UE - Urban Edge: Large Tenants Impressive Redevelopment Pipeline And Cheap

2023-10-09 04:05:58 ET

Summary

- Urban Edge Properties is expected to deliver a redevelopment pipeline worth $196.5 million, increasing capacity in 2023, 2024, and 2025.

- The company is working with well-known brands, and most tenants are large organizations.

- The recent focus on ESG investing may attract more funds to invest in Urban Edge Properties.

Urban Edge Properties (UE) is expected to deliver a redevelopment pipeline worth $196.5 million, which may increase capacity in 2023, 2024, and 2025. The company is also working with better brands, and most tenants are large organizations. Additionally, considering recent ESG efforts, I believe that more funds focused on ESG investments may pay more attention to the stock of Urban Edge Properties. There are some risks from the growth of the e-commerce industry, and the debt obligations are not small, however, I think that the stock appears cheap.

Urban Edge, And Its Redevelopment Pipeline

With a portfolio made up of 69 shopping centers, 5 malls, and 2 parking buildings that currently have 90% occupancy, Urban Edge is a real estate business company that concentrates its activity in the Boston and Washington DC corridor.

The company seeks to increase its business by focusing on urban areas due to the existing population density and the number of old buildings available for readaptation or remodeling in other types of applications. Although its assets at present are buildings of magnitude, the current strategy is oriented towards the development of retail businesses, particularly warehouses and industrial residential storage spaces, as well as medical uses.

Among the positive aspects of the corporate organization, we must say that none of these tenants occupies more than 10% of the annual income, the largest client in this sense appears to be Home Depot ( HD ).

All these activities are brought together in a single business segment through which the company not only manages and administers the rental spaces but also seeks strategies to expand its portfolio as well as the objectives of reusing spaces and optimizing the surfaces available for rent.

With that about the business model, I think that the most appealing thing about Urban Edge is the long list of projects that the company is currently undertaking. With an estimated cost of $196.5 million and target stabilization around 2023, 2024, and 2025, I believe that the incoming increase in capacity will most likely bring a significant amount of net sales growth coming from new rentals.

Source: Presentation To Investors

Expectations From Other Financial Analysts Include A Rebound In Net Income In 2024 And 2025 With Positive FCF Acceleration

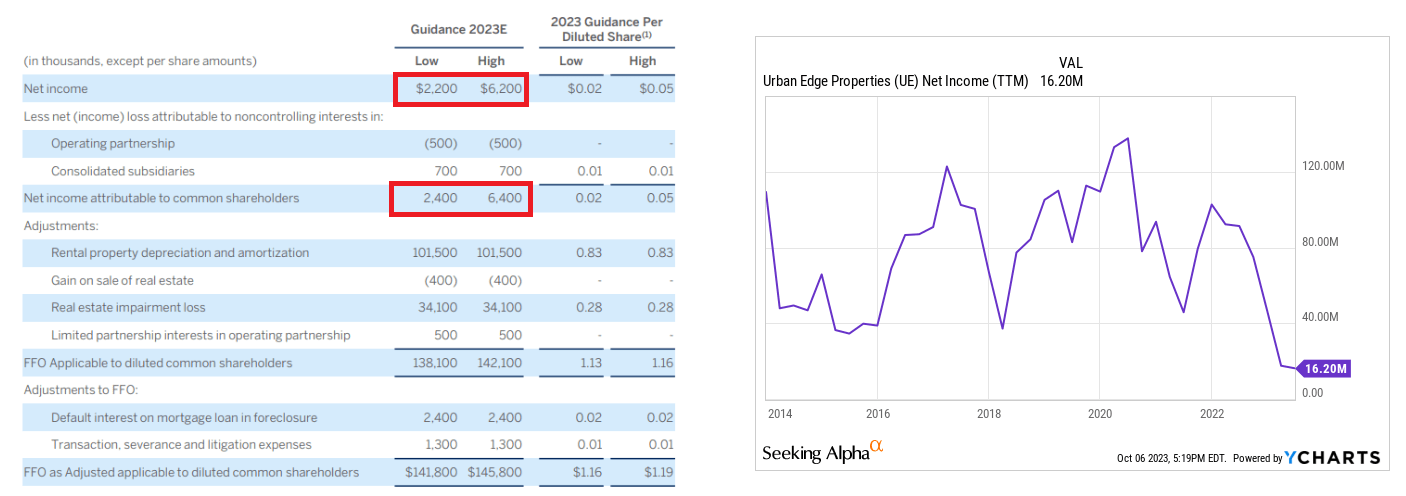

I really do not think that the 2023 net income guidance will impress most market participants out there. The company expects to deliver net income attributable to shareholders of close to $2.4-$6.4 million. It appears to be significantly lower than what the company reported in the past. With that, the good news is that most investment analysts are expecting a rebound in profitability from 2024.

{kind=link}

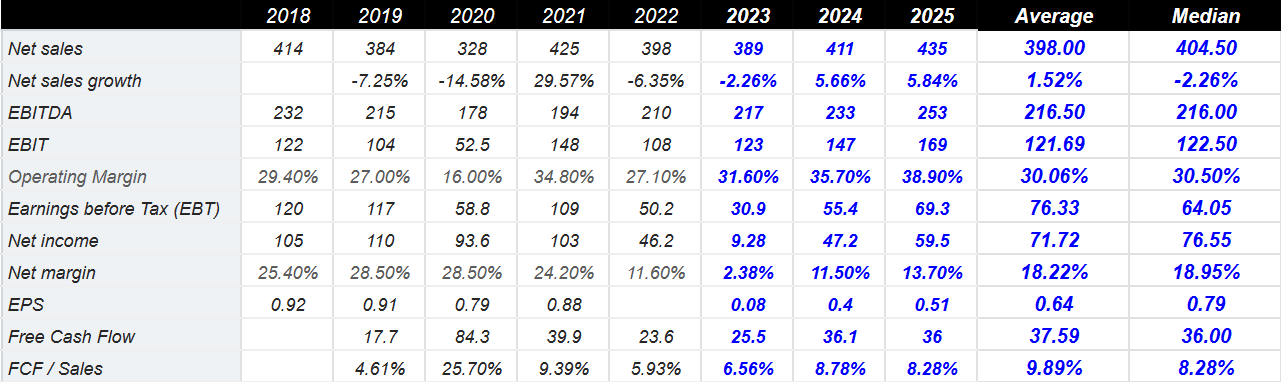

Urban Edge received beneficial expectations from other investment analysts. I did offer my own expectations, but I believe that investors may want to have a look at other opinions. Market expectations include positive net sales growth in 2024 and 2025, operating margin growth from 2023 to 2025, and FCF growth. More in particular, 2025 net sales are expected to be close to $435 million, with net sales growth of 5.83%, 2025 EBITDA of $253 million, and operating margin of 38.9%. Besides, with 2025 net income of close to $59.5 million, 2025 free cash flow would be close to $36 million.

{kind=link}

Assessment Of The Balance Sheet, And Contractual Obligations

Including land worth $543 million, buildings and improvements of close to $2500 million, and construction in progress worth $273 million, total real estate stood at $3.326 billion. Besides, with accumulated depreciation and amortization worth -$822 million, net real estate stands at about $2.504 billion.

The most relevant long-term assets are operating lease right-of-use assets worth $59 million, cash and cash equivalents close to $48 million, and restricted cash of about $44 million. Finally, total assets are equal to $2.903 billion, more than 1x the total amount of liabilities. The balance sheet appears solid, however, investors may want to have a close look at the total amount of debt.

Source: 10-Q

The list of liabilities includes mortgage payable close to $1.68 billion and total liabilities of $1.9 billion. Considering the total amount of debt, I studied carefully the obligations and interest rates being paid.

Source: 10-Q

According to documents offered by management, total long-term obligations stood at close to $2 billion when the last annual report was issued. I do not think the payment obligations are scary at all. In one to three years, the company may have to pay close to $356 million. Besides, the company pays a variable interest rate that ranged, last year, around 6% and 4%.

{kind=link}

Expanding Rental Spaces Within The Urban Areas Of Washington and Boston Will Most Likely Bring More Capacity And Net Sales Growth

I believe that further expansion of the offer of rental spaces within the urban areas of Washington and Boston will most likely bring further net sales growth. Of course, in this framework, the intention and search for acquisitions play a fundamental role since it is what allows this expansion to be carried out. I believe that Urban Edge has outstanding expertise in the M&A industry.

Within the current business, the company's efforts to optimize profit margins involve correct income management towards retail businesses as well as the permanent observation of the performance of these businesses and the physical improvements they can make. In this regard, it is worth noting that Urban Edge makes a great selection of brands to work for. Have a look at the following list, you may know some of these names.

Source: Investor Presentation

ESG Investing Will Most Likely Bring Demand From Investment Funds

I also believe that the recent efforts with regard to ESG investing, environmental, social, and governance plans will most likely bring the attention of new investors.

We consider asset sustainability and characteristics that are consistent with our environmental, social and governance plans and strategy for the future. Our due diligence process includes a full assessment of potential environmental risks associated with acquisitions. Source: 10-k

Source: Investor Presentation

According to experts from KPMG, ESG-focused products could experience an AUM growth rate of close to 27% in the coming years. Further efforts from Urban Edge with regard to ESG investing will most likely bring equity financing and demand for the stock.

Sustainable investing in its current form has recently experienced considerable market momentum, driving large inflows into ESG focused products, resulting in an average compounded annual growth rate of 27% in global assets under management over the last six years. Source: Evolution of ESG investing

With Adequate Pricing Strategies, Inflation Could Benefit The Business Model

During the year 2023, the inflation that affects the US economy does seem to affect the profitability of Urban Edge. With that, the company seems to be managing to increase rates and general maintenance costs. The company seems to be focused on optimizing the cost strategy to maintain the profit margins. Successful pricing strategies and negotiations with tenants will most likely protect the company from further inflation pressure. In this regard, Urban Edge provided the following commentary.

Most of our leases require tenants to pay their share of operating expenses, including common area maintenance, real estate taxes and insurance, although some larger tenants have capped the amount of these operating expenses they are responsible for under their lease. As a result, we believe that the structure of our leases reduces our exposure to increases in costs and operating expenses resulting from inflation. Source: 10-k

My FCF Expectations

In order to design future cash flow statements, I studied carefully previous cash flow statements and also took into account my assumptions with regard to capacity increases, inflation, and the expectations of other analysts. With regards to changes in accounts payables and changes in inventories, receivables, net income growth, or FCF growth, perhaps readers may want to have a look at previous figures before having a look at my forecasts.

Source: YCharts

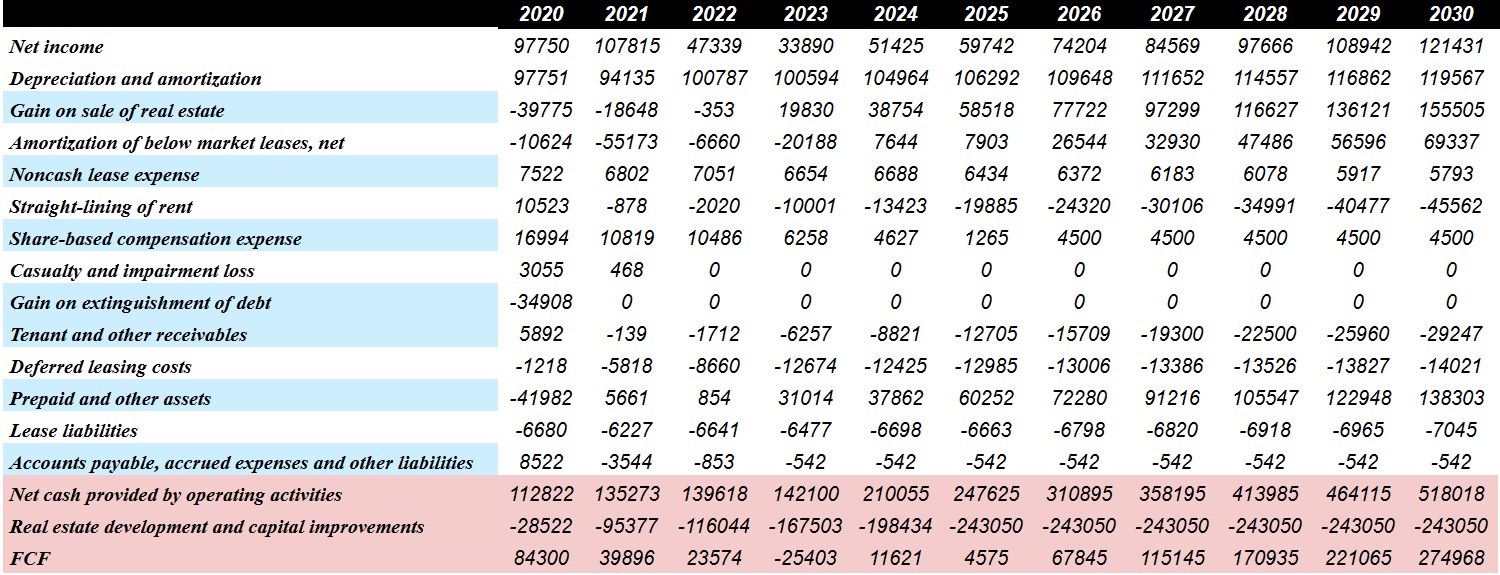

The most relevant numbers in my future cash flow statements include 2025 net income close to $121 million, with 2030 depreciation and amortization worth $119 million, gain on sale of real estate close to $155 million, and straight-lining of rent worth -$46 million.

Besides, I also included share-based compensation expense worth $4 million, tenant and other receivables worth -$30 million, and deferred leasing costs of about -$15 million. Additionally, if we also include prepaid and other assets worth $138 million, lease liabilities of -$8 million, and changes in accounts payable, accrued expenses, and other liabilities close to -$1 million, CFO would be about $518 million, with 2030 FCF of $274 million.

{kind=link}

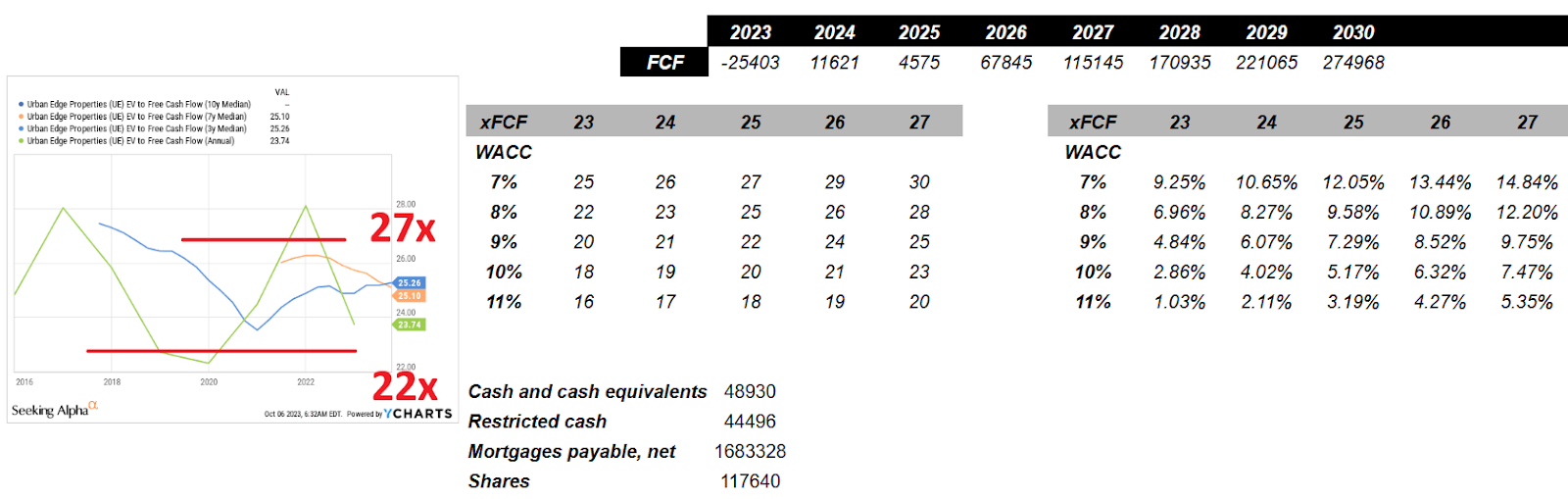

With a CAPM model that includes a WACC of around 7% and 11% and conservative EV/FCF of between 23x and 27x, my results included a forecast price of $16 to $30 per share and a maximum IRR of 14%. As shown in the table below, my figures show that Urban Edge appears undervalued at the current stock price.

{kind=link}

Competitors

Competition for the acquisition of large and considerably old properties in the urban areas of the Washington and Boston corridor is high, and due to the costs of these projects, there are high barriers to entry. Along with this and for these same reasons, they are considered high-risk investments with high margins of potential returns. In this market, there are also a large number of participants with businesses of different types such as the construction of residential homes or the rental of commercial buildings, given by both real estate firms with large portions of the market and independent construction companies.

Risks

We have seen that the nature of this company's business includes a large series of risks in relation to the high costs for project development, the need for large liquidity margins, and the concentration of participants within the geographical areas where it maintains its activities.

Furthermore, a significant part of the company's revenue in 2022 was concentrated on the margins of New York City, and the cycles of economic activity in this city directly affect the company.

Collectively, our New York metropolitan area properties in the aggregate generated approximately 73% of our annualized base rent as of December 31, 2022. Real estate markets are subject to economic downturns, and we cannot predict the economic conditions in the New York metropolitan area in either the short-term or long-term. Poor economic or market conditions in the New York metropolitan area may adversely affect our cash flow, financial condition and results of operations. Source: 10-k

The same in the sense of the economic context applies to the payment capacity of its tenants. The adaptation of its pricing strategy to the fixed rates of rental contracts is a key factor regarding Urban Edge's operations.

On the other hand, regarding the financial situation of this company, the company reports some debt obligations, and due to the nature of this business and the retail real estate market, the inability to pay in this sense can generate complications in access to capital lines to complete future acquisitions. As a result, we may see lower FCF growth in the coming years.

It is also worth noting that further growth of the e-commerce industry may affect the business model of some of the tenants that Urban Edge serves. Tenants may decide to lower the number of meters they need to sell, which may lower both net revenue and margins of Urban Edge. As a result, we may see a decline in the stock valuation of the company.

E-commerce continues to gain popularity and growth in internet sales is likely to continue in the future. E-commerce could result in a downturn in the business of some of our current tenants and could affect the way other current and future tenants lease space. For example, the migration towards e-commerce has led many omnichannel retailers to prune the number and size of their traditional “brick and mortar” locations to increasingly rely on e-commerce and alternative distribution channels. Source: 10-k

Conclusion

Urban Edge recently reported a redevelopment pipeline worth close to $196.5 million, which may offer capacity increases in 2023, 2024, and 2025. By working with well-known brands and planning to expand rental spaces within Washington and Boston, I believe that we can expect FCF growth in the coming years. Besides, I expect further visibility considering the ESG efforts announced and the growth of assets under management for this category of products. There are obvious risks from the total amount of debt obligations and the growth of the e-commerce industry, however, I believe that Urban Edge could trade at a better price mark.

For further details see:

Urban Edge: Large Tenants, Impressive Redevelopment Pipeline, And Cheap