UTL - Unitil Corporation: Conservative Play With EPS Growth Expected And Undervalued

2023-08-09 17:04:45 ET

Summary

- Unitil Corporation offers dividend growth and expects EPS growth of 5%-7%.

- Investments in infrastructure and new building permits in Maine and New Hampshire will likely lead to free cash flow and net income growth.

- The stock appears undervalued, despite risks of lower gas demand.

Unitil Corporation ( UTL ) continues to offer dividend growth, and expects to obtain EPS growth close to 5%-7%. In my view, further investments in new infrastructure, modernization, new building permits, and construction employment in Maine and New Hampshire will most likely lead to free cash flow ("FCF") growth and net income growth. I did find several risks from lower gas demand and lower client count growth, however, the stock appears a bit undervalued.

Unitil Corporation

With active operations in New Hampshire, Massachusetts, and Maine, Unitil is a company dedicated to supplying electricity and natural gas to residences and businesses. Unitil operates in each of these regions through its subsidiaries, Unitil Energy, which offers electricity to New Hampshire, Fitchburg in central and northern Massachusetts, which supplies both electricity and natural gas, and Northern Utilities, exclusively dedicated to the supply of natural gas in southern New Hampshire and the city of Portland .

Source: Earnings Call

The activities of this company are divided into two segments, electricity distribution and gas supply. Each of these segments represents approximately half of the company's annual revenues.

Both subsidiaries in this segment function as gas distributors and not as producers. The customers contract the service of other competitors and use the distribution lines of Unitil for access to gas. The company also serves businesses related to agriculture, the production of fiber paper, the plantation of cannabis, and to a lesser extent educational institutions.

Unitil's model is based on revenue decoupling. This means a separation between the amount of resources used and the economic return created. Ultimately, this is a strategy used by a large number of companies in the energy field globally, and its objective is to optimize the business and reduce operating costs.

I believe that Unitil Corporation is an interesting play for the investors looking for a conservative business model offering single digit EPS growth. In the last earnings call, the company noted that it expects long-term EPS growth rate close to 5%-7%. I included some of these figures in my discounted cash flow ("DCF") model.

Source: Earnings Call

Balance Sheet

I appreciate that Unitil Corporation continues to finance new utility plant developments, resultantly enhancing the total amount of assets. In 2023, the company reported more net utility plant assets, regulatory assets, and material and supplies than that on December 31, 2022. The balance sheet appears to be growing.

As of June 30, 2023, Unitil Corporation reported cash and cash equivalents of $6.8 million, with accounts receivable of $59.5 million, accrued revenue worth $60.4 million, and exchange gas receivable close to $9.4 million. Also, with gas inventory of $1 million, materials and supplies close to $12.9 million, and prepayments worth $11.3 million, total current assets stood at $161.3 million. Total current liabilities are worth a bit more than the total amount of current assets, which does not look ideal. Besides, with a net utility plant worth $1.357 billion, regulatory assets close to $51.5 million, and other assets of $19.5 million, total assets stood at $1.595 billion. The asset/liability ratio stands at close to 3x, so I believe that the balance sheet stands in a very good position .

Source: 10-Q

The list of liabilities includes accounts payable worth $36 million, with short-term debt close to $131 million, long-term debt current portion of about $6 million, regulatory liabilities of about $18 million, and total current liabilities worth $238 million. Besides, with cost of removal obligations worth $123 million, regulatory liabilities of $35 million, and environmental obligations worth $4 million, total noncurrent liabilities would be close to $386 million.

Source: 10-Q

DCF Model: Further Increase In PP&E, Divestitures, And Gas Customers Growth May Lead To Higher Stock Valuations

Under my DCF model, I assumed that management would most likely successfully increase the profit margin and reduce total operating costs in the coming years. Due to the nature of these types of companies, which operate in markets that are highly regulated by government institutions, business plans are totally subject to the capacity to increase the infrastructure and the arrival of new clients.

In this case, I believe that Unitil does not present views towards future acquisitions and the increase in the metropolitan centers where it provides its services. However, further increase in property, plant, and equipment as well as capacity increases will most likely lead to revenue growth and FCF margin. Considering previous increases in PP&E, I believe that we may expect further FCF growth and net income growth in the coming years.

Source: Ycharts Source: Ycharts

In line with my previous words, I would also expect further increases in dividends, which may bring the attention of more investors. The stock demand may increase, leading to stock price increases or lower cost of capital.

Source: Ycharts

I also believe that the recent customer increases are a result of the increases in capacity. In my opinion, we may see further growth in the coming years mainly in the number of gas customers.

As of June 30, 2023, the number of electric customers increased by approximately 200 over the previous year. Source: Unitil Reports Second Quarter Earnings .

The Company estimates weather-normalized gas therm sales in its Maine division, the Company’s only non-decoupled gas service area, increased 2.1% in the first six months of 2023 compared to the same period in 2022. As of June 30, 2023, the number of gas customers increased by approximately 800 over the previous year. Source: Unitil Reports Second Quarter Earnings.

In addition, in the last quarter, the company highlighted its intentions to prepare plans for four and five years to modernize some areas of its infrastructure. This modernization consists of, on the one hand, the purchase and improvement of the meters. On the other hand, it consists of a series of automation functions for the measurement of expenses, the amount of supply, and the relationship between prices and customers.

Also, in this same sense, the modernization involves the development of infrastructure to connect some of the supply sources with the same objective of optimizing performance and service. It should be noted that this modernization plan applies only to the subsidiary in Fitchburg, the only one dedicated to both the electricity segment and the natural gas distribution segment. I believe that we can expect further increase in the net income driven by the modernization plan.

With that about the developments of Unitil Corporation, I believe that ongoing development in the areas covered by the company will most likely enhance the business model. The company noted a lot of new building permits and construction employment in Maine and New Hampshire. As a result, I believe that we may see more new customer demand.

Source: Earnings Call

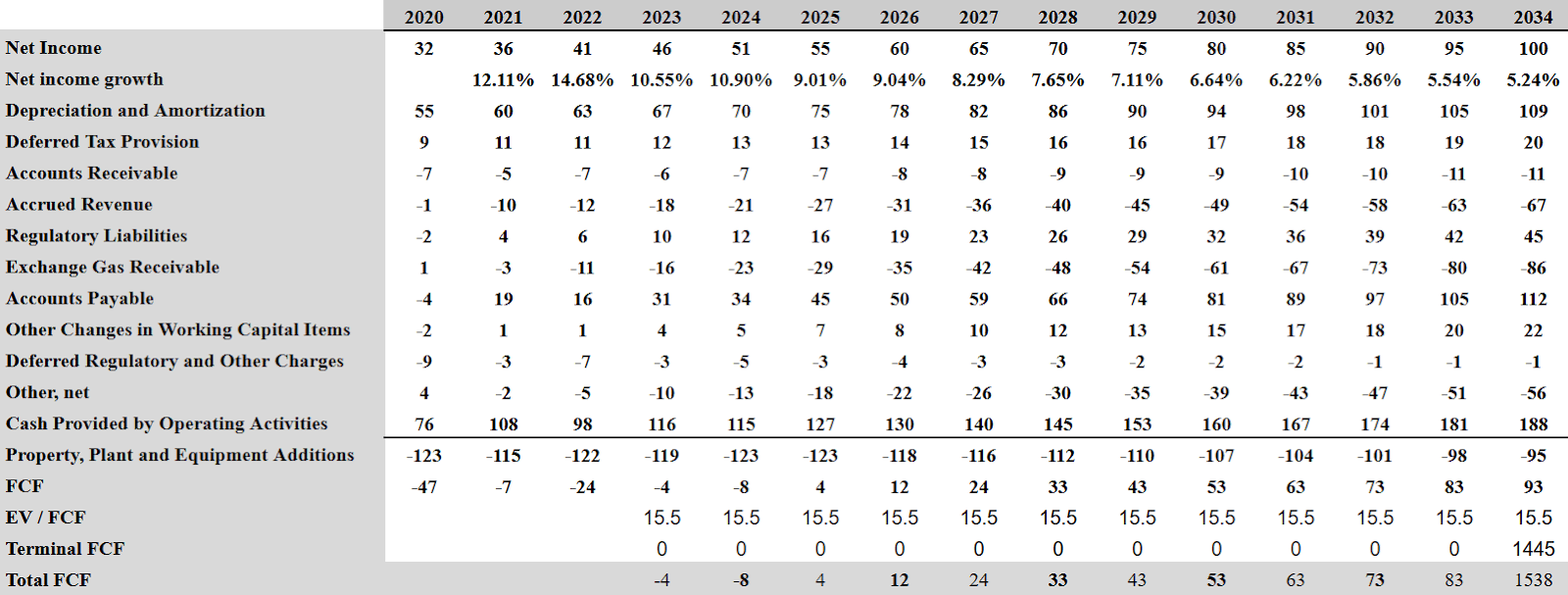

My financial model includes 2034 net income worth $100 million, with net income growth close to 5.2%. With a median net income growth close to 7.9%, I believe that my figures are conservative. The energy as a service market size is expected to grow at a CAGR of close to 10.29% from 2022 to 2030, and the utilities market may grow at a CAGR of close to 6.8%.

The global energy as a service market size was estimated at USD 65.4 billion in 2021 and is expected to hit around USD 157.87 billion by 2030, poised to grow at a compound annual growth rate (( CAGR )) of 10.29% from 2022 to 2030. Source: Energy as a Service Market Size, Growth, Report 2022-2030 .

The utilities market is expected to grow to $8,314.78 billion in 2027 at a compound annual growth rate (( CAGR )) of 6.8%. Source: Utilities Global Market Report 2023 .

{kind=link}

I also assumed depreciation and amortization worth $109 million, with deferred tax provision of about $19 million, changes in accounts receivable close to -$12 million, changes in accrued revenue close to -$68 million, and regulatory liabilities of about $45 million.

Besides, with changes in exchange gas receivable worth -$86 million, changes in accounts payable of $112 million, and other changes in working capital items of about $21 million, cash provided by operating activities would stay at close to $187.55 million. Finally, with property, plant, and equipment additions of about -$95.55 million, the implied 2034 FCF would be about $93.55 million.

{kind=link}

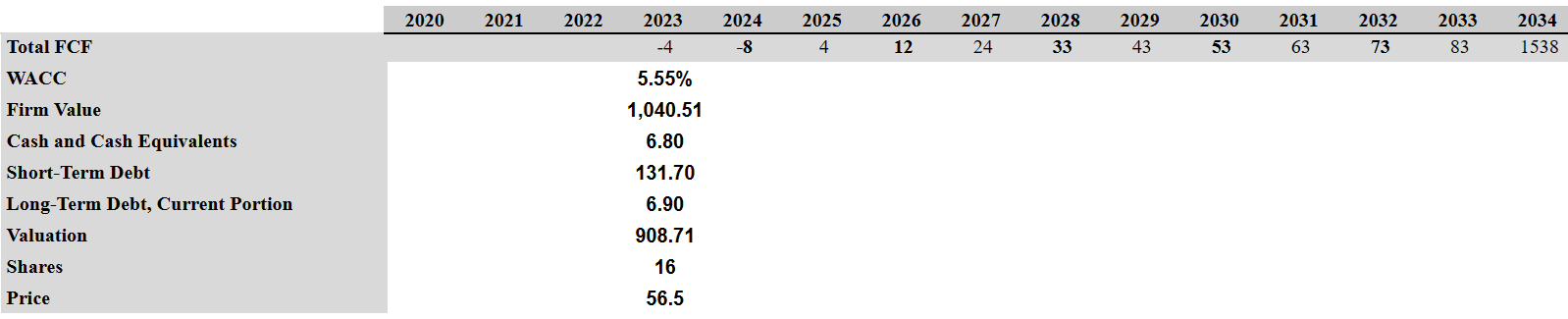

If we also assume EV/ 2034 FCF close to 15.5x and a WACC close to 5.5%, the implied firm value would be worth $1.04055 billion. If we add cash and cash equivalents close to $6 million, and subtract short-term debt worth $131 million and long-term debt close to $6 million, the implied valuation would be $908 million. Finally, the implied price would stand at $56.5 per share.

{kind=link}

The Company Does Not Have A Lot Of Direct Competition

As mentioned earlier, due to the nature of these markets, competition is not direct. However, in the case of Unitil, the possibility that the companies from which it distributes its energy develop their own distribution pipelines could generate adverse effects in the future. Let us remember that part of the natural gas segment is coordinated with a state company, which ensures a series of operations in the regions where it is currently present.

It is good to know that during 2001 a series of laws were voted which forced the deregulation of electric power in some states. Resultantly, electricity generating companies will close their facilities and will remain solely as distributors of energy produced in other centers. The same is true for natural gas, where Unitil alone operates as a distributor. This means that the company does not have direct competition or a market environment with other participants in the regions in which it is present.

Risks

The condition of this type of business has a series of risks linked to its nature: dependence on third-party services, temporary demand, price regulations, market shares, lack of competition, and the relationship between the purchase price and the sale price of energy. In addition, the inability to retain existing customers or to get new customers plays a fundamental role in the development of the company.

In this sense, the appearance of new technologies for the generation and supply of energy, especially electrical energy, represents a high risk factor with regard to its customers. The regulations not only cover the collection rates and income of its subsidiaries, but also apply to future environmental regulations that may exist in any of the regions in which the company develops its activities.

We can also add a situation of financial inconsistency that may disable the company to carry out its plans to modernize the Fitchburg silver as well as the decoupling of its two segments, which would seriously affect its operating and financial performance.

Conclusion

Unitil Corporation has delivered dividend growth for the last 19 years, continuous investment in infrastructure, and more customer growth. The company also enjoys economic growth, including new building permits and construction employment in Maine and New Hampshire. These factors will most likely lead to net income growth and perhaps FCF growth. Even considering some risks from failed modernization plans or lower demand for gas, under conservative assumptions, I designed a DCF model, which implied some upside potential in the Unitil Corporation stock price.

For further details see:

Unitil Corporation: Conservative Play With EPS Growth Expected, And Undervalued