ISENF - Uranium After The Melt-Up: How Long Can The Bull Market Last?

2024-01-22 08:06:08 ET

Summary

- U3O8 spot prices and investment vehicles Yellow Cake plc and Sprott Physical Uranium Trust are up 125% since my first article in June 2022.

- The uranium spot market is tight, miners are acting out on large price incentives, and nuclear sentiment is as positive as it gets.

- Supply is increasing, signaling a potentially topping market, but Uranium-specific frictions and geopolitical tensions outweigh the current supply increases.

- Investors should be prepared for a 2007esque price spike, but should hope for gradual price hikes.

Since my last article about Yellow Cake (OTCQX: OTCQX:YLLXF ) and Sprott Physical Uranium Trust ( OTCPK:SRUUF ) in late September of last year, the U3O8 vehicles are up around 40% on average. During the same time, the spot price of U3O8 moved roughly 50% to the upside. Once again, the metal outperformed the miners: The Sprott Uranium Miners ETF (URNM) only gained around 17%. The riskier Sprott Junior Uranium Miners ETF ( URNJ ) is up by only 16%.

It’s clear that we are in a red-hot Uranium bull market. Since I published my first article about the Uranium bull case in June of 2022, U3O8 spot prices, and the investment vehicles Yellow Cake plc and Sprott Physical Uranium Trust are up ~ 125%. The metal has outperformed every investable commodity, especially during 2023 when most commodities dropped in price.

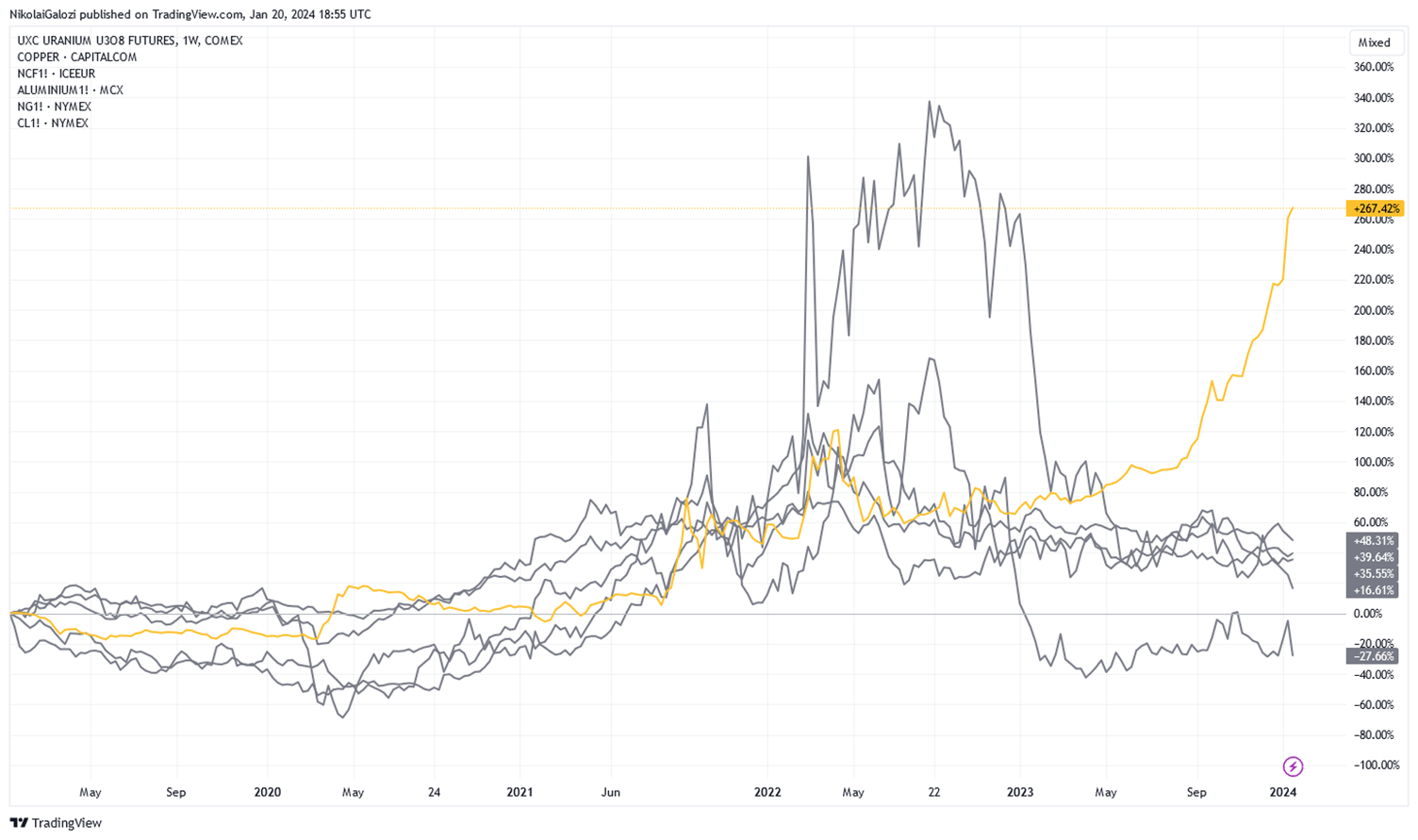

{kind=link}

U3O8 (yellow) and Copper, Iron, Coal, Oil, Aluminum, Natural Gas (grey) (tradingview.com)

In this update article I discuss the progress of the Uranium Bull Cycle. I describe the possible scenarios going forward, the dynamics of demand and supply, the risks from possible regulation for the investment vehicles, and exit scenarios for the investment case in perspective of the possibility of a recession and rate cuts in 2024.

I suggest readers unfamiliar to the uranium investment case to catch up on my previous articles about this subject: Yellow Cake: A Nuclear Buying Opportunity released in April 2023 and my two articles on the Sprott Physical Uranium Trust released in November 2022 and in June 2022 . I won’t go into detail about the basics of the uranium investment case in this article.

Overview of Yellow Cake plc & Sprott Physical Uranium Trust

Yellow Cake plc. is a British uranium trading company established in 2017. The company's core business revolves around purchasing and storing physical uranium (U3O8) as an investment. Yellow Cake's primary goal is to offer investors exposure to the uranium market.

Yellow Cake benefits from a significant strategic advantage owing to its long-term contract with NAC Kazatomprom JSC (Kazatomprom), the largest and one of the lowest-cost uranium producers globally. The contract enables the company to procure uranium at a price agreed upon before announcing any intended purchase or associated financing, allowing Yellow Cake to acquire up to $100 million of U3O8.

Currently, Yellow Cake has acquired approximately 20.1 million pounds of U3O8 – unchanged since April 2023 - which are held in storage accounts at Cameco ( CCJ ) in Canada and Orano in France.

The Sprott Physical Uranium Trust primarily invests in and stores its assets in the form of U3O8 uranium in storage facilities located in the US, Canada, and France. Investors have the option to trade trust units through an at-the-market ((ATM)) program. When the trust shares trade at a 1% premium to their net asset value, the trust can issue more units to the market. These newly issued units are used to purchase additional pounds of uranium, thus raising the fund's NAV while reducing the available physical uranium supply.

Investing in Yellow Cake plc or the Sprott Physical Uranium Trust means speculating on rising U3O8 prices.

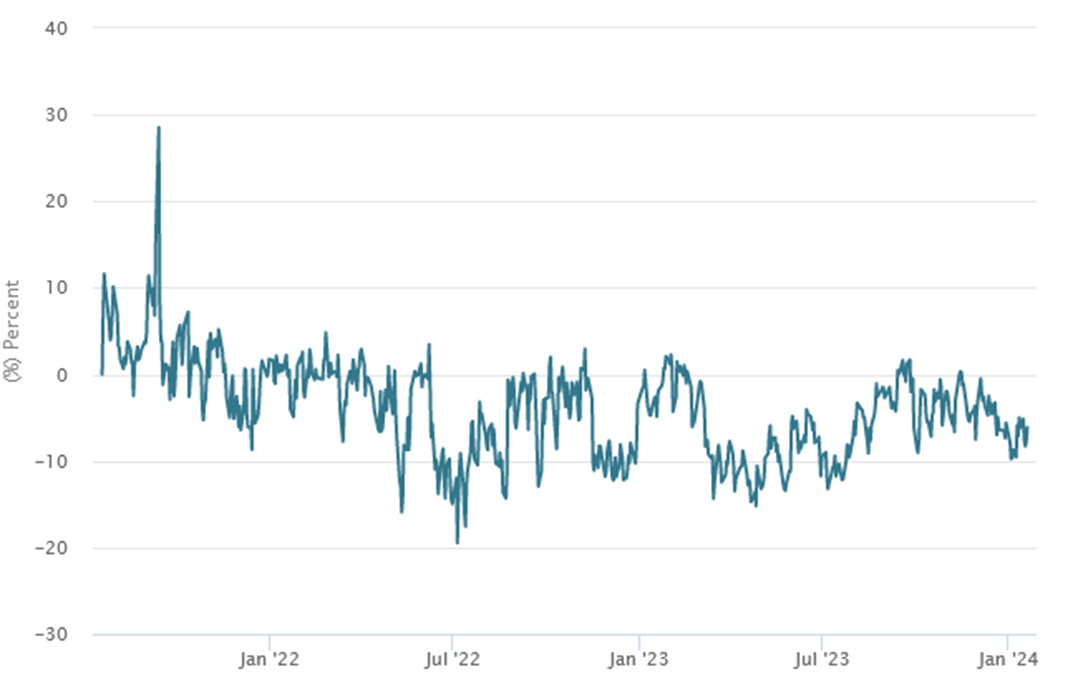

The U3O8-discounts are back again

Even though U3O8 spot prices have soared, the investment vehicles are back at discounts. Sprott Physical Uranium Trust is trading at a ~6% discount to its Net Asset Value. These discounts are not unheard of, and I expect them to stay in the range of 0% - 10%. The same goes for Yellow Cake plc., which trades at a larger discount to Net Asset Value of ~16%.

{kind=link}

Sprott Physical Uranium Trust / Discount to Net Asset Value (sprott.com)

The reemerging discounts clearly show that speculators are not the ones driving the U3O8 spot market, but rather real demand from utilities trying to secure Yellow Cake for their reactors. There have been no major inflows into the investment vehicles, and speculation has been mild, especially in light of the weakening broad markets since the start of 2024.

The spot market is historically tight

The trading volume on the spot market remains fairly limited, while significant price moves started to occur in late 2023. This is a sign that utilities trying to secure Yellow Cake are facing tougher times in securing the metal. While most Uranium contracting occurs outside the spot market, the remarkable aspect is that typical sellers from Japan or China are prioritizing the security of their stocked inventories over profits from selling into the spot market, considering the huge price hike.

Miners around the world are acting out on large price incentives

Spot Uranium prices and long-term contracting Uranium prices have reached a level where every producing or developing company is eager to increase production. This is typically a sign of a topping commodity bull market, where high demand meets rising production, and prices begin to fall. However, Uranium is unique in that almost all currently producing companies have their pounds of Uranium contracted 3-5 years out. Therefore, new supply can only enter the market if new mines actually produce additional pounds to sell. Since increasing production by developing or restarting mines is a complex process, significant additional supply may not hit the market for several years to come.

Denison Mines ( DNN ) will soon bring the new Phoenix mine into operation, producing 4 million pounds of U3O8 in the first year and 9 million pounds during the following three years. Cameco is increasing production at McArthur River by another 4 million pounds of U3O8, and Cigar Lake will remain on full production. If all operations for Energy Fuels ( UUUU ) are successful, they could supply 4 million pounds of Uranium in 2024. For some perspective: these production increases are not enough to outweigh the mere discontinuation of Uranium underfeeding (roughly 25 million pounds per year).

Further out, there is NexGen’s ( NXE ) Arrow project, which will bring in north of 20 million pounds of Uranium per year but won’t come online for several years. Mongolia ISR, in cooperation with the French, is multiple years or even a decade away from nearing production. The Uzbeks are almost guaranteed to increase production, but there is no major production increase for a couple more years.

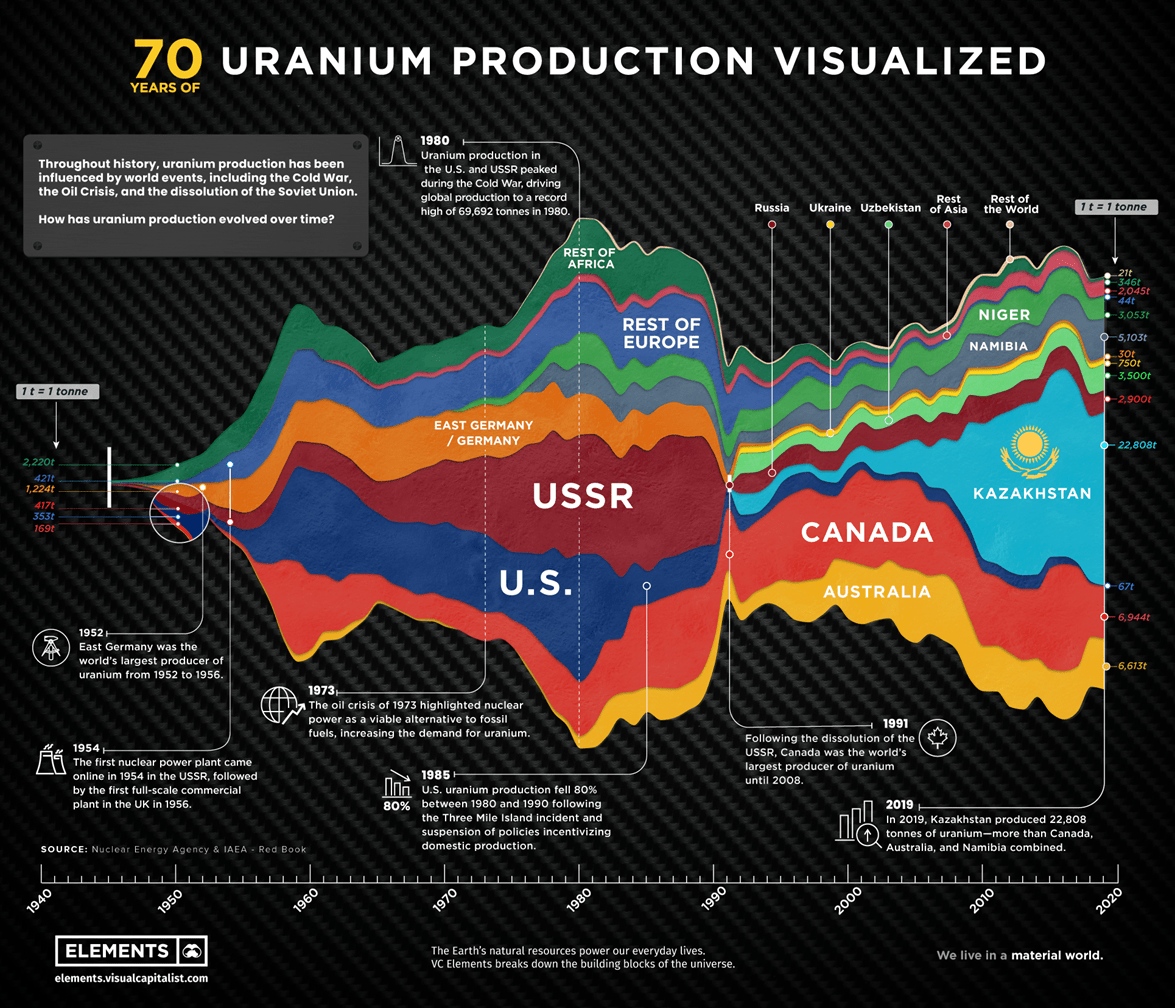

The Kazaks are by far the biggest near-term supplier of Uranium to the market, with a market share of ~43% globally.

{kind=link}

Uranium producers over the last 70 years (elements.visualcapitalist.com)

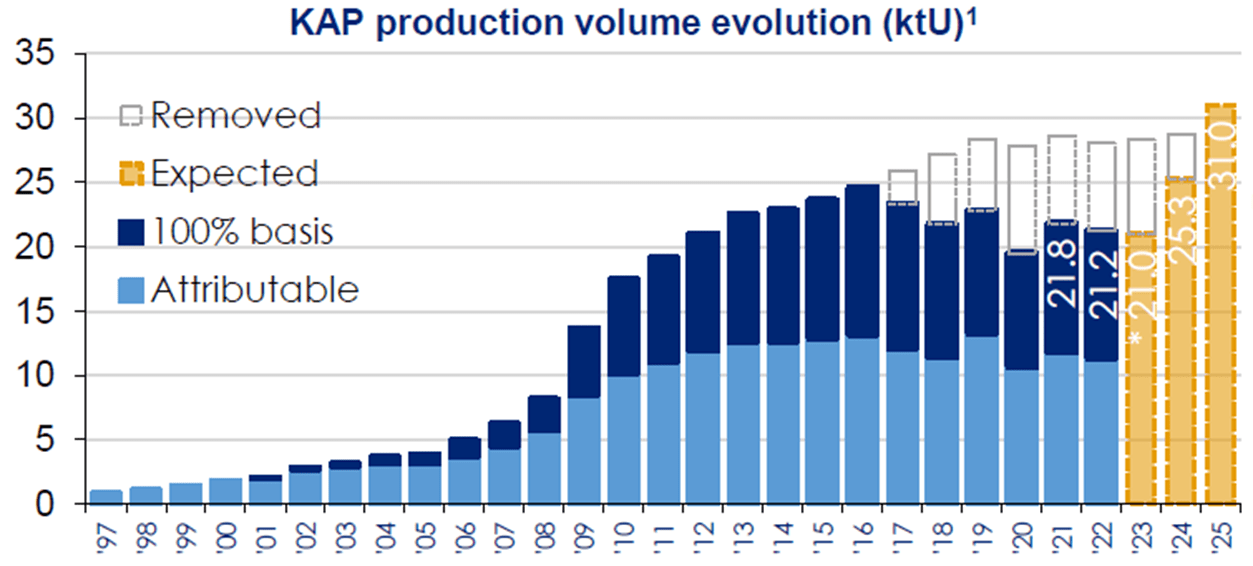

Kazatomprom aims to increase production in 2024 to 25.3 tons of U3O8, representing a substantial increase of roughly 8.6 million pounds compared to 2023. Looking ahead to 2025, Kazatomprom plans to produce 31.0 tons of U3O8.

{kind=link}

Kazatomprom Production Outlook (kazatomprom.kz)

An increase totaling 21.1 million pounds of U3O8 annual production. These projections are by far the most significant for the next two years and must be monitored closely, as they substantially increase supply. However, during the first few weeks of 2024, the company already warns of lower 2024 production in the face of supply shortages and delays in completing construction.

It is clear that we are still a few years away from new mines starting to flood the market with Uranium again. While the large producers are doing everything possible to maximize their production, there is a widening supply and demand gap further out. The 15-year-long bear market has had a lasting impact on the infrastructure of the sector, leaving behind only the biggest and most profitable miners. Kazatomprom, Cameco, and Orano are now reaping the fruits of keeping production alive or possible during bad times.

{kind=link}

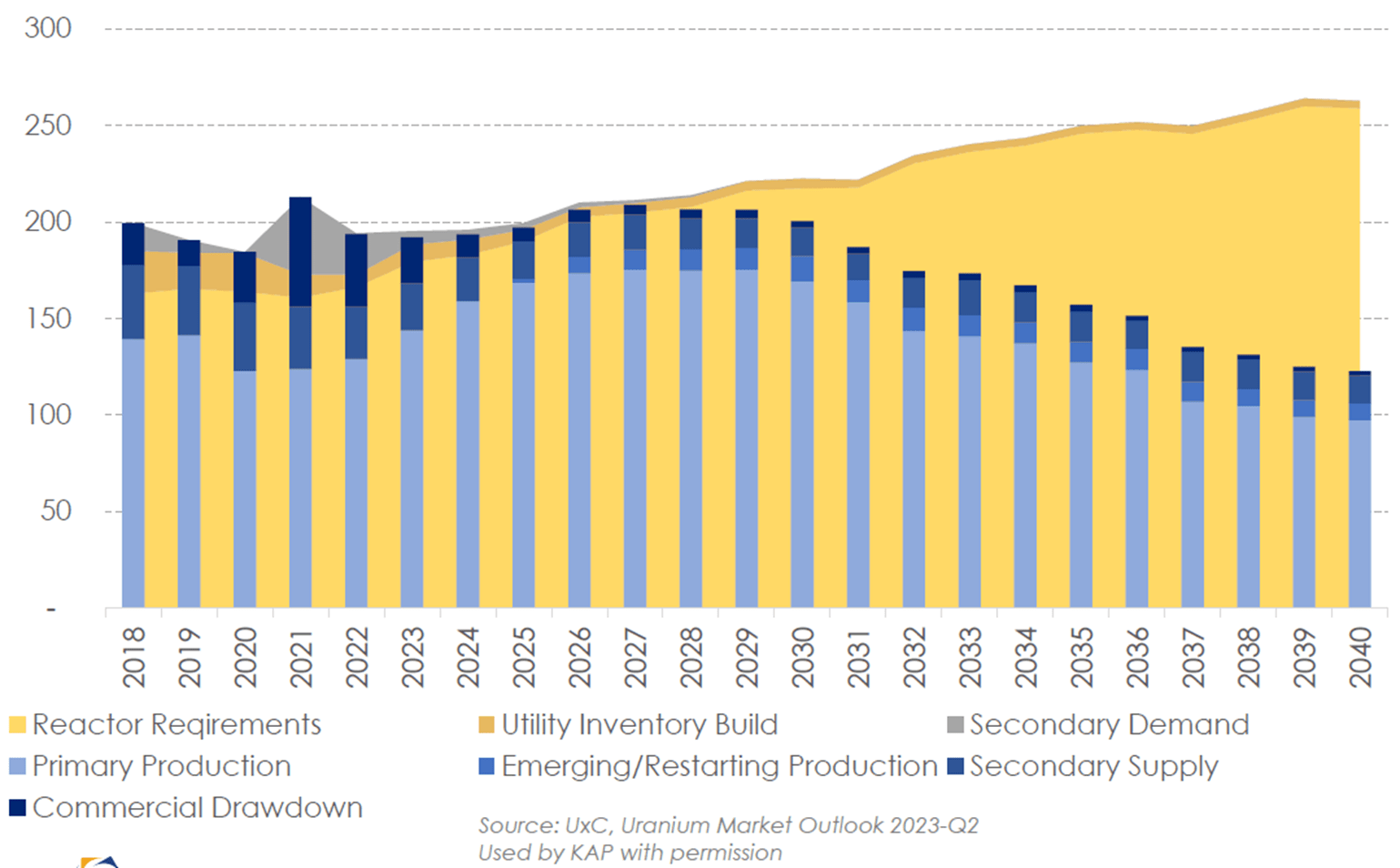

Supply / Demand projections by UxC (kazatomprom.kz)

Make no mistake: I believe the market will peak in the next two years as new supply hits the market and mines develop. There is plenty of incentive to develop even low-grade mines at spot prices in the triple digits. However, the time required to develop Uranium mines leads to the typical prolonged Uranium cycle.

The largest western producer, Cameco, is shifting towards contracts with market references with ceilings well into the 3-digit area and floors around the current long-term price of ~$68. This should speak volumes about where the company thinks prices are headed.

Regulation risks for U3O8 investment vehicles are increasing

With the clear shortage that fuel buyers face, regulatory risks for investment vehicles in Uranium are increasing. Ultimately, the supply of Uranium is vital for most electricity grids – even in my home country Germany, where we import much of the electricity from the French. Utilities usually maintain large inventories because of the immense costs of a reactor shutdown. However, if they encounter difficulties securing the fuel for the next couple of years, and meanwhile, investors are stockpiling Uranium through Yellow Cake and the Sprott Physical Uranium Trust, government interventions are more than likely. The trusts could be forced to sell their Uranium into the market. This could lead to an initial selloff, but in all likelihood, investors will be compensated for the Uranium sold.

Sentiment is as positive as it gets

The sentiment surrounding Uranium and Nuclear Energy is at its peak positivity. Recently, during the United Nations Climate Change Conference (COP28), major global powers jointly declared their commitment to triple nuclear energy capacity by 2050. Currently, China has 26 nuclear reactors under construction and plans for 42 more in the near future. The country aims to establish a total of 150 new reactors by 2035. The ongoing electrification and efforts to reduce CO2 emissions are only feasible with a stable baseload of "climate-friendly" electricity, namely Nuclear. While the Uranium cycle is undeniably supply-side driven, the strong global intentions for long-term nuclear expansion undoubtedly contribute to positive investor sentiment.

2007-esque price spike or gradual price hike?

With the tight spot market, geopolitical tensions surrounding enrichment and conversion facilities, and the significant demand and supply gap, there is more than enough fuel for a price spike reminiscent of 2007. Financial players such as Yellow Cake plc and Sprott Physical Uranium Trust could potentially kickstart the melt-up by pulling additional pounds out of the already tight spot market.

A price spike wouldn’t be ideal for explorers, developers, and producers, as government interventions would be likely. The unsustainability of a price spike would also raise concerns about the longevity of the bull cycle. For investors, a gradual price hike would be preferable due to easier exit timing possibilities.

Exit scenarios and risk adjustments

I believe we are definitely in a territory where a price spike could happen, given all the aforementioned factors. Personally, I am hoping for a gradual price hike, being invested in the Uranium space for now more than two years. However, investors have to be open to both scenarios and size their positions accordingly.

Below my last article in late November I posted about reducing my position size by around 1/3 at $80 Uranium. I plan to take profits in 2024 and 2025 gradually unless we see a real melt-up and signs of broad retail investor interest. Patience seems to be key in this sector, as prices can experience rapid movements, yet also remain flat for several years.

I don’t think the bull market has ended for now. However, the risk/reward is certainly much worse than one or two years ago. I do not believe sentiment around Uranium is going to change in the near future unless we get another Nuclear black swan. The energy crisis makes the need for Nuclear Energy abundantly clear and the climate-disciples should have nothing against it, since the Uranium process doesn’t produce major amounts of CO2. Supply is now increasing, signaling a potentially topping market, but Uranium-specific frictions and geopolitical tensions outweigh the current supply increases. I believe this structural bull market will end when significant additional supply hits the market in 2-3 years. Prices could peak before that if sentiment becomes overly bullish.

For further details see:

Uranium After The Melt-Up: How Long Can The Bull Market Last?