UVE - Universal Insurance Holdings: A Stronghold In A Stormy Market

Summary

- Universal Insurance Holdings, Inc. has been through another tough second half.

- Its fundamental stability remains one of its cornerstones.

- While it maintains a solid financial positioning, the market remains problematic.

- Well-covered dividend payments increase with exciting yields.

- The stock price remains low and sideways.

It's been a while since I last covered Universal Insurance Holdings, Inc. (UVE). For the past months, I got worried about the continued insurance exodus in Florida. Hurricane Ian was another challenge that hit the P&C insurance market in the state. But the company proves its resilience amidst these adversities. It keeps its revenue growing despite the lower policies in force. It incurred net losses due to a surge in claims, but operating expenses remain under control. Even better, it maintains a stellar Balance Sheet, allowing it to cover insurance liabilities and borrowings.

Moreover, dividends are still increasing with attractive yields. The stock price remains low and almost unchanged from my last coverage. Nevertheless, its pattern may open an entry point for investors.

Company Performance

Universal Insurance Holdings, Inc. operates in a highly volatile and hammered market. Florida is one of the states needing P&C insurance due to its higher exposure to natural calamities. It is no surprise that the demand for P&C insurance providers is higher. However, it also means higher claims due to hurricanes and roofing scams that pulverized it in recent years. In my previous coverage, an insurance exodus in Florida has intensified, leading to five more liquidations in 2022. Let’s face it, the Florida market is stumbling as insurers grapple with litigation costs and insurance claims. The massive damages left by Hurricane Ian further aggravated the situation. Despite this, I am optimistic about UVE navigating this tough market.

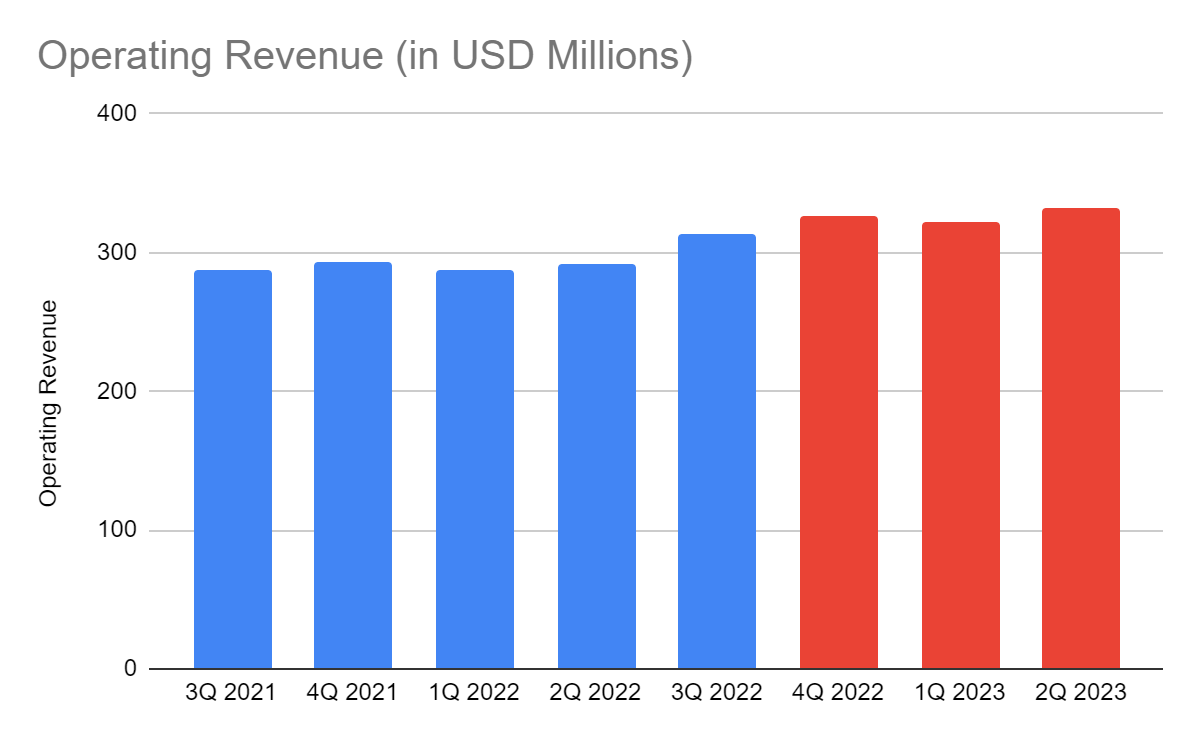

The operating revenue of the company amounts to $312.81, a 9% year-over-year growth. Various factors drove this decent growth. First, UVE maintains a strategic pricing strategy. Once again, many Florida homeowners rely on P&C insurance. But right now, insurers like UVE have become stricter with their underwriting policies due to abuses in litigation and benefits assignments. We have seen its impact in the decreased policies in force in 2022.

Operating Revenue (MarketWatch And Author Estimation)

{kind=link}

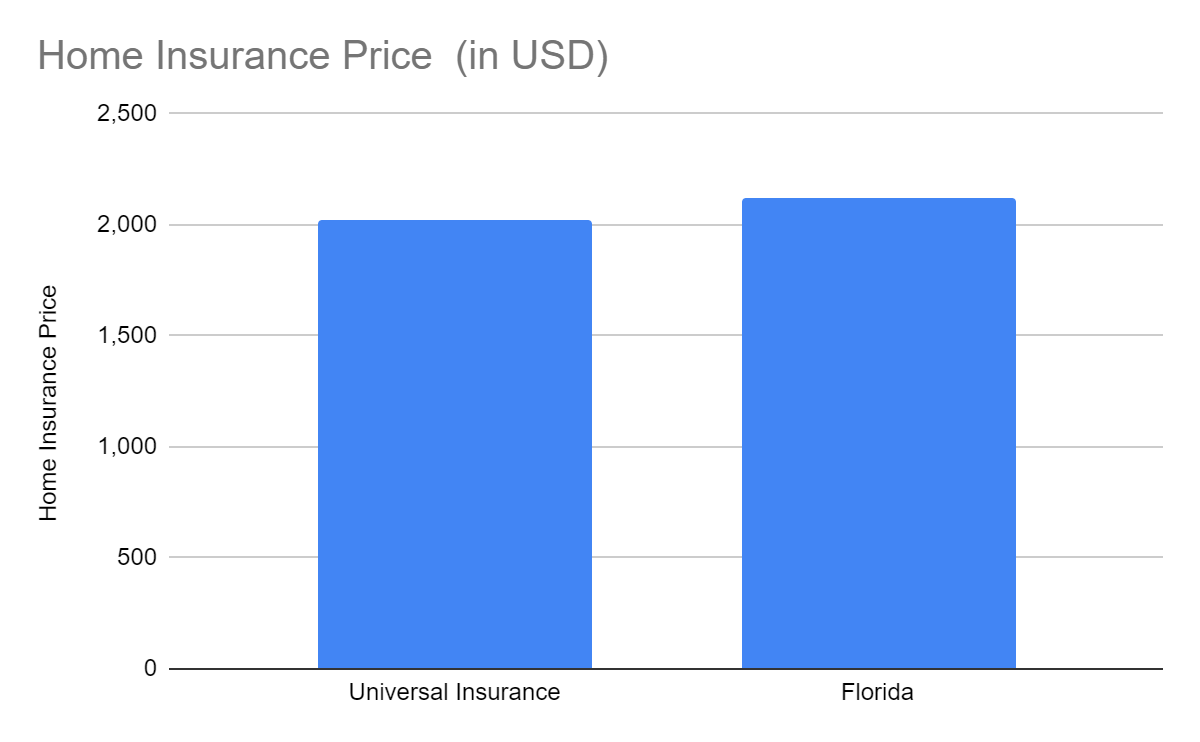

But thankfully, its adjusted prices are more than enough to make up for non-renewals. Also, property prices and mortgages keep increasing despite the recent cooling of sales. With higher value, more property protection is needed by the owners. Even better, its average premium rate of $2,019 is lower and more flexible than the state average.

Home insurance Price (NerdWallet)

{kind=link}

Second, UVE maintains its prudent portfolio diversification. Its investment securities combine corporate bonds, equities, and government-backed securities. Government-backed securities are the most favorable investments, given their inflation-linked nature. Corporate and mortgage bonds can be risky today, but they work, given the continued property appreciation. Also, inflation stays in a lull, making their yields more stable.

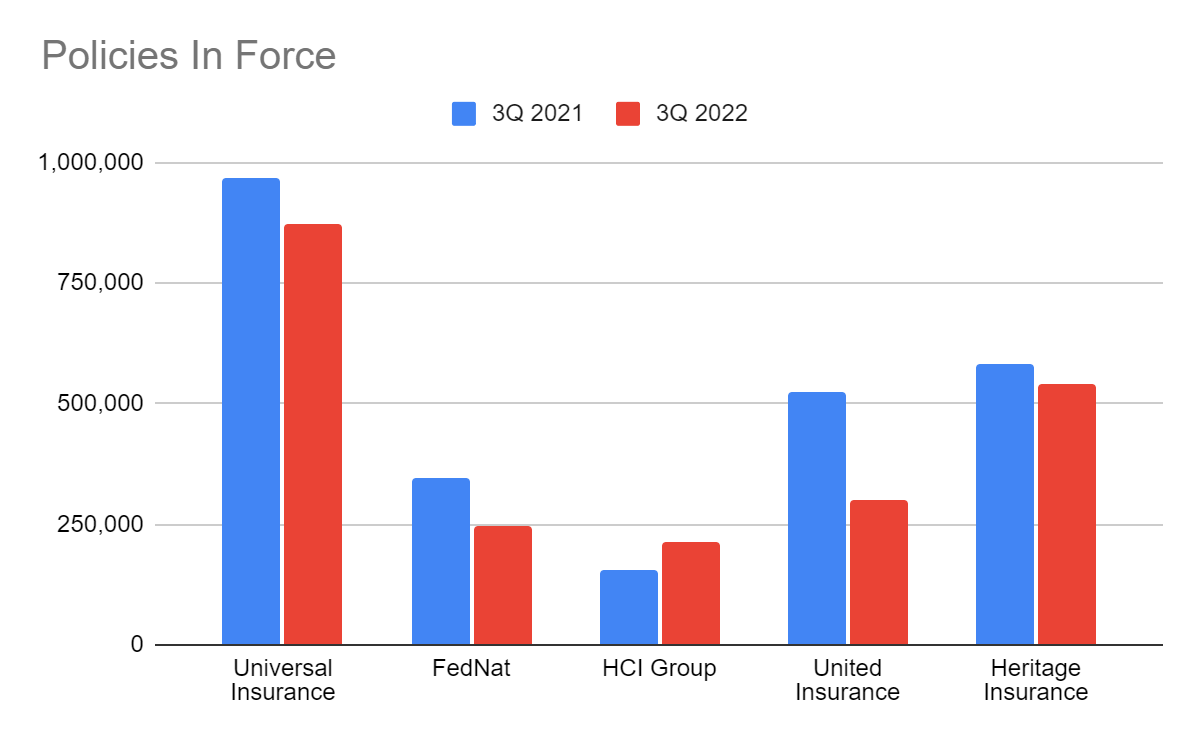

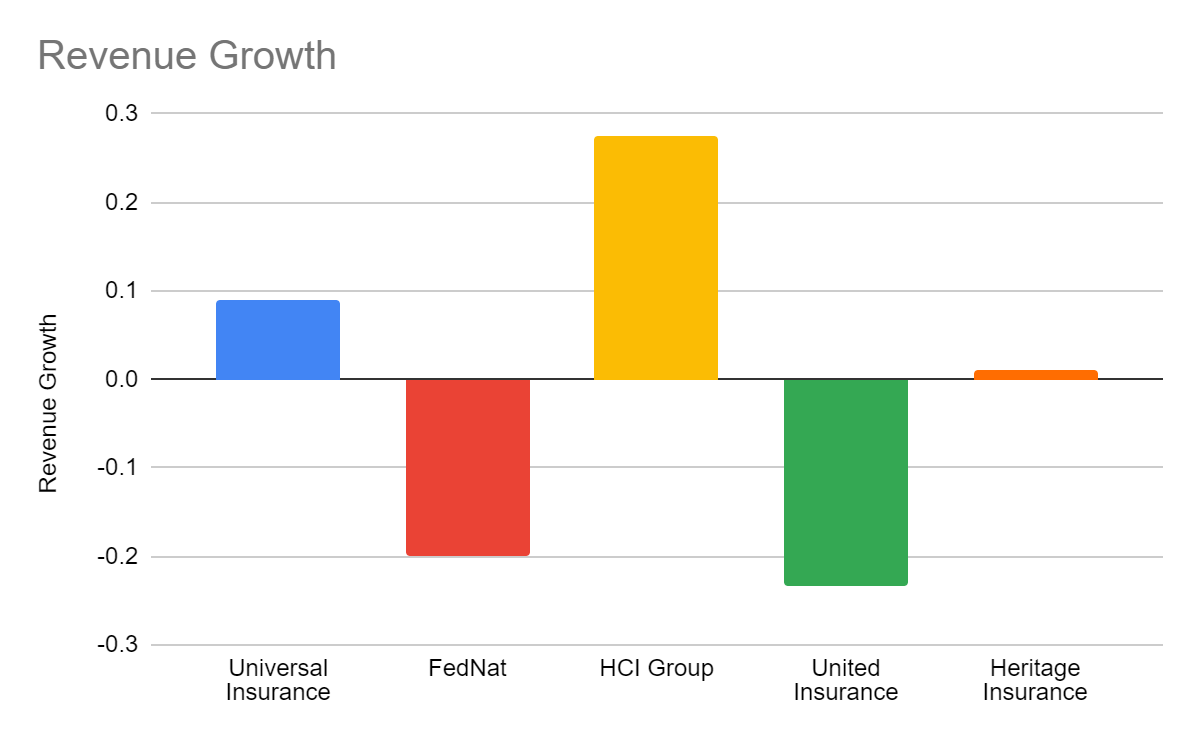

With regards to its close Florida peers, UVE remains a giant. It holds the largest number of policies in force even after the 10% decrease. Only HCI Group ( HCI ) had increased policies in force, which led to its 24% revenue growth. UVE comes far second with 9%. But it shows that UVE sets the most strategic pricing among these insurers.

Policies In Force (SEC EDGAR 3Q Filings, FedNat 1Q Filing ) Revenue Growth (MarketWatch)

{kind=link}

{kind=link}

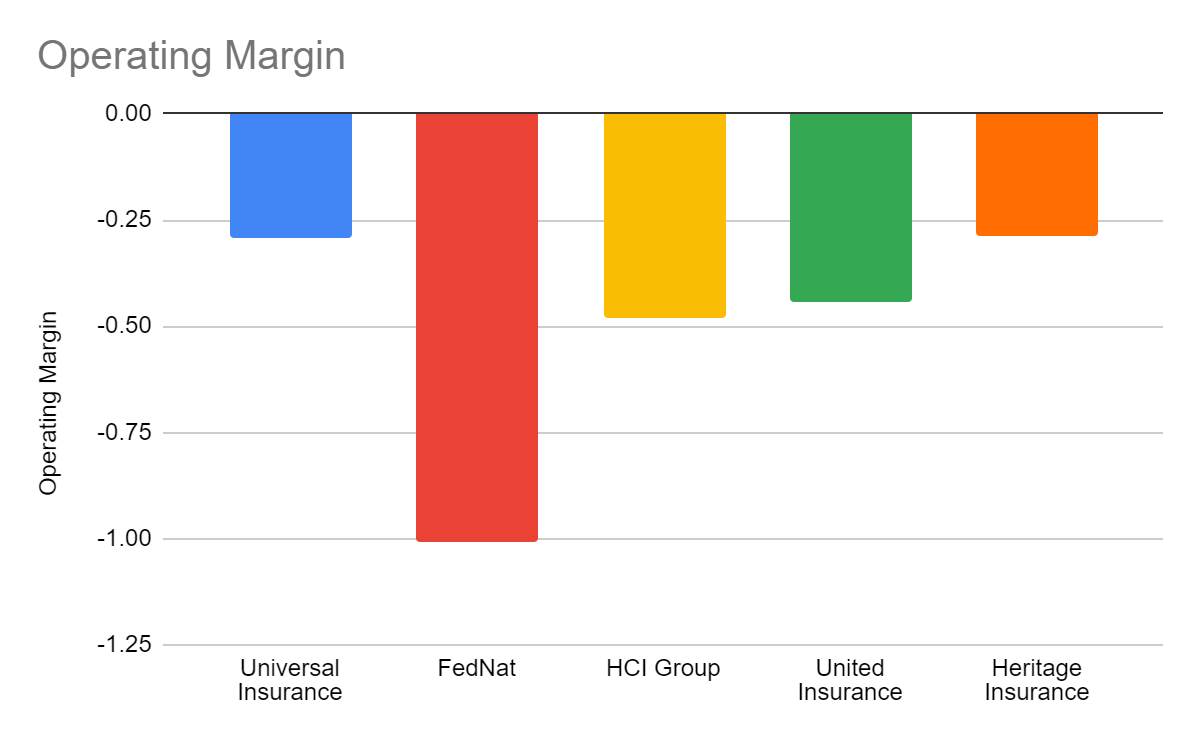

Meanwhile, insurance claims and reserves skyrocketed to $330, a 76% year-over-year increase. These were driven by the excessive claims for damages brought upon by Hurricane Ian. As such, the net value of premiums and losses dropped from $76 million to -$41 million. The consolation we have now is its stable operating expenses. UVE is not contracting amidst elevated prices, but labor-related expenses remain well-managed. The operating margin is now -29% versus 10% in the comparative quarter. While some may think that UVE relies on its relative advantage, I still believe in its strength. Hurricanes are hard to predict no matter how much insurers prepare for them, not to mention inflation and roofing scams. Of course, I do not discount its struggle with geographic diversification. This move is insufficient to offset the risks and losses in its main headquarters. Nevertheless, UVE has the most acceptable operating margin along with Heritage Insurance ( HRTG ). FedNat Holding ( OTC:FNHCQ ) while United Insurance ( UIHC ) continues to contract as it withdraws from commercial lines.

Operating Margin (MarketWatch)

{kind=link}

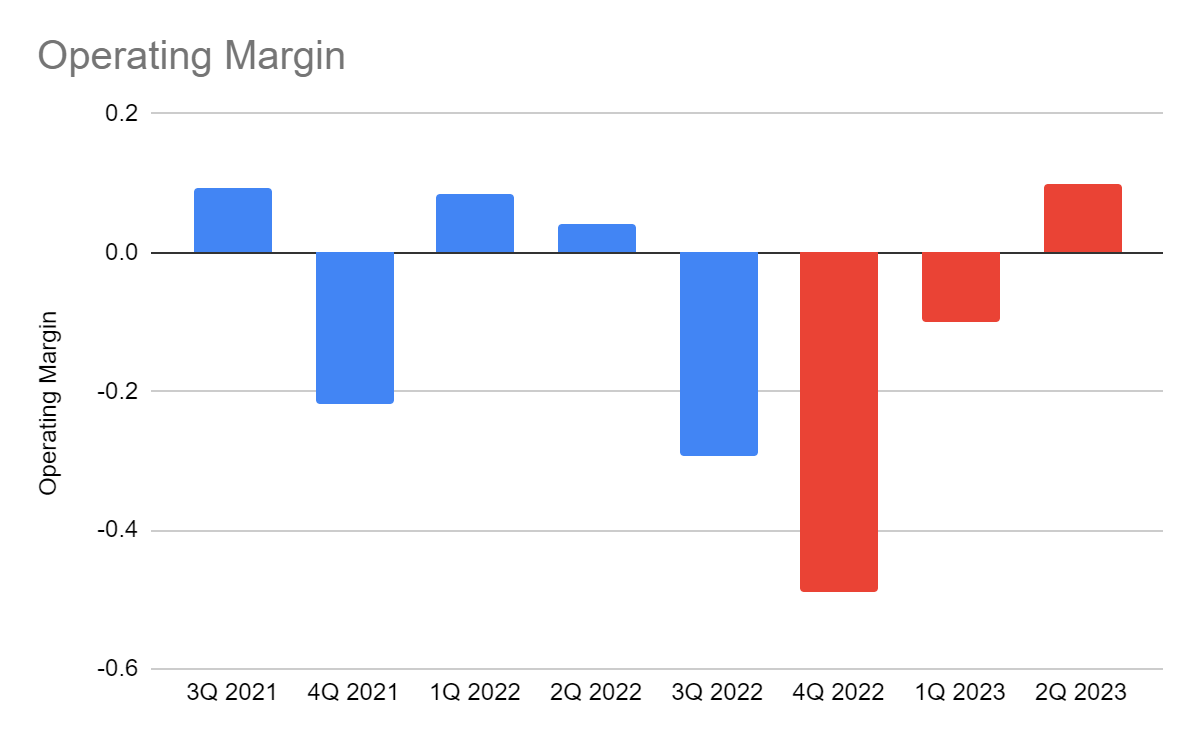

This year, I expect UVE’s performance to show a slight recovery. Home sales may cool down, but P&C insurance will remain a staple. I expect lower revenues in 1Q due to seasonality. UVE may still be completing its payouts to damages during 3Q. But it may be way lower than 3Q and 4Q 2022. With that, I estimate a higher operating margin. In 2Q, I expect more premium inflows as inflation stabilizes, matched with still higher interest and mortgage rates. The lower inflation may give downward pressure on losses on claims incurred. Also, UVE may have completed its payouts by that time, so expenses may be lower. Margins may expand and bounce back.

Operating Margin (MarketWatch And Author Estimation)

{kind=link}

How Universal Insurance Holdings, Inc. Will Fare This Year

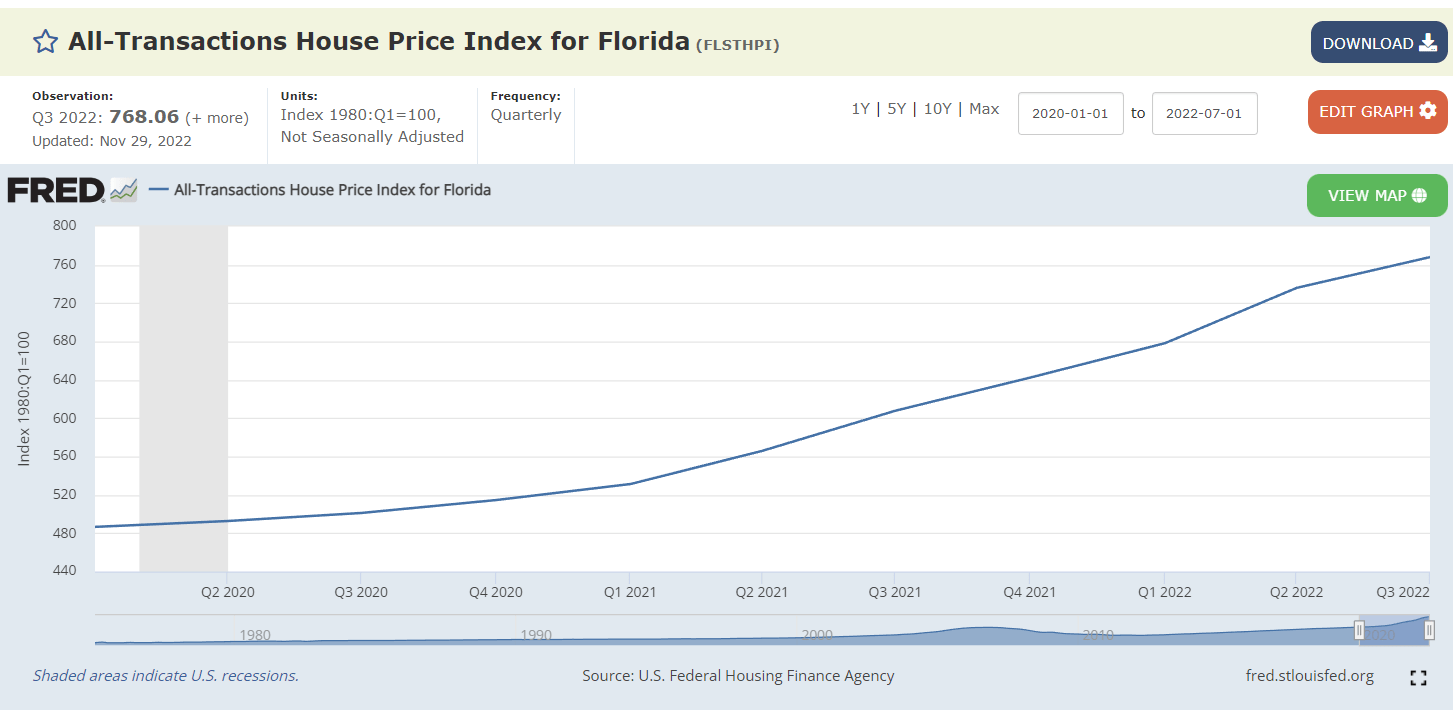

The market stays volatile today, but hope stays as inflation lulls. I expect it to become more stable this year as the Fed raises interest rates. Meanwhile, I expect interest rates to peak at 4.5%, lower than the prevailing expectations of 5-5.25%. Increments may slow down, allowing buyers and borrowers to adjust. Likewise, mortgages and home prices may rise before decreasing at a stable rate. Sales are cooling down, but I don’t expect a massive real estate bubble burst. Let’s face it, inventories are still inadequate to cover market demand. We can attribute it to builders not ramping up over the past decade, and that’s understandable. With that, P&C insurance may remain a staple and help UVE to maintain a strategic price.

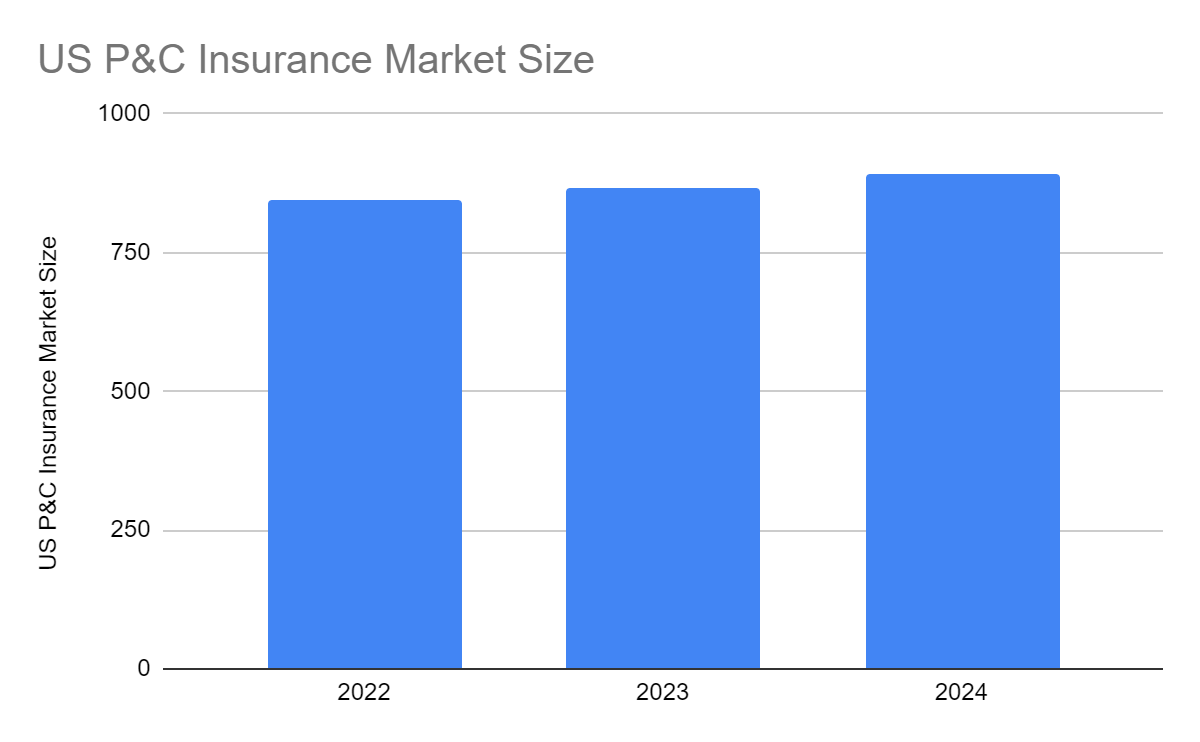

Moreover, the P&C insurance industry is now at the forefront of climate resilience. The impact of Hurricane Ida and Hurricane Ian is evident. Sadly, it is at the expense of insurers and reinsurers. Despite this, it can lead to more demand and inflows as inflation stabilizes. As estimated, the US P&C insurance market size may increase slightly. The important thing is that companies must take advantage of the other quarters to prepare their finances for potential claims. Given the above-mentioned reasons, it is more difficult for insurers and reinsurers in Florida. But UVE proves its capacity to cushion the blows and sustains its capacity.

Home Price Index (ST. LOUIS FED) US P&C Insurance Market Size (IBIS World)

{kind=link}

{kind=link}

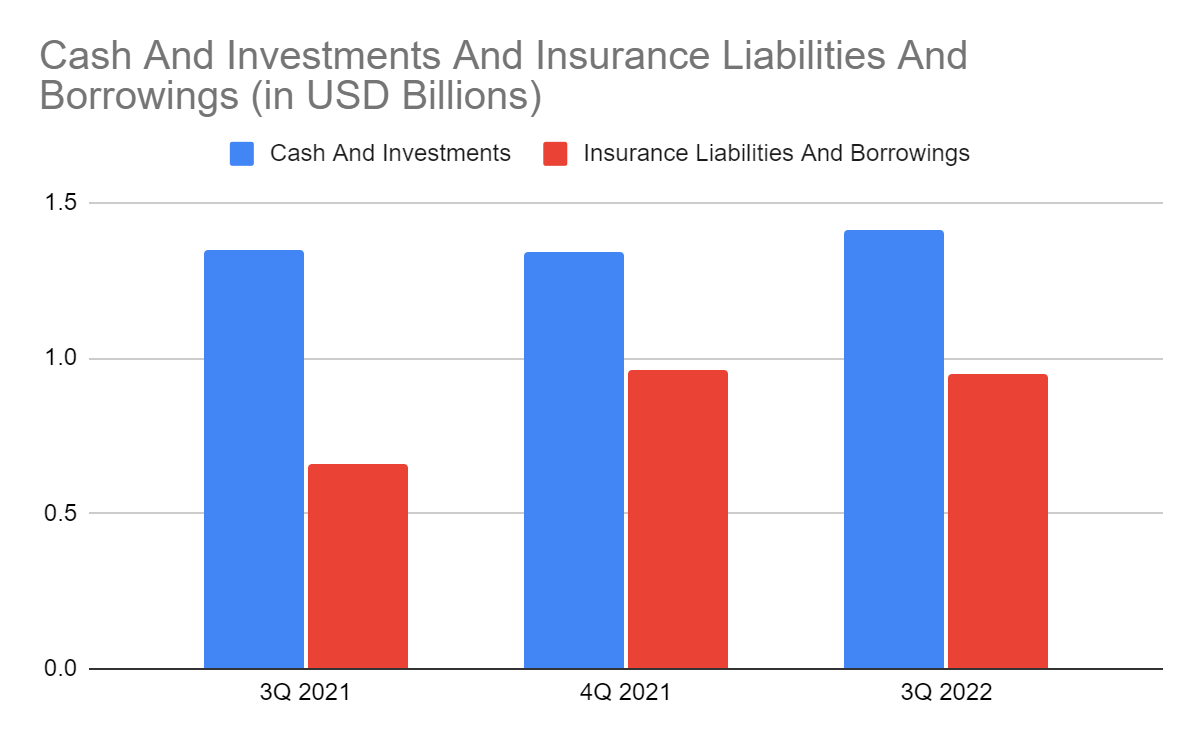

What makes it a relatively secure company is its solid financial positioning. Its stellar Balance Sheet shows UVE can suffice itself and cover liabilities despite drastic market changes. Cash levels and investments are stable with a slight uptrend, showing maintained liquidity. Insurance liabilities are also manageable despite the massive claims. Borrowings are also stable despite the higher interest rates and more insurance claims. Thankfully, cash and investments comprise 80% of the total assets. They are also more than enough to cover almost all liabilities. Cash can also cover borrowings and dividends, so the company may not have to raise its financial leverage. We can confirm it in the Cash Flow Statement, given the actual cash outflows of $2.6 million. It verifies the stability and adequacy of the company. Also, revenues help cover most cash outflows from operations. Indeed, UVE stays a sustainable Florida-based insurance company.

Cash And Investments And Insurance Liabilities And Borrowings (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of Universal Insurance Holdings, Inc. remains almost unchanged. It has been moving sideways, although lower than the price from my previous coverage. At $11.84, it has already been cut by 34% from its value last year. It remains hammered, which is understandable. It adheres to market volatility and fundamentals. Its tangible book value has decreased in recent years. This aspect may be why the stock price did not return to its 2018 highs. This year, its TBV has been cut by almost half its value. Also, the number of common shares outstanding has decreased. Treasury shares have increased, but it remained ineffective to raise the value of the stock. It may be limited in the following quarters, making it harder for the stock price to rebound.

On a lighter note, the Price-to-tangible book value multiple of 1.41x is lower than the annual average of 1.72x. It shows that the stock price has a better valuation. The current price is more realistic as it reflects the company's intrinsic value. If we use the average PTBV multiple and the current TBV multiple of 8.54, the target price will be $14.72. It shows a 24% potential upside in the next 12-18 months.

If we compare it to its peers, UVE shows the best assessment using the PTBV multiple. We can also see the decreased tangible book value of other companies. It shows the impact of the market disruptions in Florida, affecting their intrinsic value.

| Stock Price |

| TBVPS |

| PTBV |

| Average PTBV |

| Derived Value |

| Universal Insurance |

| $11.84 |

| 8.54x |

| 1.42x |

| 1.72x |

| $14.72 |

| FedNat |

| $0.0016 |

| 0.81x |

| 0.002x |

| 1.02x |

| $0.84 |

| HCI Group |

| $42.34 |

| 17.98x |

| 2.35x |

| 2.13x |

| $38.42 |

| United Insurance |

| $1.26 |

| 11.59 |

| 10.88 |

| 3.55x |

| $0.41 |

| Heritage Insurance |

| $2.26 |

| 2.54 |

| 0.88 |

| 1.21x |

| $3.16 |

Moreover, dividend payments remain continuous, ensuring sustained shareholder value. It has a dividend yield of 5.79%, way better than the S&P 600 average of 1.24%. It only comprises 10% cash, showing it has more than enough to sustain its operations and cover borrowings. To assess the stock price better, we will use the Dividend Discount Model.

Stock Price $11.84

Average Dividend Growth 0.1041832011

Estimated Dividends Per Share $0.64

Cost Of Capital Equity 0.1543572551

Derived Value $14.08451563 or $14.08

The derived value adheres to our estimations using the PTBV multiple and shows potential undervaluation. There may be a 19% upside in the next 12-18 months. So, investors may use the current stock price as an entry point to make a position.

Bottomline

Universal Insurance Holdings, Inc. operates in a highly volatile market. But it remains fundamentally stable to sustain its operations and cover excessive claims. It can also cover its continuous dividend payouts with enticing yields. Also, the stock price stays low but shows potential undervaluation. The problem we have now is the problematic situation in Florida. We must see how UVE will fare this year despite its adequate means to suffice its capacity. Taking a position is still risky, but returns may be fruitful if things turn out well. The recommendation after weighing risks and opportunities is that Universal Insurance Holdings, Inc. is a buy.

For further details see:

Universal Insurance Holdings: A Stronghold In A Stormy Market