UNM - Unum Group Stock: Buy For Potential Upside And Stable Dividend

2023-08-18 11:00:35 ET

Summary

- Unum Group has delivered strong quarterly results and is expected to sustain this performance due to favorable industry trends and strong capabilities.

- I believe the company can maintain its quarterly dividend of $0.365 as well, which can make the annual dividend $1.39, representing a dividend yield of 2.83%.

- After comparing the forward P/E ratio of 5.98x with the industry average P/E ratio of 8.74x, I think the company is undervalued.

Investment Thesis

Unum Group ( UNM ) deals in financial insurance products and operates in the United States, the United Kingdom, and Poland. The company has delivered strong quarterly results and I believe it can sustain this performance in the coming quarter as a result of favorable industry trends and its enhanced cloud-based technology. Further, this growth can help the company to sustain its high dividend payout.

About UNM

UNM mainly deals in offering financial insurance products which include group and individual income protection. The company operates in the geographic regions of the United States, the United Kingdom, Poland, and limited parts of certain other countries. It conducts its business in five reportable segments: Unum US, Unum International, Colonial Life, Closed Block, and Corporate. The Unum US segment includes various products such as group disability, Individual disability, Dental & Vision, Voluntary benefits, and group life & accidental death. This segment contributes 65.03% to the company’s total premium income. The Unum International segment comprises operations in Poland and the United Kingdom. The UK’s business includes insurance products of Group Life, Group Long-term Disability, and Supplemental. The Poland business offers whole life insurance covering accidental and health riders. This segment represents 7.46% of the company’s total premium income. The colonial life segment offers a diverse range of products including Life, Cancer & Critical Illness. This segment generates 17.68% of the total premium income. The Closed Block segment includes Group and Individual Long-term Care in addition to other insurance products that are no longer marketed. This segment earns 9.81% of the total premium income. The Corporate segment consists of investment income, expenses on corporate debt, and other income from corporate sources which is not allocated to a line of business.

Financials

UNM has recently reported its strong quarterly results . It reported revenue of $3.11 billion, up by 2.38% compared to $3.03 billion in Q2FY22. Positive underlying trends, especially in disability products, and an advantageous operating climate were the key drivers of the growth. The company reported a premium income of $2.51 billion which is 3.85% growth compared to $2.42 billion. UNM has managed to surpass the market’s revenue expectations by $20 million or 0.65%. The firm's net income for the second quarter rose 6.96% YoY from $0.36 billion to $0.39 billion. It reported a diluted EPS of $1.98. The company exceeded the market’s EPS consensus in Q2FY23 by $0.20 or 11.24%. Adjusted operating income stood at 0.40 billion. Book value per common share was $47.06 in Q2FY23, rise of 21.0% from the corresponding period last year. UNM reported $1.1 billion in liquidity and total debt stood at $3.43 billion.

The insurance industry was highly affected by inflationary pressures and geopolitical issues in the last year. It increased the costs for insurance companies arising from claim payouts. In addition, many customers are likely to switch policies or withdraw their coverage during a recession. However, this year it has remained resilient despite the headwinds. According to the Swiss Re Institute , In 2022, the US was the largest insurance market in the world in terms of premium volume with 43.7% of the global market share. The United Kingdom stood at third position on the list. The number of nonelderly uninsured people was rising constantly from 2017 to 2019. However, it fell by approximately 1.5 million in 2021, from 28.9 million in 2019 to 27.5 million in 2021. This data shows the growing need for insurance after the pandemic. In addition, technological advancements can play a crucial role in the evolution of the industry as many technological tools such as data analytics and cloud computing can increase the insurer’s efficiency by increasing its market penetration and managing its data which can further help to profit margins.

Identifying these scenarios, the company is highly focused on expanding its cloud-based HR technology which I believe can accelerate the company’s growth by increasing its reach within the employer group and make it well-positioned to capture the additional market share by penetrating deeper into the markets by leveraging technology. In 2022, the company managed to add 20,000 small business customers which shows its increased reach in the market. As per my analysis, the company’s strengthening of technological advancement can give it a competitive advantage over the insurance companies which still relies on traditional operating methods as it can monitor and expand its activities with greater ease as compared to traditional methods.

I also believe that demand can sustain in the future as a recent study conducted by LIMRA shows that an all-time high interest is reported for life insurance in 2023. Within the following year, 39% of Americans plan to get life insurance. This statistic indicates that the insurance sector is under-penetrated and that there are several prospects for industry participants. I think the company’s strong technological capabilities can significantly help it to increase its customer base which can further benefit it to generate additional premium income and expand its profit margins. The company is also confident about its future growth and expects that sales volume can rise by 8%-12% in 2023 .

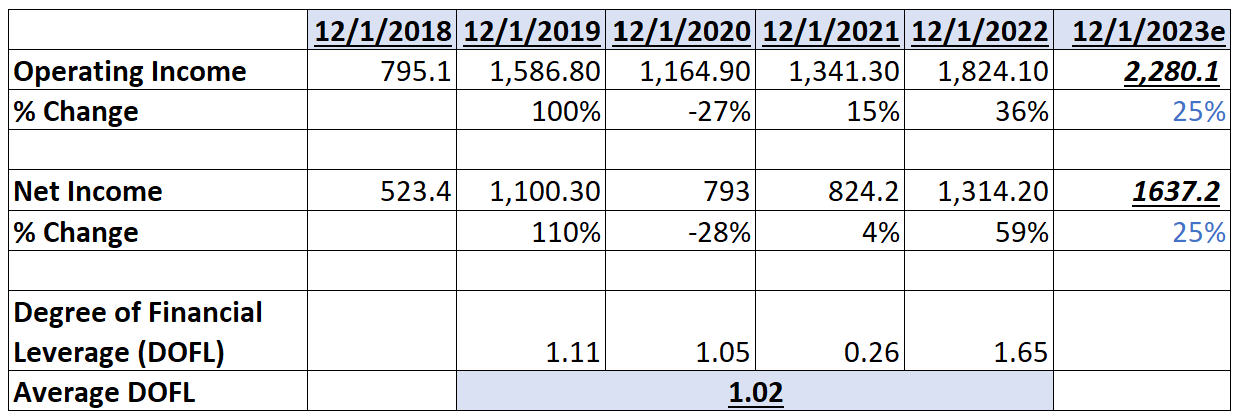

The firm has reported healthy results and I believe it can sustain this performance in the future as it is highly focused on expanding its cloud-based HR technology to increase its reach in the rapidly growing market. The company estimates that operating income per share can increase by 20%-25% for FY2023 compared to the previous year. Observing the growth potential and overall performance up to the second quarter I believe the estimate of 25% growth is correct. If we analyze the last five year’s financials, we will find that the company’s 5-year average degree of financial leverage (% change in Operating Income divided by % change in Net Income) is 1.02x.

{kind=link}

According to my estimates of 25% YoY growth of operating income, we can expect operating income to reach $2.28 billion in FY2023. The net income might be $1.64 billion as the degree of financial leverage of 1.02x, which gives the net income growth of 25%. The estimated net income of $1.64 billion results in EPS of $8.19.

Dividend Yield

{kind=link}

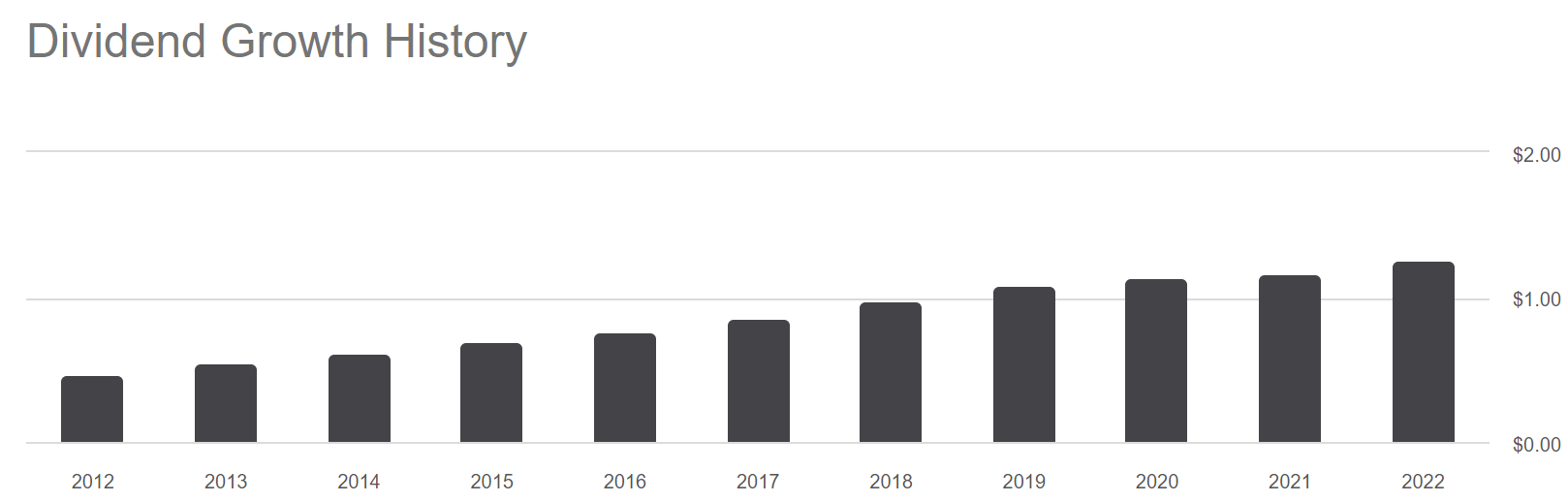

UNM has a remarkable record of dividend payouts . The company has paid a dividend to its investors for 23 years consecutively which shows the consistency of dividend payments. In 2022, UNM paid a dividend of $0.30 in the first quarter and sustained it for the second quarter as well. It paid $0.33 in each of the remaining two quarters. This dividend payout totaled $1.26 per share annually resulting in a dividend yield of 2.57%. In 2023, it paid a $0.33 per share cash dividend in the first two quarters. In the third quarter, this dividend increased to $0.365, and observing the company’s strong liquidity and healthy growth in premium income, I believe, it can maintain its quarterly dividend of $0.365 in the last quarter as well which can make the annual dividend $1.39, representing a dividend yield of 2.83% compared to current share price of $48.95. This appealing dividend yield makes the firm an attractive stock to hold in the portfolio, especially for risk-averse and retired investors who are looking for stable income.

What is the Main Risk Faced by UMN?

As the company operates in the insurance industry it is exposed to the risk of reinsurance. Reinsurance is utilized for various reasons such as to cover specific risks from its various businesses and to exit certain lines of businesses. The cost and availability of reinsurance depend on multiple market factors which are beyond the company’s control. If the reinsurance amount decreases, it may affect the company’s capital requirements. In addition, if the cost of reinsurance increases, it might affect the company negatively by increasing its expenses. This rise in expenses can further contract the company’s profit margins.

Valuation

The growing demand in the industry has created large opportunities for the company to grow and I believe the company’s continuing focus on cloud-based HR technology & geographic presence can help it to cater to the growing demand and help to increase its customer base which can further increase its profitability. After considering all the above factors and estimated operating income and degree of leverage, I am estimating EPS of $8.19 for FY2023 which gives the forward P/E ratio of 5.98x. After comparing the forward P/E ratio of 5.98x with the industry average P/E ratio of 8.74x, I think the company is undervalued as it is trading 31.6% below the average P/E ratios of all the companies in the industry. I believe the company might grow in the coming quarters as a result of rising demand in the life insurance sector and its expanding digital cloud-based capabilities which can help it to trade at the industry P/E ratio. I estimate the company might trade at a P/E ratio of 8.74x in FY2023, giving the target price of $71.58, which is a 46.23% upside compared to the current share price of $48.95.

Conclusion

UNM mainly deals in financial insurance products and it is experiencing a healthy demand which is also reflected in its strong quarterly results. I believe it can continue to perform better in the coming quarters as its expanding digital capabilities can enable it to capture additional market share by increasing its global reach. However, it is exposed to the risk of an increase in reinsurance cost which can contract its profit margins. The company also pays a decent quarterly dividend which makes it an attractive stock to hold in a portfolio. The stock is undervalued and I believe we can expect a healthy 28%-30% growth from the current price levels as a result of its continuous strong performance over the past few quarters and its enhanced digital capabilities. Considering all these factors, I assign a buy rating to UNM.

For further details see:

Unum Group Stock: Buy For Potential Upside And Stable Dividend