HCA - Universal Health Services: Attractive Even In Light Of Cost Concerns

Summary

- Universal Health Services continues to grow its topline nicely, but bottom line results have been discouraging this year.

- This is problematic, but this doesn't mean the company isn't worth considering.

- Given how shares are priced, there does seem to be some nice upside moving forward.

During difficult times, one area that you might think would be stable would be the healthcare space. After all, the industry addresses issues that we all have from time to time, creating essentially a permanent level of demand that should exist. But just like any other industry in the economy that has grown to any significant size, the healthcare space is more complicated than that. At the end of the day, it's not just about the revenue that can be generated. Profits are also important, and those can change materially based on market conditions. One company that makes for a good demonstration on this front is Universal Health Services ( UHS ), an enterprise that owns and manages various healthcare facilities. Generally speaking, I have been rather bullish about Universal Health Services, but the picture most recently has been somewhat mixed. Revenue continues to climb, but declining profits have become an issue. Even with that, though, the patient investor should find a lot about the company to enjoy. Growth continues, and shares of the enterprise are trading at fundamentally cheap levels. So while the company does have its issues right now, I do think that it still warrants a solid 'buy' rating, reflecting my belief that it should outperform the broader market for the foreseeable future.

Patience is required

Back in early March of this year, I wrote an article detailing the investment worthiness of Universal Health Services. In that article, I found myself encouraged by the company's revenue and cash flow growth. Even back then, I concluded that, from a profitability perspective, the 2022 fiscal year might be somewhat challenging for the company. But on the whole, I felt as though shares were cheap enough to warrant upside moving forward. This led me to keep the company a 'buy' like I had it rated previously. Since then, however, shares have not performed exactly as I would have anticipated. While the S&P 500 is down by 6.1%, shares of Universal Health Services have generated a loss for investors of 16%.

{kind=link}

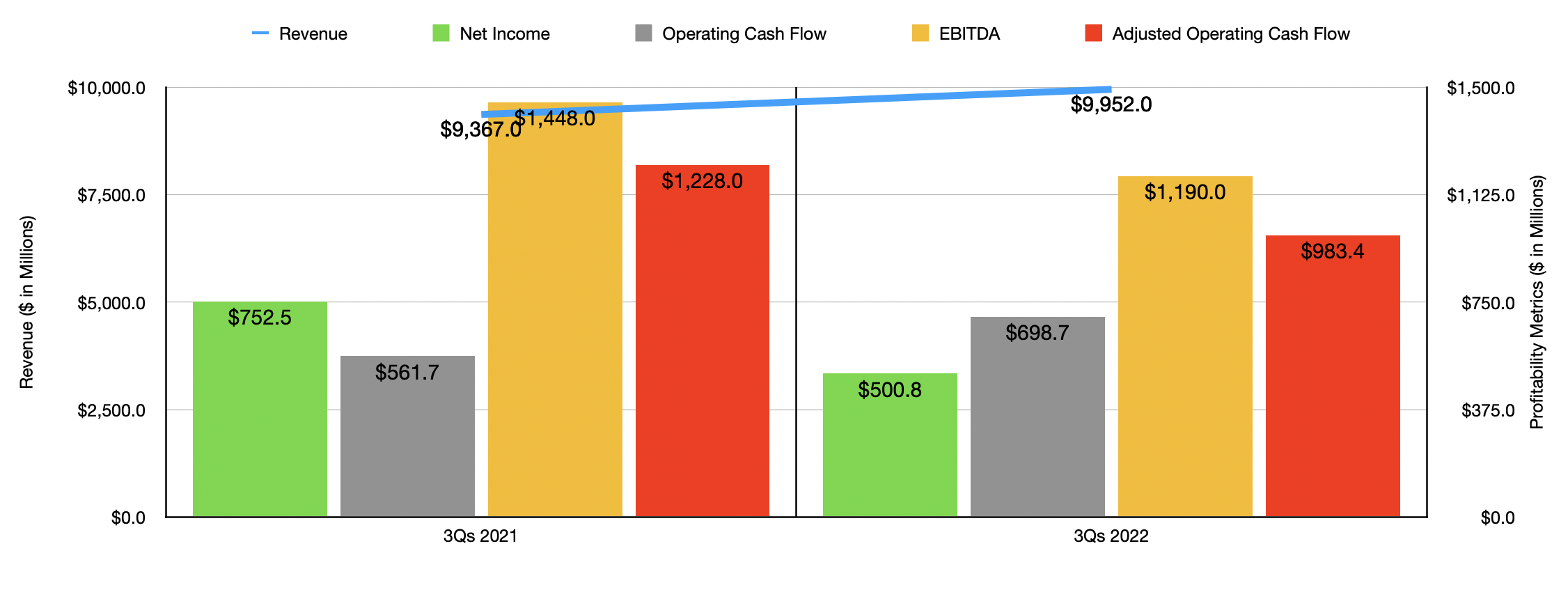

When I last wrote about the company, we had data covering through the 2021 fiscal year. Fast-forward to today, and we now have data covering through the first three quarters of 2022 . During this time, a lot has transpired. For the first nine months of the 2022 fiscal year in their entirety, revenue came in at $9.95 billion. That's 6.2% higher than the $9.37 billion generated one year earlier. This increase was driven largely by a couple of different factors. The most significant was a $400 million increase in net revenue generated from its acute care hospital services and behavioral health services business. According to management, this rise was driven by a variety of factors, including a 1% increase in net revenue per adjusted admission and a 2.6% increase per adjusted patient day. The company also benefited from a $186 million increase caused by other miscellaneous factors that they did not disclose.

With the rise in revenue, you might think that the company was due for a rise in profitability as well. Sadly, you would be mistaken. Net income in the first nine months of this year totaled $500.8 million. That's down from the $752.5 million reported one year earlier. At the end of the day, there were two key drivers behind decreased profits. The first of these was a rise in salaries, wages, and benefits, from 48.5% of sales to 50.9%. The second was an increase in other operating expenses from 23.8% of sales to 25.4%. Clearly, inflationary pressures have negatively affected the firm. Other profitability metrics sadly followed suit. Although operating cash flow rose from $561.7 million to $698.7 million, the adjusted figure for this, which ignores changes in working capital, dropped from $1.23 billion to $983.4 million. Meanwhile, EBITDA for the company also worsened, falling from $1.45 billion to $1.19 billion.

{kind=link}

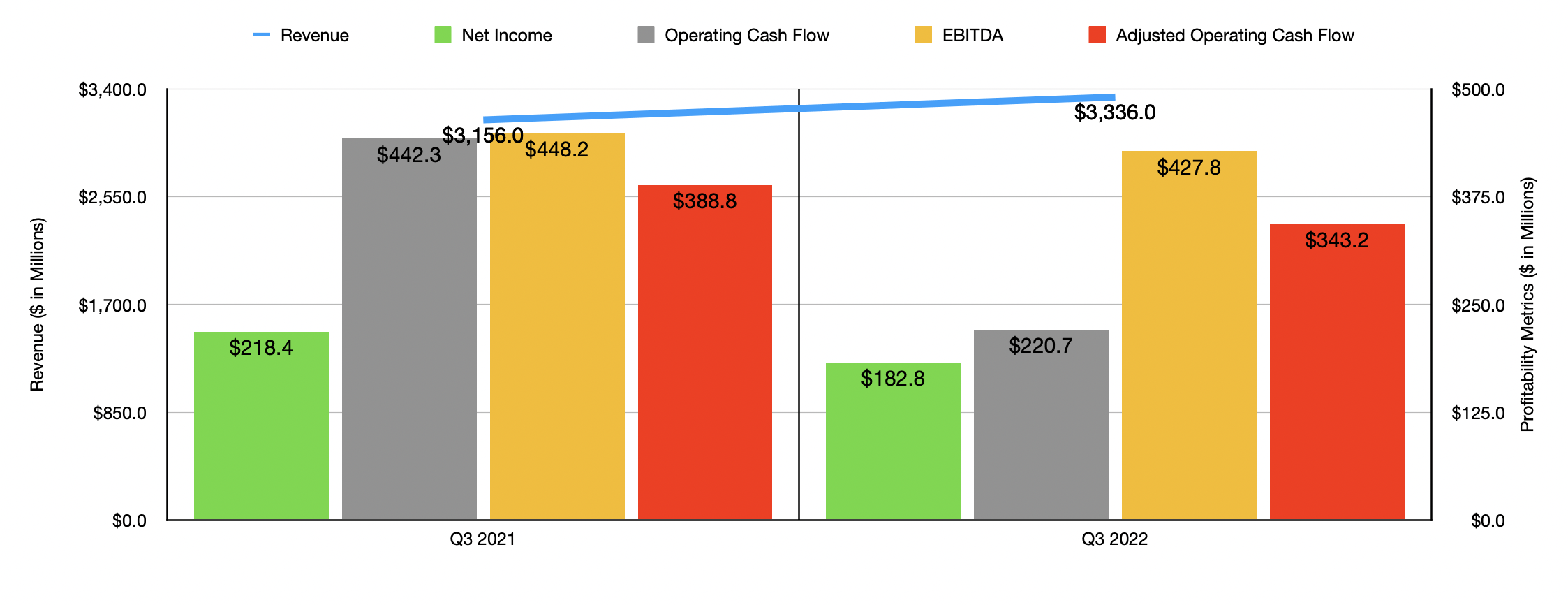

Ideally, the company should see these issues abate over time. But so far, that has not transpired. Take the third quarter of the 2022 fiscal year on its own. Once again, revenue is higher year over year, having risen 5.7% from $3.16 billion to $3.34 billion. At the same time, however, profits are on the decline. Net income dropped from $218.4 million to $182.8 million. Operating cash flow fell from $442.3 million to $220.7 million, while the adjusted figure for this dropped from $388.8 million to $343.2 million. Over that same window of time, even EBITDA worsened, falling from $448.2 million to $427.8 million.

{kind=link}

When it comes to the 2022 fiscal year as a whole, management expects revenue to come in at between $13.235 billion and $13.371 billion. If this comes to fruition, it would translate to a nice increase over the $12.64 billion generated in 2021. Earnings per share, though, should come in at between $9.60 and $10.40. At the midpoint, that would translate to net income of $730.6 million. Meanwhile, EBITDA is forecasted to come in at between $1.64 billion and $1.71 billion. At the midpoint, that would translate to adjusted operating cash flow of around $1.30 billion. Taking these figures, I calculated that the company is trading at a forward price to earnings multiple of 11.9, at a forward price to adjusted operating cash flow multiple of 6.7, and at a forward EV to EBITDA multiple of 8.6. As you can see in the chart above, these are all higher than what we would get if we valued the company using data from 2021. Relative to similar players, shares do look to be more or less fairly valued, though. On a price-to-earnings basis, the five companies I compared it to ranged from a low of 1.8 to a high of 26. Using the price to operating cash flow approach, the range was between 3.6 and 20.2. In both cases, two of the five were cheaper than Universal Health Services. Meanwhile, using the EV to EBITDA approach, the range was between 6.7 and 15.5, with three of the five companies being cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Universal Health Services |

| 11.9 |

| 6.7 |

| 8.6 |

| HCA Healthcare ( HCA ) |

| 12.7 |

| 8.0 |

| 8.3 |

| Ensign Group ( ENSG ) |

| 25.7 |

| 17.7 |

| 14.8 |

| Acadia Healthcare Company ( ACHC ) |

| 26.0 |

| 20.2 |

| 15.5 |

| Tenet Healthcare ( THC ) |

| 8.6 |

| 4.7 |

| 6.7 |

| Community Health Systems ( CYH ) |

| 1.8 |

| 3.6 |

| 7.7 |

Takeaway

Clear Lake, the last several months have not been particularly pleasant for shareholders of Universal Health Services. Rising costs are more than offsetting increased revenue. In the near term, this is problematic, but it's unclear what the end result will be. Even if this issue persists, though, the stock does look to be attractively priced on an absolute basis, even though it might be closer to fair value compared to similar players. Given this pricing and the continued revenue growth, I still do think the company warrants a 'buy' rating, even though I am no longer as optimistic about it as I was when I last wrote about it.

For further details see:

Universal Health Services: Attractive Even In Light Of Cost Concerns