TCVA - Upslope Capital's Q4 2022 Investor Letter

Summary

- Upslope Capital Management is a Colorado registered investment adviser. Upslope's core investment approach is a concentrated, long/short equity strategy, focused on mid-cap businesses.

- 2022 was a good year for Upslope, with strong capital preservation during the most violent months for the market and solid performance during relief periods.

- I believe Upslope’s low-volatility approach can continue to outperform over the long-run.

- Looking ahead, capital preservation remains front and center.

Dear Fellow Investor,

Upslope’s objective is to deliver attractive, equity-like returns with significantly reduced market risk and low correlation versus traditional equity strategies. 2022 was a good year for Upslope, with strong capital preservation during the most violent months for the market and solid performance during relief periods.

| Upslope Exposure & Returns [1] |

| Benchmark Returns |

| Average Net Long |

| Net Return |

| S&P Midcap 400 ETF ( MDY ) |

| HFRX Equity Hedge Index |

| Q4 2022 |

| 61% |

| +11.2% |

| +10.7% |

| +1.7% |

| FY 2022 |

| 67% |

| +6.5% |

| -13.3% |

| -3.2% |

| Since Inception* |

| 49% |

| +9.9% |

| +8.6% |

| +4.0% |

| Note: clients should always check individual statements for returns, which may vary due to timing and other factors. *Since Inception returns are annualized (from August 2016). |

MARKET CONDITIONS – THE WAITING PLACE

Investors have been not-so-patiently waiting for an all-clear signal. Markets have become increasingly jumpy on any “news” as a result. It doesn’t matter much if the news is good or bad. Something just needs to happen so investors can feel good about buying stocks.

I’m not sure how the big issues of the day (inflation, rates, housing, geopolitics) resolve, but the outcome that would frustrate the largest number of investors seems to be for markets to remain stuck…waiting for another 6, 12 or 18 months. The current bear market has dragged on for about a year. This compares to the “average” bear of 20 months. A sizable number ran to 30+ months. 2 Extended malaise isn’t out of the question, even if it would feel unprecedented to most active investors today. This isn’t scientific.

In theory, navigating this environment shouldn’t be that complicated (not to be confused with “easy”). But it’s a different playbook than those that were most successful for the past decade. It involves leaning on traditional value stocks (as opposed to high-class compounders or fallen growth stocks), being extra disciplined with valuation, and staying nimble. Trimming (or adding to) stocks purely on… gasp …valuation grounds is probably wise. There will come a time when letting longs run further valuation-wise makes sense. But that’s beyond The Waiting Place. Morgan Stanley’s Mike Wilson echoed this sentiment in a recent note,

“...a Fed pause will likely not lead to higher P/Es if growth is really rolling over.”

Upslope’s portfolio and recent actions reflect the above. Tactical Longs (aka traditional value) comprise the bulk of our longs and recent adds. This group is more diverse than in the past, reflecting a view that most traditional value stocks are almost by definition higher risk. It also reflects ongoing testing of “starter” positions noted last quarter (so far, so good). An overview of recent purchases, including the starters previously alluded to, is provided below.

PORTFOLIO POSITIONING

At quarter-end, gross and beta-adjusted net exposures were 148% and 28%, respectively. Positioning reflects a heightened number of perceived opportunities, particularly on the long side of the portfolio (offset with elevated hedges).

Exhibit 1: Upslope Portfolio Snapshot

{kind=link}

Exhibit 1: Upslope Portfolio Snapshot (Source: Upslope. )

| Note: as of 12/31/22 and may change without notice. |

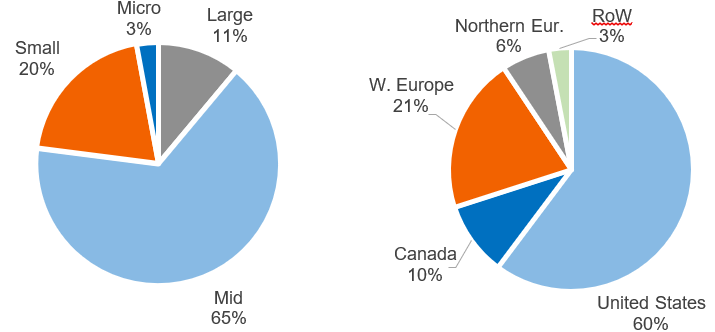

Exhibit 2: Gross Exposure by Market Cap & Geography

{kind=link}

Exhibit 2: Gross Exposure by Market Cap & Geography (Source: Upslope, Interactive Brokers, Sentieo. )

| Note: as of 12/31/22. Market cap ranges: Micro (<$400mm), Small ($400mm - $3bn), Mid ($3bn - $13.5bn), Large (>$13.5bn). |

PORTFOLIO UPDATES

The largest contributors to and detractors from quarterly performance are noted below. Gross contribution to overall portfolio return is noted in parentheses.

Exhibit 3: Top Contributors to Quarterly Performance (Gross)

| Top Contributors |

| Top Detractors |

| Long: Kongsberg (+295 bps) |

| Short: Hedges, net (-220 bps) |

| Long: Silgan ( SLGN , +210 bps) |

| Short: Undisclosed (-75 bps) |

| Long: Diploma ( DPMAY , +205 bps) |

| Short: Undisclosed (-60 bps) |

| Longs – Total Contribution |

| Shorts – Total Contribution |

| +1,535 bps |

| -295 bps |

| Source: Upslope, LICCAR, Interactive Brokers Note: Amounts may not tie with aggregate performance figures due to rounding. |

Casey’s ( CASY ) – Exited Long

Focused exclusively on the Midwest/South, Casey’s is the third largest independent convenience store operator in the U.S. The company has executed well and shares have outperformed a challenging market nicely since the position was initiated a year ago. It may seem strange to sell a position with this backdrop, but I did so for two reasons. First, it was purchased in the first place as a reasonably priced defensive during an orgy of speculation. In this context, CASY served its purpose. Second, given the developments of the past year and Upslope’s overall still-defensive portfolio, I think there are better uses of capital today – specifically cheaper, less-defensive longs. Some of these are highlighted in Exhibit 4 below.

TCV Acquisition Corp. ( TCVA ) – Exited Long

TCVA is a pre-transaction SPAC, sponsored by the venture capital firm Technology Crossover Ventures. While I added it in 2021 as a “free” call option (and a loose hedge for SPAC+ shorts), I exited this quarter due to: (a) losing realistic hope for completion of a successful acquisition, and (b) the position becoming a (mild) distraction.

New Longs

Given heightened activity in recent quarters (mostly Q3), a summary table laying out the basics of Upslope’s newest longs is provided below. The table includes the three “starter” positions discussed in the last letter, as well as one new addition (BOK Financial). For the most part, these are still sized somewhat modestly.

CLOSING THOUGHTS

2022 was a good year for Upslope’s strategy, which has outperformed its benchmarks (with far lower volatility) on a 1-, 3-, and 5-year basis, as well as since inception. A thoughtful and well-aligned client base that “gets” what Upslope’s defensive approach is and is not supposed to do was a key enabler of this result.

I believe Upslope’s low-volatility approach can continue to outperform over the long-run. While embracing volatility in exchange for theoretically higher long-term returns has become trendy in recent years, the style has never appealed to me. The basic decay math that $1.00 invested in a return stream of {+20%, -20%, +20%, -20%} will ultimately be worth $0.92 is under-appreciated, in my view. Volatility does matter – not just in helping clients stay the course, but also in delivering long-term outperformance.

Looking ahead, capital preservation remains front and center. Nevertheless, I am trying hard to be as openminded as possible for better times ahead.

Thank you again for the trust you’ve placed in me to manage a portion of your hard-earned money. If you have any questions at all, would like to add to your account, or know someone who may be a good fit for Upslope’s atypical approach, please call or email anytime.

Sincerely,

George K. Livadas

Appendix A

Appendix B

Appendix C: Portfolio Company ((Long)) Descriptions

AptarGroup ( ATR ) : Specialty packaging business focused on pumps and sprayers, with a highly profitable, defensive, and growing Pharma unit. Misclassified and undervalued due to legacy/traditional packaging businesses (Food + Beverage, Beauty + Home), which contribute 60% of sales but just 15% of EBIT.

ATS Corp. ( ATSAF ) : Canada-based factory automation solutions provider primarily serving defensive end markets (healthcare, food, etc.) in N. America and Europe. Active acquisition strategy + potentially accelerating reshoring tailwinds should sustain growth ahead.

BOK Financial ( BOKF ) : Regional bank based in and primarily focused on OK, as well as TX, NM, and CO. Conservative culture + unique energy expertise + modest valuation support BOKF shares on a standalone basis. Also view position as a portfolio hedge in the event of sustained, elevated rates and/or energy prices.

Bolsa Mexicana de Valores ( BOMXF ) : Dominant financial exchange operator in Mexico. Despite known headwinds in its equities business, the company is diversified, highly cash generative, conservatively managed, and shares appear a cheap call option on global macro reacceleration and/or Mexico resurgence.

CACI International ( CACI ) : Specialized technology and consulting services provider, primarily to U.S. defense and intelligence agencies. Anticipate company will benefit from geopolitical tailwinds, strong position in cyber defense, and continued consolidation opportunities.

Chemring ( CMGMF ) : Niche defense contractor focused on Countermeasures & Energetics (defensive flares, specialty explosives) and Sensors & Info (cyber warfare, explosive/chem/bio detection). End markets should outgrow defense market for years; also has elevated “conflict-driven” demand exposure.

Diploma ( DPMAY ) : U.K.-based specialty distributor focused on essential consumable products across life sciences, seals (machinery), and controls (aerospace wiring/harnesses). Unique model and conservative M&A strategy have historically enabled attractive free cash flow growth through the cycle.

FTI Consulting ( FCN ) : Boutique consulting and advisory firm, with leading expertise in restructuring, dispute advisory, and other practices. Should ultimately benefit from elevated deal flow in wake of longer-term pandemic effects (e.g. rising rates and SPAC boom/bust) and restructuring cycle.

Glatfelter ( GLT ) : Specialty materials company with most of its footprint in W. Europe. Commodity products largely serve defensive end markets (e.g. tea, hygiene). Significant exposure to E. Europe + ill-timed M&A put company in distress. Anticipate easing inflation to “bail out” the company, regardless of other macro considerations.

Kongsberg Gruppen ( NSKFF ) : 200+ year old defense (missile/defense, remote weapons systems) and maritime (offshore, commercial) business, majority owned by Norwegian government. Dominant positions in niche products with cyclically attractive end markets, strong management team and solid balance sheet.

Man Group ( MNGPF ) : UK-based alt. manager with $138bn of AUM (70% alts, 30% long-only). Differentiated, strategies focused on public, liquid markets have withstood sector headwinds well over years and could see resurgence, given dramatically changed macro environment. Position also provides portfolio with “cheap beta.”

Silgan Holdings ( SLGN ) : Food can, dispensing system, and plastic packaging producer managed with a private equity mindset. Defensive end markets, attractive valuation and disciplined model make for attractive baseline investment with balance sheet optionality (M&A or capital return).

Tecan Group ( TCHBF ) : Switzerland-based lab automation and consumables business, with leading market position in automated liquid handling. Attractive and defensible base business greatly enhanced by exceptional execution during the pandemic.

TMX Group ( TMXXF ) : Largest exchange operator in Canada with exposure to equities, fixed income, and derivatives, as well as European power/energy trading/data. Anticipate steady, defensive growth with outperformance during periods of elevated inflation and/or volatility.

| Upslope Capital Management, LLC (“Upslope”) is a Colorado registered investment adviser. Information presented is for discussion and educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. While Upslope believes all information herein is from reliable sources, no representation or warranty can be made with respect to its completeness. Any projections, market outlooks, or estimates in these materials are forward-looking statements and are based upon internal analysis and certain assumptions, which reflect the views of Upslope and should not be construed to be indicative of actual events that will occur. As such, the information may change in the future should any of the economic or market conditions Upslope used to base its assumptions change. The description of investment strategies in these materials is intended to be a summary and should not be considered an exhaustive and complete description of the potential investment strategies used by Upslope discussed herein. Varied investment strategies may be added or subtracted from Upslope in accordance with related Investment Advisory Contracts by Upslope in its sole and absolute discretion. Any specific security or investment examples in these materials are meant to serve as examples of Upslope’s investment process only. There is no assurance that Upslope Capital will make any investments with the same or similar characteristics as any investments presented. The investments are presented for discussion purposes only and are not a reliable indicator of the performance or investment profile of any composite or client account. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Any index or benchmark comparisons herein are provided for informational purposes only and should not be used as the basis for making an investment decision. There are significant differences between Upslope’s strategy and the benchmarks referenced, including, but not limited to, risk profile, liquidity, volatility, and asset composition. You should not rely on these materials as the basis upon which to make an investment decision. There can be no assurance that investment objectives will be achieved. Clients must be prepared to bear the risk of a loss of their investment. Any performance shown for relevant time periods is based upon a composite of actual trading in accounts managed by Upslope under a similar strategy. Except where otherwise noted, performance is shown net of management and incentive fees (where applicable), and all trading costs charged by the custodian. Composite performance calculations have been independently verified by LICCAR, LLC. Performance of client portfolios may differ materially due to differences in fee structures, the timing related to additional client deposits or withdrawals and the actual deployment and investment of a client portfolio, the length of time various positions are held, the client’s objectives and restrictions, and fees and expenses incurred by any specific individual portfolio. Benchmarks: Upslope’s performance results shown are compared to the performance of the HFRX Equity Hedge Index, as well as the exchange-traded fund that tracks the S&P Midcap 400 (ticker: MDY). The HFRX Equity Hedge Index is typically not available for direct investment. Benchmark results do not reflect trading fees and expenses. The HFRX Equity Hedge Index (source: Hedge Fund Research, Inc. www.hedgefundresearch.com, © 2023 Hedge Fund Research, Inc. All rights reserved) was chosen for comparison as it is generally well recognized as an indicator or representation of the performance of equity-focused hedge fund products. Any other benchmarks noted and used by Upslope have not been selected to represent an appropriate benchmark to compare an investor’s performance, but rather are disclosed to allow for comparison of the investor’s performance to that of certain well-known and widely recognized, investable indexes. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS These materials may not be disseminated without the prior written consent of Upslope Capital Management, LLC. |

| Footnotes [1] Unless otherwise noted, returns shown for a composite of all accounts invested according to Upslope’s core long/short strategy. Please see important performance-related details and disclosures in Appendix A. 2 Source: J.P. Morgan Asset Management, 1Q 2023 Guide to the Markets . |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Upslope Capital's Q4 2022 Investor Letter