SLGN - Upslope Capital's Q3 2023 Investor Letter

2023-10-18 09:00:00 ET

Summary

- Upslope Capital Management is a Colorado registered investment adviser. Upslope's core investment approach is a concentrated, long/short equity strategy, focused on mid-cap businesses.

- Upslope aims to deliver attractive returns with reduced market risk and low correlation to traditional equity strategies.

- The macro picture remains uncertain, with high rates and geopolitical risks, but the micro environment presents exciting opportunities for stock-picking.

- Upslope's portfolio positioning reflects a high number of perceived opportunities, with both long and short positions.

Dear Fellow Investor,

Upslope’s objective is to deliver attractive, equity-like returns with significantly reduced market risk and low correlation versus traditional equity strategies. The Fund’s portfolio was resilient in Q3, with shorts offsetting nearly all losses from longs, as the prospect of materially higher-for-longer rates finally began to sink into markets. I’m pleased that Upslope protected capital during this stretch but remain focused on returning to positive absolute returns.

| Upslope Exposure & Returns [1] |

| Benchmark Returns |

| Average Net Long |

| Net Return |

| S&P Midcap 400 ETF ( MDY ) |

| HFRX Equity Hedge Index |

| Q3 2023 |

| 57% |

| -0.5% |

| -4.3% |

| +0.2% |

| YTD 2023 |

| 59% |

| -3.0% |

| +4.1% |

| +3.2% |

| Last 12 Months |

| 59% |

| +7.9% |

| +15.2% |

| +4.9% |

| Since Inception |

| 50% |

| +8.3% |

| +8.3% |

| +4.0% |

| Downside Deviation |

| 4.9% |

| 13.5% |

| 5.1% |

| Sortino Ratio 2 |

| 1.28 |

| 0.46 |

| 0.39 |

| Note: LPs/clients should always check individual statements for returns, which may vary due to timing, fee schedules and other factors. Since inception returns, downside standard deviation, and Sortino are all annualized figures (from August 2016). |

MARKET CONDITIONS – WEALTH, WAR & WEIGHT-LOSS 3

Three comments and areas of focus:

- The macro picture remains hazy for many market participants (myself included). Inflation has eased, but rates remain perilously high. Hardly a unique view, but I would be surprised if rates remained elevated (or worse) much longer and something didn’t break (e.g. banks, housing, private equity/credit – the Fund is short a bit of each). My default assumption is that a recession was postponed, but not cancelled. This is a fairly low confidence view and somewhat against the tide .

- The “micro” (stock-picking) environment is about as exciting as any time I can remember . Markets have become narrowly focused on two big themes: GLP-1 (weight-loss) drugs and Artificial Intelligence. The former is more relevant for Upslope’s universe of stocks. While the rate environment clouds the picture, some companies have been bluntly shoved into winner/loser buckets based on perceived exposure to these themes. Upslope is not blindly fighting either trend; but, the crudeness with which markets have responded has left me overwhelmed (in a good way) on the idea generation front. The Fund was fully invested – long and short – at the end of Q3.

- Geopolitical risk is clearly the highest in decades and markets don’t care much . Sarah C. M. Paine of the Naval War College recently noted that dictators “often very accurately tell you what they're going to do.” In markets, it pays to be an optimist over the long-run. For the past decade it has also increasingly paid to be an optimist in the short run . Because of this dynamic, I think markets have gotten used to hand-waiving away even the most overt saber-rattling (“they don’t really mean it”) and risks until the last possible moment. Slow reactions to the pandemic outbreak and invasion of Ukraine are examples. Recent events in Israel (and Ukraine) have provided an increasingly stark reminder that genuine evil still exists today and must be dealt with urgently. We appear to be re-entering a period in which pretending otherwise is no longer an option. It’s difficult to guess what the path ahead looks like, but the relative calm of the past decade+ seems unlikely to repeat in the near-term. While it pales in comparison to the human and personal considerations, implications for investors are serious and will continue to be top of mind.

During the quarter, the Fund (re-)added Ball (leading beverage can business) in addition to several “Starter” longs. Details on the refreshed Ball thesis and a broader update on the Fund’s approach to portfolio construction are provided below.

PORTFOLIO POSITIONING

At quarter-end, gross and beta-adjusted net exposures were 149% and 45%, respectively. Positioning reflects an unusually high number of perceived opportunities – both long and short.

Exhibit 1: Upslope Portfolio Snapshot

{kind=link}

| Note: as of 9/30/23 and may change without notice. Positions disclosed at Upslope’s discretion. |

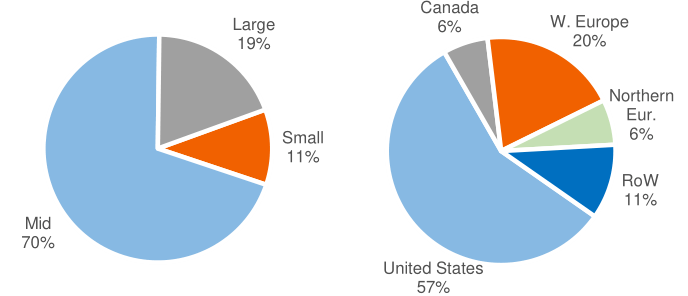

Exhibit 2: Gross Exposure by Market Cap & Geography

{kind=link}

| Source: Upslope, Interactive Brokers, Sentieo/AlphaSense. Note: as of 9/30/23. Market cap ranges: Micro (<$400mm), Small ($400mm - $3bn), Mid ($3bn - $13.5bn), Large (>$13.5bn). |

PORTFOLIO UPDATES

The largest contributors to and detractors from quarterly performance are noted below. Gross contribution to overall portfolio return is noted in parentheses.

Exhibit 3: Top Contributors to Quarterly Performance (Gross)

| Top Contributors |

| Top Detractors |

| Long: Aptar ( ATR , +105 bps) |

| Long: BALL (-140 bps) |

| Long: Japan Exchange ( JPXGY , +80 bps) |

| Long: Tecan ( TCHBF, -100 bps) |

| Short: Building Prod Co (+75 bps) |

| Long: Kongsberg ( NSKFF , -80 bps) |

| Longs – Total Contribution |

| Shorts – Total Contribution |

| -530 bps |

| +500 bps |

| Source: Upslope, Opus Fund Services, Interactive Brokers Note: Amounts may not tie with aggregate performance figures due to rounding. |

Exited Longs

Upslope exited three previously disclosed longs in the quarter: ATS (factory automation – increasingly uneasy with M&A strategy and believe better reshoring opportunities exist), Silgan ( SLGN , food cans/plastic packaging – better use of capital for the Fund, given underlying weakness in stocks), and BOK Financial ( BOKF , regional bank – cheap, but concluded outlook was ‘lose-lose’ given rate environment and macro picture).

Ball Corp ( BALL ) – ‘New’ Long

Ball is the leading global producer of beverage cans. Upslope was long Ball (briefly) in 2022 before I concluded it was too early. No doubt, the company is still facing challenges. Some are temporary and likely to reverse in the near-term (fully leveraged balance sheet, industry over-expansion, overly aggressive carbonated soft drink ((CSD)) pricing) or medium-term (Budweiser exposure). Others are highly uncertain (GLP-1 weight-loss drug impact) but are being priced with certainty, assuming no actions on the part of bevcan or CSD producers (e.g. Coke, Pepsi) to offset any still-hypothetical pain.

Importantly, Ball’s recent announcement that it is selling its Aerospace unit, which has no strategic relevance to the core bevcan business, for after-tax proceeds of ~30% of the company’s market cap, provides a hard catalyst for shares to stabilize in the year ahead. In addition to de-levering the balance sheet – more important than ever, given the rate environment – the divestiture provides Ball with significant firepower to resume buybacks. The transaction should close in 1H 2024 and seems well-aligned with a bottom or rebound across many of the issues Ball has faced of late.

Risks still remain – the issues noted above are all very real, but they are all well-known and mostly temporary, in my view. To be frank, we have already been whipsawed with the latest purchase, as I assumed the market would show more immediate appreciation for the divestiture. But the combination of: low valuation for an economically defensive business with troughing fundamentals and a significant cash windfall seems like an optimal setup for even moderately patient investors.

Other Long Activity – Comment on Portfolio Construction

The portfolio looks a bit different today than in the past due to expanded testing of the “Starter” strategy, as noted in prior letters. Currently, Upslope has several Starter longs, mostly in the 1-5% range. As always, I don’t plan to discuss individual positions until ((if)) they graduate into permanent, fully-sized status. The most notable Starters today include a defensive non-U.S. retailer, a market structure business, and a housing related industrial. Today, Starters fall into three categories:

- Ideas where I’ve completed enough work to establish a toehold, but still have more to do,

- Companies facing obvious short-term challenges where I believe the near-term path in shares is likely lower, but the stock is ‘cheap enough’ and outright attractive over the longer-term, and

- Exposure to ‘counter-shorts’ – higher-beta longs with good risk/reward that trade more in-sync with many of Upslope’s shorts on a daily basis and can be used to manage overall net long exposure more effectively and efficiently.

Historically, I used Starters primarily for #1, a little for #2, and not at all for #3. Today, I am using starters a lot for #2 and #3 and a moderate amount for #1.

While still open-minded, I am increasingly confident that the above approach will add value to Upslope’s core strategy. Notably, it helps the Fund in a few areas I’ve been seeking to improve: better crystallize outperformance following market pullbacks and reduced frustration on a daily basis (because of better long/short pairing). Importantly, it also dovetails nicely with my desire to maintain higher gross exposure (as noted a few quarters ago) without increasing single stock concentration risk. Again, I remain openminded and may conclude this approach is a distraction and I need to re-focus on just 10 longs, period. For now, I’m very optimistic and energized by the prospects of this change.

CLOSING THOUGHTS

“Survive the tough periods and good times will take care of themselves” is how I generally think of risk and portfolio management over the long-term. Surprisingly, 2023 could be characterized as one of those tough periods for Upslope’s strategy, which could crudely be described as “long defensives, short garbage” (there’s a lot more nuance, but that’s not an unfair generalization). YTD (through Sep 30), defensives have underperformed high-beta stocks by nearly 20% and were -6% on an absolute basis. [2] I’m not sure when the tide will turn, but I believe the setup is quite good for Upslope’s approach. Many steadily growing, highly profitable, and economically defensive businesses have de-rated sharply. This, precisely when rates have begun to potentially top out and the risk of recession should become front and center once again.

For further details see:

Upslope Capital's Q3 2023 Investor Letter