BKE - Urban Outfitters Still Looks Undervalued

Summary

- Sales at Urban Outfitters continue to come in strong, even in spite of specific challenges the company has faced.

- Profits and cash flows have been weak, but the issues here are likely transitory in nature.

- Even with the pain, shares look cheap on an absolute basis and likely deserve a bit more upside from here.

One beautiful thing about value investing is that, even when a company is experiencing a deterioration in bottom line results, you might still experience a nice increase in share price. This happens when the shares of the company that you acquire are cheap even after factoring in the pain that the market anticipates. One really good example that I could point to for this taking place is Urban Outfitters ( URBN ) an enterprise that produces and sells lifestyle products under a variety of brand names such as Anthropologie, Free People, Nuuly, and more. Recently, sales figures reported by management have been encouraging. But bottom line results have come under pressure. Even so, shares of the company look cheap on an absolute basis while looking more or less fairly valued compared to similar firms. At this point, I do think the easy money has been made. But given how cheap the stock remains, I would say that some additional upside might still exist for shareholders moving forward. Because of this, I have decided to keep the company as a soft ‘buy’ for now, reflecting my belief that the stock should marginally outperform the broader market moving forward.

A comfortable play so far

Back in early May of 2022, I wrote an article discussing whether or not it made sense for investors to consider Urban Outfitters as a valid opportunity. In the prior years, the company had performed quite well and I suspected that its performance would continue to be impressive moving forward. Despite that strong performance, shares of the enterprise were trading on the cheap, though they were more or less fairly valued compared to similar firms. All things considered, I felt as though the company offered nice upside potential for investors for the foreseeable future. That ultimately led me to rate it a ‘buy’. Since then, the business has delivered. While the S&P 500 is down 1.3%, shares of Urban Outfitters have seen upside of 15.1%.

{kind=link}

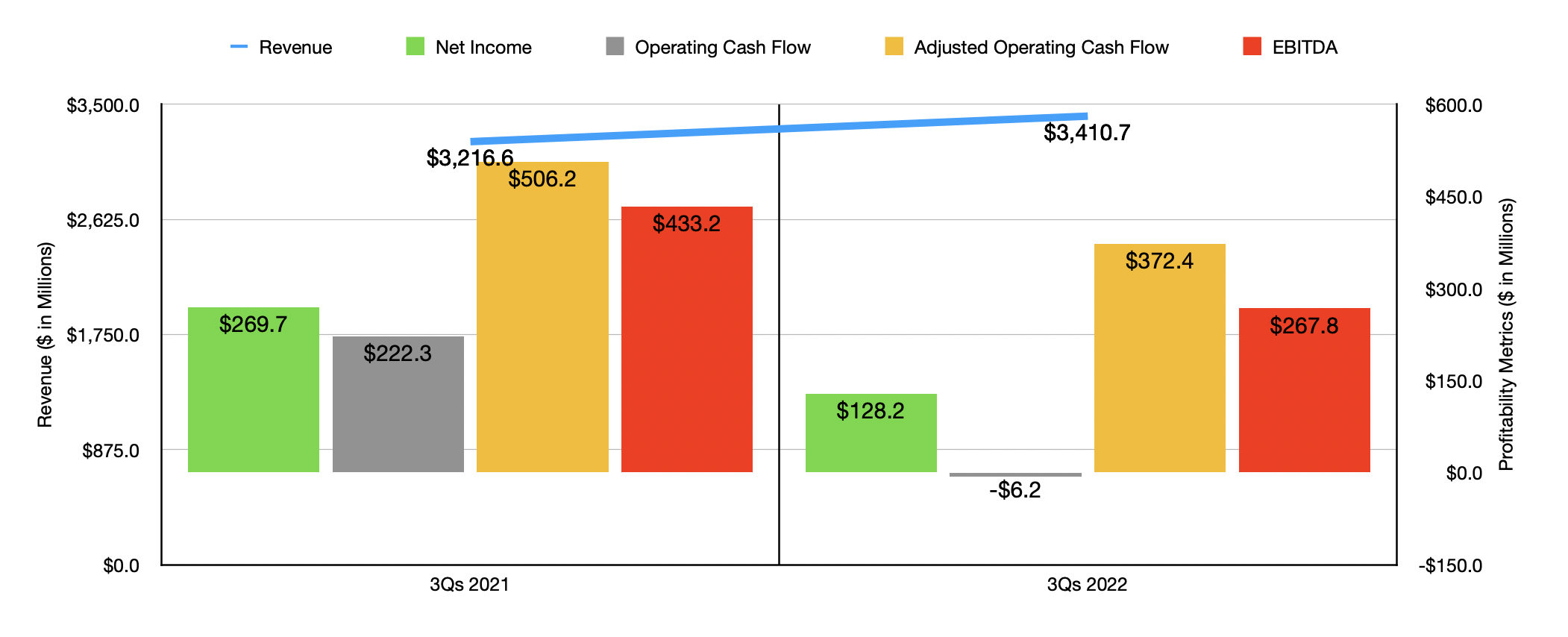

Given this return disparity, you might think that everything for the company was going great. But that's not exactly the case. On the positive side, we do have continued revenue growth. For the first nine months of 2022 , for instance, the company generated sales of $3.41 billion. That's 6% higher than the $3.22 billion generated one year earlier. Part of that increase has undoubtedly been attributable to continued growth in store count. At the end of the company's 2021 fiscal year, for instance, it had 685 stores under its Retail segment. By the end of the third quarter of 2022, this number had grown to 707. Overall, this helped to pave the way for a $135.7 million increase in sales for the aforementioned segment year over year. But the real driver involved the company's Nuuly segment, with revenue shooting up $56.5 million, or 185.4%. This particular unit consists of Nuuly Rent, a monthly women's apparel subscription rental service that allows subscribers to select rental product from a wide selection of the company's own brands, as well as third-party brands and other content that is then shipped to their home and worn as often as they like. It also includes Nuuly Thrift, which operates as a peer-to-peer resale marketplace work customers can buy and sell various apparel, shoes, and accessories. Most of the increase here was associated with a rise in subscriber count totaling 185%.

{kind=link}

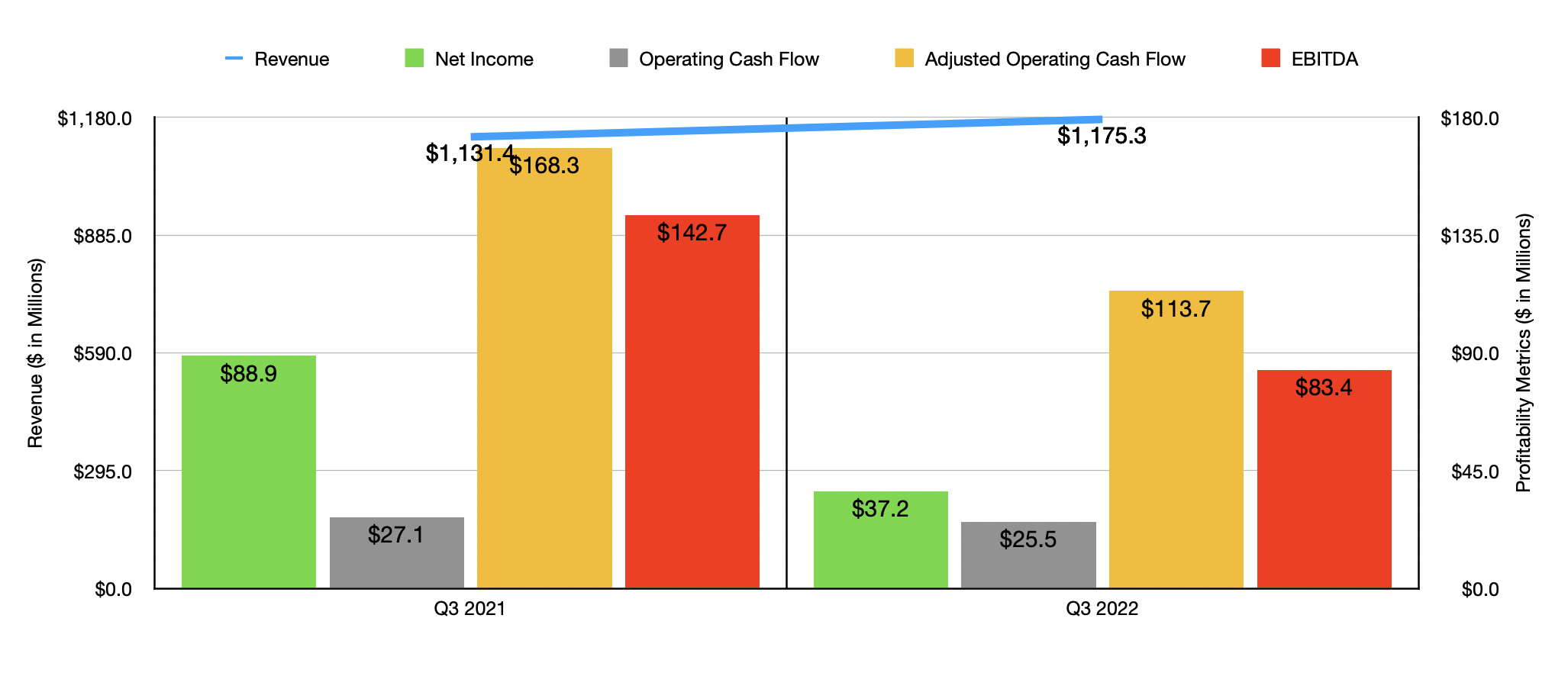

On the bottom line, the company was not so lucky. Even though revenue increased, net income plunged from $269.7 million in the first nine months of 2021 to $128.2 million the same time of the 2022 fiscal year. Higher markdowns at all three of the company's brands, as well as lower initial merchandise markups resulting from higher inbound transportation costs, played a big role in hitting the company's bottom line. The company also reported an increase in its selling, general, and administrative costs in relation to sales, with the metric climbing from 24% of revenue to 25.3%. This was related to higher store payroll expenses aimed at supporting retail store sales growth, as well as to increased store associate hours to support increased customer traffic. Higher average wages also played a role here, as did a rise in marketing expenses to support sales and customer growth. This change alone impacted the company's pretax profits to the tune of $44.3 million. Unfortunately, other profitability metrics followed a similar trajectory. Operating cash flow went from $222.3 million to negative $6.2 million. If we adjust for changes in working capital, it still would have fallen, dropping from $506.2 million to $372.4 million. Meanwhile, EBITDA for the company declined from $433.2 million to $267.8 million. As you can see in the chart above, the third quarter of 2022 in relation to the same time one year earlier was not really any different than what the company experienced in the first nine months of the year as a whole.

We don't really know what to expect when it comes to the final quarter of 2022. Having said that, management did say that in the two months ending December 31st, sales increased by 2.3% year over year. This came even as wholesale revenues dropped 22% and as the Urban Outfitters brand reported a 10% sales contraction. Other brands pushed sales higher, such as Free People Group, which reported a comparable increase of 15%. The Anthropology Group reported a comparable sales increase of 7%. Meanwhile, Nuuly saw sales jump 150% year over year, driven by a 153% rise in the number of subscribers to the platform.

{kind=link}

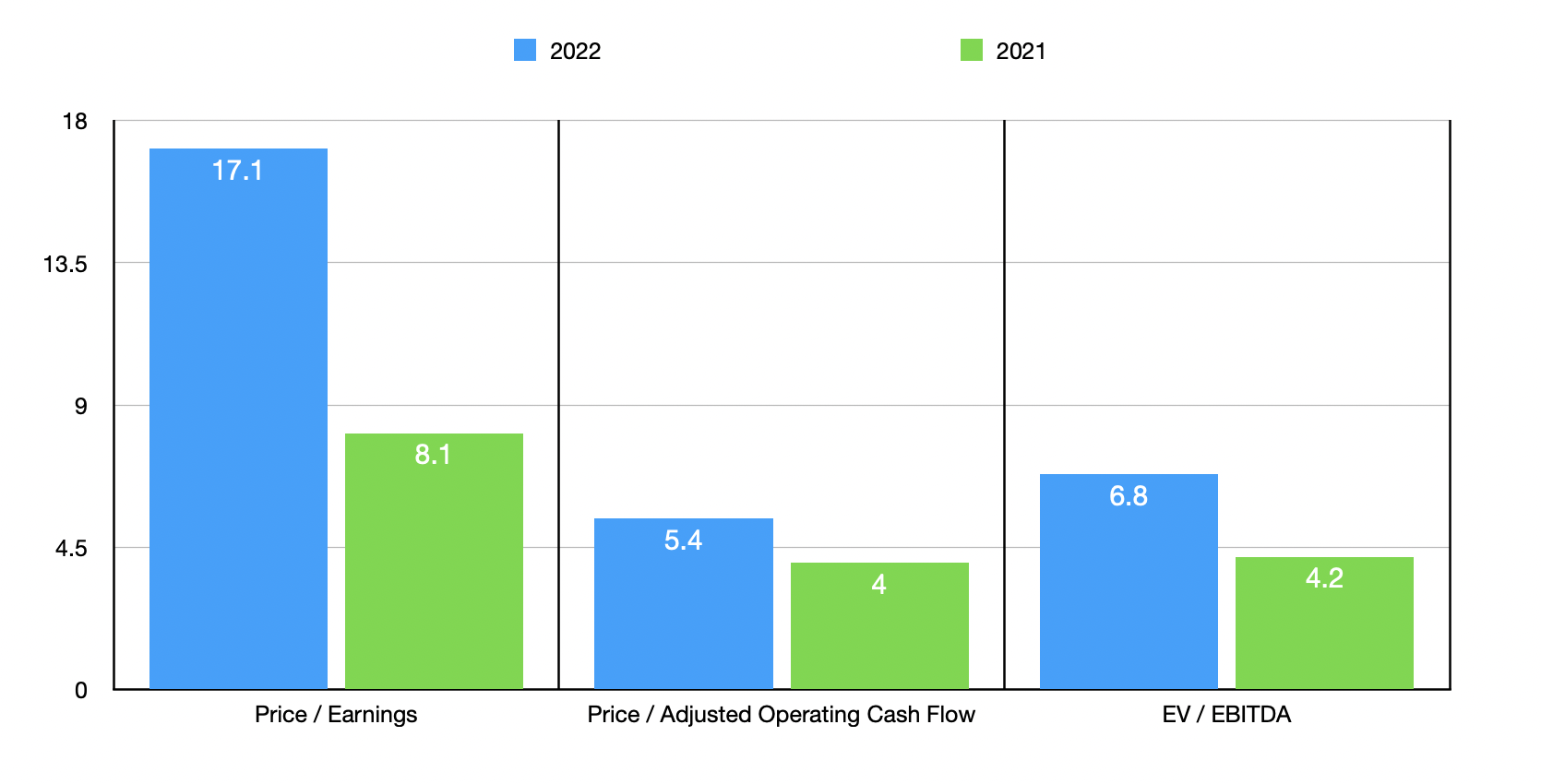

When it comes to profitability, the best thing we can do is to annualize results experienced so far for 2022. Doing this, we would get net income of $147.6 million, adjusted operating cash flow of $465.2 million, and EBITDA of $313.8 million. Based on these numbers, the company is trading at a price-to-earnings multiple of 17.1, a price to adjusted operating cash flow multiple of 5.4, and an EV to EBITDA multiple of 6.8. These numbers are higher, as you can see in the chart above, than what we would get if we used data from 2021. But on an absolute basis, they are still quite low. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 8.7 to a high of 67.4. Using the EV to EBITDA approach, the range was from 5.1 to 9.5. In both of these cases, three of the five companies were cheaper than our prospect. Meanwhile, using the price to operating cash flow approach, the range was from 9.7 to 108.2. In this scenario, all four companies with positive results were more expensive than Urban Outfitters.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Urban Outfitters |

| 17.1 |

| 5.4 |

| 6.8 |

| Boot Barn Holdings ( BOOT ) |

| 15.0 |

| 108.2 |

| 9.5 |

| Buckle ( BKE ) |

| 8.7 |

| 9.7 |

| 5.3 |

| American Eagle Outfitters ( AEO ) |

| 27.4 |

| 38.8 |

| 7.1 |

| Victoria's Secret ( VSCO ) |

| 8.9 |

| 18.7 |

| 5.1 |

| Abercrombie & Fitch ( ANF ) |

| 67.4 |

| N/A |

| 5.8 |

Takeaway

From the data that's available today, it seems to me as though Urban Outfitters is facing some cost pressures. This is problematic in the long haul and needs to be resolved at some point. Having said that, shares of the company still look quite cheap on an absolute basis, even though they might be fairly valued compared to similar firms. It is great to see revenue continue to rise and to see the company benefit from tremendous growth from its Nuuly brand. So long as these trends continue, I would make the case that shares likely have some upside moving forward. As such, I've decided to keep the ‘buy’ rating on the company for now.

For further details see:

Urban Outfitters Still Looks Undervalued