UE - Urban Edge: Best To Wait For A Discount

2023-09-18 11:29:30 ET

Summary

- Urban Edge is a retail REIT that operates an attractive portfolio with a resilient tenant base in a market with favorable supply/demand dynamics.

- Its debt is manageable and potential rent growth can be supported in the near term.

- The dividend may appear unsafe, but a closer look at the payment record and the current and historical payout ratio says otherwise.

- Regardless, the dividend yield is relatively unattractive in the current market environment.

- Also, the stock is more or less fairly valued right now; given the absence of a discount, it's best to add it to a watchlist for now and wait.

Urban Edge Properties ( UE ), founded in 2014 and headquartered in New York, NY, is a retail REIT that develops, redevelops, acquires, and manages retail real estate properties, mainly in the Northeast Corridor. It is the result of Vornado Realty Trust ( VNO ) spinning off its retail assets in order to make its portfolio more office-concentrated.

This company has an appealing portfolio, good market positioning, and manageable debt. On top of these, the market doesn't seem to assign a very significant premium for the management of Urban's portfolio. However, there is also no discount to provide investors with a margin of safety.

Even if potential rent growth is realized, the unattractive risk/reward structure here doesn't justify a purchase. In other words, you may make money, but buying this stock right now would be an unwise investment decision. It's best to add it to a watchlist and wait for a greater discount as price is the greatest issue right now. Below, I aim to first explain why it deserves monitoring before I get into valuation which will explain why it doesn't deserve a purchase yet. Let's get into it...

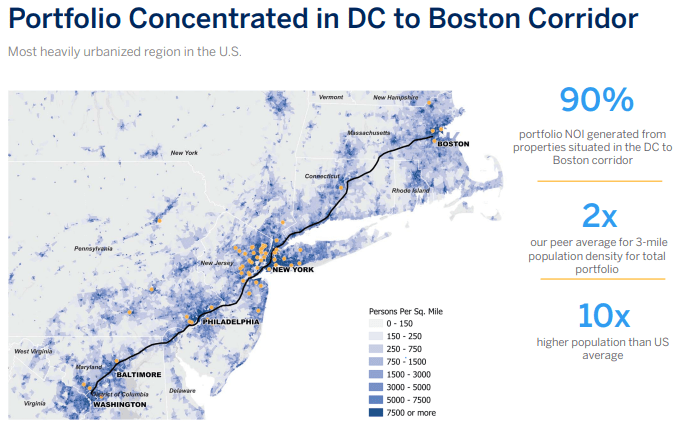

A Geographically Concentrated, Category-Diversified Portfolio

While Urban Edge has a relatively concentrated portfolio geographically-wise, focusing on this can veil how diversified it actually is. It is structured in a way that provides adequate diversification across various retail businesses with a focus on grocers whose profit margins are more resilient in times like these today.

{kind=link}

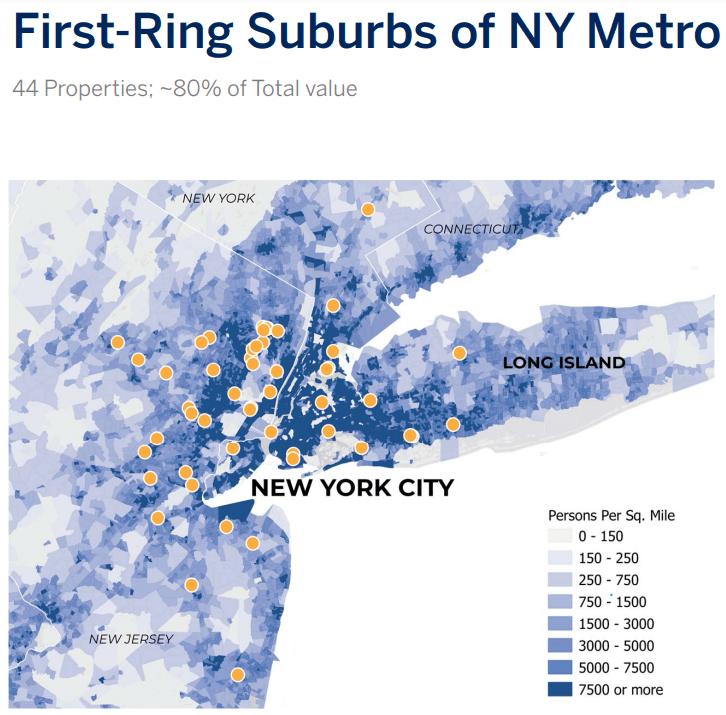

As you can see below, its portfolio is concentrated in New York; it actually has 44 properties there that account for about 80% of its assets:

{kind=link}

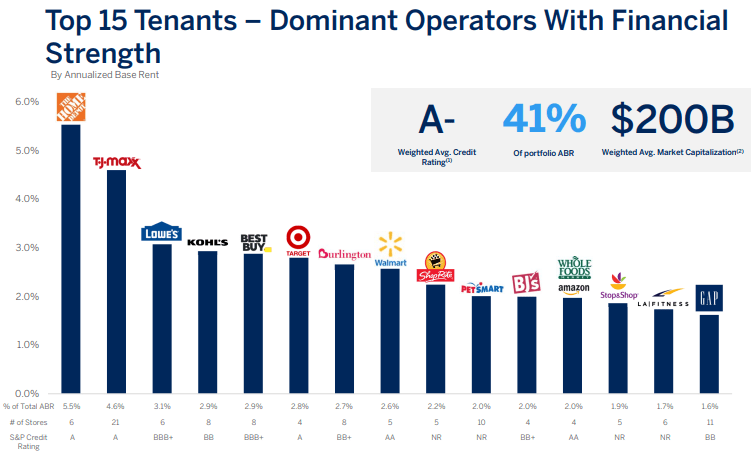

Zooming in, the company's S&P-rated tenants currently score an A- weighted average credit rating and have a $200 billion weighted average market cap. Further, 5.5% of the annualized base rent ((ABR)) comes from Home Depot ( HD ), the biggest ABR source for Urban Edge, with T.J.Maxx close behind at 4.6%; both tenants have an "A" S&P credit rating. Also, 41% of ABR comes from the 15 tenants below:

{kind=link}

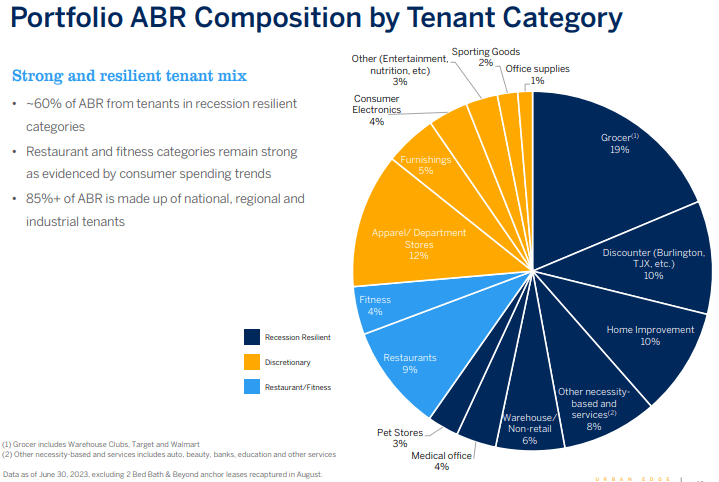

The portfolio also appears well diversified by looking at the various business types the tenants are engaged in:

{kind=link}

About 60% comes from recession "resilient" categories. How resilient each one of them really is may be up for debate, but Urban Edge's largest ABR source is grocery stores (19%), which can indeed prove safer tenants than the rest.

The Not-So-Obvious Growth Potential

Based on the most recent earnings call, the CEO of Urban Edge stated that the occupancy rate was at 95.5%. While this appears adequately high, especially considering the current environment, it's worth noting that he also mentioned that the 3-year average rate was at 98% from 2016 to 2018. So, it's fair to say there's room for improvement. Fortunately, the COO mentioned that the vacancy is represented by 9 spaces, 8 of which are involved in negotiations and 7 already have multiple retail companies bidding for them. And to be completely fair, the occupancy rate for December 31, 2022 and 2021 was 94.3% and 91.1%, respectively; so some growth has already taken place here.

NOI margin was at 28.93% for the second quarter of 2023, up from 26.97% for the same period last year; a modest increase. Zooming out, for the year 2022 NOI margin was 27%, down from 34.8% in 2021. Note that the company enjoyed both a higher rental revenue as well as lower operating expenses in 2021 than it did in 2022. However, same-property NOI was a bit higher in the last quarter YoY; $56.1 million versus $54.9 million. Annual same-property NOI also witnessed an increase from 2021 to 2022, $201.8 million versus $210 million, respectively.

Last, FFO came at $35.9 million in the last quarter versus $36.2 million in the second quarter of 2022. That reflects a modest decrease compared to the annual FFO figures; $180.3 million in 2021 and $145.2 in 2022. That said, H1 2023 AFFO witnessed a slight increase at $53.95 million from $51.8 million during the first half of 2022. However, a decrease in the annual AFFO was observed in 2022; $100.93 million versus $116.6 million in 2021.

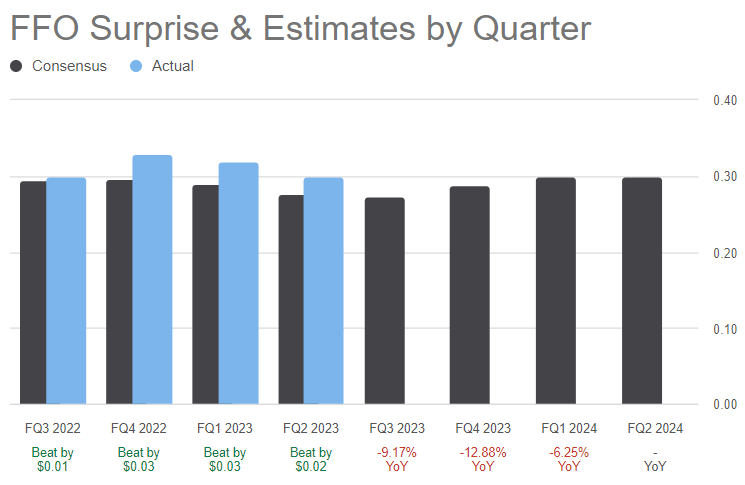

While occupancy is at a relatively attractive level and the recent performance is not alarming, the company has been guiding lower and lower recently:

{kind=link}

Though it has been beating its FFO estimates, guidance represents a significant YoY decrease in profitability in the short term.

That said, the longer-term profitability looks better. During the last earnings call, the CEO stated that the pipeline of signed but not yet opened leases represented 11% of the annual NOI at the time. He added that this is the "fuel" that will help the business realize at least 20% NOI growth in the next 3 years. He also mentioned that 70% of 400,000 sqft of leases at a 40% spread is LOI executed; something that could also help them reach their NOI target.

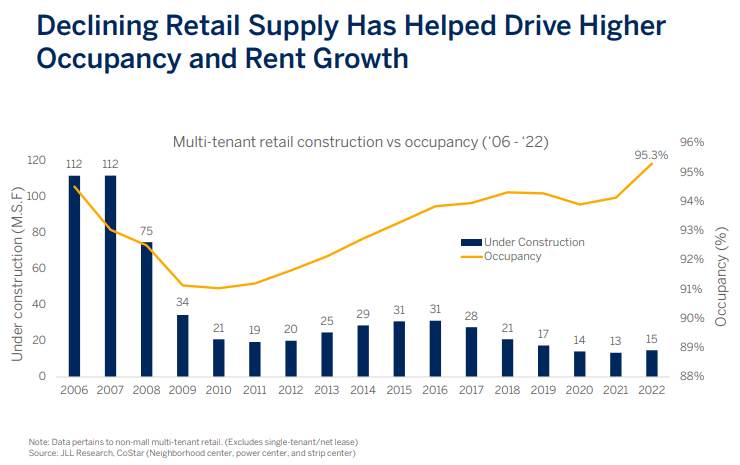

Furthermore, based on the inverse correlation between retail supply and occupancy, it's worth to see where we are right now when it comes to demand:

{kind=link}

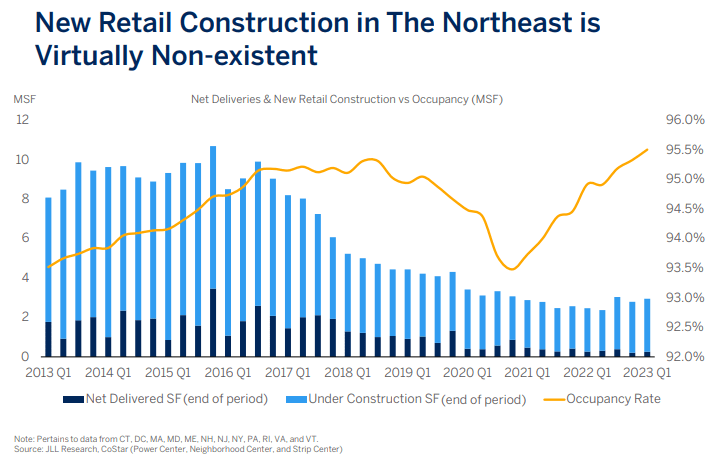

The current retail construction in the area where Urban Edge operates presents an even stronger case:

{kind=link}

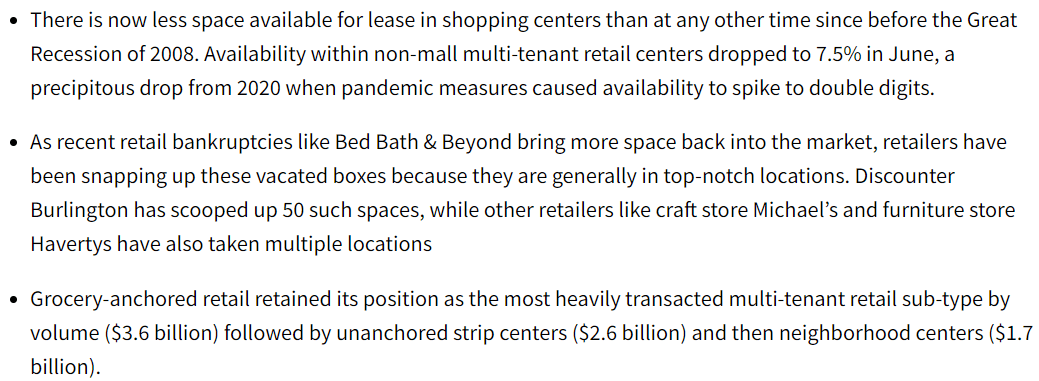

Moreso, based on JLL Research, availability of space is low, demand for properties in top-notch locations is high, and grocers (who as we've seen are responsible for 19% of Urban's ABR) have been the most heavily transacted multi-tenant sub-type.

{kind=link}

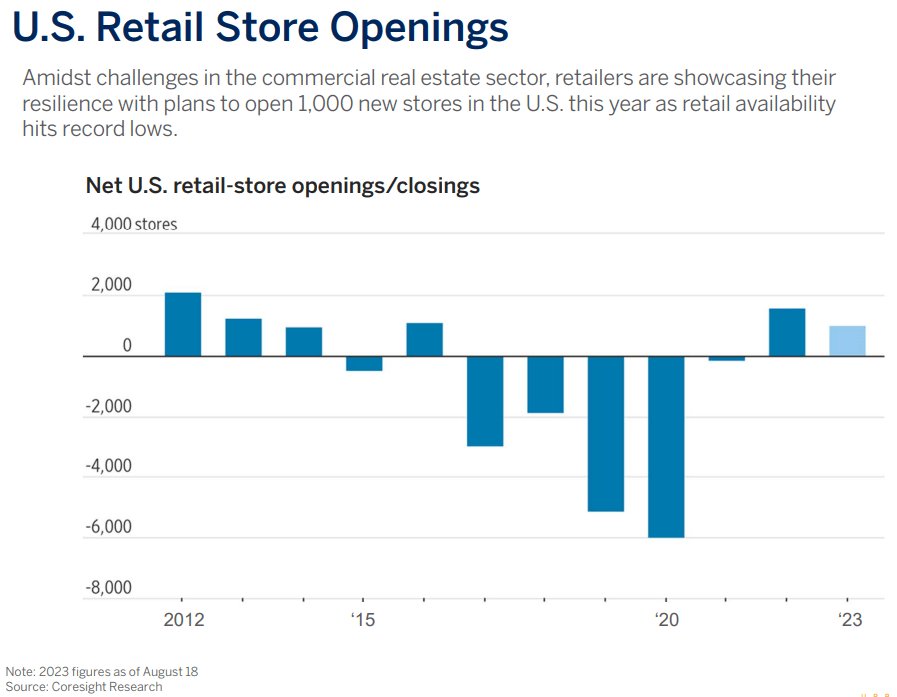

Last, it's important to note that in 2022, there was a net growth in U.S. retail store openings, something that hasn't been observed since 2016 [ source ]. There is also an indication that the same thing will take place in 2023, albeit to a lower degree:

{kind=link}

All in all, although the recent performance of Urban Edge can appear unexciting and the near term even less so, there is a strong case for its improvement in the future.

Manageable Debt for the Next 3 Years

The company's debt-to-EBITDA ratio is a bit high at 8.34x, as is its LTV ratio of 64% based on the total mortgage value and NAV. However, its operating income covered the interest and debt expense by 3 times in the last quarter.

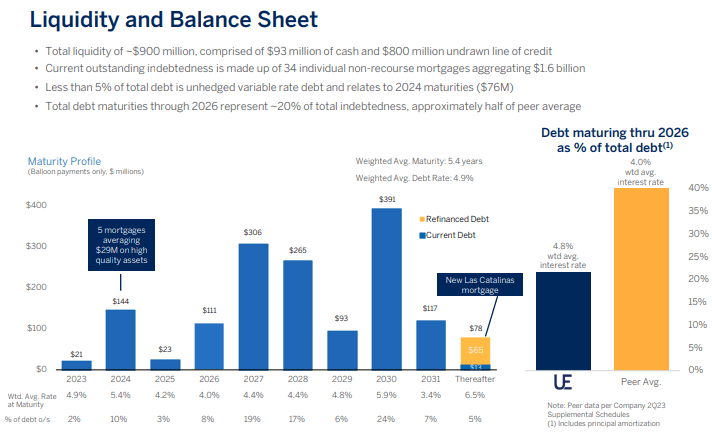

Right now, Urban Edge has secured mortgages amounting to about $1.6 billion. Only 7.7% of them have a variable rate and less than 5% have an unhedged variable rate. The variable rate mortgages have a weighted average rate of 6.32% while the fixed-rate ones have a 4.67% rate.

It's also worth noting that out of the variable-rate mortgages at $129.4 million, $76.4 million of it will mature by the end of the next year. Plus, the remaining ~$53 million will mature in 2027 and currently has a hedged interest rate of 5.26%, the highest it can reach.

Additionally, Urban's CFO, Mark Langer had that to say during the latest earnings call:

Looking forward, we feel very comfortable with our six mortgages maturing in 2024 and 2025, which aggregate only 10% of our total debt amounting to a $173 million at a weighted average in-place rate of 5.3%. These are secured by high-quality assets that we believe are financeable at rates in the 6% to 6.5% range today.

The higher debt cost can be concerning but it may end up being lower come refinancing time. And it's definitely a good thing that the debt that matures is comparatively low in the next two years.

Regardless, we have a good chunk of Urban's debt that matures next year and that deserves some consideration:

{kind=link}

Based on its latest quarterly report, the company is expecting to use some of its $93.4 million in cash, cash equivalents, and restricted cash, along with its undrawn $775.7 million revolving credit facility to cover the upcoming debt obligations. However, it's unclear how much of each it will use.

The revolver agreement involved interest at SOFR plus 1.05% to 1.50%. There is also an annual fee that will be 15 to 30 basis points. On top of that, if the company's leverage ratio increases, the cost may be even higher. Obviously, this can result in a drag on earnings.

That said, the company's maturity schedule for the next 3 years doesn't pose a significant threat. As for the long term, there are indeed some maturities involving large amounts in 2027, 2028, and 2030, but it's not easy to assess what an impact they will have; profitability may be better than today and Urban could secure refinancing at better rates.

Sustainable Dividend, but Not a Good Value

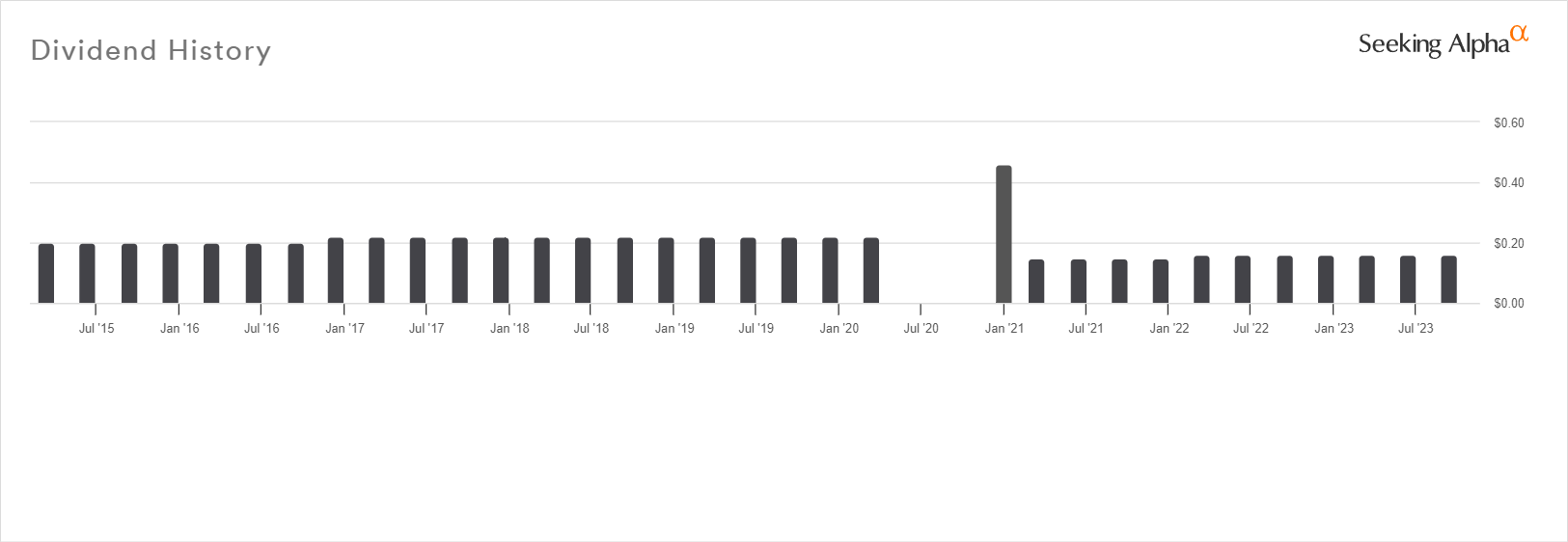

Urban Edge pays a $0.16 per share quarterly dividend. Annualized, it reflects a forward yield of 3.83% right now, which I believe to be sustainable for the rest of 2023 and next year.

First, the payment record reflects an intent to establish a conservative dividend that the company can safely grow over the long term at an equally conservative pace. When the business was spin-offed back in 2015, Urban Edge started with a $0.20 per share dividend which it increased to $0.22 in 2017 and kept paying until 2020, when it temporarily cut it.

{kind=link}

Personally, I would excuse the bump in the road even if they didn't try to make up for the cut; but they did. A special $0.46 dividend was paid in January 2021, which offset most of the loss ($0.66) in dividend income for shareholders.

In February 2021, Urban Edge reinstated the dividend at the historically more conservative amount of $0.15 per share. Given the market uncertainty during the time, I can't really blame them for playing it safe. However, I see an intent to slowly grow it as things stabilize because in August 2022 they increased it to $0.16, which they have been paying since.

Additionally, the payout ratio for the fiscal year 2022 came at 74.3% based on the AFFO of $100.93 million and a total distribution of $75 million. The ratio is about the same even when using the average AFFO figure of the last 3 fiscal years (70.8%) due to the predictable nature of rent income; $116.6 million in AFFO during 2021 and $99.8 million during 2020. Lastly, the payout ratio for the first half of 2023 was 69.6%.

All of this along with the growth potential in rental income in the near term makes the dividend not only sustainable but likely to grow as well. But this doesn't mean the current yield is a good value of course; especially in the current high interest-rate environment.

Based on Seeking Alpha, the stock is trading at 14 times its forward FFO right now, with the sector median at 12.2 times. Additionally, it is trading at a 6.17% implied cap rate. Now, commercial cap rates are forecast to average 6.39% and 6.26% in 2023 and 2024, respectively [ source ]. Therefore, the market more or less fairly values Urban's assets right now if we assume that the observed premium justifiably relates to the REIT's management.

Looking forward, the company's occupancy rate may grow in the near term as the overwhelming majority of the vacant properties are already under negotiations. This could increase NAV in the absence of materially offsetting factors regarding NOI. If the market doesn't adjust for this growth (which I doubt), another look at Urban would be worth our time.

Risks

The obvious risk is related to the retail industry in general because rent collections depend on it being stable. More specifically, Urban Edge relies on 15 businesses for a large chunk of its rental income as we noticed above, with Home Depot accounting for 5.4% of total revenue for 2022. If something were to impact their profits significantly, Urban's earnings may take a hit.

Another risk has to do with the LOIs regarding the currently vacant properties in case Urban doesn't come to an agreement with those prospective tenants.

Last, a short-term risk involves another rate hike which could put more pressure on the stock price. Even though some progress was made with inflation and it's possible that the Fed doesn't intend to raise rates but isn't willing to state so at the same time, a minority of economists expect one more by the end of 2023 [ source ].

Verdict

There's no doubt that Urban Edge manages an attractive portfolio of properties in a market with favorable supply/demand dynamics and a resilient tenant base. The growth potential is also there with multiple drivers in place. However, I believe that investors should hold back for now and content themselves with adding it to a watchlist.

There is no significant premium reflected in the stock price, but there is no margin of safety either. And with a ~4% dividend yield, there is no reason to risk it even in the context of a well-diversified portfolio.

Now, what are your thoughts? Do you own UE or intend to? Did this post help you in any way? I'm looking forward to your comments below and having a conversation with you all. Thank you for reading!

For further details see:

Urban Edge: Best To Wait For A Discount