RTNTF - Uranium Energy: Short Report Discussed

2023-03-24 12:41:15 ET

Summary

- I discuss Uranium Energy Corp. in the context of the Kerrisdale Capital short report.

- I go through countless points where I agree with Kerrisdale.

- And points where I believe Kerrisdale is making frivolous assertions.

Investment Thesis

Uranium Energy Corp ( UEC ) was on the receiving end of a short report yesterday.

In the interest of full disclosure, I'm a UEC shareholder. So, everything I say will to some extent be biased.

That being said, my hope is that you'll see my interpretation as being objective and you'll be able to make up your interpretation of the path from here.

The Kerrisdale Capital Short Report: Fact and Fiction

I have to say, most of the Kerrisdale Capital short report's points are true. I have no disagreement with them. In fact, a lot of it is obvious.

For example, UEC is not mining uranium and hasn't been for 10 years. Well, that's obvious.

{kind=link}

Not to overstress the obvious, but uranium has been in a bear market for nearly 10 years. Why would UEC be mining uranium at a loss? That simply would make no sense.

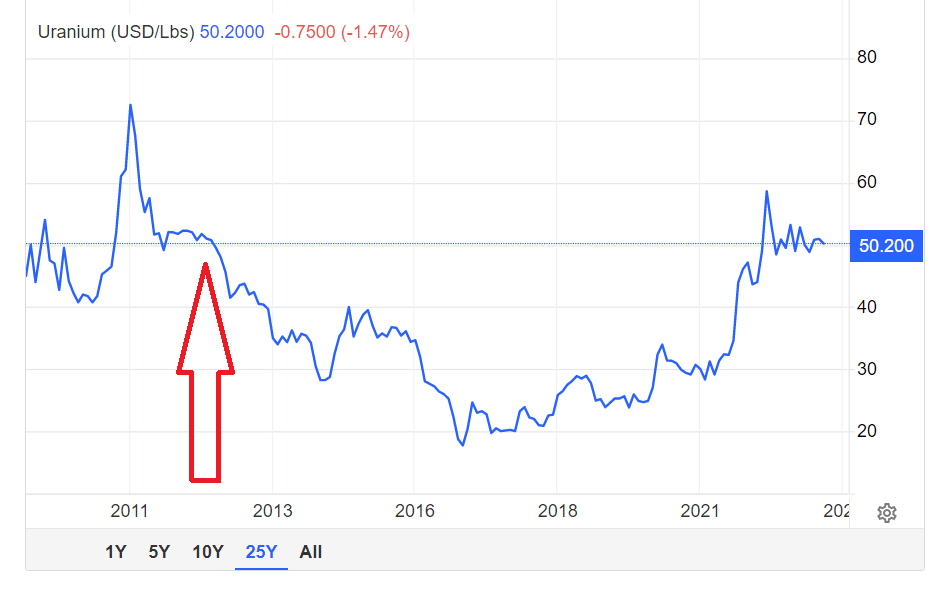

What's more, remember that inflation means that it has a massive impact too. Case in point, $50/lbs of uranium in 2011 equals $65/lbs today. And then, on top of that, the engineering and other service costs mean that UEC simply wouldn't be profitable under $60/lbs.

So again, I pose the question, why would UEC be mining for uranium today, when it's uneconomical to do so?

Moving on, another key argument is around the price that UEC paid for Roughrider. Here's the excerpt (emphasis added):

Roughrider – a uranium deposit in the eastern Athabasca that UEC acquired from Rio Tinto for $146 million in October of last year. Its 58Mlb resource estimate was published by Hathor in 2011 before being acquired by Rio, which promised to re-evaluate the project upon taking ownership. Rio did conduct a reevaluation, but never published it or publicly discussed its findings. It did, however, subsequently write down the $640 million Hathor acquisition tozero before finding a buyer – UEC – that has no experience with mining Athabasca.

The argument is thus, Rio Tinto Group (RIO) wrote off Roughrider after having purchased it in 2011. Look again at the share price of uranium in 2011.

Everyone who knows the uranium market knows that the Fukushima disaster of 2011 dramatically changed everyone's expectations of uranium. From politicians to utility companies. Note, I don't want to get into the political argument that the U.S. considers it more prudent to source refined uranium from Russian than from its own shores, as that can be an endless discussion.

Nonetheless, in North America, there was absolutely no interest in uranium. Yes, the timing wasn't great for Rio Tinto, and yes Rio overpaid at the height of the prior uranium bull market. So what?

Obviously, Rio had to write Roughrider off. There was no value for years in the assets. But time is a great healer. For Rio, a company with a market cap of £88 billion (+$100 billion mcap), Roughrider is nothing more than a distraction, at less than 0.2% of its market cap.

Next, here's another assertion (emphasis added):

UEC has spent the last few years acquiring uranium deposits with both its expensive stock as well as cash raised by issuing its expensive stock.

Again, not to get too pedantic on details, but how else would UEC acquire deposits otherwise? It's not that it made sense to mine them. We already discussed this, under $60/lbs UEC has no place in mining.

Moreover, given that the assets could be acquired cheaply either on the spot market for less than the cost to mine them, or through M&A, then why not buy uranium cheaply?

Next, let's discuss the number of shares:

UEC’s market capitalization, and its success in selling almost half a billion dollars’ worth of stock over the last 20 years (excluding its initial public offering), are a testament to the triumph of the company’s prolific use of paid stock promotion.

How else would the company support itself? It never took on debt. If UEC had held any debt in the past 10 years, it would not have survived the bear market. That's already in the share price today.

Again, I want to make it clear, there's a lot that I agree with the short report, for example, they state,

Cameco ( CCJ ) and Kazatomprom are the public markets ''pure play'' investments that meet that description.

The problem for me is that CCJ is mostly hedged out at higher uranium prices. This works in that it guarantees a floor for CCJ to be profitable at very low uranium prices, but if you want maximum unhedged exposure, CCJ may not be for you.

As for investing in Kazatomprom, that's cool and if that's your cup of tea, to invest a Kazakhstan, then, I'm not going to argue with you. But I would remind you that investing in Kazatomprom may have other risks, that have nothing to do with the price of uranium. Simply put, proceed with caution.

Finally, Kerrisdale argues that CEO Amir Adnani is over-promotional. And here, too, I agree. But I'm in no place to judge. I know that Elon Musk is also highly promotional. So is Bill Ackman, so is Marc Benioff, Tobias Lütke, and so are many other CEOs.

{kind=link}

Furthermore, Kerrisdale notes that Amir pays to be on different outlets. But Amir is interviewed by CNN, too. I'm not saying that Amir isn't paying to be on those outlets. My argument is that Amir is everywhere.

{kind=link}

The Bottom Line

I believe that an investment in Uranium Energy Corp. boils down to this. Do you believe that uranium will get above $60/lbs and stay there? If you do, nothing in this report will change your investment thesis.

If you don't believe that $60/lbs for uranium is on the cards in the next 2 years or less, then, UEC and the whole uranium space is not for you.

Finally, I believe that if one was to articulate a bearish case for Uranium Energy Corp., personally, I would have highlighted a more simplistic question, why is uranium stuck at $50/lbs?

I believe that many bulls underestimate the amount of secondary uranium inventories still around in the market today. And without a view on that and how long until the secondary uranium inventories will take to dry up, that's where the real bear case for Uranium Energy Corp. finds itself! Not on the fact that Uranium Energy Corp. doesn't mine for uranium.

For further details see:

Uranium Energy: Short Report Discussed