.15 per share. Also, on 2 May 2023, UNIT's Board of Directors declared a cash dividend of $0.15 per share for the second quarter of 2023, payable on June 30 to stockholders of record on June 16, 2023. However, the sources of these cash dividends are not UNIT's cash provided by operating activities. Furthermore, as interest rates are expected to remain relatively high for now, the company may continue paying high interest expenses at least for a few upcoming quarters. On the other hand, the stock's price has already dropped 65% in the past year. Also, regardless of the sources of its dividend, UNIT's 1-year forward dividend yield is relatively high (about 16%). Thus, some investors may see it as opportunistic, and pile on the stock. However, based on the company's financial position, signaling a dividend cut in the second half of 2023, and the company's limited ability to benefit from the strong market outlook (due to its customer concentration), I conclude that buying the stock even at its current prices still may be too risky. UNIT stock is a hold.

Financial results

In its first quarter 2023 financial results, Uniti Group reported total revenues of $290 million, compared with $278 million in 1Q 2022, driven by higher leasing revenue and fiber infrastructure revenue. The company's total costs and expenses increased from $228 million in 1Q 2022 to $312 million in 1Q 2023, as a result of increased interest expenses (due to hiked interest rates), and other expenses of $20 million. Thus, UNIT's net income (attributable to common shareholders) of $52 million in 1Q 2022, turned into a net loss of $29 million in 1Q 2023.

It is worth noting that the company's net income in 1Q 2022 turned into a net loss in 2Q 2022 due to one-time items.

"Net loss attributable to common shares was $19.5 million for the period, and included the write-off of $10.4 million of deferred financing costs and $52.0 million of costs related to the early repayment of the 7.875% Senior Secured Notes due 2025," the company explained.

At the end of the first quarter of 2023, UNIT's unrestricted cash and cash equivalents, and undrawn borrowing availability under its revolving credit agreement were $495 million, compared with $356 million at the end of 4Q 2022, and $387 million at the end of 1Q 2022. Thus, despite impaired FFO and AFFO in the first quarter of 2023 compared with the previous quarter and the same period last year, UNIT managed to increase its cash equivalents, and undrawn borrowing availability under its revolving credit agreement, which made the Board of Directors able to declare a 1Q 2023 quarterly cash dividend of $0.15 per common share, flat YoY and QoQ. Excluding undrawn borrowing availability under revolving credit agreement, at the end of 1Q 2023, UNIT's cash, and cash equivalents were $70 million, compared with $44 million at the end of 4Q 2022 and $51 million at the end of 1Q 2022. However, the company's cash and cash equivalents at the end of 1Q 2023 were higher than in 1Q 2022 and 4Q 2022, as the company's proceeds from the issuance of notes increased from zero in 1Q 2022 and $307 million in 4Q 2022, to $2.6 billion in 1Q 2023. Also, you should know that the company's repayment of debt in 1Q 2023 was $2.3 billion, compared with zero in 1Q 2022. Furthermore, it is essential to know that UNIT's net cash provided by operating activities in 1Q 2023 was significantly lower than in the previous quarter and the same period last year.

While the company's FFO dropped from $105 million in 1Q 2022 to $35 million in 1Q 2023, excluding special items (most importantly, write off of deferred financing costs and debt discount of $10.4 million, and costs related to the early repayment of debt of $52.0 million), UNIT's AFFO in 1Q 2023 was $107 million, about $72 million higher than its FFO. However, UNIT's AFFO in 1Q 2023 was still 4.5% lower than in 1Q 2022.

The company estimates its full-year 2023 net income per diluted share to be between $0.26 to $0.34, compared with a net loss of $0.04 per diluted share in 2022. Also, UNIT estimates its full-year 2023 FFO and AFFO to be $1.05 to $$1.12 per diluted share and $1.38 to $1.45 per diluted share, compared with the full-year 2022 FFO of $0.77 per diluted share, and AFFO of $1.75 per diluted share.

The company's full-year 2023 interest expense is estimated to be $517 million, compared with $377 million in 2022. Also, UNIT's 2023 total revenue is expected to be between $1.2 billion, compared with $1.1 billion in 2022. It is worth noting that in its 4Q 2022 financial results, the company estimated that in 2023, its total revenue to be $1.2 billion, its interest expense to be $550 million, its FFO to be between $1.00 to $1.06 per diluted share, and its AFFO to be between $1.36 per diluted share to $1.43 per diluted share. Thus, we can see that after a few months, UNIT's management concluded that the company's full-year 2023 interest expense can be lower than previously expected, and its 2023 FFO and AFFO can be higher than previously expected. However, the company still expects its AFFO to be lower than in 2022.

The market and performance outlook

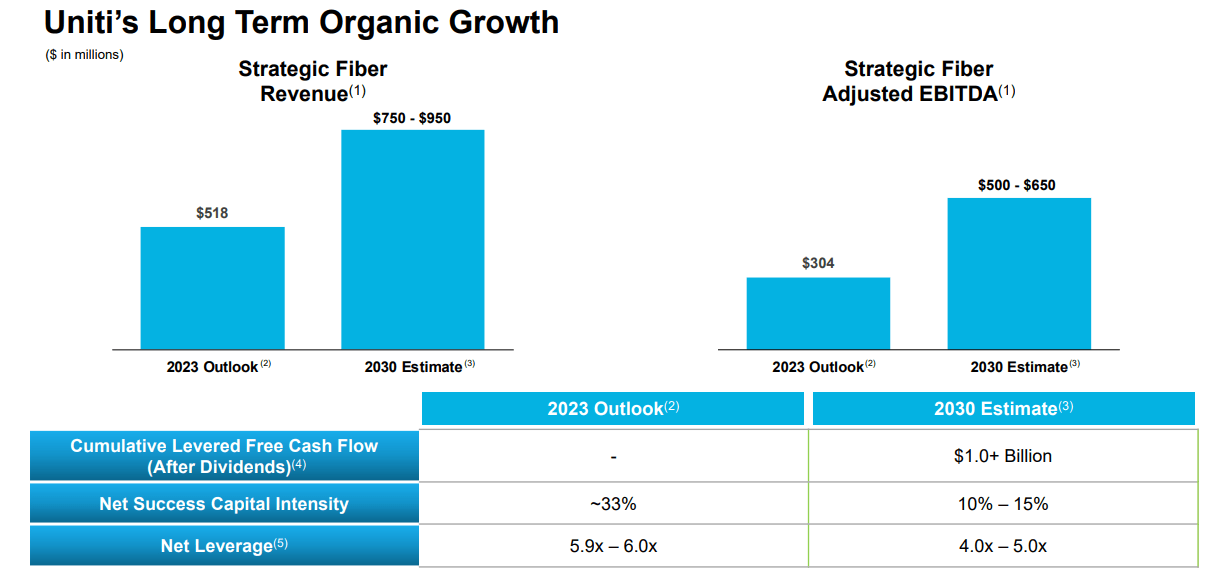

The market outlook for high-capacity long-haul market routes is strong. According to Figure 1, the North American dark fiber demand is expected to grow at a CAGR of 10% from 2022 to 2030, reaching $4 billion, compared with less than $2 billion in 2022. Also, the annual North America wavelength sales which is currently about $2 billion, is expected to grow at an annual rate of 7%. According to its current capacity and customers, UNIT estimates its 2023 strategic fiber revenue and strategic fiber adjusted EBITDA to be $518 million and $304 million, respectively. Figure 2 shows that by 2030, Uniti Group expects its strategic fiber revenue and strategic fiber adjusted EBITDA to increase to $750-$950 million and $500-$650 million, respectively. Furthermore, the company expects its net leverage (calculated as net debt divided by total adjusted EBITDA) to decrease from 5.9-6.0 in 2023 to 4.0-5.0 in 2030.

At first glance, according to the strong market outlook for high-capacity long-haul market routes and strong dark fiber demand in the following year the United States, UNIT has the opportunity to increase its revenue and decrease its debt ratios in a significant way. However, it would not be easy. According to the company's 2022 Form 10-K , some of UNIT's competitors are significantly larger and have greater financial resources and lower costs of capital. Also, a great part of UNIT's revenue is dependent on the ability of Windstream to compete with other communication services. For the year ended 31 December 2022, 66.5 of UNIT's revenues were derived from leasing its distribution systems to Windstream. According to comparably.com, compared with AT&T ( T ), T-Mobile ( TMUS ), and Verizon ( VZ ) (three of the greatest competitors of Windstream), Windstream ranks 4th in the product quality score, net promoter score, pricing score, and customer services score. Thus, if Windstream couldn't increase its market share as much as its competitors, UNIT may not be able to improve its financial results as easily as it can be said in the following years. Also, it is worth noting that the initial term of the Windstream leases expires on 30 April 2030, and UNIT may not be able to renew the Windstream leases upon their expiration or find new customers on commercially attractive terms. Thus, as the company's customer portfolio is not diversified, and its main customer may not be able to grow along with its peers, UNIT's financial results may not improve as it expects.

Figure 1 - North America dark fiber demand

1Q 2023 presentation

Figure 2 - Uniti's long-term organic growth

{kind=link}

Summary

65% of UNIT's revenue is connected to its long-term agreement with Windstream. As Windstream's competitiveness in the industry is not significant, this customer concentration may limit UNIT's ability to benefit from the strong market outlook in the following years. Despite impaired financial results, UNIT's Board of Directors managed to maintain the company's quarterly dividends at $0.15 per share. However, they may get into a condition to start cutting dividends soon. The stock is a hold.

For further details see:

Uniti Group: The Trap Of High Dividend Yield