UNM - Unum: Definitely A 'Hold' Here

2023-10-31 03:33:43 ET

Summary

- Unum has outperformed the market and achieved a 100%+ return on investment in less than 24 months.

- Higher interest rates pose some risks for insurance companies, but Unum remains a safe and attractive business.

- Unum's current valuation is unattractive, and there are other insurance companies with more favorable upsides.

Dear readers/followers,

So, I underestimated what sort of trajectory Unum ( UNM ) would do, and since my last article , the company has actually outperformed the market. Way back when I invested in Unum at under $20/share and made over 100%+ RoR in less than 24 months, I already had my "TRIM" targets ready for when this happened, and I ended up selling out the company before it went on the 15%+ RoR spree it has been since then.

However, while it's obviously worth taking a lesson or two from this development, I do not see the current forecast or environment as workable for the company to outperform in the longer term. While higher interest rates in some ways are a great net positive factor for insurance companies, they also come with some downside risks. I've been through clearly before that insurance companies and banks cannot be compared when it comes to their risks with unrealized losses in fixed income - I maintain this. But this is not the same as those unrealized losses, which are currently building up, as not having a valuation impact. The argument I've often fielded is that these losses not having a material impact on the fundamental safety of a company. They don't typically, and even less so than with banks, cause bankruptcies.

But they do affect valuation.

In this article, I'll explain to you why I remain at a "HOLD" on Unum.

Unum - Plenty to like - below $35/share.

Investing successfully in anything, but insurance as well requires a strong understanding of the dynamics as well as an iron stomach. This can be clearly seen as well as look at the trends affecting Lincoln National ( LNC ). Despite this company is in a not-completely dissimilar situation from Unum back when Unum was trading at sub-$20/share and certain analysts were arguing for bankruptcy.

This is how I invest in insurance companies. I tend to pick them up on the cheap, provided they have the fundamentals that I am looking for, and then rotate them when I believe they've cycled as high as they can realistically go.

With Unum's current situation, I say that Unum is a foundationally safe business. It's going nowhere, in terms of dire risk. If you want to get a sweet, sweet yield of 3% while making annualized RoR of 5.17% inclusive of company dividends, then Unum is "your gal".

My question is, why on earth would you want to make an annualized dividend-inclusive RoR of 5.17% when you can get 5-6% risk-free and 8-9% on investment-grade rated bonds and pref stocks?

Everything about investing comes to valuation - what you pay versus what you believe that the company can deliver.

Unum is a qualitative company - I've been through that discussion numerous times, I've not changed my stance a whit on this point.

But investing in a good company is not enough. Unless you invest at the right price, you're going nowhere. Microsoft ( MSFT ) is undoubtedly a good company, but if you invested at dot-com bubble valuations it would take a very long, long time to become profitable here.

So, valuation.

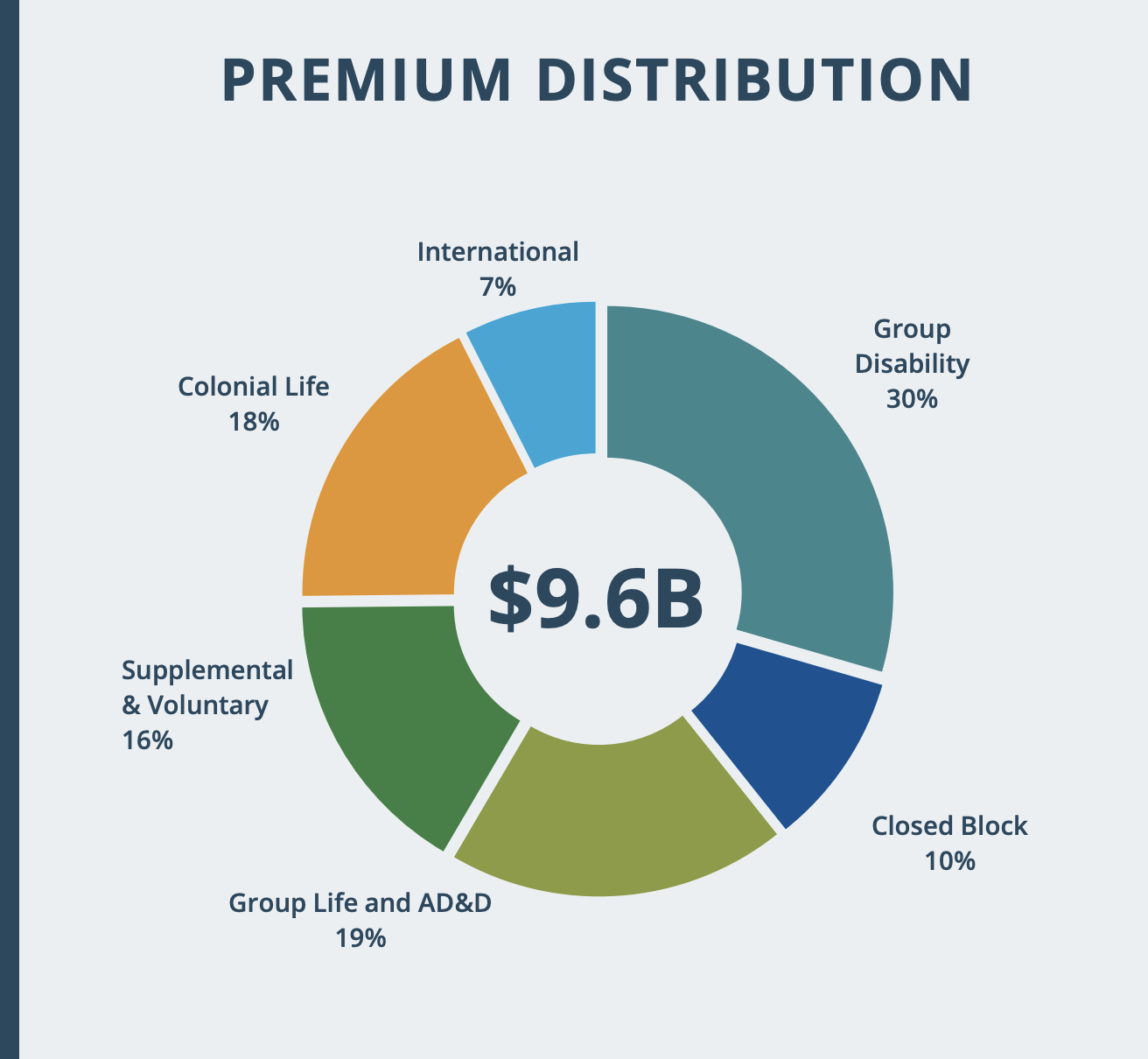

Unum has reported 2Q23 and has delivered a 2023E outlook. The outlook is good. The company has come out of the pandemic a powerhouse, managing over $1.25B in after-tax adjusted op. earnings, over $12B in revenues, and a RoE of 11.6% with a BV of $60.45. The premium distribution for the company is looking stellar.

{kind=link}

Little of what made many analysts leery about Unum remains. It's very "popular" to like Unum here. The problem that is seen is, that this is exactly what I saw several years ago. I could not tell you when this would occur - no one could. I could not guarantee anything - no one can. But I could see with a high enough conviction this scenario materializing, to where I invested tens of thousands of dollars in it happening.

Because Unum, at its heart, is a very capable and qualitative business (just as LNC is).

{kind=link}

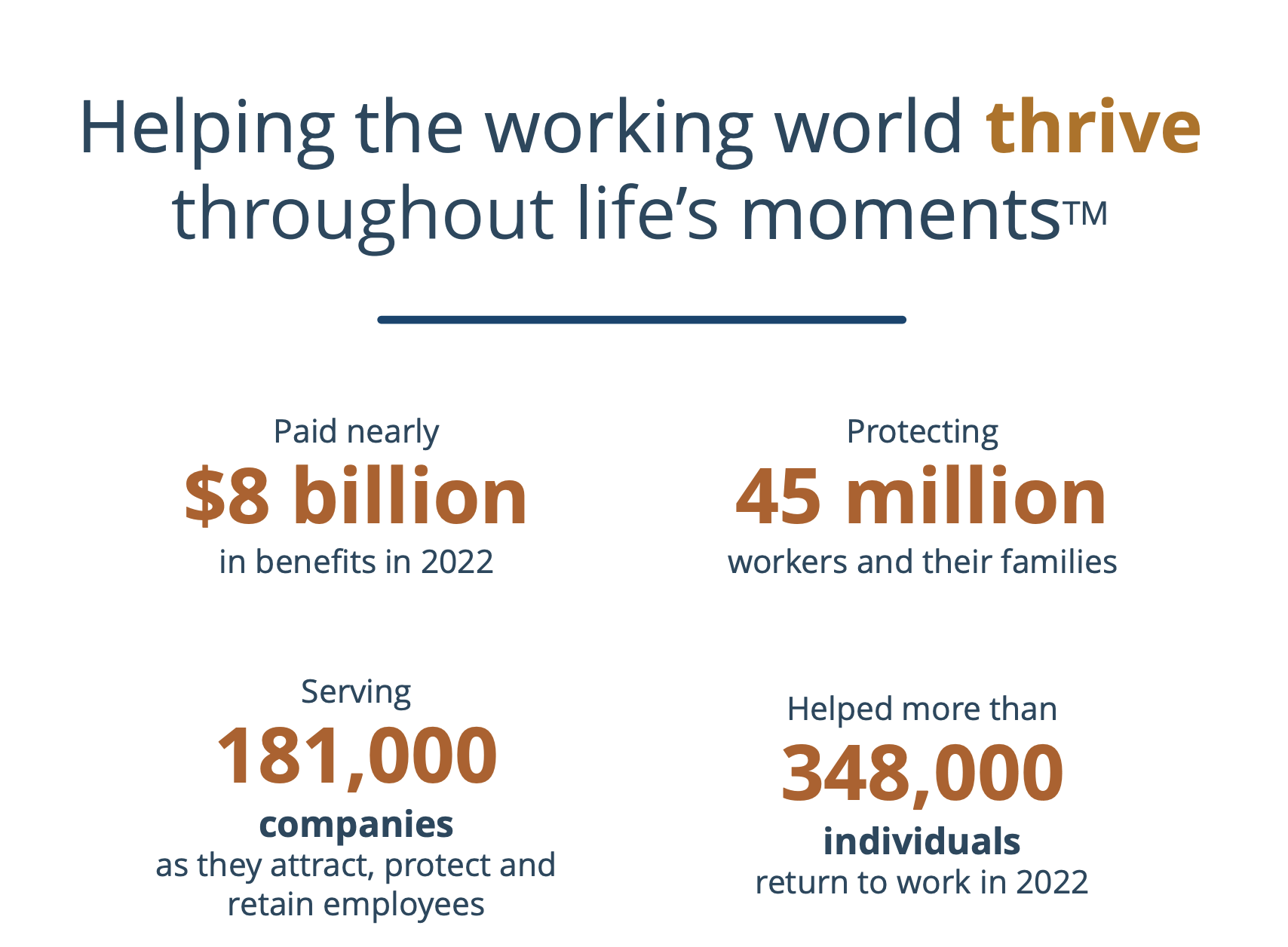

There is an addressable market for Unum which means the company has its work cut out for it. A higher amount of uncertainty, as we're moving into, will result in higher needs for the company's products and services. According to Unum statistics, 63% of people live paycheck to paycheck, 25% of workers will at one point or another be disabled, and 10% of workers are on family leave at any one time. The company's position in this value chain between employer and employee as a provider is very attractive.

Unum is a market leader. It's #1 in US disability, #1 in UK Disability, #2 in Voluntary benefits and #4 in life insurance. Every factor of its business model and results confirms the company's resilience over time.

{kind=link}

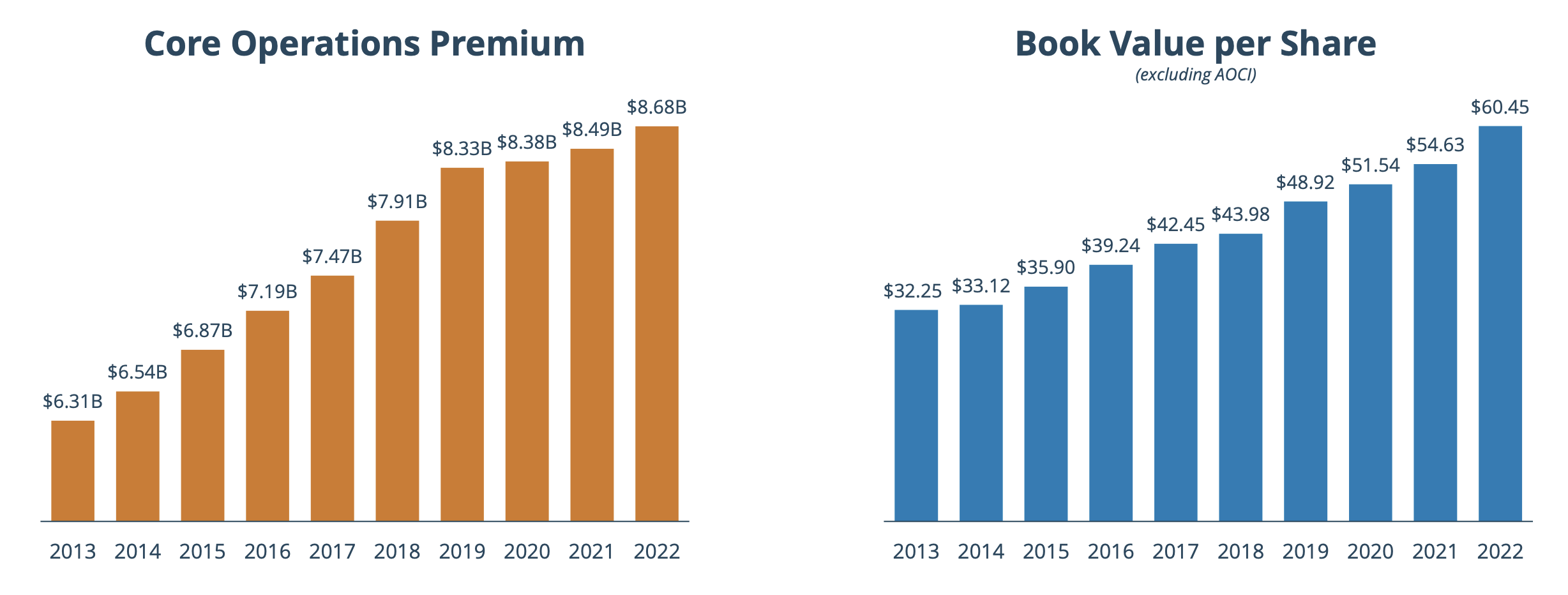

It's also come out of 2022 with the strongest capital profile it has ever had , with 420% RBC, $1.6B in company cash, leverage of below 24%, and a 10% dividend increase. Again, the problem is that while I could not estimate the specifics here, it was already "clear" that during the worst of the downturn when Unum traded at less than 2x P/E, this was the likely outcome.

Going against the grain is both a science and an art if doing it profitably. I by no means claim an unfailing ability to do so, but I claim the track record of doing so in this case - and it is the reason why I am not particularly interested in buying this recovered insurance company at a rather expensive valuation.

There are insurance companies that are playing other parts of the cycle, which makes them far more attractive to me at this time.

Some would say that Unum is not investable due to the unrealized losses in the company's investments. That is not what I say, because that is not how insurance companies typically work. They are not banks. Interest rate increases typically end up, historically, as a net positive but a short-term to medium-term negative or drag on the company's valuation, typically. And Unum is already valued at fairly high levels.

Let's look at what sort of valuation this current situation gives us, and why this is so unattractive to me, despite this company being in such a good situation.

Unum - Plenty to like - just not at this price.

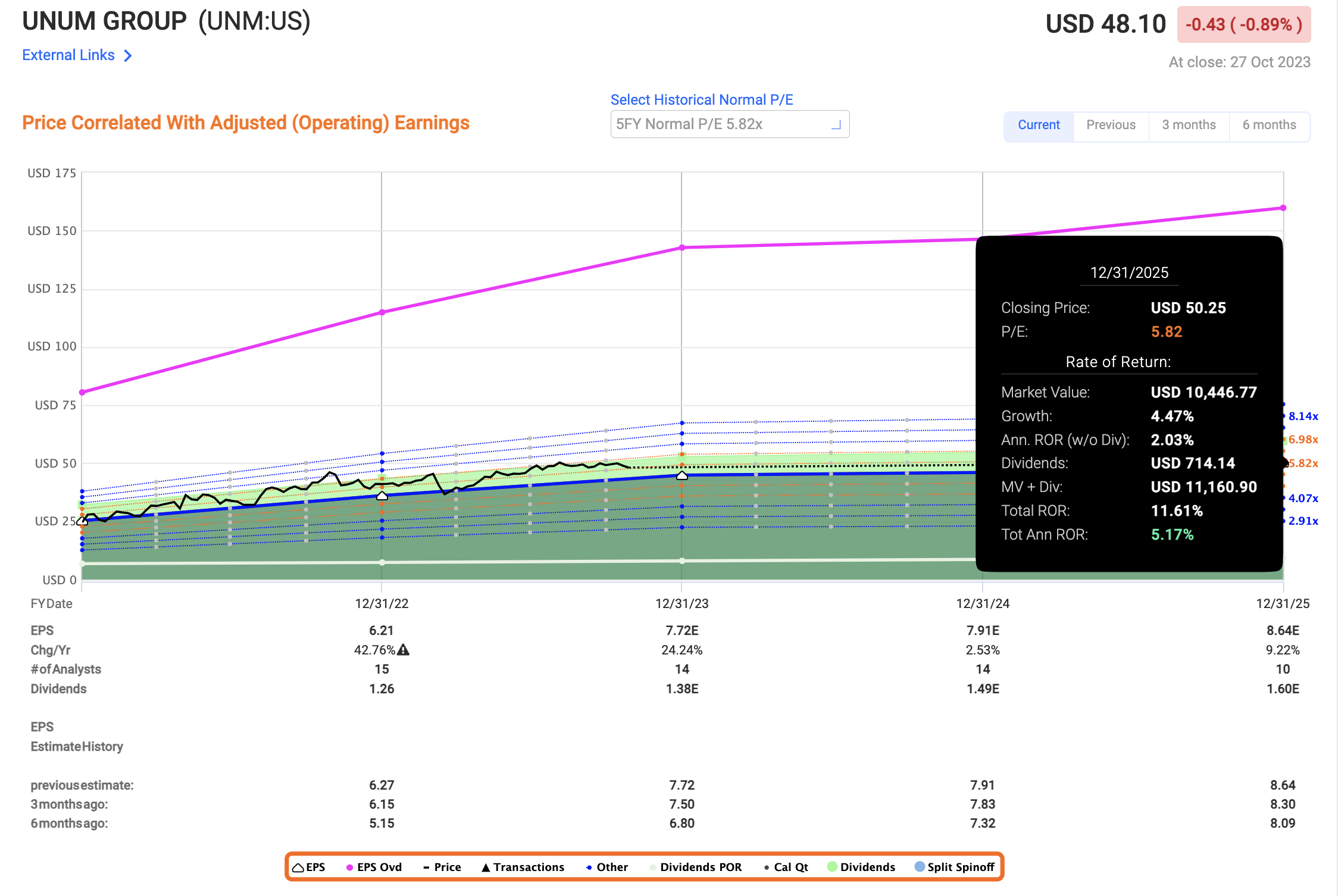

my last price target on Unum was $35/share or below. It should not surprise those of you familiar with, or following my work, that I am sticking to this price target. Nothing has changed for me here. Unum is currently trading at over $48/share, which I view as an overvaluation relative to what I say Unum is capable of. In the last 20 years, Unum has only traded above 6-8x P/E for momentary amounts of time, and in the last 10, that discount has widened.

The 5-year average is below 6x - the 10-year average is around 7.5x. even at 6-7.5x average, which by the way would imply close to a 100% book value for the company, Unum has less than 15% annualized upside inclusive of dividends. And that is with a 7x+ P/E, which the company has not managed in several years.

At 5-6x P/E, which I view as more realistic in the short to medium term, this is the likely outcome based on close to 6x.

{kind=link}

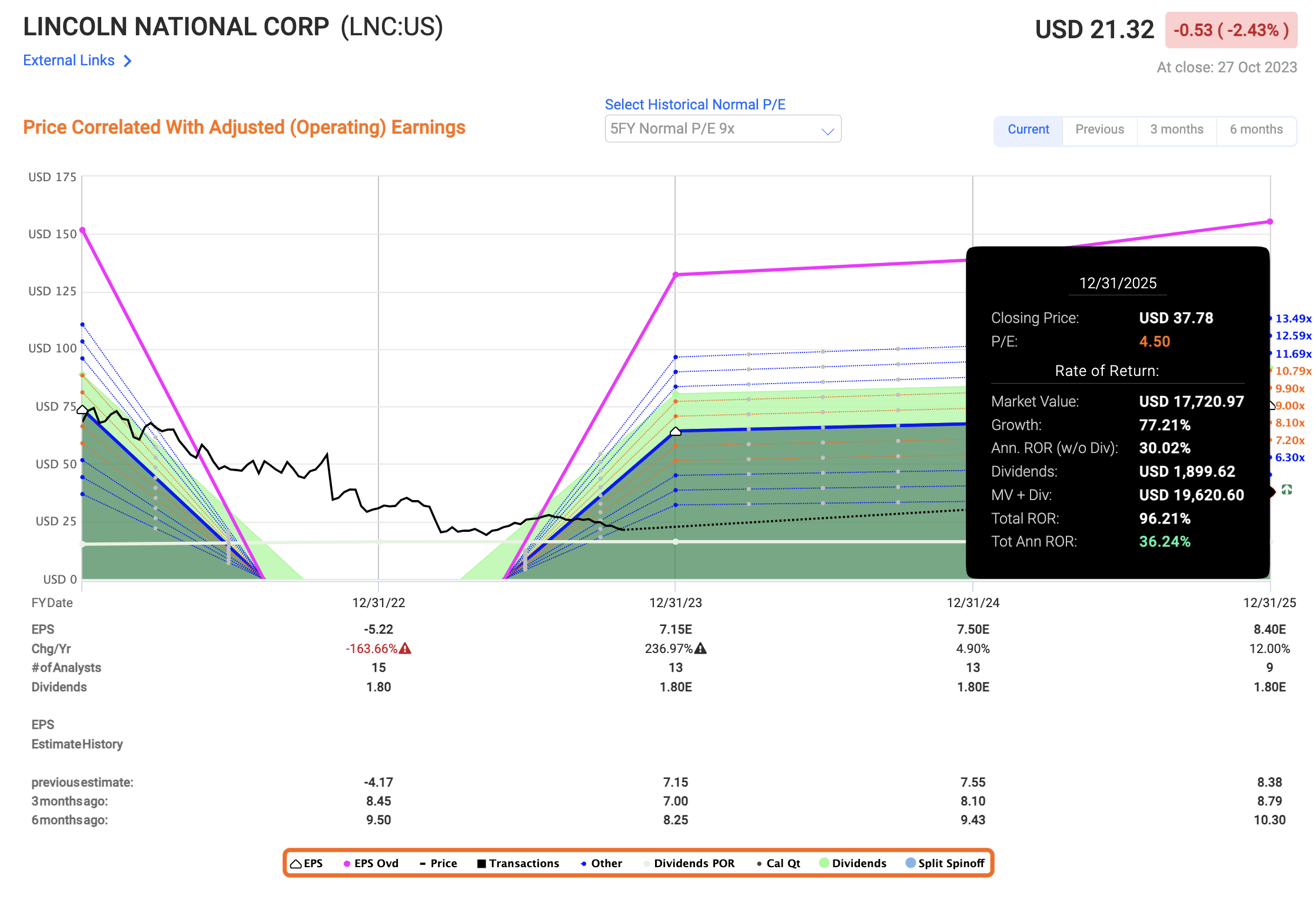

This is, of course, neither attractive nor market-beating. Is it impossible? No, nothing is impossible - Unum could rise to $60/share. However, I would rather invest my capital in companies or investments that I see have a better chance of outperforming their discounts or the market. LNC is one such business.

It now trades at 4.3x P/E due to a material collapse in the 2022A earnings that I have covered - but recovery is already ongoing, at least insofar as earnings and fundamentals go.

LNC has an even better-starting position than Unum. It's still BBB+ rated despite the ongoing challenges, and it now yields over 8.4%, a dividend that by the way even with the current estimated EPS is more than well-covered, and is this high due to the sheer discount of the company.

You could, theoretically, forecast LNC at 4.5x P/E, and still end up with a double-digit RoR - and not just any double-digit RoR.

{kind=link}

No, we're talking almost triple-digit RoR to a 4.5x P/E on a 3-year basis. In the case of any amount of long-term normalization, value-conscious investors such as myself have the potential to make not 100%, but 273% to a 9x P/E . Unrealistic, maybe - at least from the current perspective. But back when Unum was trading for comparatively pennies on the dollar, the arguments were similar at that point.

So, Unum isn't in a great investment position if you compare it to LNC at this time. There are numerous other insurance companies, in fact, that offer far more favorable upsides than Unum. If you're willing to "go to Europe", AXA ( OTCQX:AXAHY ) is another one that trades at A+ fundamentals, a 6%+ yield, again well covered, that to a 9x average has an upside until 2025E of 18% per year.

The simple fact is, dear readers, I see no reason to invest in Unum here. But I see reasons to invest in other parts of the insurance industry.

So that is what I am doing.

Thesis

My view on Unum is currently as follows:

- Unum is a theoretically appealing insurance company, but it no longer has a significant upside in terms of valuation.

- However, this upside is now more based on earnings growth than on reversal - and ideally, I want both when I invest.

- Unum is now a "HOLD" with a PT of $35/share, and I would still consider other investments significantly above Unum at this valuation and upside.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion

For further details see:

Unum: Definitely A 'Hold' Here