UHT - Universal Health Realty: An Undervalued 6% Yield

Summary

- UHT has high exposure to Medical Office buildings and has a long track record of raising its dividend.

- It should benefit from long-term demographic tailwinds with growing healthcare spend.

- The current valuation presents an attractive entry point for income investors.

The past 12 months have been tumultuous for REITs, to say the least, with ones like Medical Properties Trust ( MPW ) and Omega Healthcare ( OHI ) seeing plenty of negative market sentiment in the healthcare segment.

Not all REITs are created equal, however, and this brings me to Universal Health Realty Income Trust ( UHT ), which may be a better choice for investors seeking less headline risk combined with a high yield. As shown below, UHT has also traded down over the past year, and in this article, I highlight what makes UHT a good value pick at the current price.

{kind=link}

Why UHT?

UHT is a self-managed REIT that specializes in owning and leasing healthcare properties across the U.S., including hospitals, medical office buildings, and rehabilitation centers. It's headquartered in Pennsylvania and was formed back in 1986, when it bought properties from subsidiaries of hospital operator Universal Health Services ( UHS ). Today, UHT has a diversified presence across 21 states in well-populated areas in the Northeastern, Sunbelt, Midwestern, and Western regions, as shown below.

{kind=link}

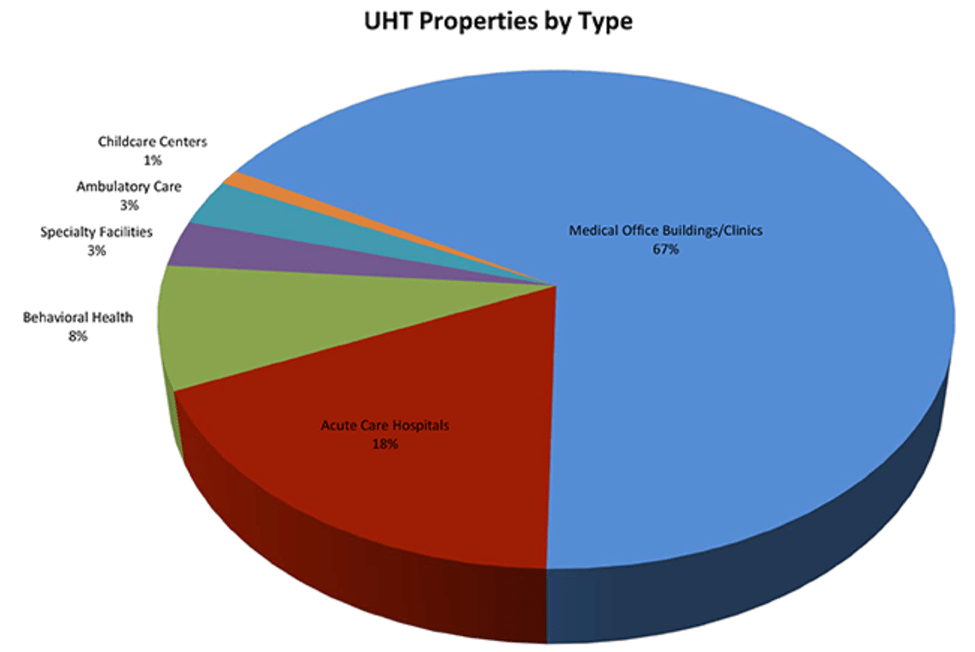

What differentiates UHT from other diversified healthcare REITs such as Ventas ( VTR ) and Welltower ( WELL ) is its higher exposure to Medical Office Buildings. This is arguably the highest quality asset class in the healthcare space, because it's not labor-intensive like skilled nursing facilities and assisted living, and hence its tenants are not exposed to high cost inflation. Moreover, MOBs are benefitting from a shift in patient services from hospitals to an outpatient setting. As shown below, MOBs comprise two-thirds of UHT's total underlying property value.

{kind=link}

Meanwhile, UHT saw topline revenue grow by 4.5% YoY to $22.2 million in the third quarter, and by 6% YoY for the first nine months of 2022. However, the company is being weighed down by higher interest expense of $2.8 million during Q3 compared to $2.25 million in the prior year period. This contributed to FFO per share declining by 6 cents YoY to $0.86.

Nonetheless, UHT's $0.715 quarterly dividend remains well covered by an 83% payout ratio. Moreover, while UHT's dividend growth isn't high, it has increased its dividend every year since 1991. As shown below, the yield is currently sitting at one of its highest levels over the past decade.

(Note: the following table shows TTM dividend yield while the forward yield is 5.9%)

{kind=link}

Risks to UHT include unpredictability of Covid's trajectory, which may lead to higher hospitalizations that may include non-insured patients. Moreover, while UHT has diversified its property base over the years, it still remains highly associated with UHS, which represents 41% of UHT's consolidated revenue.

This risk is mitigated by the master lease structure, which protects leases at the property level. In addition, UHS carries a BB+ credit rating, just one notch below investment grade, and leases are generally considered to be an operating expense, so lease payments can be allowed to continue in the worst-case event of a tenant bankruptcy.

Notably, UHT maintains a strong balance sheet, with a net debt to EBITDA ratio of 5.98x, sitting just under the 6.0x level generally deemed safe by ratings agencies. In addition, I see plenty of long-term value in UHT's properties given their essential nature and the favorable demographic trends, with the age 65+ group being the fastest-growing population segment.

According to CMS, U.S. national healthcare expenditures are expected to grow at a faster rate than GDP and represent 20% of GDP by 2028. On a dollar-for-dollar comparison, healthcare spend is expected to rise at a 6% CAGR over the next six years. UHT should be well positioned to benefit from this trend, as most of its properties are located in warmer climates, which are expected to attract a disproportionate share of retirees over the next decade.

Turning to valuation, UHT appears to be attractive at the current price of $48.51 with an annualized P/FFO of 14.1, sitting below its normal P/FFO of 16.2 over the past decade. A reversion to the mean valuation could translate to a potential 21% total return including dividends.

Investor Takeaway

UHT offers investors a diversified healthcare real estate portfolio with high exposure to Medical Office Buildings, a reasonably strong balance sheet, and an attractive dividend yield. With a valuation below its historical average, UHT represents an attractive long-term investment opportunity that should benefit from favorable demographic trends and the growth of healthcare spend in the U.S.

For further details see:

Universal Health Realty: An Undervalued 6% Yield