MDY - Upslope Capital's Q1 2023 Investor Letter

2023-04-26 11:40:00 ET

Summary

- Upslope Capital Management is a Colorado registered investment adviser. Upslope's core investment approach is a concentrated, long/short equity strategy, focused on mid-cap businesses.

- During Q1, markets saw notable up-and-down volatility. These months were not particularly dramatic for Upslope.

- In addition to the usual updates, I am thrilled to announce the launch of Upslope Partners Fund, LP, a commingled hedge fund that will deploy the same differentiated strategy Upslope has used via SMAs (which will be converted into the fund) since inception.

Upslope's objective is to deliver attractive, equity-like returns with significantly reduced market risk and low correlation versus traditional equity strategies. During Q1, markets saw notable up-and-down volatility. These months were not particularly dramatic for Upslope: we lost a little in January as markets went vertical (up) and made a little in February and March, as markets dropped.

| Upslope Exposure & Returns [1] |

| Benchmark Returns |

| Average Net Long |

| Net Return |

| S&P Midcap 400 ETF (MDY) |

| HFRX Equity Hedge Index |

| Q1 2023 |

| 66% |

| -1.2% |

| +3.8% |

| +0.8% |

| Last 12 Months |

| 67% |

| +5.5% |

| -5.2% |

| -2.1% |

| Since Inception* |

| 50% |

| +9.3% |

| +8.9% |

| +3.9% |

Note: clients should always check individual statements for returns, which may vary due to timing and other factors. *Since Inception returns are annualized (from August 2016).

In addition to the usual updates, I am thrilled to announce the launch of Upslope Partners Fund, LP , a commingled hedge fund that will deploy the same differentiated strategy Upslope has used via SMAs (which will be converted into the fund) since inception. The fund will be open to Accredited Investors, and I expect an initial close on July 1. This change was a long-time coming, and I believe it will greatly enhance Upslope's operating and tax efficiency as well as long-term growth trajectory. If you are an Accredited Investor and interested in learning more or joining the partnership, please contact me.

Market Conditions - Known (Un)knowns

"Cautiously pessimistic" 2 is an apt way to describe my current views towards markets. I see a couple of big bad 'Known Knowns' - deeply inverted yield curve and bank crisis/tightening credit. We know these are issues, and we know what they generally lead to: recession. On the positive side, we have an economy and jobs market that have proven amazingly resilient. No doubt a big deal, but are they likely to get better or worse from here? Pull up a long-term chart of the unemployment rate and you know the answer.

The Known Unknowns (issues we're aware of, but whose effects are unclear) list is daunting: still unresolved inflation, wildly uncertain geopolitical tensions, and possible central bank reactions (helpful, adversarial?) to all of the above. On inflation, many continue to mistakenly put our troubles in the Known Knowns category - "we know it's almost over and this will be good for stocks." We do not know this. We know it will end, but importantly we don't know when or how . Inflation antidotes have some notorious and lagging side effects. The geopolitical issues are serious and frankly I feel like a conspiracy theorist for mentioning them. The path and outcomes are impossible to predict. But we don't have to keep our heads in the sand. While Upslope is generally positioned to benefit from volatility, I hope such crises are not the spark. Our positioning reflects my views on market conditions and opportunities - not the other way around.

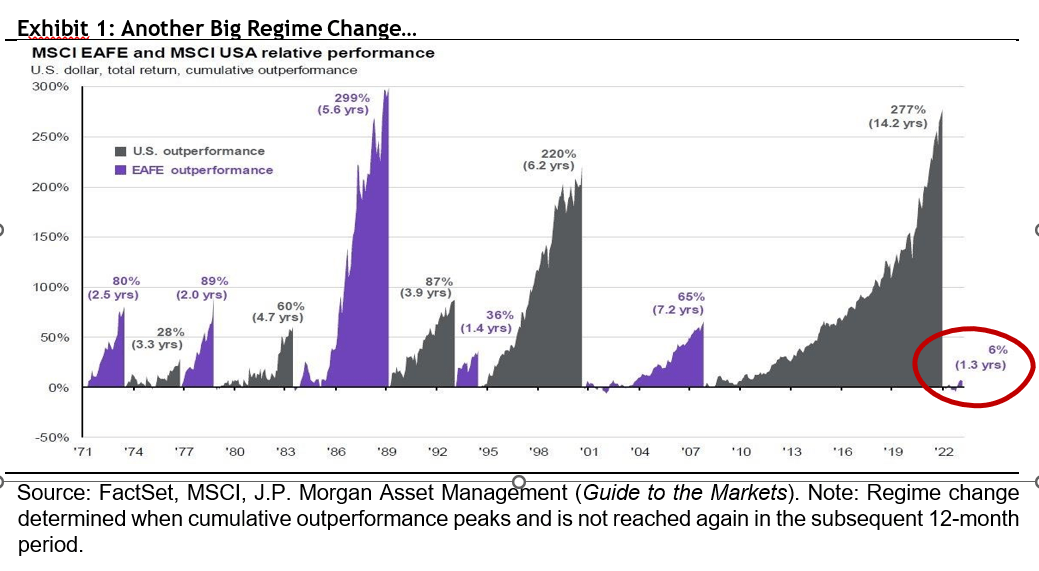

I'll close this section with a thought-provoking analysis from J.P. Morgan's quarterly Guide to the Markets , as well as a related and curiously timed contrarian "cover indicator" from The Economist . Last year's growth-to-value "regime change" was much talked about. However, another big regime change is also afoot. For the first time since the Financial Crisis, US stocks have consistently underperformed (squint at the bottom right of the chart below) global peers. This could be a mere blip, as some have been in the past. For now, it seems early and that the change has the potential to last for some time. Investors with the ability to invest overseas, such as Upslope, should have an advantage in navigating evolving investment regimes.

{kind=link}

{kind=link}

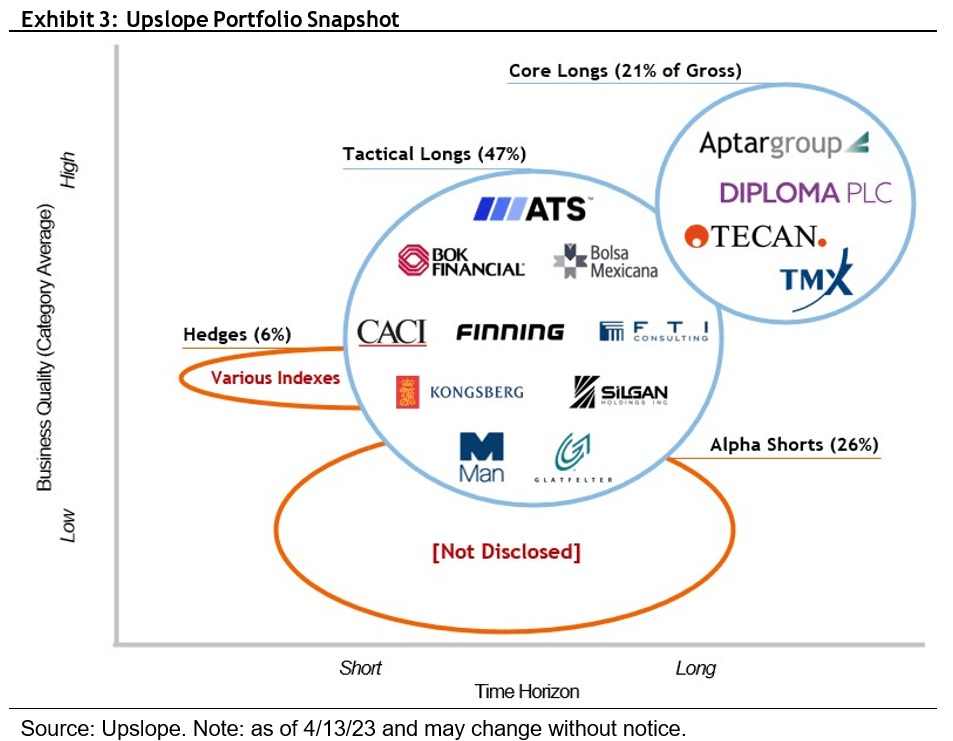

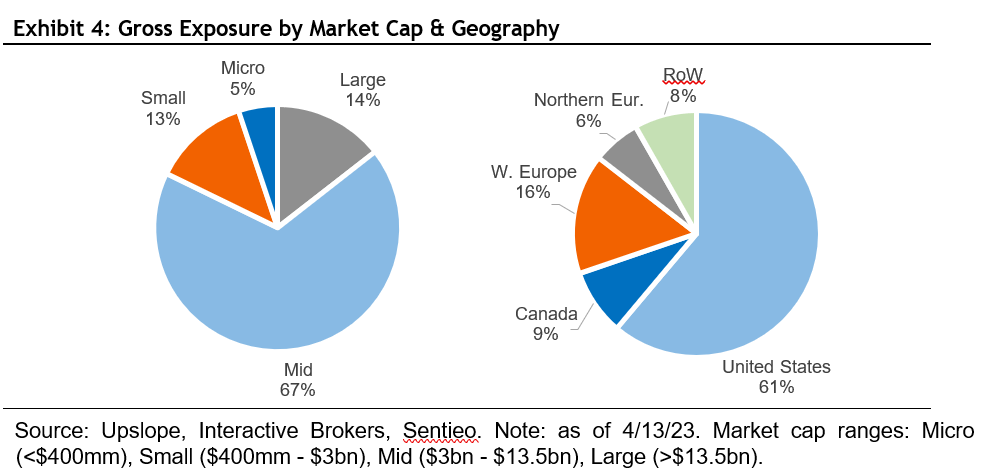

Portfolio Positioning

At quarter-end, gross and beta-adjusted net exposures were 146% and 39%, respectively. Positioning reflects a heightened number of perceived opportunities, both long and short.

{kind=link}

{kind=link}

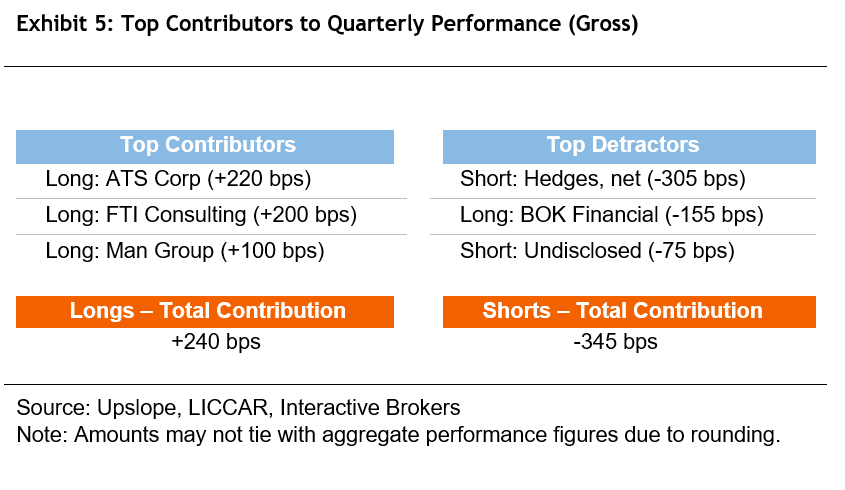

Portfolio Updates

The largest contributors to and detractors from quarterly performance are noted below. Gross contribution to overall portfolio return is noted in parentheses.

{kind=link}

Chemring (CMGMF) - Exited Long

Chemring is a niche defense contractor focused on flares, energetics, and cyber warfare, among other areas. The company has navigated the uncertain environment fine but has not benefited as materially as I expected. Additionally, the CFO, who played a key role in driving the company's recent turnaround, announced plans to retire. I'm not overly concerned by the change, but the loss of a key executive is another negative. We may be CHG shareholders again in the future. But, for now there appear to be better opportunities for our capital.

Banks - Long & Short Update

Given recent events and Upslope's long BOK Financial position noted last quarter, I wanted to briefly discuss our involvement with bank stocks. While the outlook for regional banks appears cloudy at best, BOKF appears well-positioned to weather the crisis due to a conservative culture, niche geo/sector focus and strong balance sheet. Understandably, shares were not immune; however, BOKF outperformed the sector and losses were blunted a bit by several bank shorts. On the short side, exposure has been diverse, and themes include hard-to-reverse funding/confidence spirals, questionable credit, and extraordinarily crowded "safe-havens" (the latter has not worked to date). I am not sure how the regional bank "crisis" will resolve; however, our long BOKF position is modest, and overall Upslope is net short bank stocks today.

Finning ( FINGF ) - New Long

Finning is the world's largest dealer and distributor of Caterpillar equipment. The company operates in three regions: Canada, South America (Chile, Argentina, Bolivia), and UK & Ireland. I view FTT as a reasonably high-quality business (classic dealer model that benefits from steady service income) serving highly cyclical end markets driven by commodities, mining, energy and infrastructure. Shares appear very cheap today. As with all cyclicals though, cheapness is often a reflection of peak cycle worries. I share these concerns, which is why FTT is a modestly sized "starter" position for Upslope. Why not wait until the coast is clear before initiating the position at all? Because FTT is highly complementary to Upslope's defensive portfolio and cycle timing is notoriously difficult. I plan to discuss FTT in more detail if/when it graduates to a full size.

Closing Thoughts

As investors grapple with the prospect of a recession ahead, Upslope's unique and defensive portfolio appears exceptionally well-positioned to navigate the uncertain environment. Exposure to more traditional "value" stocks and non-U.S. businesses should provide an added tailwind for some time.

With the transition of Upslope's core business model from SMAs to a fund vehicle, I am more thankful than ever for Upslope's clients. I sincerely appreciate your trust, support, and, recently, your patience with the fund transition process. I can't wait for Upslope's next chapter ahead.

If you have any questions at all, would like to add to your account, or know a qualified investor who may be a good fit for Upslope's atypical approach, please call or email anytime.

Sincerely,

George K. Livadas

Appendix A: Long/Short Composite Performance (Net)

Source: Upslope, Interactive Brokers, LICCAR, Sentieo, Morningstar Source: Upslope, Interactive Brokers, LICCAR, Sentieo, Morningstar

{kind=link}

{kind=link}

Note: Returns shown for composite of all accounts invested according to Upslope's core long/short strategy. Upslope also manages a long-only version of the strategy for a subset of assets under management. Performance for a composite of these (or all) accounts is available upon request. Performance for S&P Midcap 400 represented by total return for related exchange-traded fund (ticker: MDY). Individual account performance may vary (minimum returns, net of fees, for an account invested since inception and YTD 2023 were +72.4% and -1.8%, respectively). Clients should always review statements for actual results. 11% of composite assets were non-fee paying at period-end. Data from inception (August 29, 2016) to June 24, 2017 based on portfolio manager's ("PM") performance managing the strategy under a prior firm (as sole PM). Thereafter, PM managed the strategy/accounts on a no-fee basis through August 11, 2017, after which Upslope became operational. Past performance is no guarantee of future results.

Appendix B: Monthly Average Net Long & Gross Positioning

{kind=link}

Appendix C: Portfolio Company (Long) Descriptions

AptarGroup (ATR) : Specialty packaging business focused on pumps and sprayers, with a highly profitable, defensive, and growing Pharma unit. Misclassified and undervalued due to legacy/traditional packaging businesses (Food + Beverage, Beauty + Home), which contribute 60% of sales but just 15% of EBIT.

ATS Corp. (ATSAF) : Canada-based factory automation solutions provider primarily serving defensive end markets (healthcare, food, etc.) in N. America and Europe. Active acquisition strategy + potentially accelerating reshoring tailwinds should sustain growth ahead.

BOK Financial (BOKF) : Regional bank based in and primarily focused on OK, as well as TX, NM, and CO. Conservative culture + unique energy expertise + modest valuation support BOKF shares on a standalone basis. Also view position as a portfolio hedge in the event of sustained, elevated rates and/or energy prices.

Bolsa Mexicana de Valores (BOMXF) : Dominant financial exchange operator in Mexico. Despite known headwinds in its equities business, the company is diversified, highly cash generative, conservatively managed, and shares appear a cheap call option on global macro reacceleration and/or Mexico resurgence.

CACI International (CACI) : Specialized technology and consulting services provider, primarily to U.S. defense and intelligence agencies. Anticipate company will benefit from geopolitical tailwinds, strong position in cyber defense, and continued consolidation opportunities.

Diploma (DPMAY) : U.K.-based specialty distributor focused on essential consumable products across life sciences, seals (machinery), and controls (aerospace wiring/harnesses). Unique model and conservative M&A strategy have historically enabled attractive free cash flow growth through the cycle.

Finning (FINGF) : World's largest dealer and distributor of Caterpillar (CAT) equipment, operating in Canada, South America, and UK/Ireland. Well-managed cyclical business, with "pick and shovel" type exposure to commodities and infrastructure. Highly complementary to Upslope's otherwise-defensive portfolio.

FTI Consulting (FCN) : Boutique consulting and advisory firm, with leading expertise in restructuring, dispute advisory, and other practices. Should ultimately benefit from elevated deal flow in wake of longer-term pandemic effects (e.g. rising rates and SPAC boom/bust) and restructuring cycle.

Glatfelter (GLT) : Specialty materials company with most of its footprint in W. Europe. Commodity products largely serve defensive end markets (e.g. tea, hygiene). Significant exposure to E. Europe + ill-timed M&A put company in distress. Anticipate easing inflation to "bail out" the company, regardless of other macro considerations.

Kongsberg Gruppen (NSKFF) : 200+ year old defense (missile/defense, remote weapons systems) and maritime (offshore, commercial) business, majority owned by Norwegian government. Dominant positions in niche products with cyclically attractive end markets, strong management team and solid balance sheet.

Man Group (MNGPF) : UK-based alt. manager with $140bn+ of AUM (70% alts, 30% long-only). Differentiated, strategies focused on public, liquid markets have withstood sector headwinds well over years and could see resurgence, given dramatically changed macro environment. Position also provides portfolio with "cheap beta."

Silgan Holdings (SLGN) : Food can, dispensing system, and plastic packaging producer managed with a private equity mindset. Defensive end markets, attractive valuation and disciplined model make for attractive baseline investment with balance sheet optionality (M&A or capital return).

Tecan Group (TCHBF) : Switzerland-based lab automation and consumables business, with leading market position in automated liquid handling. Attractive and defensible base business greatly enhanced by exceptional execution during the pandemic.

TMX Group ( X:CA ) : Largest exchange operator in Canada with exposure to equities, fixed income, and derivatives, as well as European power/energy trading/data. Anticipate steady, defensive growth with outperformance during periods of elevated inflation and/or volatility.

Important Disclosures

General

Upslope Capital Management, LLC ("Upslope") is a Colorado registered investment adviser. Information presented is for discussion and educational purposes only. This presentation is not an offer to sell securities of any investment fund or a solicitation of offers to buy any such securities. Securities of the fund managed by Upslope are offered to selected investors only by means of a complete offering memorandum and related subscription materials which contain significant additional information about the terms of an investment in the fund (such documents, the "Offering Documents"). Any decision to invest must be based solely upon the information set forth in the Offering Documents, regardless of any information investors may have been otherwise furnished, including this presentation. Investments involve risk and, unless otherwise stated, are not guaranteed.

The information in this presentation was prepared by Upslope and is believed by Upslope to be reliable and has been obtained from public sources believed to be reliable. Upslope makes no representation as to the accuracy or completeness of such information. Opinions, estimates and projections in this presentation constitute the current judgment of Upslope and are subject to change without notice. Any projections, forecasts and estimates contained in this presentation are necessarily speculative in nature and are based upon certain assumptions. It can be expected that some or all of such assumptions will not materialize or will vary significantly from actual results. Accordingly, any projections are only estimates and actual results will differ and may vary substantially from the projections or estimates shown. This presentation is not intended as a recommendation to purchase or sell any commodity or security. Upslope has no obligation to update, modify or amend this presentation or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, project on, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

The graphs, charts and other visual aids are provided for informational purposes only. None of these graphs, charts or visual aids can and of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions.

This presentation is strictly confidential and may not be reproduced or redistributed in whole or in part nor may its contents be disclosed to any other person without the express consent of Upslope.

Investment Strategy

The description herein of the approach of Upslope and the targeted characteristics of its strategies and investments is based on current expectations and should not be considered definitive or a guarantee that the approaches, strategies, and investment portfolio will, in fact, possess these characteristics. In addition, the description herein of the fund's risk management strategies is based on current expectations and should not be considered definitive or a guarantee that such strategies will reduce all risk. These descriptions are based on information available as of the date of preparation of this document, and the description may change over time. Past performance of these strategies is not necessarily indicative of future results. There is the possibility of loss and all investment involves risk including the loss of principal.

The investment targets described in this presentation are subject to change. Upslope may at any time adjust, increase, decrease or eliminate any of the targets, depending on, among other things, conditions and trends, general economic conditions and changes in Upslope's investment philosophy, strategy and expectations regarding the focus, techniques, and activities of its strategy.

Portfolio

The investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles or SMAs managed by Upslope and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. Past performance of Upslope's investment vehicles, investments, or investment strategies are not necessarily indicative of future results. Investors should be aware that a loss of investment is possible. No representation is being made that similar profits or losses will be achieved.

Performance Results

Performance results presented are for information purposes only and reflect the impact that material economic and market factors had on the manager's decision-making process. No representation is being made that any investor or portfolio will or is likely to achieve profits or losses similar to those shown.

Performance results are net of all fees, including management and incentive fees, as well as all trading costs charged by the custodian, to the investor. Composite performance calculations have been independently verified by LICCAR, LLC. Performance of individual investors may vary based upon differing management fee and incentive allocation arrangements, the timing related to additional client deposits or withdrawals and the actual deployment and investment of a client portfolio, the length of time various positions are held, the client's objectives and restrictions, and fees and expenses incurred by any specific individual portfolio. Performance estimates are subject to future adjustment and revision. The information provided is historical and is not a guide to future performance. Investors should be aware that a loss of investment is possible.

This presentation cannot and does not guarantee or predict a similar outcome with respect to any future investment. Upslope makes no implications, warranties, promises, suggestions or guarantees whatsoever, in whole or in part, that by participating in any investment of or with Upslope you will experience similar investment results and earn any money whatsoever.

Indices Comparisons

References to market or composite indices, benchmarks, or other measures of relative market performance over a specified period of time are provided for information only. Reference or comparison to an index does not imply that the portfolio will be constructed in the same way as the index or achieve returns, volatility, or other results similar to the index.

Indices are unmanaged, include the reinvestment of dividends and do not reflect transaction costs or any performance fees. Unlike indices, Upslope's investments will be actively managed and may include substantially fewer and different securities than those comprising each index. Upslope's performance results as compared to the performance of HFRX Equity Hedge Index and S&P Midcap 400 (ticker: MDY) are for informational purposes only. HFRX Equity Hedge Index is an index that main positions both long and short in primarily equity and equity derivative securities. S&P Midcap 400 (ticker: MDY) is a stock market index that serves as a gauge for the U.S. mid-cap equities sector.

The investment program of Upslope does not mirror the indices and the volatility may be materially different than the volatility of the indices. Direct comparisons between Upslope's performance and the aforementioned indices are not without complications. The indices may be unmanaged, may be market weighted, and indices do not incur fees and expenses. Due to the differences among the portfolios of Upslope and the aforementioned indices, no such index is directly comparable to Upslope.

Fund Terms

The summary provided herein of the terms and conditions of the fund managed by Upslope does not purport to be complete. The fund's Offering Documents should be read in its entirety prior to an investment in the fund.

Footnotes

1 Unless otherwise noted, returns shown for a composite of all accounts invested according to Upslope's core long/short strategy. Please see important performance-related details and disclosures in Appendix A.

2 With a nod to a Twitter friend who goes by a handle of this name.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Upslope Capital's Q1 2023 Investor Letter