UPST - Upstart: Things Are About To Get Worse In 2024

2023-11-29 03:43:33 ET

Summary

- Upstart's 3Q23 results were slightly below guidance and expectations.

- The market environment is worsening as even prime borrowers are showing weakness, leading to lower approval rates by UPST.

- The company also did not obtain material long-term committed funding as the funding environment remains challenging.

- On a positive note, Upstart continued to improve the model accuracy and make progress on other aspects of its business like auto and HELOC.

- Guidance was also weaker than expected as management expects no sequential growth in the next quarter amidst a challenging environment.

Upstart ( UPST ) recently reported 3Q23 results.

This was a great snapshot of the shape of the business, the macro environment, and the funding environment.

I have covered Upstart extensively in my previous articles, which can be found here .

Since the last article, I have further downgraded Upstart from a Hold to Sell rating. In the previous article, the Hold rating was on the premise that there was no margin of safety in entering Upstart at the valuation.

That said, the backdrop and fundamentals of the company have continued to deteriorate in the past few months.

In general, 3Q23 was yet another challenging quarter for the company as the macro and funding environment remains a challenging one for Upstart, which is one of the contributing factors for the downgrade given a difficult funding environment impedes the entire business.

On top of that, the difficult macro environment is causing consumers to weaken, with even prime borrowers starting to show weakness in the quarter.

As a result, I expect things to get much worse in 2024 before we see an improvement and thus, I am downgrading the stock to a Sell rating.

Let us dive right into the details.

How was Upstart's 3Q23 results?

For 3Q23, results were just a touch below guidance and expectations.

Transaction volume increased 4% sequentially, while total revenues declined slightly sequentially. Both missed street estimates by about 4%.

Contribution margin fell by 260 basis points to 64.2%, 80 basis points below guidance but it remains well above its historical levels.

Marketing spend was up $9 million sequentially due to a rising mix of new customers rather than repeat borrowers. For these newer customers, they come with higher acquisition costs having been new to the platform.

Adjusted EBITDA came in at $2 million missing the street and guidance of $6 million and $5 million respectively.

Market environment and platform constraint

To be clear, the market environment in 3Q23 was not an easy one for Upstart. On its platform, rates offered were higher than the company expected them to be, and it reached an all-time high in the quarter.

This, of course, is due to the high interest rate environment as well as significantly elevated risk in the consumer economy.

In turn, this has resulted in a difficult environment for growth as Upstart continues to want to operate responsibly in this current environment.

Management mentioned this multiple times in the earnings call as being conservative and prudent looks to be their top priority in the near term, as should rightly be.

As a result, in 3Q23, the company decided to forgo growing quickly, and instead, decided to operate in a conservative manner. This means continuing to manage the company well financially by being EBITDA positive for the second quarter.

The constraint of platform growth for most of 3Q23 has been Upstart's ability to approve borrowers in this current market environment.

Realistically, loan volumes have been constrained as Upstart has made the decision for fewer approvals given the environment, as well as consumers accepting Upstart's loans at a lower rate.

Only 30% of applicants are accepting Upstart's loan terms, compared to 60% historically.

In addition, Upstart's fewer approvals were due to the company tightening lending standards in response to weakness in prime borrowers.

The next question would be more on the funding side of things and whether funding will likely see improvements in the near-term.

Funding

The key question for Upstart has been on the funding side of things given that it has been a major constraint for the company for the past few months.

I think Upstart is certainly taking the right step forward by continuing to try to pursue a large number of committed funding partnerships and they are in discussions for these partnerships and structures.

While there was a comment made in the 3Q23 earnings call that recently, there has been significant institutional capital raised for deployment into private credit and that there are encouraging trends for the volume of discussion and negotiation, these remain just discussions and have not progressed to anything more.

Unfortunately, there was no concrete update to Upstart's committed capital base in 3Q23 as the company did not close any meaningful committed capital deals in the quarter.

The lack of any large, committed funding partnership is also concerning me given it has been some time since management has started this initiative.

I also found it odd that management was trying to downplay the importance of the funding side in 3Q23 by explaining that it is not the constraint of the quarter. Instead, management stated that the borrower side and the company's inability to approve loans are the main platform constraints today.

However, when things start to improve, Upstart will definitely need this long-term committed capital when the volumes start returning.

Last but not least, management does not expect the funding or macro environment to ease over the next few months.

All these facts point to an increasingly challenging near-term outlook for Upstart, which is already struggling in the current environment today.

Improvements to the model

The backbone of Upstart is its AI platform and model.

In 3Q23, the company launched Model 15.0 , which is the most recent core personal loan underwriting model.

One of the most improvements to the model is model accuracy and for Model 15.0, it improved model accuracy by 15%, which is the largest improvement the platform has seen since tracking these improvements in 2018.

In fact, this model accuracy improvement was larger by a factor of 1.5, according to the company.

One addition to the new version was to add personalized timing curves, which led to a huge accuracy improvement, and this new version also added personalized macro effects to the model for the very first time.

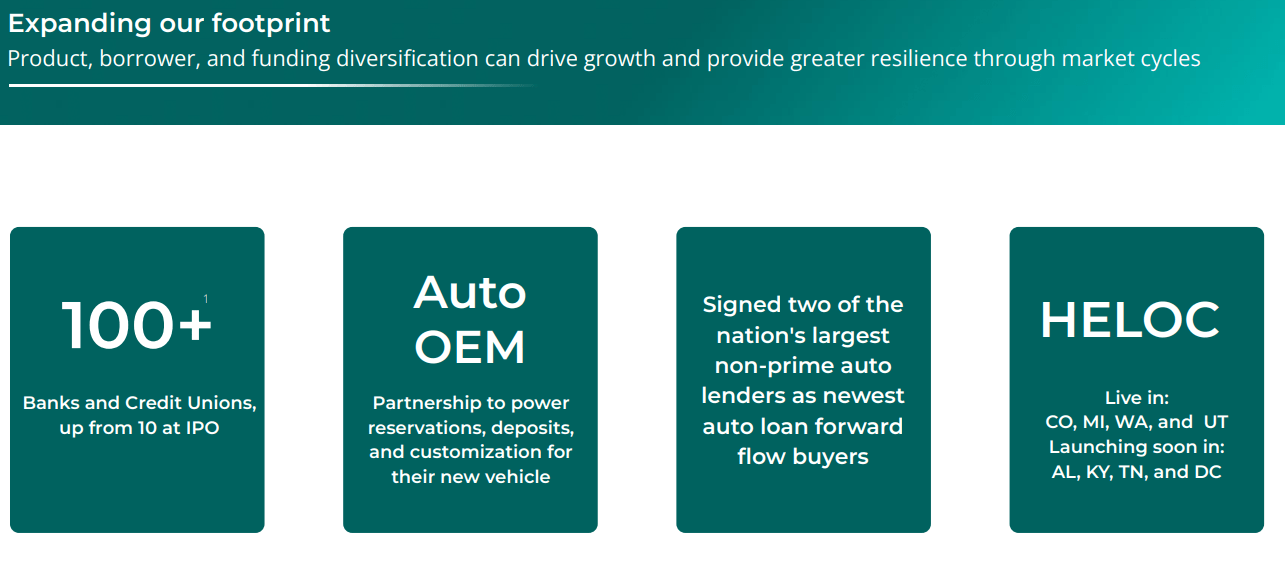

Business opportunities

The autos side of things got a big boost in multiple areas.

Firstly, Upstart is partnering with a major OEM to implement its software for the launch of a new vehicle. Upstart's auto retail platform powered its customer reservation, deposit and customization and was implemented in 99% of all its dealerships in the US.

In addition, Upstart expanded the car dealerships from 61 to 69 in the quarter and the company has expanded its reach to 70% of the US population as it added support for rooftops in Arkansas, Maryland and Virginia, expanding our reach to 70% of the US population.

Also, Upstart signed agreements with two of the largest national, non-prime auto lenders, both of which will help fund its auto lending solutions.

However, auto loan volume declined 48% sequentially to $29 million, its lowest level since 2Q21, peaking in 1Q22 at $219 million.

New business opportunities (Upstart)

{kind=link}

Upstart is expanding its home equity product to four new states and early feedback from applicants has been positive, especially around speed to fund.

Guidance

Guidance was weaker than expectations.

4Q23 revenues are expected to come in at $135 million, 7% below consensus expectations.

Management expects contribution margin to further decline 200 basis points sequentially in 4Q23.

The company expects EBITDA to come in at breakeven in 4Q23, $10 million to $15 million below consensus expectations.

Valuation

Forecasting Upstart's financials is somewhat challenging because it depends on multiple factors like the macro environment, and how the platform constraints play out.

Based on 4Q23 guidance, there is no sequential volume or revenue growth for the next quarter while contribution margins are expected to come in lower.

As such, my financial forecasts for Upstart have also been revised lower to reflect this. I expect 2025 to be the year where things become more normalized for the company as the macro environment becomes more favorable.

With the revisions of the financial forecasts for Upstart, the 1-year and 3-year price targets are revised down $25.20.

I will share more of my thoughts on the opportunity for Upstart in the conclusion section below.

Conclusion

The investment thesis for Upstart is a tricky one.

The long-term potential of the company looks promising as the company continues to focus on improving fundamentals and taking a conservative approach.

In the short term though, I think things will remain challenging in the near term given the comment that management does not expect the funding or the macro environment to ease over the next few months.

Without long-term committed capital or improvements to the macro environment, the business will remain challenged in the near term. It was disappointing that this was the second quarter in a row where there were no major deals on the funding front.

On top of that, with prime borrowers now showing weakness, I think we are starting to enter a downturn in the consumer cycle as the savings rate in the US economy has dropped to historically low levels.

I currently have 4% of my portfolio in Upstart, and this represents the remaining profits from an initial larger position of almost 9%.

On July 21, I sold off my entire cost basis in Upstart as valuations were getting stretched then.

It turned out to be an excellent call because Upstart is down more than 50% since.

Today, I also decided to further de-risk the rest of my remaining profit position in Upstart.

The funding environment remains challenging with no signs of material improvements.

The consumer landscape is worsening with even prime borrowers starting to show weakness.

Even if rates were to come down, the challenged consumer environment would continue to pose a challenge for the company.

As a result, I will be cutting the Upstart position from the current 4% weight to a small 1% weight to continue to monitor the company, get some small upside if there are any positive surprises, and continue to have skin in the game.

I will also be reducing the conviction rating of Upstart to a rating of 1. Without the necessary long-term funding, this increases the risk for Upstart. At the same time, the weakening of prime borrowers, will likely bring an increased risk environment for Upstart to operate in and thus, further justifies the rating downgrade.

Upstart will continue to be very rate sensitive and prone to short squeezes. The company has 30 million shares of short interest, against 72 million shares of float or 85 million shares outstanding, representing 42% of the float and 35% of the shares outstanding.

As a result, I think we will continue to see volatility in the shares in the near term given if there is a positive upside on the business or on the rate front, a short squeeze may drive some upside.

If I start seeing the environment turn or improve, there is definitely scope to increase the weight of Upstart in the portfolio once again.

For further details see:

Upstart: Things Are About To Get Worse In 2024