GEO - Unlocking Hidden Value: The GEO Group's Remarkable Transformation In A Niche Industry

2023-09-14 06:32:51 ET

Summary

- The GEO Group is a dominant player in the secure facility sector, particularly in electronic monitoring.

- The company's transition from a REIT to a C-Corp structure has improved its flexibility for reducing debt and reinvesting in core operations.

- Despite impressive growth in revenue and profit margins, GEO stock is currently undervalued, presenting a compelling investment opportunity.

Editor's note: Seeking Alpha is proud to welcome Stefan Lingmerth as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Executive Summary And Investment Thesis

This report unveils a compelling investment opportunity within a unique industry segment. The GEO Group holds a dominant position in the secure facility sector, particularly as a leader in the high-margin Electronic Monitoring domain. Its recent transition from a REIT to a C-Corp structure has unlocked greater flexibility for reducing debt and reinvesting in its core operations. Despite impressive growth in both revenue and profit margins, the company currently trades at a notably modest valuation, with EBITDA multiples at 5x and a P/E ratio of 6.5. The financial transformation, along with the company's concerted efforts to enhance its policies and procedures, has elevated it to align with industry best practices. Through a comprehensive analysis of its constituent parts, we reveal a remarkably compelling value proposition, and set a target of $24/share.

Historical Context And Corporate Evolution

Founded in 1984 by George Zoley, The GEO Group has achieved prominence through the ownership, leasing, and management of correctional and detention facilities across multiple countries, including the US, South Africa, Australia, and the UK. The company oversees an extensive network of 102 facilities, offering approximately 82,000 beds. The company went public in 1994 and with the acquisition of BI Inc. in 2011, The GEO Group expanded its portfolio to include electronic monitoring, a pivotal aspect of its operations. The culmination of these efforts resulted in a company that is well-poised to capitalize on growth and innovation. Previously structured as a REIT, The GEO Group's transition to a C-Corp model was an instrumental step towards optimizing its debt management strategy. Under the new leadership of CEO Jose Gordo, the company is vigorously executing its debt reduction program, impressively decreasing debt from $2.7 billion in 2021 to $1.9 billion by 2Q23.

Ownership

There is a total of 123.3 million shares outstanding. The top holders of the stock, as of 6/30/23 Nasdaq report , are BlackRock Fund Advisors, with 16.1%, and The Vanguard Group with 11%, and FMR LLC with 9.1%. There are no other holders above 5% and insiders have a total of 5% ownership. Mr. Zoley had as of latest filings 3.37 million shares or 2.7%. The CFO is Brian Evans who's been with the company since 2000 and the COO is Wayne Calabrese who held various positions since 1989 but came out of retirement and re-joined the company in 2021. Mr. Zoley serves as the Executive Chairman of the board; Mr. Gordo is also a board member along with 7 other independents for a total of 9 board members.

Financial Performance And Segment Contribution

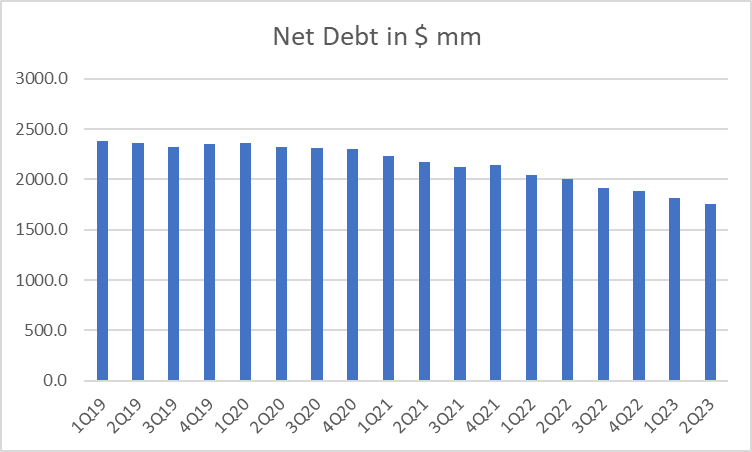

The GEO Group's revenue and EBITDA have demonstrated an impressive trajectory, culminating in $2.4 billion in revenue for 2022, yielding an EBITDA margin of 22.7%. This substantial performance was bolstered by an EPS of $1.17. The company's focus on debt reduction is mirrored in its financial prowess, with $296 million in cash flow from operations and $200 million in free cash flow for the year . The first half of 2023 continued this upward momentum, with revenue reaching $1.2 billion, reflecting year-over-year growth of 5.3%. EBITDA stood at $260 million, compared to $257.5 million the previous year, which is $540 million on trailing twelve-month basis. This thriving financial landscape has been instrumental in The GEO Group's pursuit of debt reduction, with the company effectively reducing its debt load from $2.7 billion to $1.9 billion (net debt $1.75 billion) between 2021 and 2Q23, see 10-Q for the period ending 6/30/23.

Net Debt trajectory (SEC 10Q filings)

{kind=link}

The largest customer is the US Fed Gov with close to 60% of the revenue, the rest comes from various states and international exposure. The largest segment was the US Secure Services (the Prison segment) with $1.4 billion in revenues and gross margins of 25% in 2022. There is minimum short-term contract risk for the prison segment. In 2023, the company has 6% of its business up for re-bid and an even smaller amount in 2024 and 2025.

The Electronic Monitoring business consisted of close to $500 million in revenues and have doubled since 2020. The margin for this business is much better as well with gross margins at 54% for 2022. The company got rewarded with a contract in 2020 that goes to 2025 and is the sole provider of Electronic Monitoring services to the federal government program, ISAP, to provide an alternative to detention for migrants apprehended at the border. We believe this is good for business but there is a risk that they will have to share some of this business with its competitor CoreCivic (CXW). However, the incumbent, The GEO Group, has a much better head start in front of 2025 to deal with providing a quality product and a scalable service. We don't think there is a risk they will lose it in its entirety as the government is dependent on this service.

Strengthening The Balance Sheet

The successful metamorphosis from a REIT to a C-Corp structure has been a catalyst for The GEO Group's newfound balance sheet fortification. In 2022, the company generated $200 million in free cash flow, while the first quarter of 2023 yielded approximately $80 million, see company's annual and quarterly statements. The GEO Group's strategic debt reduction initiative has been further fortified through a well-executed debt exchange in August 2022, which offered a solution to short-term maturities. This strategy is underscored by the company's ongoing focus on achieving leverage targets of below 3.5x by the end of 2023 and below 3x by the conclusion of 2024. This disciplined approach has significantly improved The GEO Group's financial standing.

Industry Landscape And Competitive Edge

The GEO Group's distinct position within the broader incarceration sector is marked by its comprehensive suite of secure facilities and pioneering electronic monitoring services. Despite the prevailing reluctance among financial institutions to invest in "prison companies," The GEO Group has emerged as a beacon of improvement, consistently refining its policies and procedures to align with industry best practices, for instance see press release from Oct 6, 2022, The GEO Group Publishes Fourth Annual Human Rights and ESG Report .

As we delve into the landscape of secure and community reentry services, a remarkable window of opportunity has emerged against the backdrop of current immigration regulations. The United States' incarceration system is predominantly governed by public entities, supplemented by a significant private sector presence. As of year-end 2021, the public system accommodated around 1.2 million individuals across federal and state prisons. See Bureau of Justice Statistics published Dec 2022. Concurrently, approximately 96,000 individuals found themselves under the care of private prisons.

Over the past two decades, the distribution of imprisoned individuals between private and public facilities has remained notably consistent. In this environment, The GEO Group stands as a premier private provider of diversified secure and community reentry services. Capturing a commanding 40% market share, The GEO Group maintains control over 82,000 beds. Close on its heels is CoreCivic, occupying 38% of the market with 78,500 beds. The landscape is further enriched by the presence of MTC (Management and Training Corporation), contributing a 14% share, while other operators collectively constitute the remaining 8%.

A pivotal juncture has emerged due to the escalating inflow of undocumented immigrants across the US border , particularly along the southwest frontier. In 2022, an unprecedented 2.76 million undocumented immigrants traversed into the United States. This marked increase, as compared to the 1.72 million recorded in 2021 - the previous annual peak according to Customs and Border Protection data, was fueled by a significant surge in Venezuelans, Cubans, and Nicaraguans seeking refuge in the US.

Within this context, these individuals, seeking legal status or waiting for asylum proceedings, will invariably find themselves in detention or under monitoring while awaiting adjudication. This dynamic ensures a steady stream of business for The GEO Group. As we navigate the evolving immigration landscape, the potential to effectively serve this population presents a strategic and impactful avenue for the company.

Unveiling Value Proposition

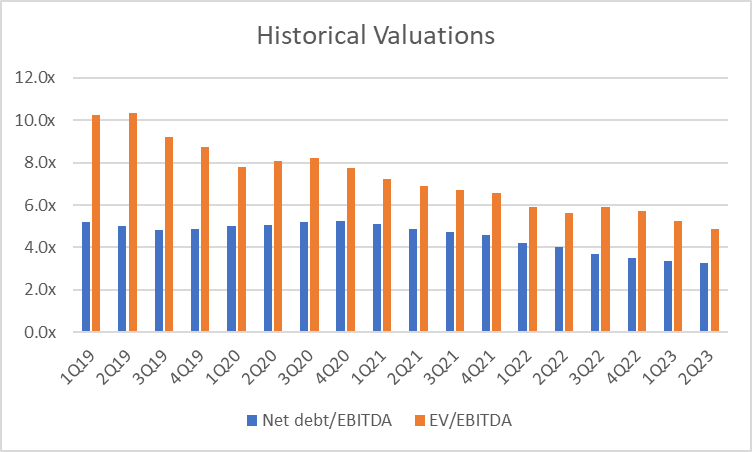

Amidst this transformational journey, The GEO Group's current enterprise value of $2.7 billion offers a striking contrast to its valuation as a REIT in 2019, which stood at $4.6 billion with higher debt and lower EBITDA. The market's current valuation at 5x EBITDA contrasts with a past multiple above 8x-9x.

Historical Valuation (SEC 10Q filings plus market price data)

{kind=link}

As a further reference, CoreCivic trades at 7.5x without a high-margin electronic monitoring business. By harnessing these metrics, a price target of $24 per share is envisaged, by using 8.5-9x on trailing twelve-month EBITDA. Furthermore, by segregating the prison and electronic monitoring businesses (sum-of-the-parts), we witness substantial latent value. The real estate segment alone, underscored by the recent market transaction by CoreCivic, which sold 2k beds to the State of Georgia for $130 million or $65,000 per bed, would value GEO's 57.5k beds at $3.7 billion, which remarkably exceeds the company's current enterprise value (i.e., another $15.5 in stock value). In tandem, the electronic monitoring business, with its strong growth trajectory ($500 million in sales) and impressive gross margins of 54%, can be attributed a value of approximately $1 billion. This supplementary value equates to an additional ~$8 per share. Supported by robust and consistent cash flows, GEO showcases a remarkable free cash flow yield of 23-34% relative to market capitalization, with $200-$300 million in free cash flow on a current market capitalization of $875 million. As this cash will continue to go to reducing debt, it will accrete value to the stock until the leverage is below 3x and company will actually start buying back shares.

| Sensitivity Analysis - Share Price with different EBITDA and Multiple |

| EBITDA in $ mm |

| 400 |

| 450 |

| 500 |

| 540 |

| 550 |

| 600 |

| 650 |

| Multiple |

| 4 |

| -1.27 |

| 0.35 |

| 1.97 |

| 3.27 |

| 3.59 |

| 5.21 |

| 6.84 |

| 5 |

| 1.97 |

| 4.00 |

| 6.03 |

| 7.65 |

| 8.05 |

| 10.08 |

| 12.11 |

| 6 |

| 5.21 |

| 7.65 |

| 10.08 |

| 12.03 |

| 12.52 |

| 14.95 |

| 17.38 |

| 7 |

| 8.46 |

| 11.30 |

| 14.14 |

| 16.41 |

| 16.98 |

| 19.82 |

| 22.66 |

| 8 |

| 11.70 |

| 14.95 |

| 18.19 |

| 20.79 |

| 21.44 |

| 24.68 |

| 27.93 |

| 8.5 |

| 13.33 |

| 16.77 |

| 20.22 |

| 22.98 |

| 23.67 |

| 27.12 |

| 30.56 |

| 9 |

| 14.95 |

| 18.60 |

| 22.25 |

| 25.17 |

| 25.90 |

| 29.55 |

| 33.20 |

| 10 |

| 18.19 |

| 22.25 |

| 26.31 |

| 29.55 |

| 30.36 |

| 34.42 |

| 38.47 |

| Shares o/s |

| 123.3 |

| Net Debt |

| 1757.1 |

Risks

We believe the main risk for the company is to lose contracts with the government due to various operational reasons, like misconduct by staff, serious mismanagement of prisons, etc. New federal administration with new policies is another risk as well as losing business to competitors as government wants to diversify contractors within the electronic monitoring sector.

Future Catalysts And Performance Evolution

The catalyst that will further propel The GEO Group's value proposition is its ongoing trajectory of performance improvement. As the company attains its goal of 3x leverage, it is poised to initiate shareholder-friendly initiatives, such as share buybacks and dividends. Although the current emphasis is on debt reduction, the forthcoming inflection point is anticipated in the latter half of 2024, coinciding with the US presidential elections. This juncture signifies a pivotal moment in The GEO Group's journey towards delivering enhanced shareholder value and embodying the quintessence of a deep value investment opportunity.

For further details see:

Unlocking Hidden Value: The GEO Group's Remarkable Transformation In A Niche Industry