UEIC - Universal Electronics: A High-Risk/High-Reward Turnaround Play

2024-01-09 01:35:06 ET

Summary

- Sales have decreased significantly since 2020 and are expected to decline again in 2024.

- Profit margins are currently depressed due to lower volumes and inflationary pressures.

- The company now plans to expand its presence in the HVAC industry to replace lost sales in the video services industry.

- The balance sheet is robust, as the company has enough resources to withstand current headwinds for a long time.

- The recent share price decline represents a good opportunity for those investors with enough patience and risk tolerance.

Investment thesis

Although it was a trend that had already been expected before the coronavirus pandemic, Universal Electronics ( UEIC ) did not expect the demand for its remote control products for video-service customers to decrease as rapidly as it did in the 2020-2023 period. Added to this are the recent (and current) high inflation rates, which have significantly impacted the purchasing power of many households around the world, pushing them to postpone the purchase of discretionary goods. Additionally, increased production costs and unabsorbed labor due to lower volumes have caused a collapse in profit margins, pushing the EBITDA margin into negative territory and forcing the company to report negative income for 4 consecutive quarters. That is why it is not surprising that the share price has fallen by 89% from all-time highs reached in 2016.

Although I do not expect the company's business of remote controls for video services to cease anytime soon, it is quite likely that the sales of these products will increasingly have less weight in the company as a whole until becoming just another business. Now, most of the company's efforts are focused on expanding its footprint in the HVAC (heating, ventilation, and air conditioning) industry while trying to cushion the decline in sales in the video services industry through partnerships with emerging streaming services.

Certainly, the global HVAC market is poised to grow at very generous rates in the coming years, and the company has been operating in the industry for more than 10 years, so the revenue growth potential is there. Additionally, the company is still rightsizing production capacity to operate more efficiently in the face of current low demand, so profit margins should begin to stabilize once its efforts to expand in the HVAC industry translate into new projects won by the company. For these reasons, I consider that the current pessimism prevailing in the market towards the company represents a good opportunity for those investors with enough risk tolerance to wait for the company's prospects to improve since the upside potential is significant.

A brief overview of the company

Universal Electronics is a global manufacturer of control and sensor technology solutions, as well as universal control systems, audio-video accessories, and wireless security and smart home products. The company was founded in 1986 and its market cap currently stands at $114 million (although it reached $1 billion in 2016) as it employs over 4,000 workers worldwide.

Universal Electronics logo (Uei.com)

The company's products are used by leading technology brands operating in a wide range of industries, including video services, consumer electronics, climate control, security, safety, home automation, and home appliances. These customers include Samsung Electronics ( SSNLF ), Sony Group Corporation ( SONY ), LG Electronics, Comcast Corporation ( CMCSA ), Liberty Global ( LBTYA ), Vodafone Group ( VOD ), Daikin Industries ( DKILF ), Vivint Smart Home, Somfy, Ring LLC, and Hunter Douglas, among others.

In recent years, customers operating in the video services industry for which the company manufactured remote controls have been losing customers due to the emergence of new key players, a trend that has accelerated with the arrival of the coronavirus pandemic in 2020, so the weight that sales of remote controls for HVAC systems have in the company's results is gaining prominence and will most likely continue to do so in the future.

Currently, shares are trading at $8.77, which represents an 89.08% decline from all-time highs of $80.42 reached in August 2016, which reflects great pessimism among investors as both sales and profit margins have been severely damaged in recent years due to changing consumer needs in the video-services market. In part, I consider that a significant part of the decline in sales could have been avoided if management had prioritized acquisitions over share buybacks as it spent $268 million in share repurchases since 2013, which is more than double the current market capitalization.

A lack of acquisitions has significantly limited revenue growth

Considering that the company has spent a total of $268 million in share repurchases since 2013, its acquisition history is very limited in comparison and is, in my opinion, one of the main reasons why the company has not yet found a (big enough) replacement for the loss of sales that it knew would end up arriving in the video-services industry once it was dominated by streaming services on the level of what we today know as Netflix ( NFLX ), Disney+ ( DIS ), Amazon's ( AMZN ) Prime Video, or Hulu. In fact, only two acquisitions took place in the past 10 years, and these were very small in size.

In August 2015, the company acquired Ecolink Intelligent Technology , a leading manufacturer of intelligent wireless security and home automation products, for $24.1 million, and almost two years later, in April 2017, the company acquired Residential Control Systems , a U.S.-based manufacturer of energy management and control products for the residential, small commercial, and hospitality markets, for $12.6 million.

In conclusion, it seems that the management has been more focused on rewarding shareholders through share buybacks than on growing (and diversifying) the business through new acquisitions, which is why today it is suffering a significant contraction in sales that has not yet been offset.

Revenues are expected to keep decreasing

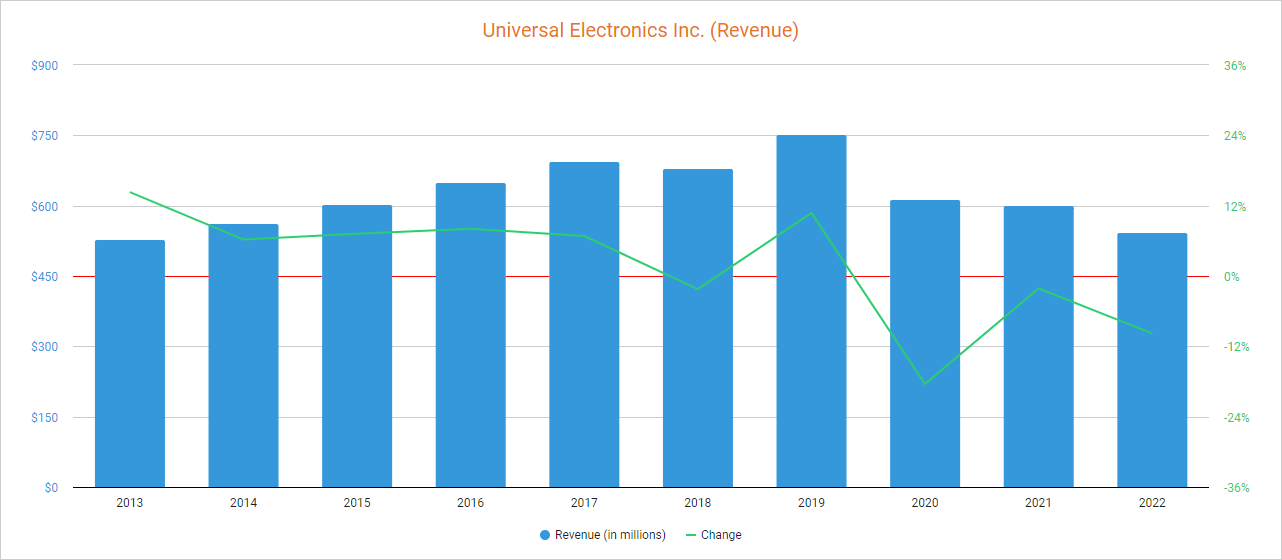

In the past, the company's sales steadily increased year after year until the coronavirus pandemic caused a decline of 18.42% in 2020 due to substantial subscriber losses in the company's video service customers, and the situation has continued to worsen in 2021 and 2022 as revenues again decreased by 2.13% and 9.78%, respectively.

{kind=link}

As for 2023, revenues decreased by 18.15% year over year in Q1, by 22.80% year over year in Q2, and by 27.87% year over year in Q3 to $107.1 million as the company's video service customers kept losing customers. In addition, high inflation rates have negatively affected the purchasing power of many households around the world, which tends to postpone the replacement of discretionary goods such as remote controls during difficult times. For this reason, 2023 is expected to close with revenues of $420 million, which would represent a ~23% decline compared to 2022, and 2024 is expected to bring another 4.2% drop to $402 million.

The company periodically launches new products on the market to maintain its leading position in the industries in which it operates and is now focusing on launching remote control products for the connected home industry (especially HVAC) while trying to win new customers in the video services business by marketing new control products for emerging streaming services in order to stop the decline in sales. Using 2022 as a reference, 31% of revenues are generated within the United States, whereas 24% are provided by operations in Asia (except China), 19% in Europe, 16% in China, 5% in Latin America, and 6% in the rest of the world, which means the company enjoys wide geographical diversification.

The global thermostat market size is expected to grow at a CAGR of 12.9% through 2032, and the company has been operating in the remote control thermostat industry for more than 10 years, which means that it has the opportunity to turn its business around if it figures out how to play its cards when it comes to finding new customers and winning new projects. In this regard, it has recently launched a new portfolio of thermostat controls for the North American and European markets, but its exposure in the industry is still limited. From the current trailing twelve months' revenues of $445.6 million, less than $100 million are provided by climate control products, so less than 25% of the revenue comes from these products. Still, the management hopes to double these sales in the next few years.

But for now, the market expectation is that sales will continue to decline in 2024 and that a potential turnaround would be rather slow in the coming years, which is one of the main reasons (apart from the weakening profitability profile) that have caused a steep decline in the P/S ratio to 0.252, which means the company generates $3.97 in sales for each dollar held in shares by investors, annually.

This ratio is 75.75% lower than the average of the past 5 years and represents an 86.78% decline from the 1.906 peak reached in 2015 as investors are placing very little value on the company's sales not only because they are expected to continue falling and the recovery to be slow, but also because profit margins have collapsed as a result of lower volumes and inflationary pressures.

The company is currently unprofitable as profit margins remain depressed

Until very recently, both gross profit and EBITDA margins were more than acceptable as the company enjoyed gross profit margins that were usually above 25% and EBITDA margins that hovered around 8%, but inflationary pressures and declining volumes have recently caused a very worrying contraction as the trailing twelve months' gross profit margin currently stands at 22.87% whereas the EBITDA margin entered at negative territory and is currently at -1.86%. The company currently has excess manufacturing capacity as the drop in demand from video service customers has been so significant that the company has not yet had time to rightsize its production capacity, which is understandable because sales have continued to fall in recent quarters.

In this regard, the company seized operations in its southwestern China factory and moved production to Vietnam in June 2023, and manufacturing capacity in Mexico is expected to be reduced in the first half of 2024 to operate more efficiently. Both changes are expected to achieve savings of $15 million to $18 million per year once finished, but so far profit margins have continued deteriorating throughout 2023 as the company reported a gross profit margin of 19.06% in Q3 and an EBITDA margin of -4.20%, which is damaging the balance sheet as the company is paying over $15 million in annual capital expenditures and almost $5 million in annual interest expenses.

On a positive note, capital expenditures have decreased significantly from $40.7 million in 2016 to $10.7 million in the last 12 months, although this is nothing to praise considering the size of the business has also decreased. Nevertheless, this should help partially cushion the damage that current headwinds are having on the balance sheet, which thankfully remains robust.

The balance sheet is very strong, but it is deteriorating fast

In the last 10 years, the company has gone from being debt-free to holding $75 million in long-term debt. In turn, cash and equivalents have decreased from $76.2 million at the end of 2013 to $60 million today, which reflects a significant deterioration in the balance sheet.

Still, it should be said that the current $75 million in long-term debt represents a significant improvement compared to the $88 million it had when 2023 began, and this has been possible thanks to the $20.1 million of cash from operations generated through the use of accumulated inventories, which decreased by $46.7 million in the first nine months to $93.46 million. Considering that cash and equivalents currently stand at $60.08 million and that current inventories of $93.46 million are significantly higher than long-term debt of $75 million, the risk that debt represents for the company is very limited in the short and medium term.

Moreover, total receivables of $123 million are much higher than total payables of $54.78 million, which suggests that the company will continue to report stronger cash from operations in the coming quarters, which should serve to navigate the current headwinds and the ongoing transition stage while ideally slightly reducing long-term debt so that interest expenses do not represent a burden in the medium term. This is important because the recent surge in long-term debt, as well as rising interest rates, has caused a new spike in interest expenses, which have been $4.34 million in the last 12 months.

In addition, the company reported total interest expenses of $1.22 million in Q3 2023, so it is expected to bear almost $5 million in annual expenses from now on. Therefore, investors need to keep in mind that interest expenses could continue to increase if sales do not return to the growth path in the medium term and if profit margins do not stabilize soon as the company's balance sheet could continue to deteriorate to the point where the company could be forced to make more use of debt, which would mean entering a dangerous circle.

Share buybacks are to blame for the current situation

Over the past few years, the management has performed regular share buybacks to reward shareholders as the company has never paid dividends. The initial idea was to improve per-share metrics thanks to a continuous reduction in the number of shares in circulation, and although it is true that the size of the company that each share represents has increased in recent years (as the number of shares outstanding has decreased by 18.49% in the last 10 years), the truth is that this has not compensated for the company's weakening results as a whole.

The impact that such aggressive buybacks have had on the company's evolution, in the sense that these resources could have been allocated to other items such as acquisitions and innovation efforts, is better understood when we put a number on it, and that is that the company has spent $268 million in stock buybacks since 2013 while the current market capitalization stands at just $114 million.

Now, the management has recently authorized a new share repurchase program of up to 1 million more shares, which has already started and would have a total cost of ~$8.8 million if fully completed, which is, in my opinion, a mistake at this point as the company truly need these resources to navigate current headwinds with enough room for maneuver. In part, I understand the management's intention to take advantage of the recent drop in the share price by reducing the total number of outstanding shares by over 7% by investing a relatively low amount of cash, but I believe that investing these resources in the expansion of the HVAC business would have greater value for shareholders in the long term.

Risks worth mentioning

In my opinion, Universal Electronics has many strengths thanks to a robust balance sheet whose cash and equivalents are almost higher than long-term debt, not counting high inventories and accounts receivables. Even so, I consider that despite the enormous upside potential, this is a highly speculative investment since not only is it a company that has historically been cyclical, but it is currently in the midst of a reorganization process that will change the weight that various industries have in sales as a consequence of recent changes in consumer needs. Therefore, below I have highlighted those risks that I consider most significant, especially for the short and medium term.

- Recent interest rate hikes could trigger a global recession, which could not only have a negative impact on revenues but would likely also cause a further contraction in profit margins due to even more unabsorbed labor as a consequence of declining volumes.

- The company could fail to penetrate the HVAC industry as much as it intends, which would derail current plans to reverse the negative sales trend it has experienced since 2020.

- Sales in the video services industry could continue to decline beyond 2024, even at a faster rate than the sales growth expected in other businesses, which would further deteriorate its operations.

- Current efforts to reduce production capacity in order to operate more efficiently may not have the desired results, resulting in profit margins taking longer than expected to recover, causing further damage to the balance sheet.

- Profit margins could be negatively impacted if inflationary pressures intensify again.

- The company is currently in a position of survival while efforts to increase its manufacturing efficiency and to expand in the HVAC industry bear fruit, and although its resources are very extensive thanks to high cash and equivalents, inventories, and accounts receivables, it could be forced to make more use of debt if sales and profit margins do not eventually improve.

Conclusion

Investing in Universal Electronics today means trusting that the company will be able to absorb a significant part of the expected growth in global demand for HVAC products, as well as in its ability to win new customers and projects in the video services industry in order to cushion ongoing revenue declines for its video services remote control products and thus be able to continue operating in the industry in the long term. Luckily, the company has been operating for over 10 years in the HVAC industry, and therefore, it already has a presence and has the potential to expand its footprint, and the management expects to double HVAC revenues in the foreseeable future.

At this point, it is prudent to affirm that share buybacks carried out in recent years represented a misuse of cash as the company could have used all those resources on other items such as acquisitions or innovation efforts, and shareholders are now paying the price. Profit margins have continued to worsen as volumes continued declining, and the balance sheet is deteriorating as the EBITDA margin entered negative territory in 2023 with no recovery signs so far. Furthermore, the management has decided to risk an additional ~$8 million in cash to buy back shares at very low share prices to boost the potential upside in the medium term, which has the potential to do so but not without risks involved.

Despite all these bad news, the balance sheet is very robust thanks to high cash and equivalents, inventories, and receivables, and efficiency efforts are already underway as the company is resizing its manufacturing capacity, which should help in boosting profit margins starting in H2 2024. Although sales may take time to recover, the truth is that, in my opinion, the company has enough resources to withstand the current headwinds for much longer, so prospects should improve as the company gains new customers and contracts in the HVAC industry, and sales of remote controls for video services companies should stabilize at some point as I don't expect the company to stop operating in the industry anytime soon. For these reasons, I consider that the 89% share price decline from all-time highs represents a good opportunity for those investors with enough patience and risk tolerance to wait for current plans to materialize in the form of better prospects since the upside potential is significant.

For further details see:

Universal Electronics: A High-Risk/High-Reward Turnaround Play