DLAKF - Upgrading Lufthansa Stock To Buy

2023-05-08 17:35:09 ET

Summary

- Lufthansa missed on topline but beat expectations on topline.

- Management indicated that analyst consensus for the full year is conservative.

- I am upgrading Lufthansa stock to buy on continued demand strength and supply constraints.

Lufthansa ( DLAKF ) has been one of the European airlines that stood out for me, because of the way the company manages its liquidity and debt. Two or three years ago, the company was setting itself up for survival by taking on a lot of debt, and today, we see the airline deleveraging as it capitalizes on a strong demand environment for air travel. In this report, I will analyze the first quarter results.

Lufthansa Turnaround In Full Swing

{kind=link}

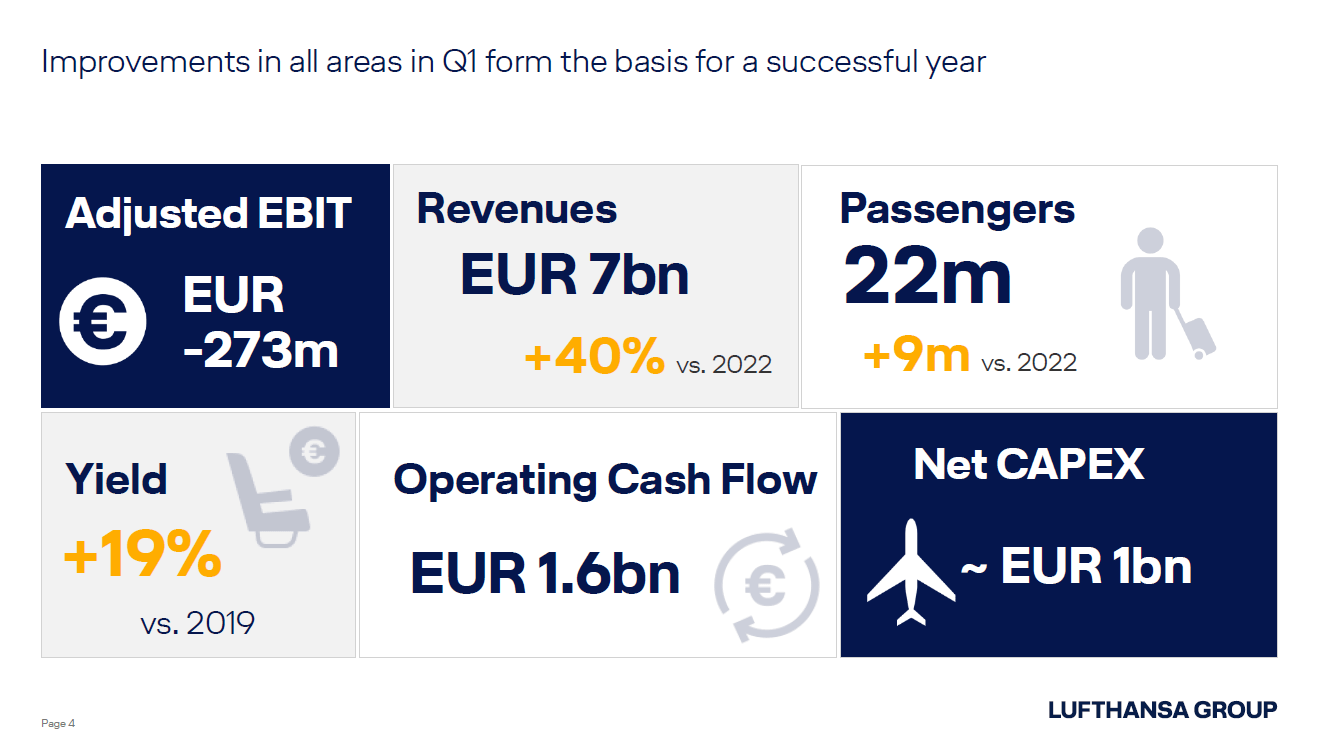

The slide above really captures the essence. The company saw passenger volume pop by 70% resulting in 40% higher revenues. At first sight, you might say that the revenue growth was somewhat underwhelming, but it should be kept in mind that Lufthansa also operates other businesses next to its passenger airlines. So, the full revenue growth figure is not fully reflective of passenger airline performance. MRO is a relatively stable business which saw 16% growth while logistics saw a 30% decline in revenues. So, those elements offset some of the growth relative to the passenger traffic growth.

Adjusted EBIT was a €273 million loss compared to €577 million loss a year earlier, marking a 53% improvement. From an earnings perspective, the MRO adjusted EBIT of €135 million showed 5% growth and the passenger segment saw 54% growth, seeing their operations become €602 million less loss-making. The gap between the reported numbers for the group is smaller at €304 million and so the full improvement in profitability for the passenger airlines wasn't visible on group level and that is because the cargo segment profits were €344 million lower. Were it not for the cargo segment, Lufthansa would have been soundly profitable during the quarter. Cargo operations have carried many airline operations during the pandemic, but while the business is doing better than in 2019, the reality is that extremely strong days for the cargo business are over, and we will see more normalized levels going forward.

{kind=link}

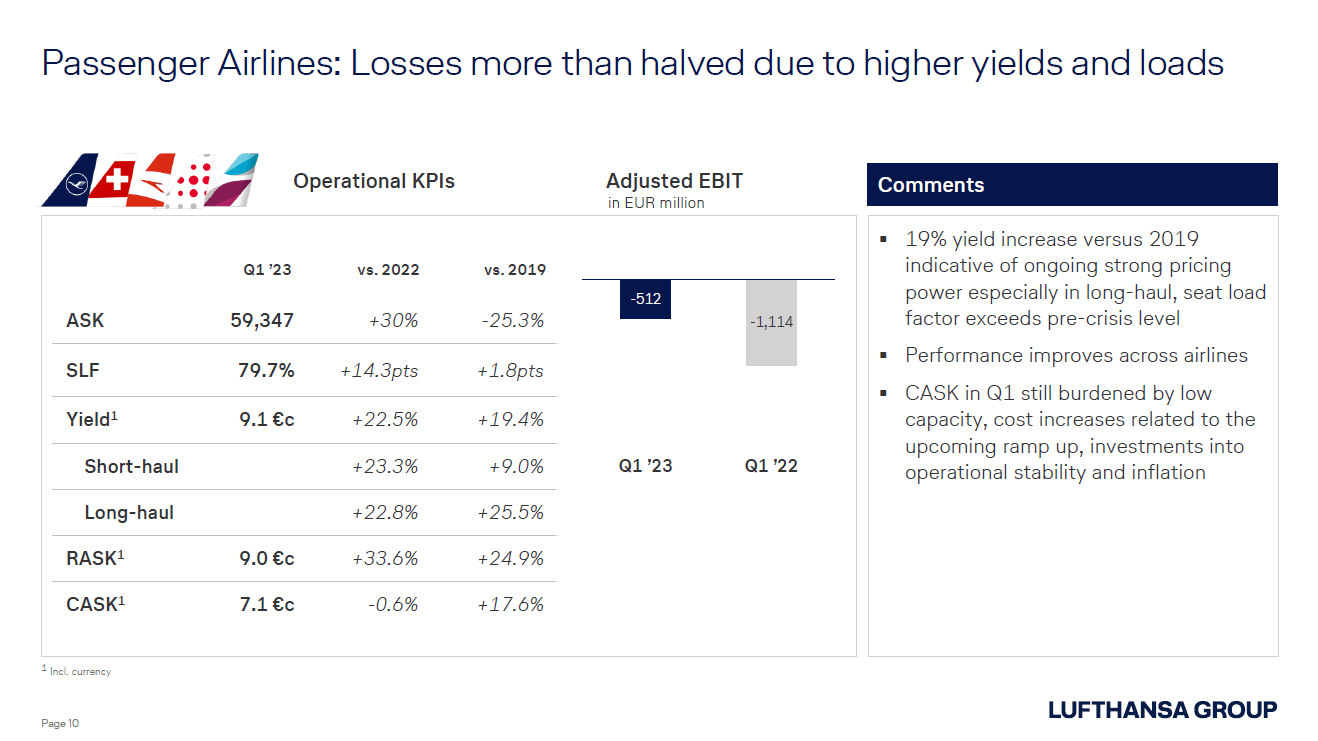

As said, Lufthansa carried 70% more passengers and that translated into 72.5% higher revenues supported by a better unit revenue. The adjusted EBITDA saw a 54% or €602 million improvement as some of the topline growth was absorbed by higher operating expenses. Fuel costs were up 77% or almost €700 million while staff costs were up €244 million. That already accounts for nearly €1 billion in additional costs, offsetting some of the €2.2 billion improvement in revenues. The rest of the cost growth can be attributed to two other elements. The first is the inflationary cost pressure and the second item is what I would call the seasonality on the costs as the airline group ramps for the summer season, and they are introducing some preparation costs for that in Q1.

On seasonality, Lufthansa executives echoed a change in flying habits, noting that demand or growth of the said demand is more concentrated around the high-demand travel period, and in the first quarter, around 60% of the business came from corporate travel.

Lufthansa: Superior Debt Management

{kind=link}

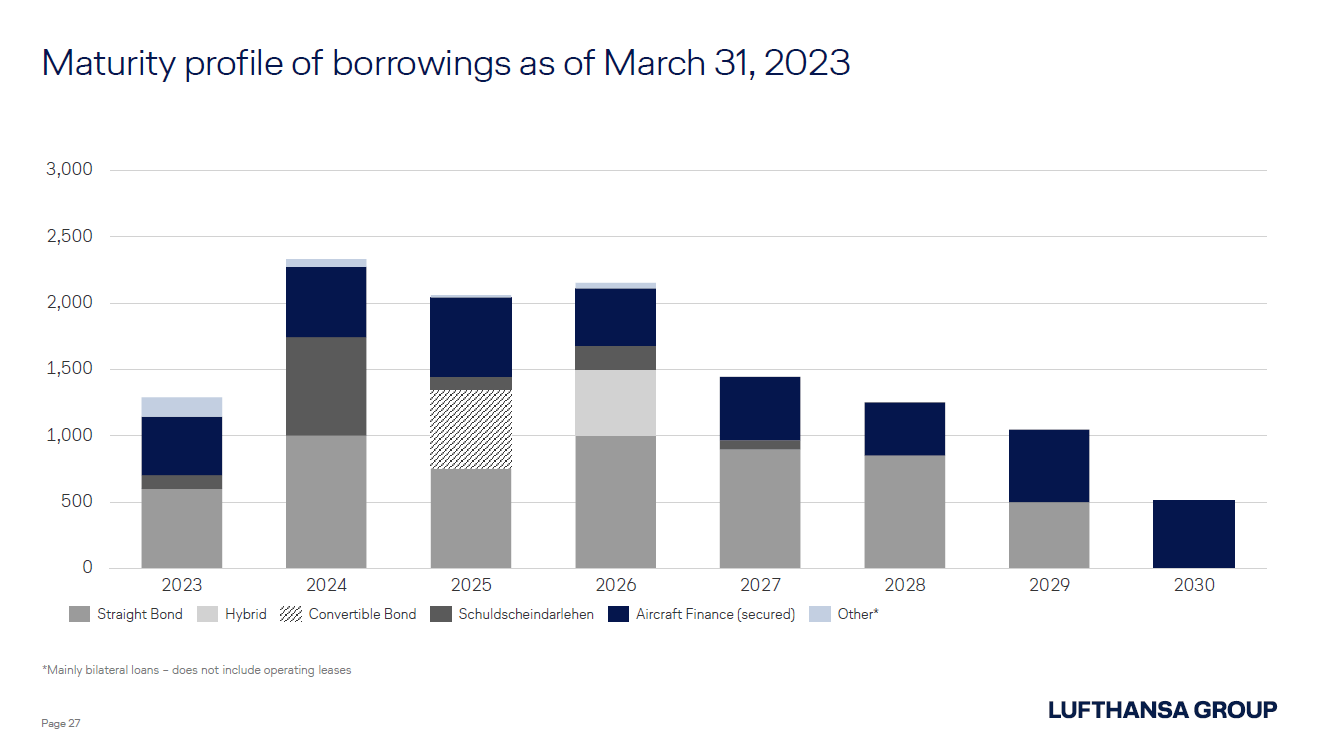

Looking at the profile of the maturities, including aircraft financing, we do see that Lufthansa doesn't have a clear runway, but with the current liquidity, Lufthansa can cover its debt maturities up to and including 2027.

In one of my previous reports on Lufthansa, I noted that the years 2025-2026 would be more challenging as its debt maturities were concentrated in those years. What we see now is that instead of significantly reducing the near-term maturities early, the company has elected to reduce the debt in 2025-2026 by roughly €1 billion. As the 2023 debt matures, Lufthansa will reduce the debt there obviously, but I also see possibilities for the airline to reduce the 2024-2026 debt to €1.5 billion annually which can be seen as a de-risk and a smoother maturity profile for the business.

Lufthansa Maintains Guidance For Further Recovery

{kind=link}

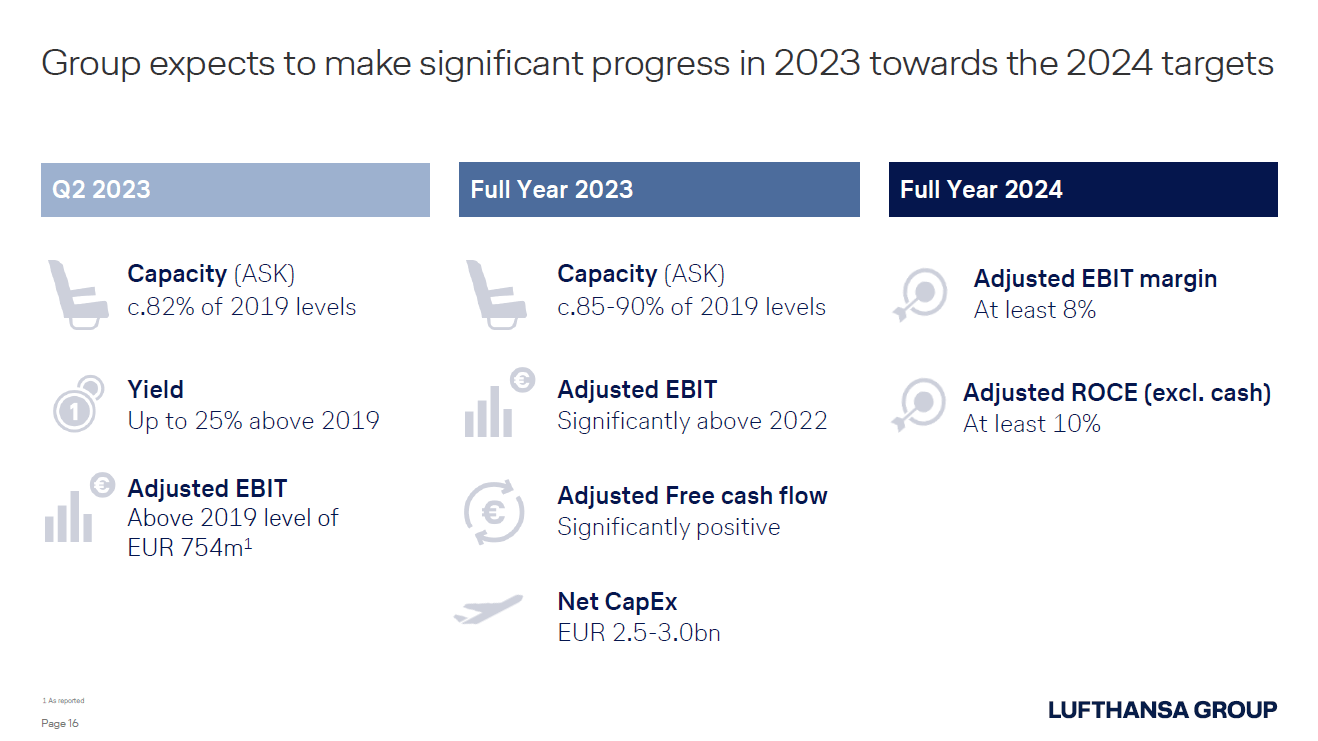

For 2023, Lufthansa continues to expect capacity to recover to up to 90% with adjusted EBIT significantly above 2022, which is not odd given that, with a persistently strong demand environment for air travel, we should see the airline replicating the H2 2022 strength over the entire year in 2023. Maybe it's somewhat unfortunate to see that adjusted free cash flow was guided down year-over-year to the €2 billion range during the fourth quarter earnings call, but that is still €2 billion going towards the liquidity and further improving the leverage and net debt position.

Growth drivers for Lufthansa will be the re-opening of parts of the Asia-Pacific region as well as improvement in corporate travel volumes while unit costs excluding fuel will be stable year-over-year, offsetting inflationary pressures. Lufthansa has not guided on revenues, but even if we assume that revenues remain constant which, combined with capacity expansion, would simulate a weakening in unit revenues and apply a margin of 6.5%, adjusted EBIT could still come in at €2.13 billion, up from €1.5 billion in 2022. That quick calculation is actually not too far off from the consensus, and actually even that consensus might be conservative.

Is Lufthansa Stock A Buy?

In 2019, Lufthansa achieved a €2 billion EBIT, or €2.98 per share. Over the course of that year, share prices declined with a high of €16.40 per share, meaning that the stock traded at roughly 5.5x adjusted EBIT as measured from the highest price point. Lufthansa has not targeted an adjusted EBIT, but I am increasing my EBIT adjusted estimate to €2.425 billion, applying the EBIT multiple.

Applying that to the €2.13 billion projection for 2023 gives us a €10.36 price target. So, is Lufthansa a Buy? Yes. We've seen more positive signs, and the strikes that we saw at German airports are largely behind us, meaning that Lufthansa should be able to continue benefiting from a strong demand environment that is constrained from the supply side with a 12% upside.

In case we see a strong pricing environment persist and results exceed expectations, the stock price target would increase to €12.25, providing a 32.5% upside. So, there's an upside if the year goes as Lufthansa expects it to go.

Conclusion: Lufthansa Management Is Executing Well, I Am Upgrading To Buy

Lufthansa's stock price softened somewhat after posting its first quarter results, as revenues fell short of expectations by roughly half a billion euros. However, while missing on topline, the company did better on adjusted EBIT than analysts had expected. So, perhaps that topline miss should be taken with a grain of salt, especially since a significant portion of the miss can be attributed to the cargo division, indicating that there are no concerns on the topline growth for the passenger airlines. I have flown on two of the five passenger airlines of the Lufthansa Group post-pandemic, and while the travel experience is underwhelming, with the softening of the stock prices, the continued strength in air travel demand and Lufthansa, considering the analyst consensus for the year is soft, I do think this could be a moment to consider buying the stock.

For further details see:

Upgrading Lufthansa Stock To Buy