UPH - UpHealth: Deteriorated Balance Sheet Likely Terminal For Sick Business

2023-03-20 08:28:58 ET

Summary

- UpHealth Inc. is a tech focused telehealth specialist with a mission to reshape healthcare.

- The digital health specialist was the product of a SPAC merger in 2021 during a period of easy money and buoyant economic conditions.

- Increases in risk premiums and cost of capital may put an end to a business with fundamental structural issues with its finances.

Company Introduction

Remember SPAC-mania? That ugly period at the start of the decade when cheap money enabled a sponsor led cash grab targeting retail traders more akin to taking advice from YouTube gurus rather than trawling through copious amounts of financial data?

It is likely that inflationary pressures, high interest rates, inflated equity risk premiums and a growing disinterest in capital markets will lead to a spac-tacular (pun intended) implosion of the business model.

It has been a common theme among celebrated SPAC sponsors – whether it be Chamath Palihapitiya, Betsy Cohen, Howard Lutnick, or Michael Klein – they all share one common trait, below average Spac-related returns.

So, it is perhaps no surprise that our telehealth upstart, UpHealth ( UPH ) has been on a crusade of vigorous capital destruction. The venture was the product of SPAC era cheap money and a timely marriage of UpHealth holdings and Cloudbreak Health via blank-check firm GigCapital2 in 2021. Since then, shareholders have reeled in losses with perhaps only sponsors seeing any form of returns since the company’s flotation on public markets.

The Florida based telehealth specialist provides digital health technologies and tech-focused services to provide integrated care solutions. The firm’s goal is to reshape healthcare by developing and managing a range of technological platforms geared towards remote consultation, data science, and developing predictive models to improve health care.

In summary, the company provides a unique and differentiated set of advanced technology products and services focused on improving population health and does this with offerings across integrated care management, virtual care infrastructure and services.

{kind=link}

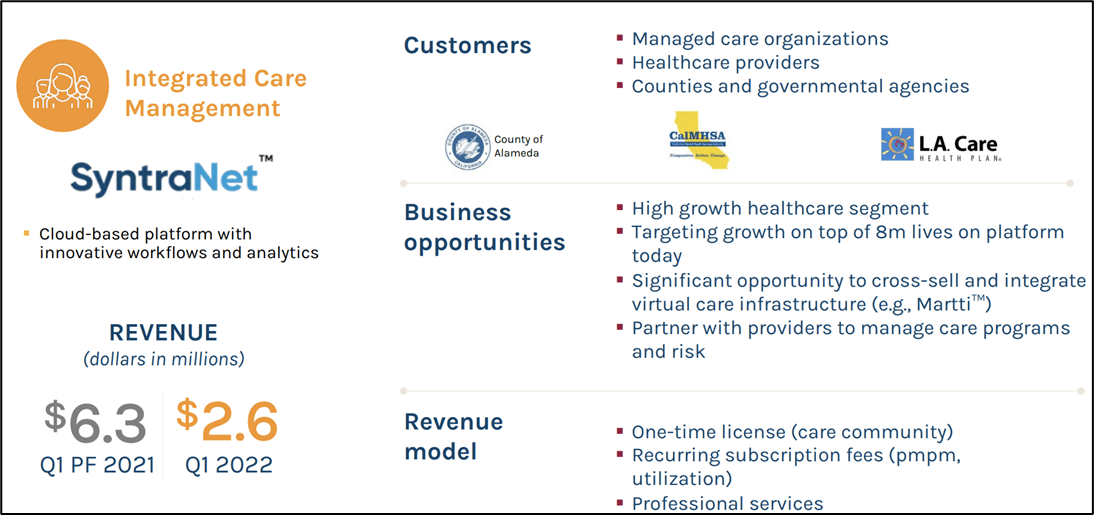

Integrated care management, one of UpHealth’s business lines has seen a considerable drop in revenue.

It’s hard to get excited about the business or its prospects, given a track record of red ink, continued losses and a changing monetary environment. Since its founding, the company has shed 98% of its value, effectively turning the virtual health pioneer into a micro-cap stock.

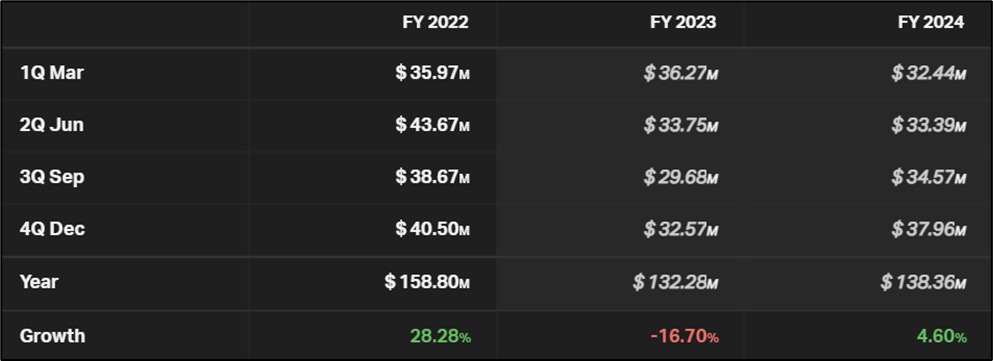

With FY2022 sales of $158M, the firm has experienced incredible growth over its short life. Yet that growth has come at the expense of profits in a model that has been facilitated by recourse to easy credit markets. Times have since changed.

{kind=link}

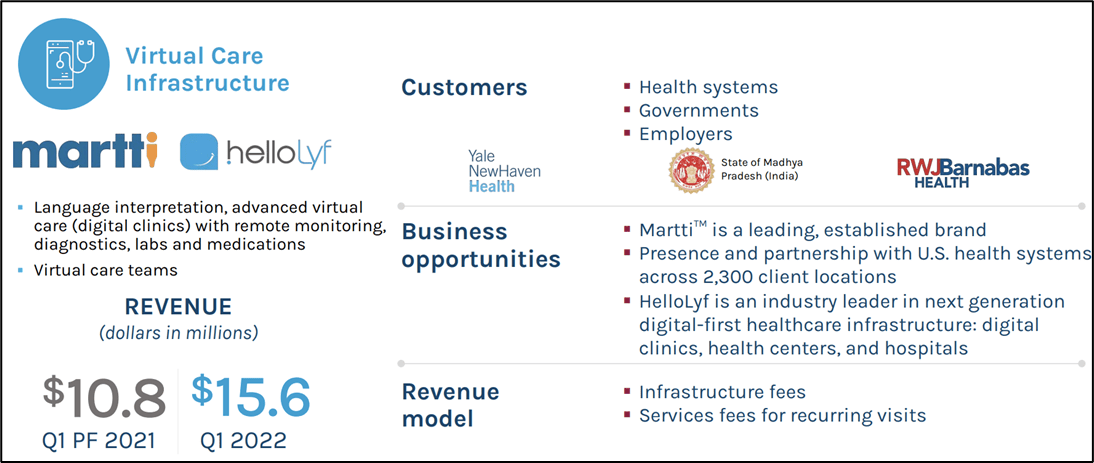

Virtual care infrastructure has provided strong growth for the company.

At ZMK Capital, we are bearish on the firm’s prospects. Buying growth, gaping holes in cash flow from operations, coupled with a reliance on cheap credit markets and easy money have never made for a sustainable business strategy.

At a time when winds are changing and the macro-economic environment is forcing a re-think on cost of capital and equity risk premiums, we believe the company will struggle to survive.

{kind=link}

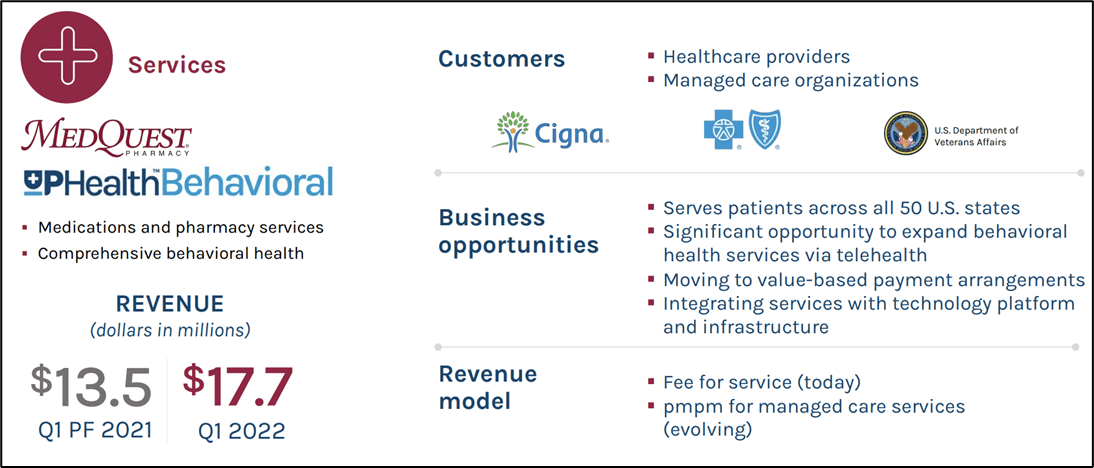

Services are the company’s core business and continue to grow albeit at an increasingly slower rate.

While this may be the case, we would also like to bring to readers’ attention that UpHealth Inc. is now in penny stock trading territory and susceptible to sizable swings in price. Low float and a lack of liquidity means this is not an appropriate short sell. While our rating is short, we do not recommend that readers actively try to hold equity short given the above-mentioned dynamics.

Financials

UpHealth's financials are simply unsustainable. Continued but slowing growth, sky-high operating expenses coupled with lofty sales, general & admin costs ($71M FY 2022 on $158M FY 2022 sales!!). $26M in annual net interest expense emphasizes the strain under which the firm’s finances continue to be given shifts in monetary environment.

{kind=link}

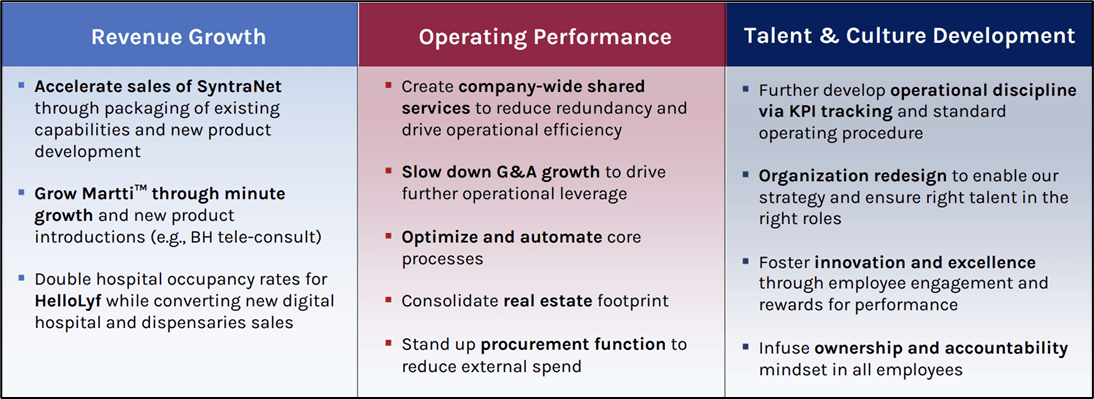

A complete strategic re-think of the business is required to stem the losses.

Recognizant perhaps of this, the company has recently hired a new CEO, Samuel J. Meckey and started a strategic revamp of the business model. This includes accelerating sales in SyntraNet, Marti and focusing on occupancy rates for HelloLyf.

Improvements in operating performance can only be achieved through a wholesale focus on cost reduction by creating a shared services function, reducing office space, professionalizing procurement and radically trimming sales, general and administrative costs. Improvements in operational discipline are equally targeted with different initiatives around talent & culture development.

It's likely that Samuel J. Meckey, a Harvard MBA graduate, identifies more corporate skeletons in the near term leading to more bad news before a slow but gradual redressal. Beyond the concerns regarding slowing forecasted growth, deep troubling issues lie within the health tech venture’s balance sheet.

Total debt to EBITDA is presently 128.3x and the quality of current assets pails in the face of current liabilities. UpHealth Inc. has a current ratio of 0.6x and quick ratio of 0.5x underpinning woes the company presently has to finance current liabilities with current assets. This implies continued recourse to credit markets to keep the business afloat, at the cost of lofty interest expenses on debt.

{kind=link}

Sales forecasts show a potential tapering of growth during 2023.

Little has been achieved to accelerate receivables and only substantial changes in duration to pay vendors (increased from 35 days in FY 2021 to 67 days in FY 2022) has helped the company optimize working capital. Cash and cash equivalents has meaningfully dropped, from $58M FY 2021 to $15.6M in FY2022.

The elephant in the room remains the goodwill loaded on the balance sheet - $159M during FY2022. Any sizable impairment would be enough to entirely wipe out the company given equity of solely $105M. That is perplexing for a firm bleeding cash, reliant on credit markets to operate, while facing excessive operating costs. Goodwill merits close monitoring because any changes in valuation would likely lead to existential capital structure issues for UpHealth Inc.

{kind=link}

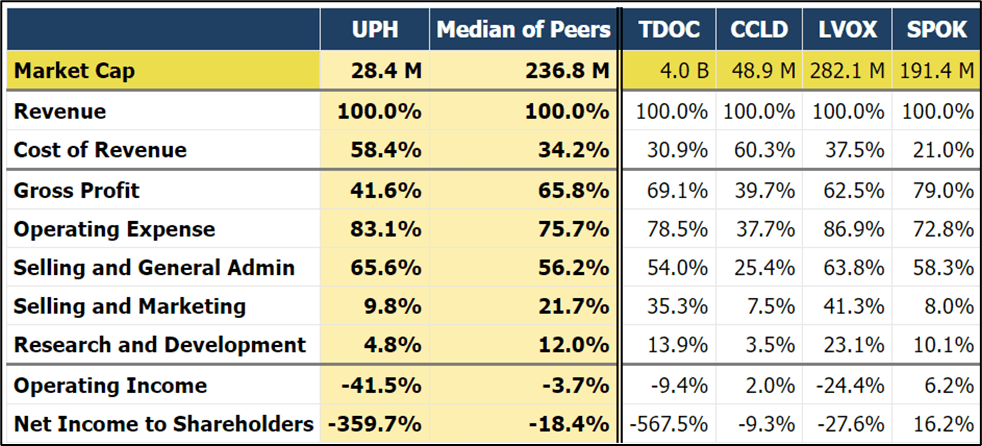

A comparative analysis of UpHealth's income statement against a basket of peers shows how troubled the sector is.

Risk

The risks linked to a targeted investment in UpHealth Inc are sizable. The firm’s current financial condition is unsustainable. With approximately $3M in monthly cash burn on only $15M in cash on hand, the clock is ticking before a capital raise of some sort is required to throw the firm a life-line.

Selling, general & administrative costs have gotten out of control and the growth focused business model appears underpinned by them. Analysts are already forecasting a tapering of sales this year, implying that gapping losses can no longer be covered up by huge improvements in the top line.

The level of goodwill on the balance sheet is an existential threat to the business should any impairment result in a radical downside valuation. Goodwill has already been impaired on two occasions ($-297M in FY 2021 and -$114M in FY 20222) suggesting that excess prices paid for the acquisition of companies/ business units were high.

The company has successfully managed to refinance some debt (+67.5M) but the risks that credit markets continue to remain volatile is high, particularly after the present jitters in the banking sector.

Key Takeaways

UpHealth is a structurally damaged business with no easy out. Its growth has been reliant on continued burning of cash, particularly in SG&A and it has visibly managed to navigate an easy money environment.

Yet that environment has changed – equity risk premiums are continuing to accelerate to the upside while credit markets dry up. Regardless of the new talent onboard and changes in strategy, this may be too late for a firm burning $3M with only roughly $15M in cash on hand.

For further details see:

UpHealth: Deteriorated Balance Sheet Likely Terminal For Sick Business