UPMMY - UPM-Kymmene: One Of The Best Forest-Product Companies A Buy (Rating Upgrade)

2023-05-07 23:47:06 ET

Summary

- It's a bold move or statement to call a company one of the "best", especially when that company does not boast class-leading or high-percentile margins.

- UPM does have excellent profitability, but its appeal is mixed from a myriad of different root causes. We will go through them here.

- UPM is a company I have been reviewing for years, and I have seen significant profit from my position. I'm buying more at this time.

Dear readers/followers,

UPM-Kymmene Oyj ( OTCPK:UPMKF ) (UPMMY) is a company I've been reviewing for years on seeking Alpha. I don't mind tooting my own horn, as it were, especially when I have a good track record of providing my readers with appealing entry and exit points for investments that I make myself.

My latest position at UPM was actually a "HOLD" - back in February. My rationale at the time was fairly clear - as is my rationale for shifting that stance at this time. If you'd followed my "HOLD" rating, you'd have avoided a 12.5% negative RoR in a relatively short time as the stock basically traced part of the commodity and finance downturn.

UPM Kymmene RoR (Seeking Alpha)

UPM Kymmene - An upside has once again materialized for the stock

It's not a market of stocks, but a stock market. It's a good saying, and one I try to take to heart when I invest. There are times to invest in a business and times not to - and it oftentimes doesn't have much to do with the overall state of the market.

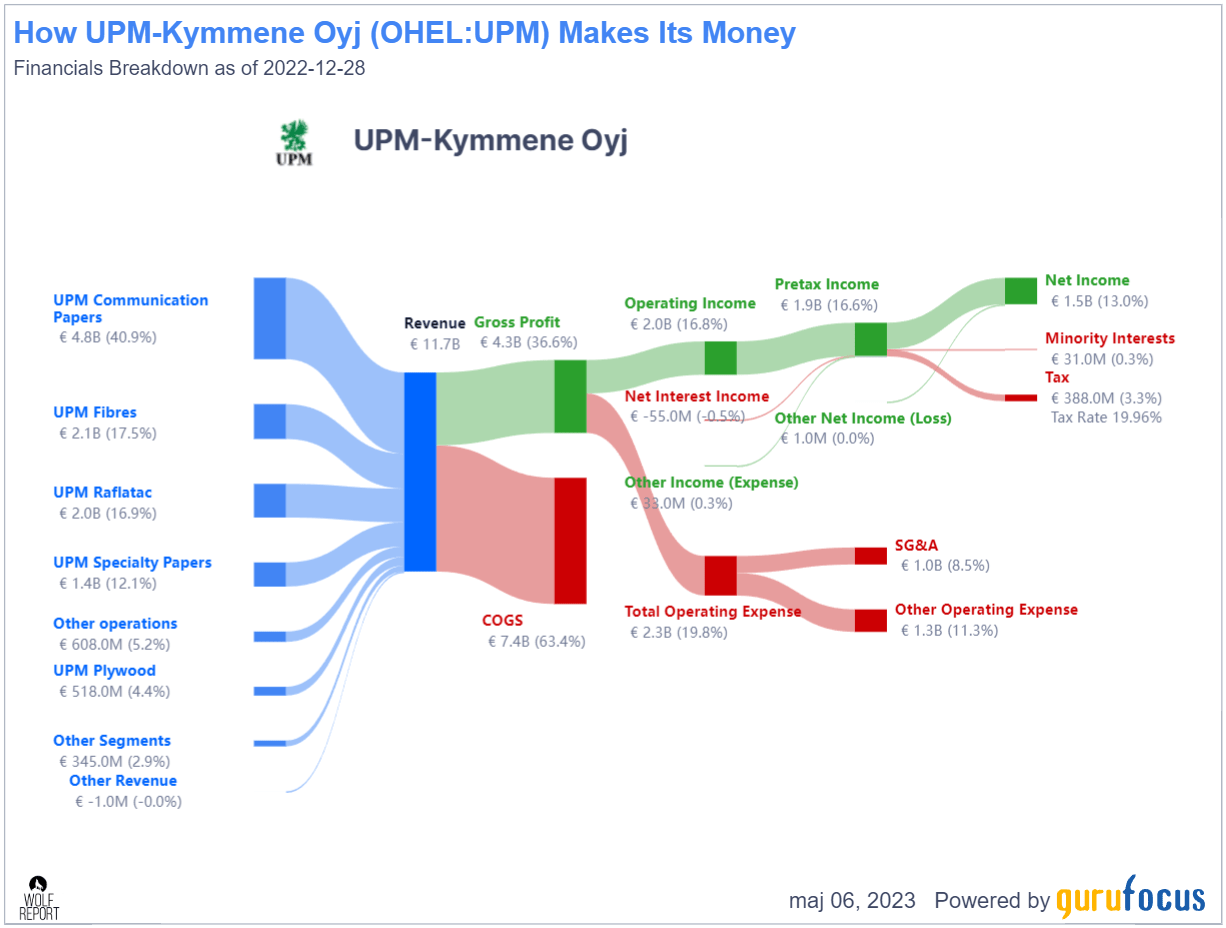

UPM, owing to its mix, has a higher exposure to cyclicality than many other companies. The company is in a mix of Forest Products in terms of industry and is one of the biggest on the planet. Its mix is all-encompassing. It does papers, Fibres, Rataflac, Specialty papers, plywood, and a mix of other operations. These operations, in total, generate a gross margin of nearly 37%, to OM of 16.8%, and a net income of 13%. That is good enough on a gross margin level, but it's superb on an operating and net margin level, where the company is among the 80-90th percentile in a segment that includes giants like Enso ( OTCPK:SEOJF ), Suzano, Mondi, Holmen ( OTCPK:HLMNY ), Klabin and many other companies I periodically have, or current am investing in.

A common thread for the forestry segment is that most leading companies are not based in NA. UPM is in fact the largest with a market cap of around $18B. Its history, going back a century if you look at some of the assets and an appealing merger from -96, is very positive.

Its sales mix is one of the best around - of any company in this segment.

{kind=link}

UPM Rev/net (GuruFocus)

Just looking at that graph, you can see that the company's margin and processing from revenue to net income at appealing margins. This gets even better when you look at the company's fundamentals from a sector comparison. The company's debt/equity is less than 30%, better than 0.62x equity/asset ratio, and an interest coverage of 32.8x. The company has one of the best ROIC scores net of WACC in the entire sector, owing to its investments and appealing start-ups of operations not only in legacy paper products but things like biofuels.

All of these operations have given it a profitability record of 10 years that outstrips 99.75% of the other companies in the segment, and there are nearly 300 global companies it's being compared to.

So, you know that UPM is effective at what it does, and you know that it's more profitable than the average business in the segment. Both of these are crucial to me when I look at putting my hard-earned money to work.

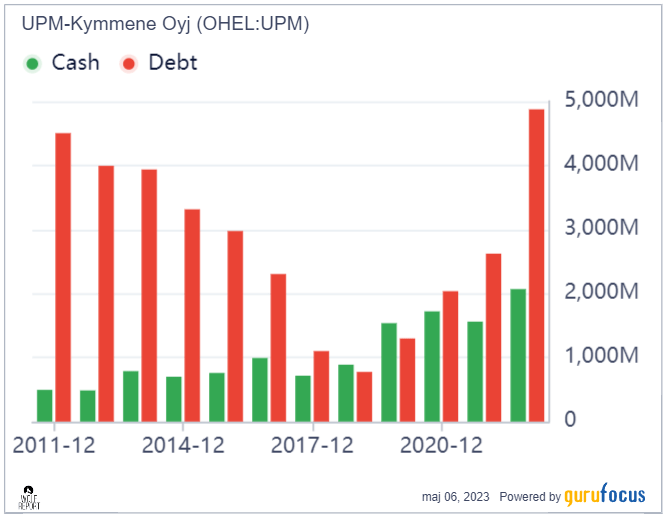

UPM has been very effective at growing shareholder equity and assets at an attractive rate without taking on too much debt that the company has been unable to pay back. Yes, debt has been taken on - but it's been paid back in cycles, and the current level of debt does not give me worry for this cycle either.

{kind=link}

UPM debt/cash (GuruFocus)

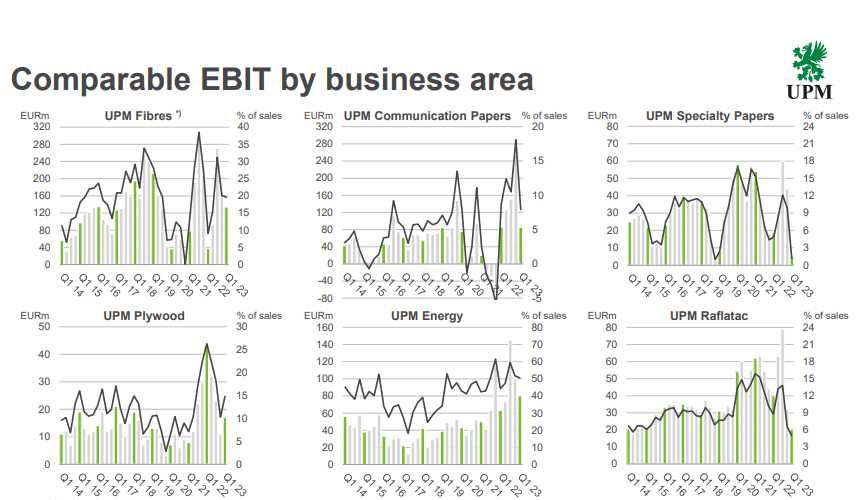

Recent results confirm the company's positive upside. 1Q, which tends to be a decent quarter in terms of cyclicality and seasonality, saw sales increase double digits by 11%, and EBIT on a comparative basis up nearly 30%. OCF was up over €700M YoY. The new Paso de los Toros started production, and while the company started to see some margin impacts across some areas due to de-stocking across some value chains, we'll see what happens to things and trends as we go forward.

UPM IR (UPM IR)

Comparable EBIT was negatively impacted by pricing, variable costs, and volume as well as some timing impacts. With the number of segments and business lines UPM has, it's almost a foregone conclusion that some things will be down, while other things will be up.

{kind=link}

UPM IR (UPM IR)

The aforementioned debt is up, but the company has cash and available funds of nearly €7B, which is more than 3x the company's current debt, with a net debt/EBITDA of less than 0.85x. This is still a very conservative level, and with no financial covenants holding the company back, it's easy to see why expectations are positive.

The company's 2022 earnings were at record levels. As with most companies in this, or adjacent areas, I do not expect a larger or repeat performance in this fiscal. However, also as with most of the companies I review in the segment, I do expect that the baseline level of operating performance and earnings will be higher going forward than during pre-COVID-19 periods.

There are multiple factors underbuilding this assumption from my side. First off, the ramp-up of Paso de los Toros, a pulp mill, as well as the OL3 nuclear power plant unit related to it. While production is expected to be up, and asset utilization will be good, there will nonetheless be significant de-stocking across several product value chains - but this will in turn be balanced by the normalization of parts of Asia, specifically China.

{kind=link}

UPM IR (UPM IR)

Input costs will remain on the higher side, and low demand will continue to press prices - but inputs are also, not just in UPM, but market-wide past their peak. We're seeing that we're past "peak price/cost inflation", and this will drive things down.

While uncertainties continue to mount with the geopolitical macro, I have no doubt that UPM will continue to increase efficiency and work positively in its operations, delivering value, earnings, and dividends to shareholders.

The company's long-term ambition and business mix transformation is going on track - and things will be moving forward, regardless of the specific flows and trends in 2023. This includes the slow wind-down of communication papers.

{kind=link}

UPM IR (UPM IR)

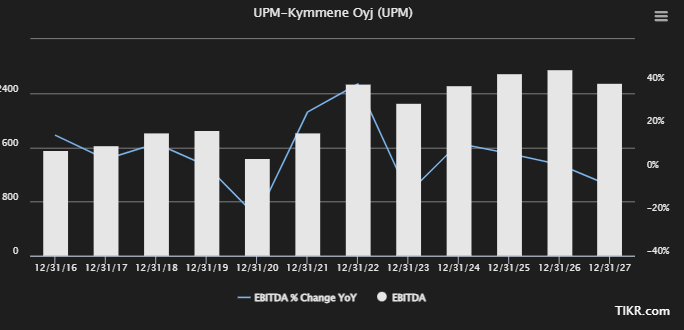

Forecasting UPM results, I expect EBITDA declines in 2023, followed by double-digit bounce backs in 2024, then normalization as value chains start to normalize. The 2022A EBITDA of over €2.4B was, from a historical perspective, significantly above the norm - but I expect normalization and expansion to put UPM's EBITDA somewhere along the €2.2-€.2.4B mark for the next few years. You won't see it going towards €3B, but there are plenty of reasons to believe it won't drop far, or below €2B at all. I am hardly alone in these forecasts either - in fact, many of my colleagues are more positive than I am.

{kind=link}

UPM EBITDA (S&P Global/TIKR.com)

I remain conservative as always, and as such, this is my conservative forward estimate and valuation for UPM Kymmene.

UPM Kymmene - Updated valuation and thesis for May/2H23.

In my previous article on UPM, I characterized the company as somewhat stretched in terms of pricing. After a double-digit valuation decline, this picture has obviously shifted a bit. My previous PT was €36/share, and I called it attractive at below or close to €30/share. That is obviously where we currently are, with a native share price of €30.16 for the company.

Current analyst averages haven't changed materially from a few months back. We were far higher back then, but the target from 15 analysts remains at around €28-€45, with an average of €36/share, close to my own conservative PT. The difference now to then is that there is a near-20% upside in the current share price compared to a share price of €35/share.

At €35/share, this company's upside, even considering positive results, goes almost below double digits. At below €30/share though, this is a different story. We now have a 14.25% annual upside to a valuation of 13.7x, which also happens to be the company's historical P/E average over 5 years. That's a 42% RoR in 3 years, based on an attractive yield of 5.06%, which is attractive both inside the context of this segment and outside of it, based on risk-free rates of return.

While the company's valuation may go up and down, the dividend and the company's operations are, as I would consider them, "risk-free" compared to many other investments here. I don't mind the ups and downs, as some do - and for that reason, I'm increasing my rating for UPM Kymmene at this particular time. I now consider the company to be an attractive "BUY" with a double-digit upside annually, and around 40%+ potential RoR for the next 3 years.

That makes it not the best investment out there - but certainly a decent one.

Thesis

- UPM is one of the world's best and most appealing, Finnish-based forestry and pulp/chemical companies with a good energy arm. It also has a great yield. At the right price, this company goes from being lukewarm to a full-fledged must-"BUY" - that's my view, at least. This time has now come.

- At a share price of below or around €30/share, this company will eventually, I believe, reward shareholders with good returns. While there is potential for a downturn further in 2023, I believe the eventual upside will materialize in this investment, causing it to beat the market.

- For that reason, I'm raising my rating on the company to a solid "BUY" here, with a price target of at or around €35/share - though at €35/share, the upside is barely double digits.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company, because of this, fulfills the key criteria I have, though I won't call it cheap here. It does, however, have an upside, and for that reason, it's worth buying.

For further details see:

UPM-Kymmene: One Of The Best Forest-Product Companies, A Buy (Rating Upgrade)