UE - Urban Edge: Positive Catalysts Support Upside Potential Of Over 15% (Ratings Upgrade)

2023-06-05 06:31:08 ET

Summary

- Urban Edge Properties has a strong protective buffer against downside risks due to its exposure to grocers, top retailers, and resilient asset classes.

- The company expects significant growth in net operating income over the next three years, driven by lease commencements and contractual rent increases.

- I view shares as attractive at current pricing, with upside potential in the share price of over 15%, excluding dividends.

- Expected occupancy gains in the periods ahead, attractive opportunities from key tenant departures, and a healthy development pipeline are a few positive catalysts that can support this upside potential.

Urban Edge Properties ( UE ) owns a +$4.0B portfolio of retail real estate located primarily in the DC to Boston corridor of the U.S, with about 80% of the portfolio value located in the New York metro.

In addition, about 65% of their overall asset value is anchored by grocers generating nearly $900/square foot in sales, 10% by Home Depot ( HD ) or Lowe’s ( LOW ), and 7% by industrial and self-storage assets. The exposure here to grocers, top retailers, and resilient asset classes provides a strong protective buffer against downside risks.

The company is also expecting significant growth in net operating income (“NOI”) over the next three years, driven primarily by lease commencements and contractual rent increases.

Given recent strength, full-year guidance for funds from operations (“FFO”) was increased at the midpoint. And their three-year target sees FFO up 16% from 2023 levels.

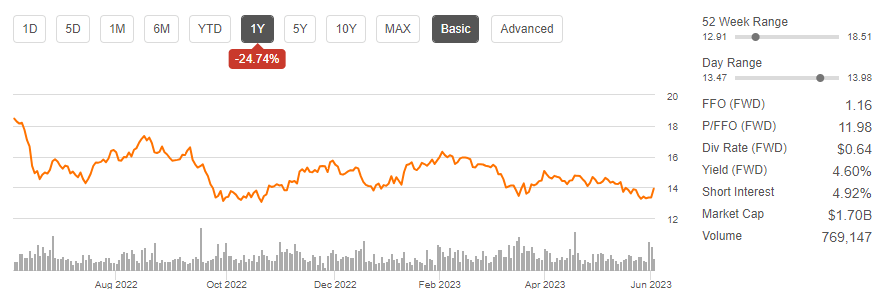

Over the past year, the stock is down nearly 25% and is down over 10% since my last update . Then, I had expressed reservations about an upcoming debt maturity. I also did not see enough catalyst for new or further initiation.

Seeking Alpha - Basic Trading Data Of UE

{kind=link}

Since that update, the company released a more detailed plan in their investor day presentation. And they also addressed the near-term maturity that I had been concerned about. Given the pullback and their recent performance, I’ve become more bullish. At current pricing, I can see shares trading fairly at about 12x their 2025 estimate for FFO. This would represent upside potential of over 15% from current trading levels.

Healthy Spreads On Robust Leasing Volume

In the first quarter, UE leased a total of 430K SF, 412K SF of which was attributable to their same-property population. On an overall blended basis, the company realized a 7.5% cash spread on these signings. This compares favorably to the 5.1% blended spreads realized in the same period last year.

Broken out between new and renewal signings, the company signed 111K SF of new signings at cash spreads of 17.6% and 319K SF of renewals at 5% spreads. Compared to last year, uplifts on new signings were down slightly from the 19.7% increase realized last year. But this was offset by strength in renewals, which was up on a YOY basis.

Upside Potential Through Expected Occupancy Gains

At the end of the quarter, same property leased rates stood at 95.3%. As expected, this is down slightly quarter over quarter. But it’s up several turns on a YOY basis. Likewise, consolidated leased occupancy, excluding Sunrise Mall, which is currently undergoing repositioning plans , is up to 94.6%.

Looking ahead, management expects total portfolio leased rates to settle between 97% and 98%. This would be up significantly from the current rate of 94.6%. In addition, shop rates, which were up 50 basis points (“bps”) during the quarter to 85%, is ultimately expected to reach 90% by the end of this year.

The increase in their shop rates, along with an expected improvement in their anchor figures is expected to take their same property rates up to 96%.

Attractive Opportunity Upon Departure Of Bed Bath & Beyond ( BBBYQ )

UE currently has exposure to six stores occupied by Bed Bath & Beyond. As a percentage of total annualized base rents (“ABR”), this represents just 0.8% exposure.

It should also be mentioned that they began the year with seven stores, but one lease expired in January of 2023. For this lease, there are currently several prospects that are likely to take over the space at spreads well above the investments that went into the properties.

For their remaining locations, the makeup consists of two Bed Baths, one BuyBuy Baby, and three Harmon Face Values stores. The Harmon locations represent just a small portion of the space, and all three are expected to be re-leased.

For the Bed Baths and the BuyBuy Baby, rents were current through April and May. And through their earnings release, the leases have not been rejected. According to management, if they are able to recapture the spaces, they believe they can realize significant spreads of between 20% and 70% on existing rents. This would be well above what they are getting portfolio-wide.

Clear Visibility Into Future NOI Growth

UE has a significant pipeline of pending commencements. Furthermore, this pipeline through Q1FY23 has grown for four consecutive quarters, increasing to over +$30M in the first quarter.

April 2023 Investor Day Presentation - Signed But Not Commenced Pipeline Of UE Compared To Peer Set

In addition to pending commencements, the company has about 600K SF of leases under negotiation equating to approximately 6% of NOI.

Together with contractual rent increases, the pipeline is expected to contribute to 80% of the expected 20% NOI growth over the next three years.

Furthermore, the company has a healthy repositioning and redevelopment program totaling approximately +$218M in active projects. Ultimately, these projects are expected to turn in a 12% return. In terms of leasing, 95% of the total project gross leasable area (“GLA”) had been pre-leased through the date of their earnings release.

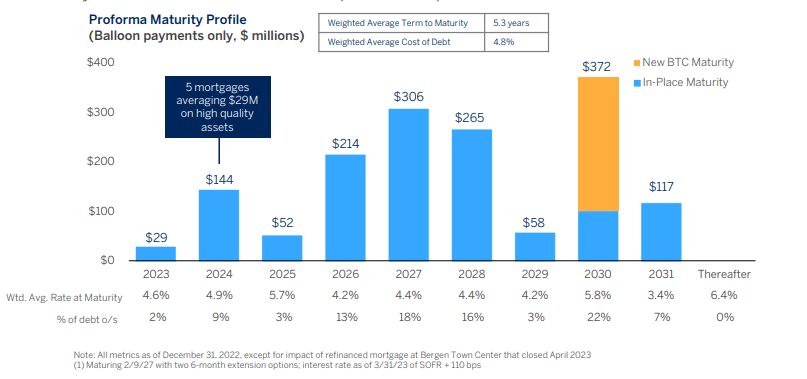

De-Risked Maturity Profile

In my prior update on the stock, I noted the uncertainty surrounding negotiations on their nearest debt maturity at Bergen Town Center. This concern, however, was ultimately addressed subsequent to quarter end.

On the release, they noted that the loan was successfully refinanced into a seven-year, fixed rate loan bearing interest at 6.3%. With the refinancing, less than 15% of their total debt stack will be due through the end of 2025.

April 2023 Investor Day Presentation - Debt Maturity Schedule

{kind=link}

And on an overall basis, their total leverage ratio is expected to decline to the 6.5x range, as measured as a multiple of net debt to forward EBITDA, upon commencement of their pending leases. In the interim, the company has significant liquidity of over +$900M. This includes a cash on hand balance of +$129M.

A high percentage of fixed rate holdings, limited near-term maturities, and ample liquidity provide confidence that the company can continue meeting all their reoccurring operating commitments.

Why UE Stock Is A Buy

There are many catalysts for UE in the periods to come. For one, occupancy levels are expected to track back up to historical highs from present levels, beginning with an expected 500bps improvement in their shop rates by year end.

The recapture of Bed Bath’s space also provides an attractive mark-up opportunity. Though UE will face headwinds on lost rent upon their immediate departure, this was already built into forward guidance. And even with the build in, full-year guidance is still up a few cents at the midpoint from their prior outlook. Additionally, once the space is re-leased, I expect UE to recover all their losses from the lost rent via the new rent premiums.

A sizeable pipeline of pending commencements, which is the largest among their peer set, provides further visibility into future NOI growth. In fact, these commencements along with contractual rent bumps are expected to contribute primarily to the 20% expected growth in NOI over the next three years.

The growth would be in combination with a healthy development pipeline that is mostly pre-leased. An improvement in their debt profile via the refinancing of their most immediate debt maturity adds a layer of additional confidence that the company can meet their remaining commitments for their pipeline. This is further supported by their significant liquidity position of over +$900M, including a cash balance of about +$130M.

Altogether, these opportunities are expected to translate into a three-year target of $1.35/share in FFO. On a forward basis, then, shares are currently trading at about 10.3x. In my view, this appears discounted. I, instead, can see shares fairly valued at about a 12x multiple. This would indicate upside potential in the share price of over 15%, excluding dividends. For investors seeking new or further positioning, I view this potential as attractive in the current market environment.

For further details see:

Urban Edge: Positive Catalysts Support Upside Potential Of Over 15% (Ratings Upgrade)