ANDE - Up 70% This Year: Why I'm Still Bullish On The Andersons

2023-12-31 05:24:29 ET

Summary

- The Andersons, a diversified agriculture company, has seen its stock rise close to 70% this year.

- The company's Renewables segment had a record quarter, driven by strong crush margins and efficient ethanol production.

- The Trade segment faced challenges, but the Nutrient & Industrial segment reported positive trends with improved margins.

Introduction

It's time to talk about a company I have consistently covered since I started to turn bullish on agriculture and energy stocks in 2020. That company is The Andersons ( ANDE ) , a fascinating diversified agriculture play from Maumee, Ohio.

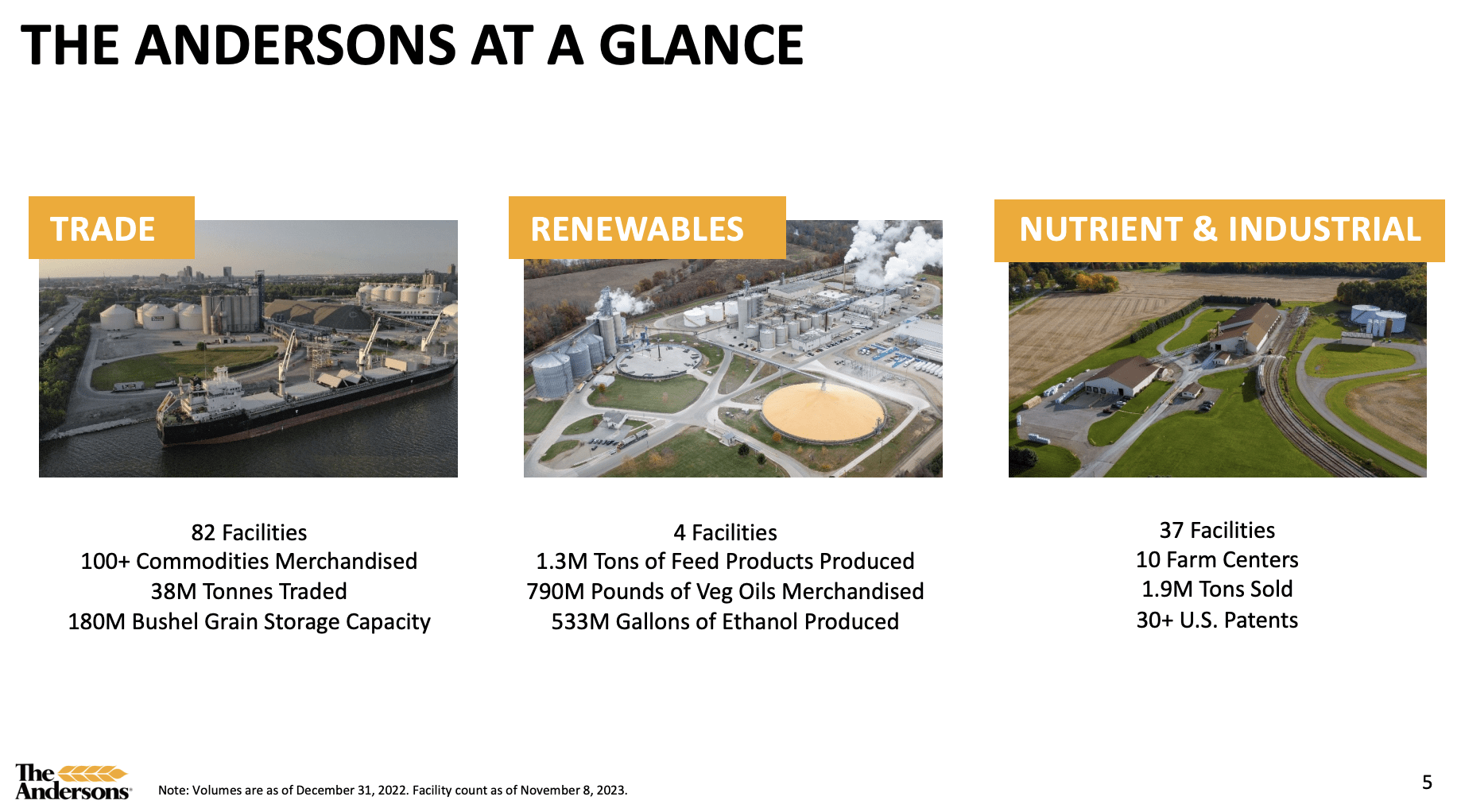

The company has a well-diversified business model that includes Trade, Renewables, and Nutrient & Industrial, meaning it sells fertilizers to farmers, trades and stores crops using its 82 facilities, and produces ethanol in one of its four facilities capable of producing more than 530 million gallons per year.

{kind=link}

This year (it may be 2024 when you're reading this), the stock is up close to 70%, making it one of the best performers in agriculture.

On May 5, 2022, I wrote that the stock had room to run to the range of $65 to $70.

I still believe that the fair value of this company is between $65-$70. However, after the sell-off, I doubt we'll see that number this year unless something truly crazy happens. I think we could see it at the end of next year if the commodity supercycle in agriculture lasts.

Thanks to a 17% performance over the past four weeks, the stock has come very close to that range.

My most recent article was written on August 19, when I wrote that the stock had more than 50% upside.

Hence, in this article, I will use recent developments and ANDE's valuation to make the case for even more long-term upside.

So, let's get to it!

Positive Developments Despite Tough Comparisons

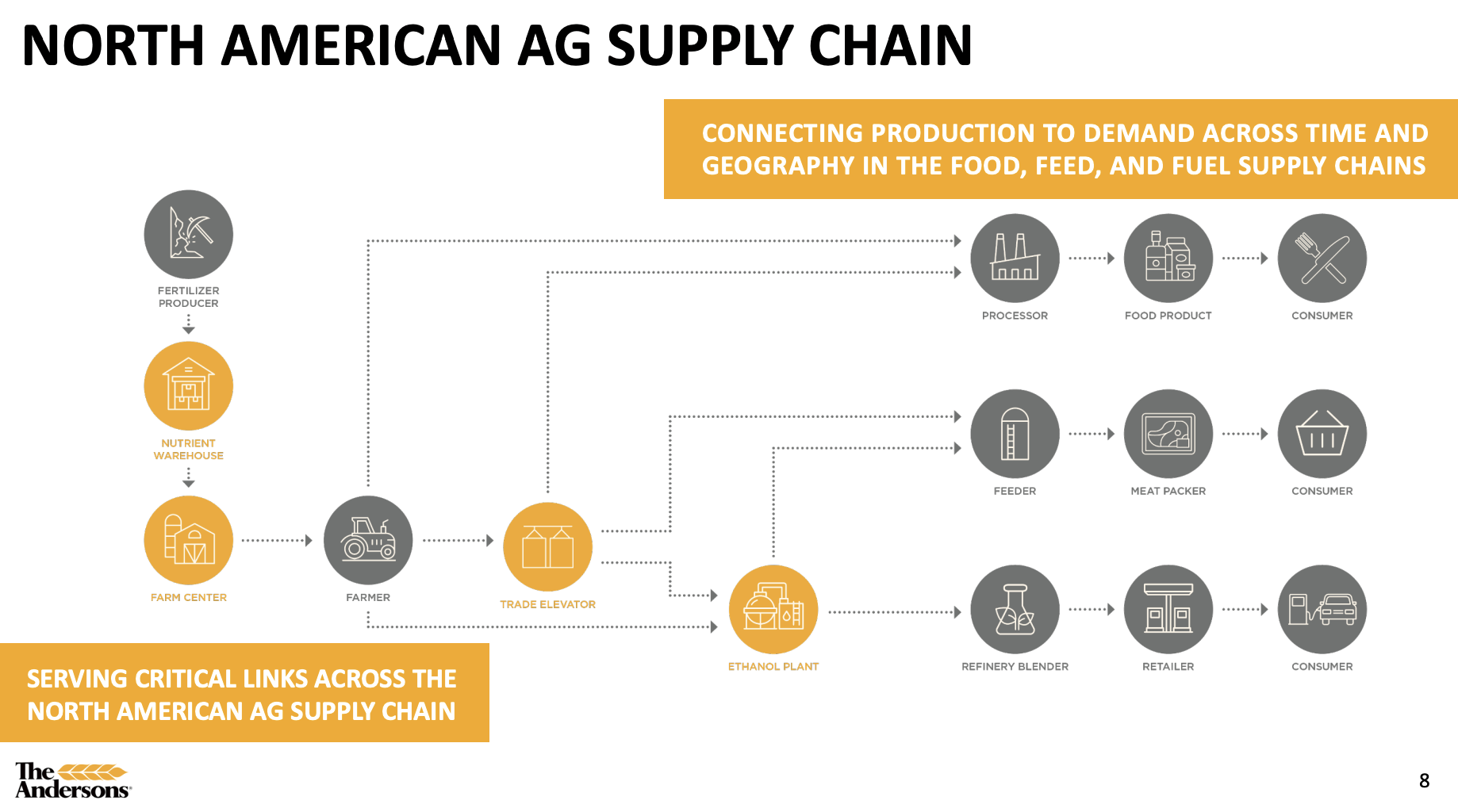

I already briefly mentioned it, but ANDE is everywhere in the agriculture supply chain. While it does not produce tractors, equipment, or fertilizers, it connects buyers to sellers, turns corn into energy (ethanol) and by-products, and helps farmers store crops and buy fertilizers.

{kind=link}

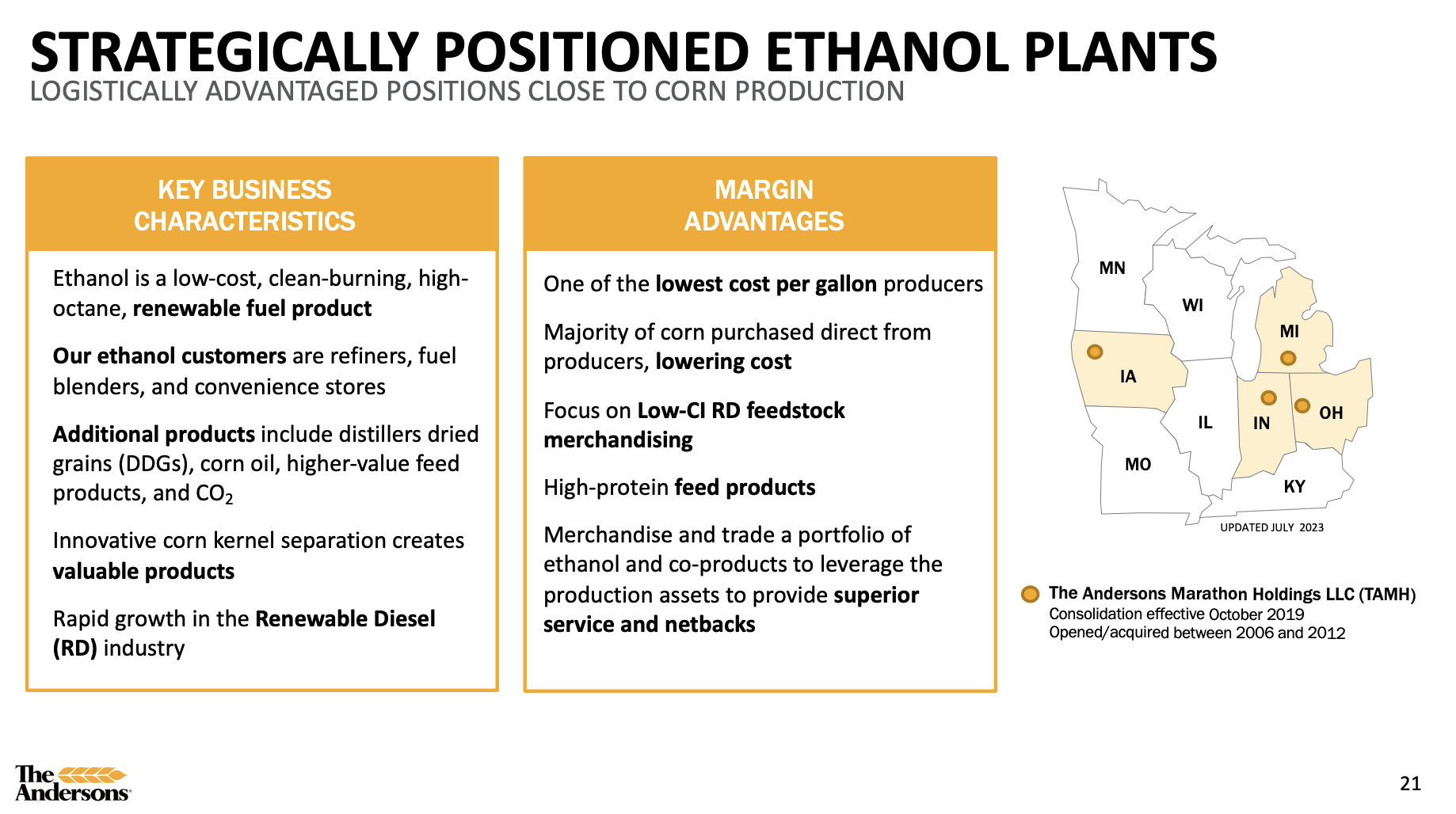

To give you an example of my favorite segment, Renewables, the company produces more than 530 million gallons of ethanol per year. It produces side products like feed products. It can produce 1.3 million tons of feed products and vegetable oils like corn oil.

It is so large that it is the fifth-largest ethanol producer in the U.S., with benefits like lower costs per gallon and higher quality by-products.

{kind=link}

Right now, this business is booming, although it may not look like it because 2022 was also such a strong year.

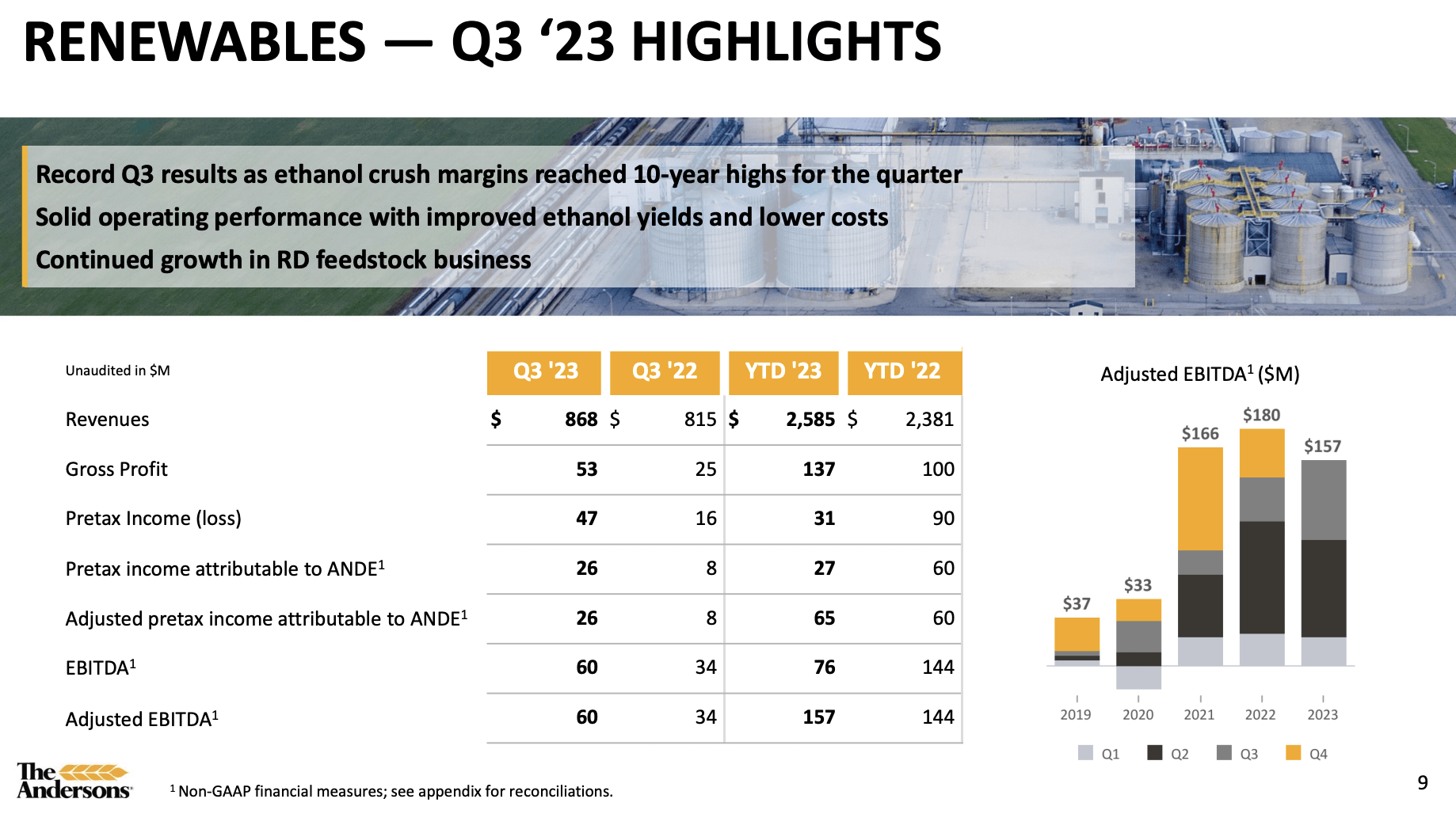

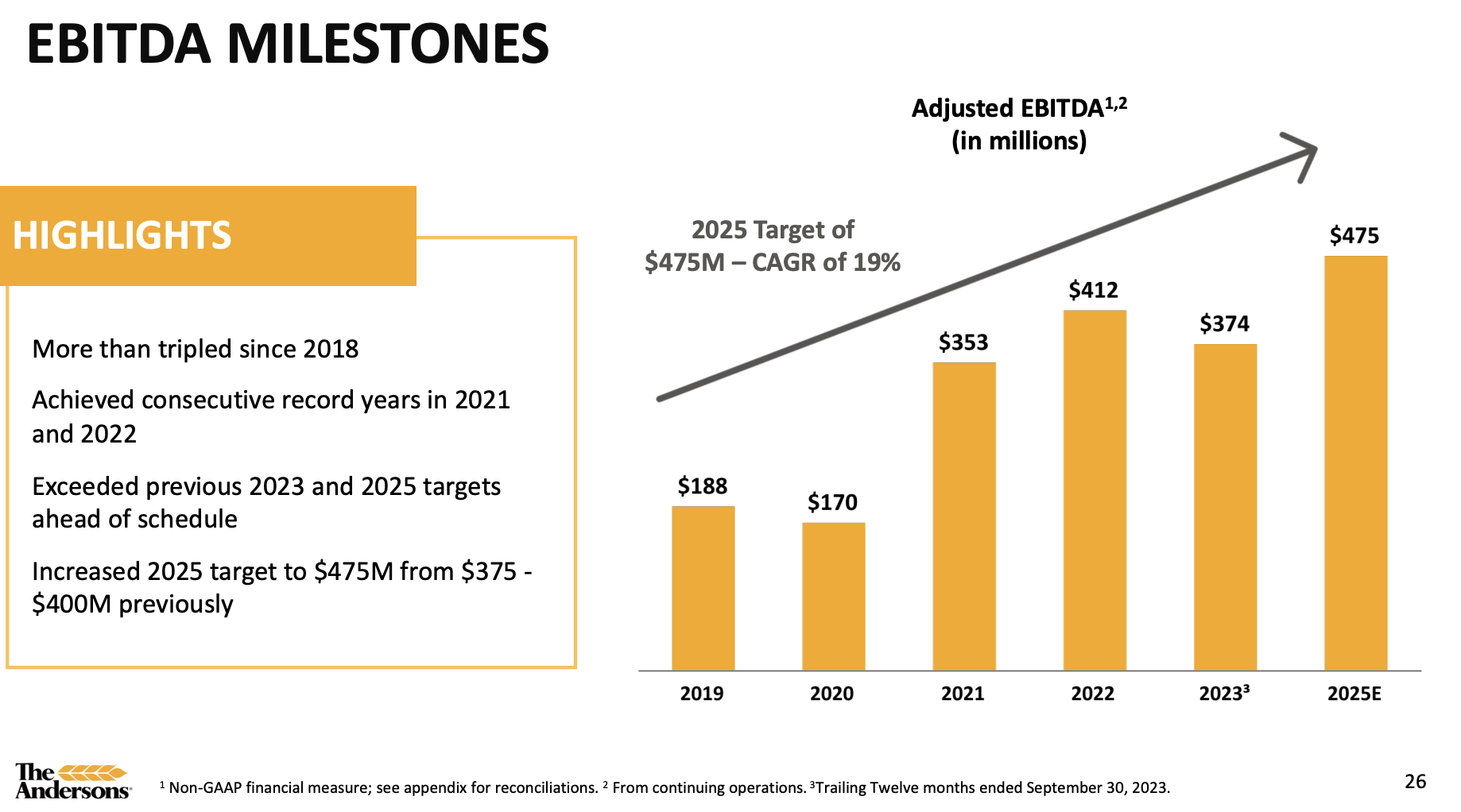

The third quarter of 2023 saw solid results for the company compared to the best-ever third quarter of the previous year. While YTD adjusted EBITDA from continuing operations fell from $308 million to $270 million, it remains well above pre-2021 levels.

The Renewables segment notably had a record quarter, outperforming expectations, with exceptional results attributed to strong crush margins and efficient operations in ethanol production.

{kind=link}

Merchandising results for renewable diesel feedstocks also showed substantial improvement, contributing to the overall positive performance.

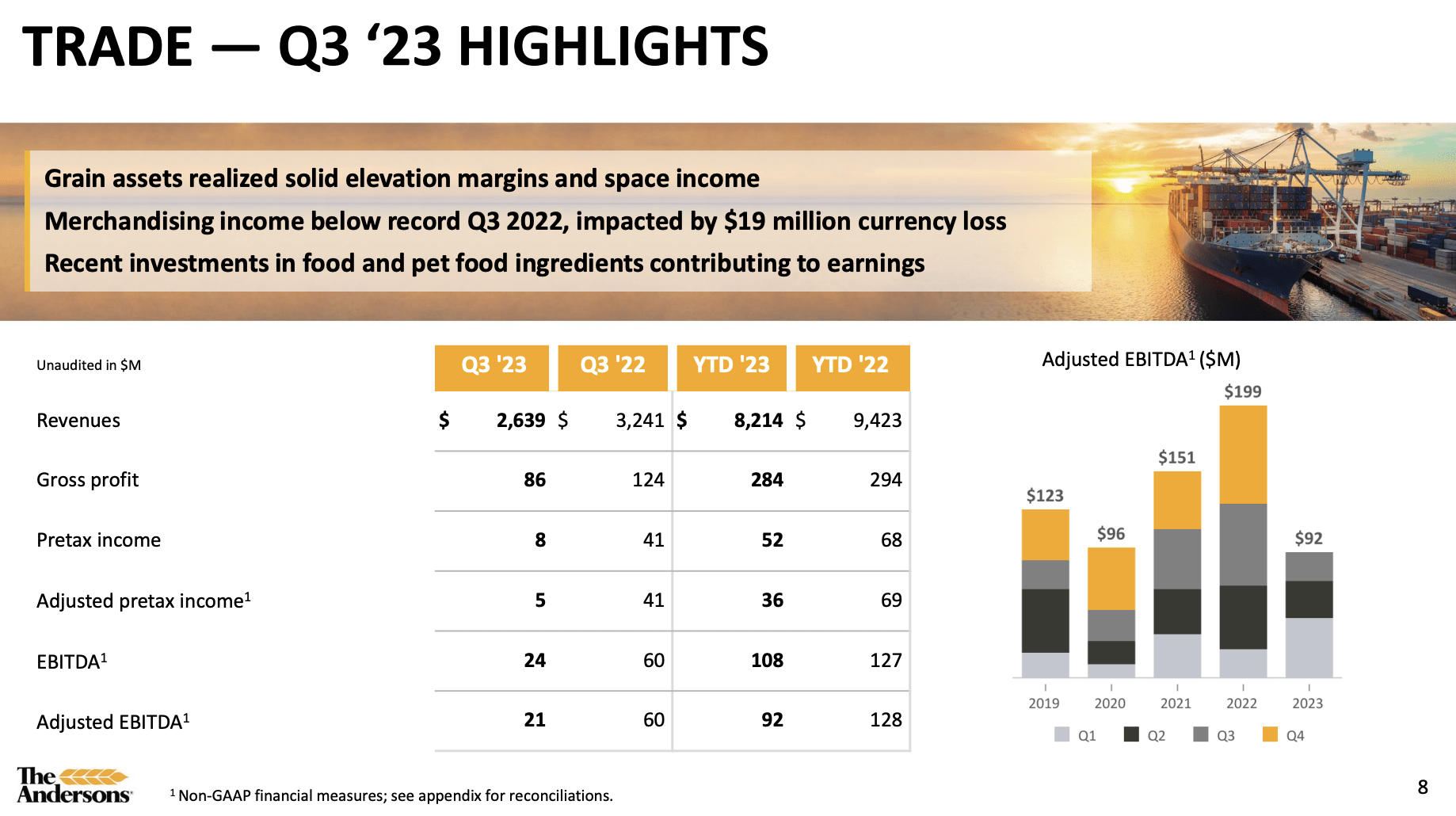

However, the Trade segment faced challenges, with results down compared to the exceptional third quarter of 2022.

Various factors, including atypical charges and a less dynamic U.S. grain market, contributed to the decline.

{kind=link}

Nonetheless, the North American assets and recent investments in premium food and pet food ingredients showed improvement.

Unfortunately, the Middle Eastern and North African businesses experienced a currency-related loss in Egypt, impacting merchandising results.

Personally, I'm not worried about any of this, as currency headwinds were still small, and 3Q22 was a very tough comparison period.

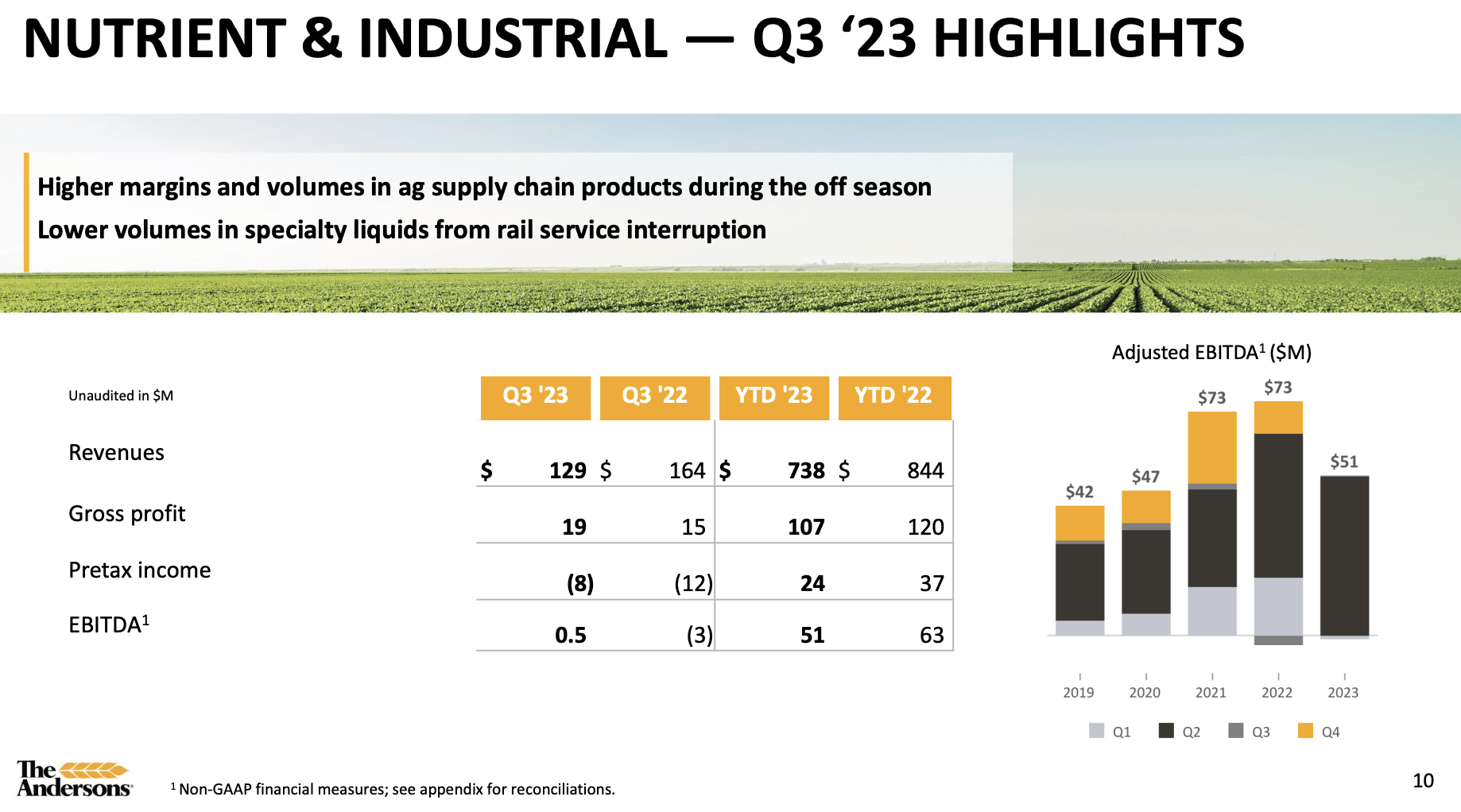

Last but not least, the Nutrient & Industrial segment reported positive trends, with improved margins in the seasonally quiet quarter.

While volumes in the ag supply chain increased, challenges such as a rail disruption affected specialty liquids, and manufactured products were lower due to slow consumer demand.

Despite these challenges, positive EBITDA for the quarter marked an improvement from the same period in 2022.

{kind=link}

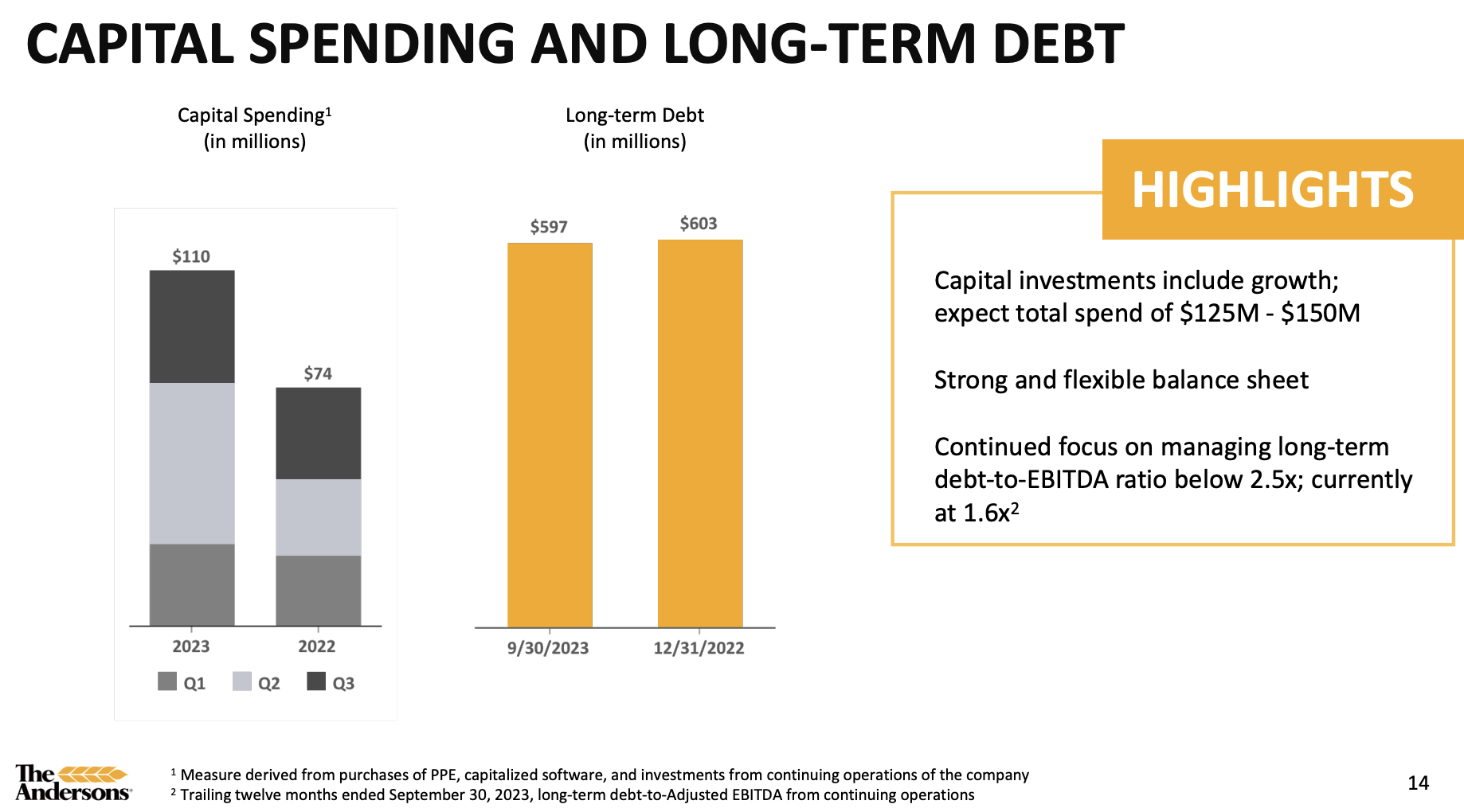

Adding to that, the company has a healthy balance sheet. It maintains $600 million in long-term debt and a 1.6x long-term leverage ratio, which is below its target, meaning it has room for investments and/or a buffer in case it were to face falling EBITDA in the future.

{kind=link}

Furthermore, the company remains very upbeat about its future, which matters more than anything else.

The Future Looks Bright

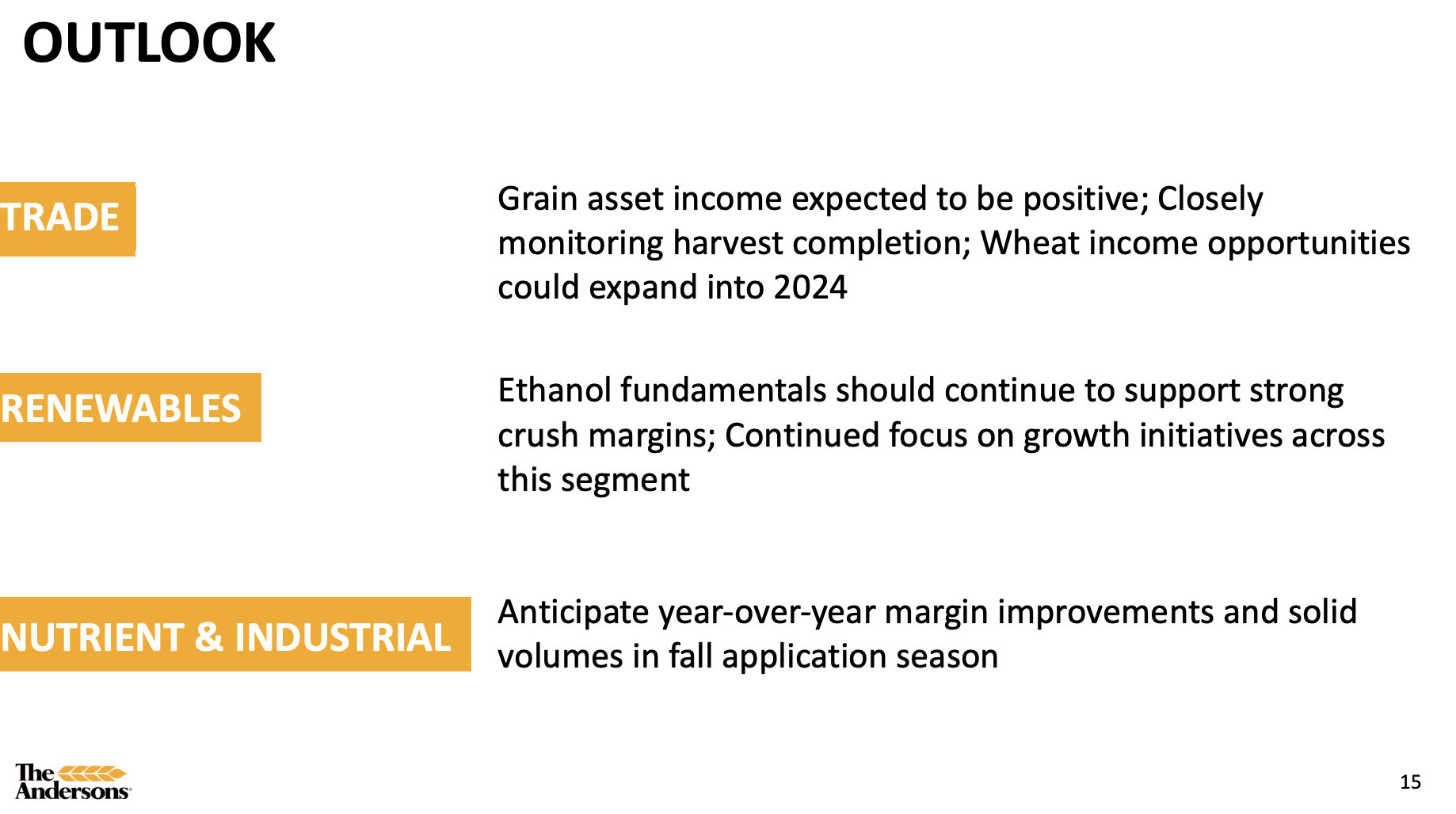

During its earnings call, the company expressed a positive outlook for the company's 2023 EBITDA, expecting to meet or exceed the $350 million to $375 million range.

The optimism is driven by high U.S. agriculture production, particularly benefiting from a strong harvest and favorable grain asset footprint.

Despite projections of lower farm income due to commodity price decreases, farmers are anticipated to continue investing in crop inputs.

I can confirm this after having worked my way through countless agriculture-related earnings calls this year.

{kind=link}

Furthermore, the Renewables segment is seeing positive trends.

Investments in production facilities and increased fermentation capacity contributed to exceeding last year's fourth-quarter earnings.

The renewable diesel feedstock merchandising business shows growth, aligning with the company's growth strategy targets and efforts to lower carbon intensity with potential benefits from the Inflation Reduction Act.

In its Nutrient & Industrial segment, corn producers are expected to value specialty products, maximizing yield, and fourth-quarter demand is projected to improve over last year.

Going beyond 2023, the company aims to grow adjusted EBITDA to roughly $475 million, which would imply 19% compounding growth since 2019.

{kind=link}

Adding to that, the company's strategic move to directly engage with end-use customers in the Middle East and Africa presents significant growth opportunities.

The focus on building long-term relationships in regions with growing populations and increasing demand for grains and food positions The Andersons strategically.

While facing the aforementioned challenges in currency fluctuations, the company remains committed to this international strategy, viewing it as a forward-looking approach to tap into emerging markets.

On top of that, the company's emphasis on a balanced approach to investments, including both capital projects and mergers and acquisitions (M&A), provides diversification opportunities.

Successful integration of previous acquisitions, such as Bridge Agri and ACJ, demonstrates the company's capability to identify and capitalize on incremental, higher-return assets, which I expect to pave the road for long-term growth.

After all, the core business is a low-margin business. Using capabilities to expand into new areas that go higher up the value chain is a smart move.

Valuation

I stick to my belief that ANDE has a lot of room to run.

Using the data in the chart below:

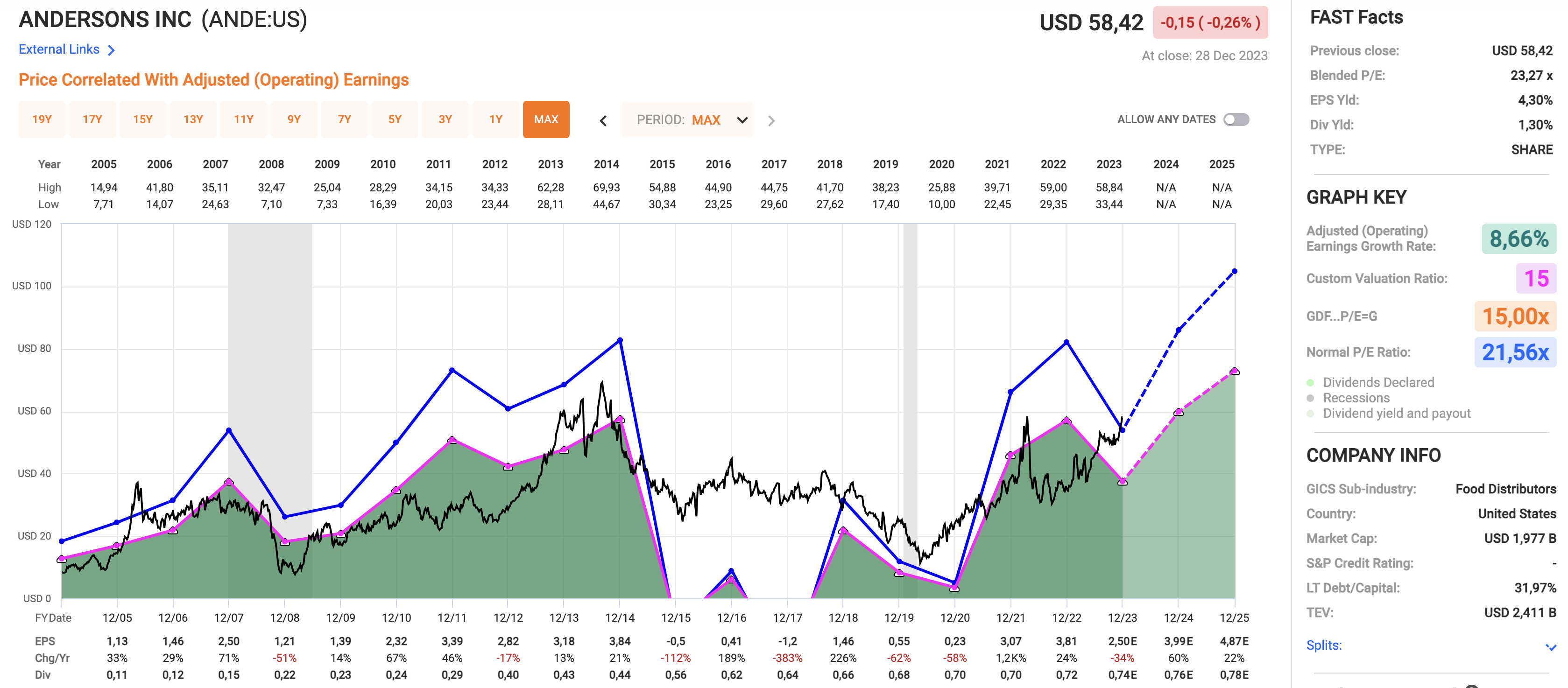

- ANDE is currently trading at a blended P/E ratio of 23.3x, which is partially caused by the expected 34% EPS decline this year (due to business normalization and a tough comparison versus 2022).

- In 2024, EPS is expected to increase by 60%, followed by a 22% surge in 2025.

- Historically speaking, ANDE has traded at a normalized multiple of 21.6x. However, this is highly skewed due to volatile earnings. I believe that a 15x multiple is more appropriate.

- Based on expected EPS growth and a return to a 15x multiple, the stock has a fair value of roughly $73, which is roughly 25% above the current price.

{kind=link}

All things considered, I remain long ANDE in my trading portfolio.

Bear in mind that it is not a holding of my dividend account. ANDE is volatile and unsuitable for conservative investors. If I weren't trading a few themes on the side, I would likely not own ANDE.

Nonetheless, the key takeaway here is that ANDE is still attractively valued after a stellar performance in 2023.

Takeaway

The Andersons continue to stand out as a compelling agriculture investment.

From a diversified business model to robust segments like Renewables, the company navigates challenges with resilience.

Despite headwinds in the Trade segment, positive trends in Renewables and Nutrient & Industrial segments paint a promising picture.

Meanwhile, ANDE's strategic outlook, focusing on international expansion and balanced investments in higher-margin areas, positions it for growth.

With a positive 2023 outlook and a fair value projection of $73, there's potential for further upside.

For those willing to embrace volatility, ANDE remains a captivating choice with room to run.

For further details see:

Up 70% This Year: Why I'm Still Bullish On The Andersons