FLNC - Unleashing Energy Solutions: A Bullish Outlook On EnerSys

2023-06-06 13:20:58 ET

Summary

- EnerSys, a global provider of stored energy solutions, is well-positioned to capitalize on growth opportunities in transportation, telecom, and other markets, with a strong backlog of $1.3 billion and easing supply chain and labor shortages.

- The company anticipates increased demand for its products and services due to government policy support (like the Inflation Reduction Act) and megatrends such as electrification, decarbonization, and automation.

- EnerSys is committed to sustainable growth, reducing its carbon emissions, and improving operational efficiency, with a focus on expanding capacity for its lithium-ion and Thin Plate Pure Lead (TTPL) batteries.

Investment Thesis

The energy crisis after the invasion of Ukraine prompted a surge in renewable energy projects being undertaken around the world.

This rapid adoption of renewable energy serves as a key catalyst in the growing demand for Energy Storage Systems "ESS". ESSs play a crucial role in addressing grid instability caused by the intermittency of renewable sources by storing surplus energy produced during periods of high generation and releasing it as and when required.

EnerSys, which has a significant portion of its manufacturing in the US, is set to benefit from policies such as the Inflation Reduction Act coming online this year. These Investment Tax Credits would help the company improve its margins and/or expand its capacity even further.

As we gradually move towards a more sustainable energy future, Energy Storage Systems are becoming increasingly vital, and EnerSys is well-positioned to profit from this momentum. The company's two other business segments (Motive Power and Specialty) are also set to greatly benefit from megatrends that include EV charging, 5G, and warehouse construction booms.

Introduction to EnerSys

EnerSys ( ENS ) is a leading manufacturer and distributor of reserve power and motive power batteries, power equipment, chargers, and battery accessories. It operates in three Lines of Business: Energy Systems, Motive Power, and Specialty.

With its global presence and 125+ years of battery experience, EnerSys caters comprehensively to stored DC power products. The company claimed a global market share of 22% in FY21 with over 10,000 customers in over 100 countries.

EnerSys offers a diverse range of batteries, which are primarily marketed and sold under renowned brands such as PowerSafe, NexSys, Genesis, Hawker, Odyssey, Cyclon, DataSafe, IRONCLAD, Fiamm Motive Power, General Battery, Oldham, and Express. These products are distributed through an extensive network that includes distributors, independent representatives, and their own dedicated sales teams. The company was formerly known as Yuasa and renamed itself to EnerSys in Jan '01.

ENS is a differentiated provider of stored energy solutions transitioning into a full provider of power solutions. The company is well-positioned to overcome its immediate challenges and capitalize on growth opportunities in transportation, telecom, and other markets.

Financial Results & Operations

The company's fiscal year ends in March every year, and on May 25 the company released its F4Q23 & FY'23 results that beat top and bottom line, well above Wall Street estimates.

The company's balance sheet remains strong, with over $340 million of cash on hand and a credit agreement leverage ratio at 1.8 times EBITDA. Capital expenditures for FY'23 were below the original full-year guidance due to supply chain headwinds on capital projects, but the company remains on track for continued expansion of TPPL capacity for FY'24.

The company reported record revenue of $990m, with a growth of 9% y/y in Q4 FY23. Revenue growth was driven by a 7% increase in pricing (strong price realization) and a 4% increase in organic growth, but this was partially offset by a 2% decrease in foreign currency translation impact.

However, a 340 bps y/y improvement in gross margin was the key highlight, which was driven by a $17m reduction in COGS derived from Inflation Reduction Act (IRA) tax credits under the IRC 45X section. This resulted in a 400 bps expansion in EBITDA margin, leading to actual EPS beating estimates by 32% (GAAP diluted EPS of $1.59 and adjusted diluted EPS of $1.8). Notably, these EPS figures represent a $0.62 increase from the previous year.

The IRC 45X section (Advanced Manufacturing Tax Credit) is a section within the Inflation Reduction Act, specifically designed for manufacturers who produce eligible components within the United States and sell them to unrelated parties. The scope of eligible components encompasses various items found in wind, solar, and battery projects, including PV cells, PV wafers, solar modules, blades, nacelles, inverters, battery cells, and modules, among numerous others (with specified energy densities).

Note : Using a discount rate of 10-15%, I estimate that the NPV of these Tax Credits to be worth about $400m-$450m. These tax credits would further help the company to increase its domestic capacity and source Thin Plate Pure Lead (TTPL) and lithium-ion technologies. I would expect these moves to contribute to revenue growth and margin improvements. Furthermore, additional capacity expansion opens up avenues for the company to enter new markets, including the battery aftermarket, which I estimate could contribute as much as $500m in incremental revenue.

Full Year Results

For the company's full FY'23 performance , EnerSys surpassed its own guidance, achieving growth in both sales and earnings. Despite operating in a turbulent environment marked by inflation, rising interest rates, foreign exchange headwinds, and operational challenges, EnerSys managed to deliver commendable results. The effective management of operating capital and net earnings resulted in significant financial achievements, including $280m of operating cash flow, $191m of free cash flow, and $51m returned to shareholders through repurchases and dividends.

As illustrated in the table below, EnerSys generated about three-fourths of its revenues for FY23 from the Americas, with the Energy Systems business segment contributing nearly half of the total revenue.

| Revenue by Geography |

|---|

| Americas |

| 69% |

| EMEA |

| 24% |

| Asia |

| 7% |

| Revenue by Segment |

|---|

| Energy Systems |

| 47% |

| Motive Power |

| 39% |

| Specialty |

| 14% |

The earnings report also highlights how the Motive Power segment saw adj. operating earnings improve due to strong TPPL mix improvements in the Americas and ongoing positive price cost recapture. Specialty segment adjusted operating earnings were down slightly due to performance issues in the Missouri plant and higher costs in the Sylmar plant, which is being closed and production transferred to other factories. The closure of the Sylmar plant will cost the company about $6m but will bring in savings of $4m per year, leading to a net positive effect.

EnerSys also reported about $1.3 billion in backlogs, which are now seen to be normalizing towards Pre-COVID levels. With supply chain and labour shortages easing, the company should be able to increase its total product output. This will support the company in achieving robust sales in the near term.

2024 Guidance

Looking ahead to the first quarter of fiscal year 2024, EnerSys anticipates operating within a dynamic macro environment, characterized by headwinds such as foreign exchange fluctuations, geopolitical tensions, supply chain challenges, and inflation.

EnerSys expects the gross margin for Q1 to range from 24.5% to 26.5% (benefiting from 150-250 bps from the 45X tax credits). Capex for the full fiscal year is estimated to be approximately $120m. The company eagerly awaits further clarification from the IRS on section 45X, as they intend to use these tax credit proceeds to expedite its strategic initiatives, including securing a domestic source of lithium cells, which may result in an increase in its capital spending projections.

However, in the absence of additional clarification from the IRS on 45X credits (expected during H2 this year), the company expects adjusted diluted earnings per share for the quarter to range between $1.77-$1.87. This projection includes a $0.40-$0.50 benefit from IRA credits. Excluding the IRA credits, the projected earnings per share would still reflect a 20% increase compared to the prior year, at the midpoint. Stable demand trends and a healthy backlog are supportive of this positive outlook.

During the latest earnings call , management emphasized their commitment to innovation as EnerSys continues to invest strategically in proprietary technology solutions. The company is reportedly making progress (on a production roadmap) towards fully commercializing its proprietary EV Fast Charge and Storage system "FC&S" - a proprietary solution that integrates energy storage, backup power, and EV fast charging capabilities into a single offering. While the commercial feasibility of this product is yet to be seen, I do believe this could set a new benchmark for all-encompassing, industrial-grade energy storage solutions.

The company repurchased $23m worth of its shares during FY'23 and still has $40.8m left to utilize from its buyback program. At a low dividend yield of 0.68%, the company also distributed $21.4m in dividends to its shareholders.

Strategic Alignment to Large and Growing Markets and Industry Megatrends

EnerSys's lines of business are all well-positioned to capitalize on the growing global demand for energy storage solutions, driven by megatrends such as 5G, IoT, eCommerce, grid stabilization, EV charging, and renewable storage. Government policy support, exemplified by initiatives like the Inflation Reduction Act and the Rural Digital Opportunity Fund (RDOF), will further accelerate the demand for its products and services.

Firstly, the company's leadership in high-growth stored (non-EV) energy solutions in the B2B sector provides it with a significant competitive edge. In particular, Enersys anticipates substantial growth within the energy systems segment. This growth is expected to be driven by the global expansion of 5G telecom infrastructure and increased data usage, creating a favourable environment for the company's offerings in this area.

Secondly, Enersys' Motive Power business segment is strategically aligned with the booming trend of warehouse construction and expansion. As the demand for instant deliveries grows, the company stands to benefit from the growing market associated with the high-growth segment of warehouse infrastructure.

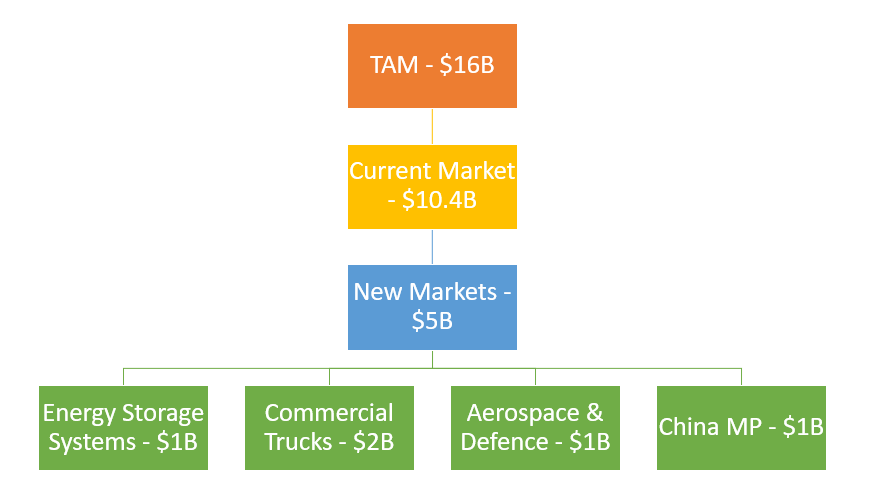

With a total addressable market exceeding $16B, Enersys has a significant opportunity for expansion. This market consists of $10.4B in the current market and an additional $5B from untapped new markets (see chart below). By leveraging its strengths and targeting these markets, Enersys is well-positioned to capture a substantial portion of this lucrative opportunity.

Total Addressable Market (Company Website)

{kind=link}

Planning for Sustainable Growth

To generate long-term sustainable value, the company plans to prioritize profitable growth projects first, while also adhering to a strict capital allocation.

The company is focusing on an improved mix of premium products and reduced costs to lead further margin improvements:

- Expansion of capacity for premium products, including lithium-ion, is among the company's targets.

- Growing maintenance-free motive power solutions and increasing its share in transportation are key objectives, expected to act as strong growth drivers in the long run.

- The company has set its sights on achieving gross savings of over $25M annually by harmonizing factories worldwide and eliminating waste.

Reviewing the company's latest sustainability report 2022 highlights notable achievements in its journey towards achieving carbon neutrality by 2040. The company has reduced its Scope 1 emissions by over 24% in 4 years. EnerSys has also managed to improve its water efficiency, reducing over 2% of water consumption per kWh of storage produced since 2020. Finally, despite a 3% increase in energy storage production, the company managed to decrease its total energy consumption by 1% in 2022. These improvements are indicative of their commitment to enhancing the company's economic resilience in the face of volatile energy prices. Furthermore, I believe this also demonstrates an effective decoupling of growth from energy usage, showcasing the management team's ability to improve operational efficiency and optimize resource utilization.

The upcoming Investor's Day on June 15th should provide more colour to the company's strategic plans to grow the business across markets.

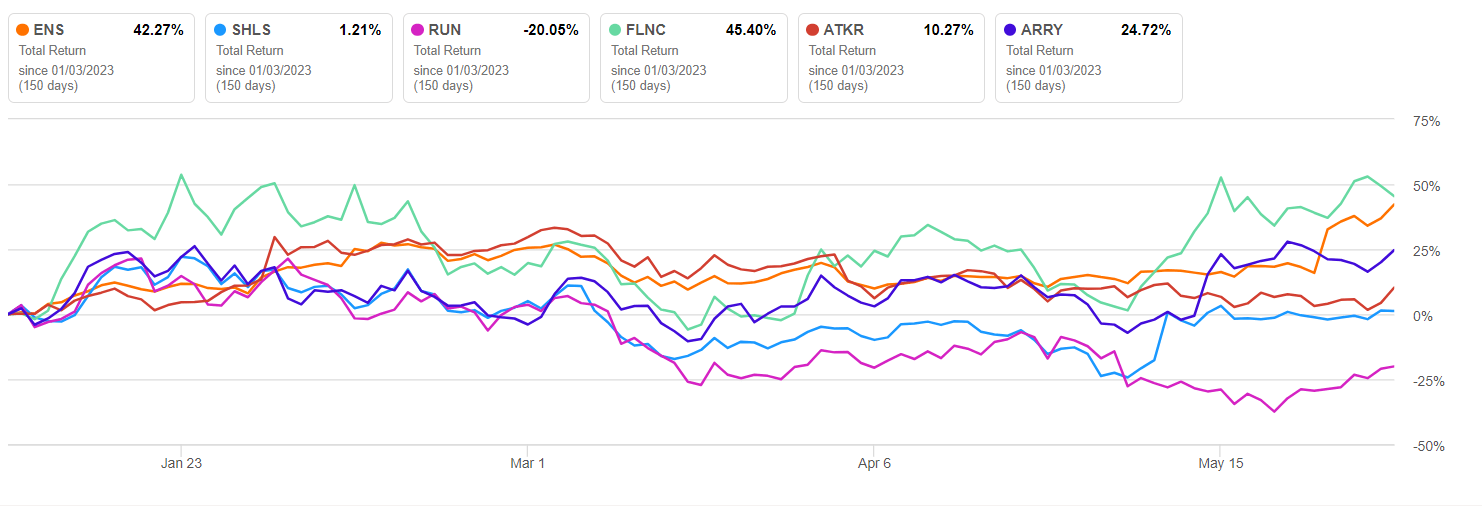

Share Price Performance

After reporting a strong Q4 FY'23 last month, EnerSys is breaking out of a stage-one, 14-week consolidation base on above-average trading volume. The company has also performed better amongst most of its peers on a YTD Total-Return basis (see below)

Total Return vs Peers. (Seeking Alpha)

{kind=link}

A side note - ENS has the lowest short interest at 1.9% ( compared to its peers : FLNC at 19.63%, RUN at 17.7%, ATKR at 10.54% and ARRY at 11.23% short interest). This points to the market's bullish sentiment of the company performing well relative to its peer group.

Price Target

My 12-month price target of $110 is derived from my estimated 14x adj. EPS of US$7.8 for FY'24. Please see the attached Income Statement Projections worksheet below for additional details.

My preferred entry point is $98. Despite the stock being near its 52W highs, I see a considerable runway for EnerSys to push on higher for all the reasons listed above.

Risks to Investment Thesis

Having mentioned why I think EnerSys is a Buy, it's also imperative to highlight some of the key risks for an investor to keep in mind while analyzing the company.

Global supply chain constraints -> The battery systems sector relies on a complex global supply chain for raw materials, components and manufacturing processes. Any disruptions in the supply chain stemming from trade conflicts, hoarding of scarce and critical minerals (lithium, cobalt) and transportation issues can lead to higher costs, reduced capacity and delays in implementing their strategic plans. If commodity prices continue to remain elevated or move towards an upward trajectory, this may hamper their cost-control measures.

Financing and investment risks -> Building up and scaling battery systems often requires substantial capital investment, and with money no longer being cheap to borrow, securing financing for large-scale projects can become challenging for smaller players, leading to a pullback in new orders.

Competition from other battery manufacturers -> Intense competition from within the sector can create pricing pressures and a margin squeeze for EnerSys.

Conclusion

Energy Storage and 5G are sectors that are growing quite rapidly and the company's positioning to leverage some of the current megatrends in the industry should help its top line grow effectively.

I also anticipate that the IRA 45X credit will provide a significant and sustained boost to the company's bottom line and EPS over the next decade. This aligns seamlessly with the company's strategic objectives and its shift towards advanced battery chemistries and solutions, which should further strengthen EnerSys's overall market position.

Furthermore, the company has a relatively healthy balance sheet and I'm comfortable with management's transparency and skill in leading the business forward.

Final note - As with most assets in this space, I do not view EnerSys as a quick-buck company and potential investors in this company should be comfortable holding for a period of 12 months at the least.

For further details see:

Unleashing Energy Solutions: A Bullish Outlook On EnerSys