UHT - Universal Health Realty: Decent Income At A Great Price

2023-04-14 08:05:00 ET

Summary

- Universal Health Realty's asset base is mostly comprised of safer Medical Office Buildings.

- UHT pays a well-covered dividend and carries a strong balance sheet.

- Recent share price weakness presents a nice opportunity for income investors.

Higher interest rates have given many investors pause around high yielding stocks, considering that there are plenty of fixed income alternatives available. However, it's worth asking how durable that fixed income yield really is. For example, those who bought Treasury I Bonds last year are finding that their interest rate will fall to an estimated 3.8% next month, due to lower inflation.

That's why it may still be worth sticking to equities, which have more long-term upside potential. This brings me to Universal Health Realty Income Trust ( UHT ), which I last covered near the start of the year here . UHT is back to yielding 6.1% and in this article, I highlight recent developments and why income investors may want to consider the stock at present levels.

Why UHT?

UHT is an internally-managed REIT that owns hospitals, medical office buildings, and rehabilitation centers across the U.S. It was founded back in 1986 and at present, has 76 property investments across 21 states in the Northeast/Mid-Atlantic, Midwest, Sunbelt (including Texas) and Southwest (Nevada, Arizona, and Southern California).

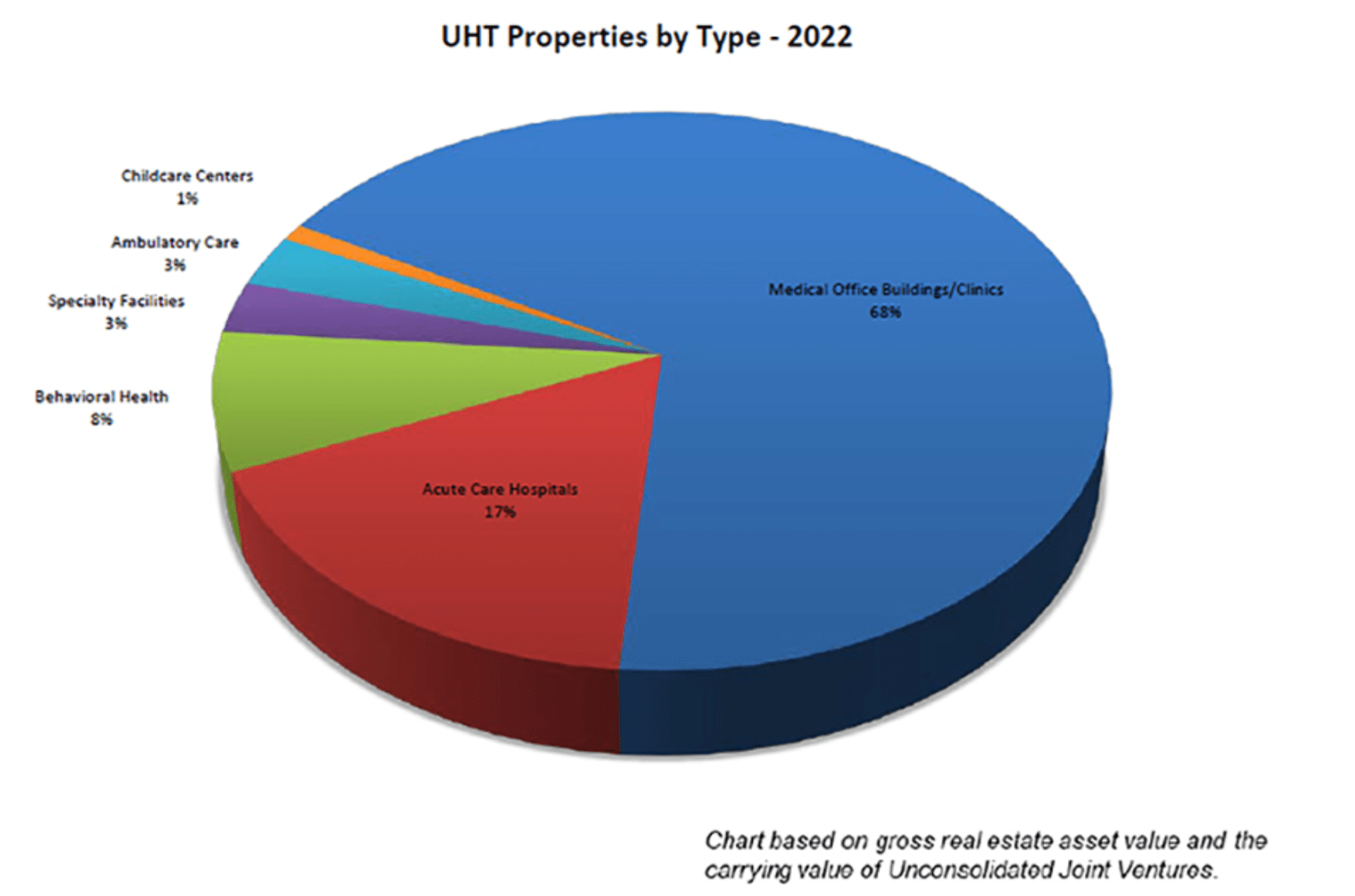

As shown below, UHT's main focus is medical office buildings, which represent 68% of its gross asset value, with the remainder falling to acute care hospitals, behavioral health, and specialty/ambulatory care facilities.

{kind=link}

Medical office buildings are generally viewed as being the safest healthcare asset class. This is considering the tenant troubles that senior housing and skilled nursing landlords like Ventas ( VTR ), Omega Healthcare Investors ( OHI ) have experienced in recent years.

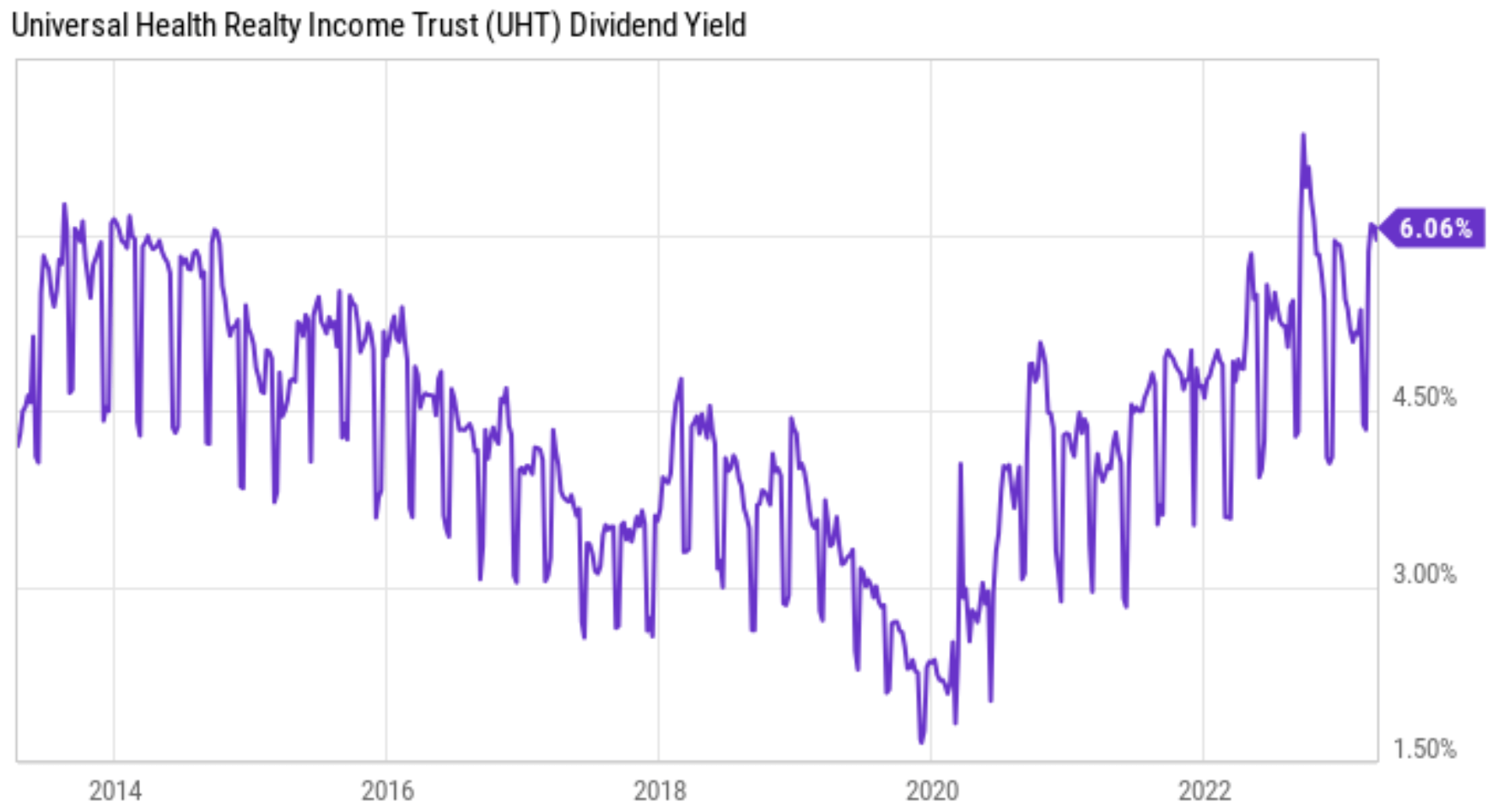

Meanwhile, UHT closed out a strong year in 2022, generating $3.54 in FFO per share. This enabled management to raise the dividend twice last year to the forward annual rate of $2.86 per share. This forward rate is also well covered at an 81% payout ratio. As shown below, UHT's 6.1% dividend yield is currently at one of its highest levels over the past 10 years.

{kind=link}

While UHT's FFO/share did decline from $3.69 in the prior year, this had to do with lower depreciation and amortization expense on consolidated and unconsolidated ventures rather than troubles in the underlying business. Despite a difficult environment for healthcare tenants, UHT still managed to grow its rent on renewed leases by 2% last year.

It's also worth noting that UHT, like other REITs, are feeling the effects of higher interest rates. This includes interest expense rising by $1.9 million last year. Doing back of the envelope math, this comes to a $0.14 impact on a per share basis. I don't see reason to be overly concerned, as UHT maintains plenty of buffer between its $2.86 per share dividend and $3.54 FFO per share. Moreover, the March CPI report showed inflation coming in at 5% , the lowest in two years. This, combined with recent regional bank failures, leads to the potential for a steadier interest rate environment going forward.

Importantly, UHT maintains plenty of balance sheet strength, with fixed charge coverage ratio of 4.3x, sitting well above the 1.5x covenant requirement, and a total leverage of just 43%, sitting well under the 60% or less covenant. The bond market doesn't appear to be concerned with UHT's debt, as UHT's borrowing terms appear under its credit facility appear to be favorable, at just LIBOR plus a margin range from just 1.1% to 1.35%.

Turning to valuation, UHT appears to be in value territory at the current price of $47.11 with a P/FFO of 13.3. Considering UHT's quality asset base and 19 consecutive years of dividend growth, I don't think it's unreasonable for UHT to return to a P/FFO of 15x. Meanwhile, investors get paid a safe 6.1% yield for holding onto this quality REIT.

Investor Takeaway

Investments in fixed income securities come with reinvestment risk, and the lower yields now on Treasury I Bonds is one such example. That's why it may pay to have a basket of quality income stocks and UHT is a healthcare REIT that may appeal to income investors. It owns a diversified asset base and has demonstrated an ability to grow its dividend, even during difficult environments. Furthermore, the recent pullback in the stock price from the mid-50s level in February combine with 6%+ dividend yield makes UHT worth considering for income investors.

For further details see:

Universal Health Realty: Decent Income At A Great Price