EA - Unlocking Long-Term Success: Why Electronic Arts May Outperform In The Gaming Industry

2023-07-13 03:40:12 ET

Summary

- Electronic Arts is expected to outperform in the gaming industry by leveraging its 'games as a platform' strategy, backed by robust financial performance and growth track record.

- EA's revenue and cash flow have grown consistently over the past decade, with a compounded annual growth rate of 7.6%, outperforming key competitors.

- EA's strong balance sheet, diverse portfolio of games, and investment in mobile gaming and creator tools are expected to drive long-term growth.

Electronic Arts ( EA ) is poised to outperform in the dynamic gaming industry by leveraging its 'games as a platform' strategy. We believe that the company's robust financial performance and growth track record, the rapid projected growth of the gaming industry, the company's competitive edge arising from superb IP and player momentum and its ability to invest in key areas are all elements that support a long-term growth picture.

EA’s Strong Business Performance

EA is a mature company in a fast-growing industry that shows no signs of slowing down. EA has remained competitive and been able to grow revenues and cash flows consistently while maintaining a healthy balance sheet. Over the last ten years EA has done this despite an industry that is evolving quickly with the pace of technology and an increasing number of competitors entering the space. EA’s top competition is Activision Blizzard (NASDAQ: ATVI ), Take-Two Interactive (NASDAQ: TTWO ), Ubisoft (UBSFY), and Roblox (NYSE: RBLX ). In addition to those gaming focused companies, many large technology companies like Apple (NASDAQ: AAPL ), Microsoft (NASDAQ: MSFT ), Meta (NASDAQ: META ), and Alphabet (NASDAQ: GOOGL ) have dipped their feet in gaming as a new source of revenue. Perhaps EA’s largest risk alongside their other gaming focused counterparts is the fact that these larger technology companies who are extremely well funded may be able to innovate and create experiences for gamers that are higher quality than what traditional gaming companies have been able to do. One thing we’ve seen is Meta and Apple releasing VR and AR headsets that can create new gaming experiences for players. Apple also came out with their own mobile games through Apple Arcade. These types of events could be signaling a shift where the big technology players end up taking over the gaming space, but we believe EA will continue to thrive in any circumstance because of their healthy fundamentals.

Revenue and Cash Flow Growth

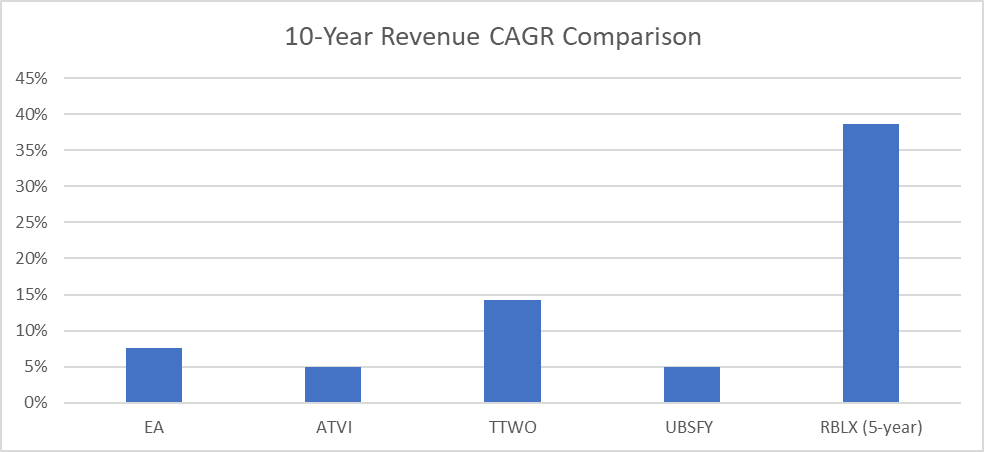

Two key factors to EA’s fundamental strength are their increasing revenues and cash flows. Over the past ten years, EA has grown revenues at an annual compounded rate of 7.6%. Relative to their key competitors as shown in the chart, this is a quality rate.

{kind=link}

What might jump out is TTWO and RBLX. As for RBLX, they are a new company and there’s only five years of revenue data, so their compounded annual growth rate (CAGR) is over a five-year period. They’ve clearly had strong success in generating revenues, but what we don’t like about RBLX is the fact that they’re not profitable and have yet to prove they can sustain such a rapid growth rate. In general, we like to take a more value-based approach to investing. That is, finding high quality companies that consistently grow revenues and free cash flows, have a strong and durable moat, and are valued based on conservatively predicted future earnings that can be derived from analyzing the businesses track record of success. This effectively eliminates RBLX as they do not check all these boxes.

As for TTWO, they look more enticing as they are a more mature company, growing quickly with a proven history of generating free cash flows. However, in their most recent fiscal year they took reported a significant net loss for the first time since 2015. In addition to that, they’ve shown only a short period of cash flow generation that one could argue was due to the COVID-19 pandemic. As consumers stayed inside looking for entertainment and had an easy money environment inducing more spending, gaming companies benefitted significantly. However, this cash flow was not able to be maintained which makes us uncomfortable about the future financial health of TTWO.

ATVI and UBSFY are the remaining contenders, but right off the bat, EA beats them both by a good margin when it comes to revenue growth. We think this is because of EA’s strong momentum in their broadly diversified portfolio of games that cater to different audiences across the globe. So, when it comes to revenue growth, EA takes the cake. We also mentioned increasing free cash flows for EA. Over a ten-year period, EA has grown free cash flow at a CAGR of 15.07%. This compared to UBSFY going negative in free cash flow as of their most recent annual filing and ATVI growing at only 6.18% compounded shows EA to be a better cash generating machine.

EA’s Healthy Balance Sheet

EA’s balance sheet looks strong and durable. At the close of EA’s fiscal year 2021 they had 6.3 billion in cash and short-term investments on the balance sheet relative to only 2.964 billion in current liabilities. When looking at the total current assets and total current liabilities, EA boasted a quick ratio of 2.43 at this time showing they have over double the amount of liquidity to cover their obligations. In addition, with a debt-to-equity ratio of 0.69 at this time, EA was in great financial health. One argument one can make though is that these numbers are inflated due to excess video game demand during the pandemic lockdowns, so let’s look at the balance sheet on the most recent annual filing . EA saw a decrease in cash likely from pandemic numbers normalizing, but they still had 2.767 billion in cash and short-term investments. In addition, when looking at current assets and current liabilities, EA has a quick ratio of 1.2, which is good but not great. They have enough liquidity to cover their obligations but not with a significant margin like they did in 2021. We think this is because EA took their large cash position and invested heavily in growing their business through research and development (R&D). Historically, EA has shown strength in returning capital to their investors, so this increased investment looks like a good sign for future growth, which we’ll discuss later in the article.

We’ve talked about EA’s strong financial position and abilities to generate revenues and cash flow at strong rates relative to their competitors, but now we need to talk about why they’ve been able to do this and why we think they’ll continue to do this at rates better than their competitors.

EA’s Growth Strategy in a Growing Gaming Industry

The video game industry has seen rapid growth and significant changes in the past five to ten years. According to Statista , the industry has grown from revenues of 156.66 billion in 2017 to 331.51 billion in 2022 and is projected to hit 521.54 billion in revenue by 2027. That’s a 7.89% compounded annual growth rate (CAGR). Some of the biggest changes have been the shift to mobile gaming, free-to-play games with extra content available for purchase (also known as live services), and social connectivity through online multiplayer gaming. In the gaming industry over 50% of revenue comes from mobile gaming. We’ve seen companies like RBLX put their primary focus on mobile gaming and giving control to the user with great success as seen previously in their revenue growth. We’ve also seen companies like Microsoft, Alphabet, and Apple enter the mobile gaming market as its gained momentum. What makes mobile gaming such a hot trend aside from the fact that it makes gaming more accessible, is that most games have a free-to-play model that’s supported by live services. Live services are the extra content that can be purchased within games and the revenue from this is what supports free-to-play games. We love the live services revenue model because players can easily become attached to a game as it’s free-to-play and once they’re attached, it’s highly likely they will pay for extra content to enhance their playing experience. This is especially powerful because it creates a recurring revenue stream for gaming companies, increases game lifespan and revenue, and allows them to predict future earnings more accurately.

As for EA, they are not the strongest when it comes to mobile gaming. They’re traditionally a console and PC focused company, but they have been investing in growing their mobile presence. In their most recent earnings call , there were twenty-two mentions of mobile gaming as EA believes this to be a key part of their business moving forward. They’ve made some recent acquisitions including Glu Mobil and Playdemic Limited which are both mobile gaming companies that have increased mobile profitability by three times over the last year. We think EA can continue to grow their mobile footprint and make it a material part of their future revenue growth; however, we think more importantly, the near-term catalyst for growth will be EA’s strategy to make games become a platform.

In EA’s most recent earnings call they mentioned “games as a platform” and how the future of gaming will involve more creator tools to immerse players in games. We’ve seen RBLX give power to its players by allowing them to create their own games through Roblox Studio and publish these games for the communities to play. Roblox is also big in social interaction through chats, groups, collaboration, and team gameplay. As the world shifts to become more digital, the gaming industry is positioned well to benefit from this as there are already massive communities online for certain games. Another note about Roblox is they have a full-on virtual economy. Creators of games can choose to monetize their games and players can make purchases in games with a virtual currency called Robux. We have to say, Roblox is doing some great things when it comes to “games as a platform” and we’ve seen proof of this from their revenue growth, however we think EA is positioned to take advantage of this trend and grow more significantly than Roblox in the long run.

First and foremost, EA consistently generates free cash flow at high levels like we saw earlier, which allows them to reinvest in their business to develop necessary new functionalities to compete with companies like RBLX. The functionalities EA is focused on are play, watch, create, connect. In their most recent earnings call, they stated they’re investing meaningful resources in this over the coming years. We expect continued investment into these key pillars of making games a platform will be a strong growth driver.

Another reason EA will outperform RBLX is because of their diverse portfolio of intellectual property ((IP)) and games. Some of their most popular games are Apex Legends, EA Sports FIFA, and The Sims. Each of these games has seen massive momentum in growth over the past few years and have gigantic player bases. With large online communities around diverse sets of games, there’s an inherent network effect that pulls more people in. Most popular games nowadays are popular because of the social connectivity aspect and online multiplayer experiences. When more people join the game, it creates better balanced teams and matches, a more robust and fulfilling community, and an overall more engaging player experience. Now, it's time to dive into the momentum of each of EA’s key games and how that will translate to continued revenue growth. We’ll especially hit on EA Sports FIFA as they are re-launching in the fall of 2023 as EA Sports FC and we think this is a key catalyst.

Momentum in Key Games: A Catalyst for Growth

First, we’ll discuss Apex Legends which was released relatively recently and has quickly grown in popularity. In 2019 when the game was released, it was the most downloaded free-to-play game on PS4. That helped EA realize 9% year-over-year digital net bookings growth. In the following year Apex Legends had over 100 million players life to date while also having 12 million weekly average players. Apex Legends is a free-to-play game battle royale third person shooter game supported by live services. Battle royale games became popular after the release of a game called Fortnite, so EA decided to capitalize on this trend, and it clearly has paid off for them. We expect the Apex Legends community to continue growing its player base as the game is still in its early stages and has much more room for growth.

Then there’s The Sims franchise. The franchise has four total games with the current one being The Sims 4. In EA’s most recent 10-Q, The Sims 4 player network alone was said to have grown to 70 million players across the globe. That’s a 48.5% increase in network since Q4 of EA’s fiscal year 2021 where the player network was at only 36 million. To top it off, as of 2021, The Sims 4 had its sixth consecutive year of franchise growth. This game is also free-to-play and it’s more of a lifestyle game where users can create unique characters, build homes for themselves, and essentially live life in a simulated alternate universe. We think the Sims will grow in popularity based on the shift towards games like Roblox where there are many games within the game. What we mean by this is that players can join the game, chat with friends, build houses together, and potentially have monetization tools as EA invests more in creator tools as they’ve mentioned during their most recent earnings call. Another sweetener when it comes to the Sims is that 60% of The Sims 4’s audience is women between the ages of 18 and 24. This compared to Roblox’s audience consisting of over 50% of players under the age of 13 and 75% under 18 makes The Sims look like a better long term investment. Kids usually must ask their parents for money which creates one additional layer of difficulty when it comes to spending in the game and there is simply a wider audience when looking at adults. There are 2.4 working age adults for every child under 14. Considering half of Roblox’s audience is under 13, this makes EA look better positioned to create a great game platform through The Sims as they simply have a further reach.

Now we’ll talk about the big catalyst, FIFA. The rebranding of EA Sports FIFA to EA Sports FC is said to be a “fan-first future for global football”. Right now, there’s not a lot of information about the specifics of the release of EA Sports FC but based on EA’s said investments in “games as a platform”, we would imagine that the new game will include some exciting new features giving players more creative control. The popular game mode in EA Sports FIFA has been Ultimate Team Mode which again is free-to-play. With this game being a sports game, players are more incentivized to spend money to get good players on their team and compete at high levels. This of course drives live services revenue for EA which made up 83% of revenue in Q-4 of fiscal year 2023. The FIFA franchise has gained massive momentum recently. In 2021 Ultimate Team players grew by 16% year-over-year and in fiscal year 2023 the FIFA franchise Q4 net bookings grew by 31% year-over-year. More players playing FIFA means more Ultimate Team live services revenue. In 2023 FIFA23 surpassed lifetime sales of FIFA 22 within 6 months making it the most successful launch in franchise history. With this growth in the franchise coming before a highly anticipated launch of EA Sports FC, the launch is likely to deliver strong results for EA.

Strong Returns on Investment to Drive Growth

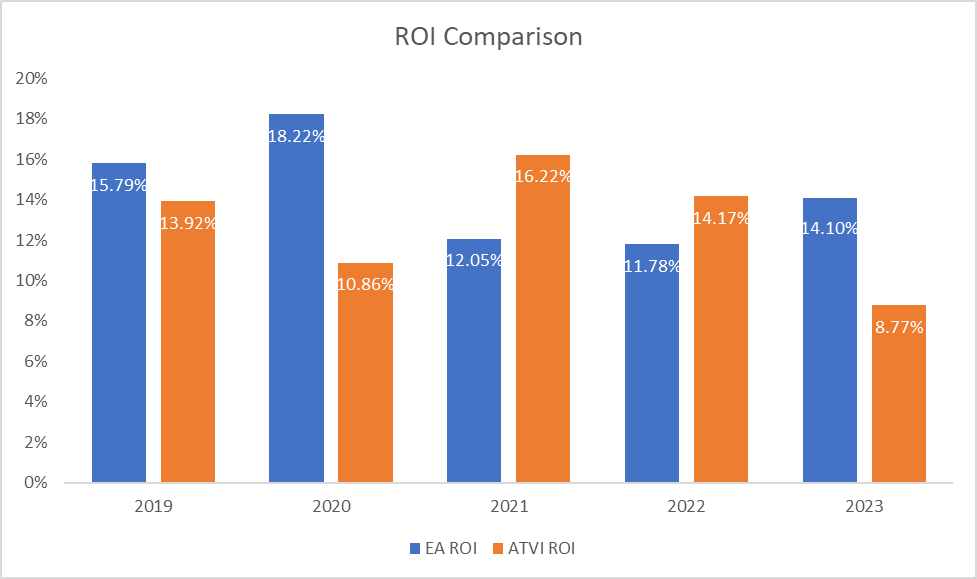

We’ve talked a lot about how EA is investing in “games as a platform” which to our understanding is going to look like the online community of Roblox. We also talked about how EA Sports FC and The Sims with their strong momentum and strong foundation to build the game into a platform will likely be the catalysts for growth in coming years. But just because EA is investing in this trend of gaming as a platform doesn’t mean they’ll succeed in returning that investment to shareholders. To understand EA’s ability to return capital we’ll look at their historical return on invested capital ((ROIC)). To make it simple, this chart shows the ROIC from the last five years with a comparison to their most fundamentally stable competitor ATVI for context.

{kind=link}

Clearly EA has done relatively well at returning capital on their investments, however there was a dip in 2021 and 2022. This can be explained by increased R&D expenses. In terms of R&D expenses, there was a 12% increase from 2020-2021 and a 19% increase from 2021 to 2022 as compared to smaller increases of about 8% in the former two years. As a percent of gross profit in 2021, 2022 and 2023 R&D was 43%, 42.5% and 41% respectively. This is up from the previous two years where R&D was 39% of gross profit in 2019 and 37% in 2020. What likely happened here is after 2020 EA was sitting on a ton of cash from strong momentum from a growing gaming industry and a record year during the pandemic lockdowns. With their large cash pile they chose to significantly allocate that capital towards R&D to develop their vision of “games as a platform”. Inherently, R&D takes time to have benefits materialize which is potentially why we see a drop in ROIC in 2022, but then a decent increase in 2023 as those investments start to materialize. This uptick in ROIC along with the strong momentum in their large gaming franchises that we discussed earlies shows good signs of growth in the short-term that we expect to continue in the long-term.

Valuation

By this point, we know EA is a financially strong and stable company with competitive advantages in a growing industry. EA is investing in what they think, and we think is the future of gaming and looks to be positioned to grow significantly as these investments start to materialize. Now, we need to value the company to give us a fair price to buy at with a good margin of safety. To do this we’ll use the discounted cash flow method ((DCF)). For this analysis we’ll give a range of values giving us a base case, worst case, and best case. For the base case and best case, we’ll use a customary 10% discount rate. For the worst case, we’ll use 12%. For projected growth rates, we’ll keep it simple by using EA’s historical free cash flow CAGR of 15.07% over a 10-year period as the best case. This is assuming that EA’s most recent ten-year period is slightly overinflated from the stay-at-home orders during the pandemic. The worst case will use an 8% compounded rate and the base case will use a 10% compounded rate. We will also assume the company will grow perpetually at a conservative rate of 3% for all cases. Our worst case, base case, and best-case values are listed below.

- Worst case: $129

- Base case: $206

- Best case: $360

As an investor looking to buy with a healthy margin of safety, one could argue that now could be an interesting time to initiate a position as it trades near our worst-case valuation and within a consolidation point on the chart. After long periods of consolidation, catalysts can force the stock price out of its consolidation range. For EA, we think the catalyst will be the release of EA Sports FC in the fall of this year, however with economic uncertainty still high, one might look to buy with an extra layer of safety.

With that being said, if you’re a long-term investor, we think EA is at acceptable buying levels right now. Even with short-term potential downside from market uncertainty, we feel the upside asymmetrically outweighs the downside. A long-term investor who believes in the strong fundamentals of EA and the promise in an evolving gaming industry should be able to stomach a short-term drop and even see it as a great opportunity to add to their position.

We would like to thank N Henry for this piece.

For further details see:

Unlocking Long-Term Success: Why Electronic Arts May Outperform In The Gaming Industry