URNM - URNM: Uranium Miner Bull Market Peaking As Valuations Stretch

2023-12-17 23:11:19 ET

Summary

- Uranium has been the best-performing energy commodity in 2023, with a rise in value and mining stocks increasing by around 50%.

- The uranium market has unique economics, with inelastic demand and the potential for a long-term shortage as secondary supplies run dry.

- While uranium fundamentals are solid, many uranium mining stocks are overvalued, and production levels may rise to meet demand in the case of a shortage.

- I believe the Canadian-listed Uranium Physical Trust is likely superior to URNM today.

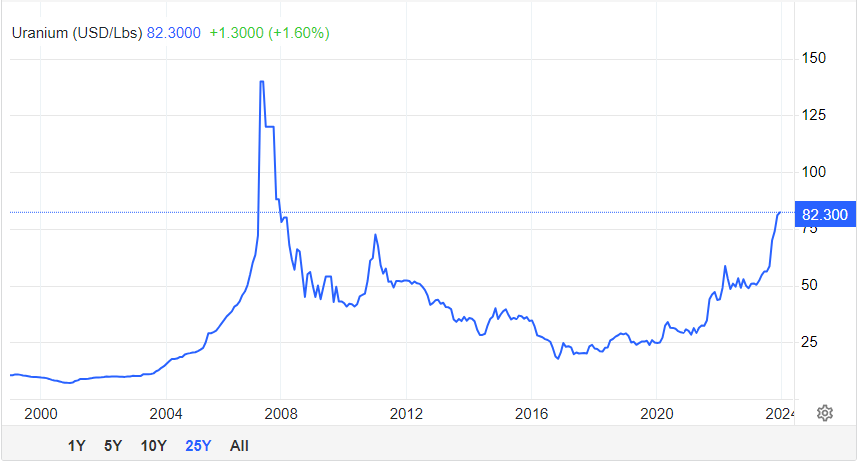

While 2023 has been a lackluster year for energy commodities, not all fuel sources have lost value. Uranium has risen by a staggering 69% YoY , making it the best-performing energy commodity and one of the few to gain value YoY. If not for orange juice and cocoa, uranium would be the best-performing commodity of all since last December. Uranium mining stocks, such as those in the popular ETF ( URNM ), have risen by around 50% this year, causing many investors to hope for a repeat of the 2007 uranium price explosion.

I was an early bull on the uranium trade, being very bullish on URNM in December 2019 . The ETF has risen by roughly 164% since then, with a total return of ~190%. Cameco ( CCJ ) has been one of my favorite uranium companies because, unlike most, it is generally profitable and is a significant market player. Its equity price has risen by around 375% since I last covered it in 2020, assuming its production issues would trigger a broader bull market.

I've watched the uranium market rise tremendously through this bull market over the past four years. Today, the economics of uranium are shifting, and production and demand levels continue to change. For the most part, most energy commodities are seeing renewed output levels today that are in line with or above pre-COVID levels. Uranium production is the exception to that trend, having declined over recent years. Many uranium mining stocks are also highly valued today, potentially making them riskier investments, particularly compared to their 2019-2020 positions. Given this, I believe it is an excellent time to take a close look at uranium and the miners in URNM to determine whether or not the bull market is likely to extend into 2024 or may reverse soon.

The Nuclear (Mining) Winter Has Begun

The uranium market has fundamentally different economics than most other energy commodities. For one, the uranium demand curve is inelastic, likely the most inelastic demand curve of all markets. The reason is that raw uranium is absurdly cheap per KWH of potential power, having around 10 GWH of potential power per pound of raw material. Of course, nuclear power plants' enrichment costs and operating expenses are incredibly high, partially exposing uranium demand to increasing service wage costs and capital goods prices. However, that is a very long-term issue as increasing utility investment costs for nuclear plants impacts development planning over one decade out.

Once a nuclear plant is created, it will need a constant supply of uranium indefinitely, and higher raw material prices have no material impact on demand, given raw material prices are many magnitudes below other costs. Accordingly, in the event of a uranium shortage, there is virtually no ceiling on how high uranium could rise. Nuclear plants cannot buy less of it, and even if raw materials prices increased by 10X, it would not materially impact the utility buyer because raw material prices are so low per KWH.

On the other hand, uranium likely has a very elastic supply curve . Uranium is extremely abundant and relatively inexpensive to mine, although it has high environmental concerns. Most uranium today comes from Kazakhstan , accounting for just over half of total production globally. Other countries, such as Canada, Australia, Russia, and various African and Central Asian countries, also produce uranium. Niger is one more giant producer that may be having issues today following its recent coup, partially explaining the ongoing uranium bull market.

Theoretically, uranium is headed into a long-term shortage as secondary supplies (such as old weapons) run dry and existing mines mine their existing resources. Further, uranium demand is expected to rise by around 15% by 2035 as new Chinese plants are opened. However, other estimates project a 28% demand increase by 2030, given many European countries have decided to extend the life of existing plants, many of which are toward the end of their initial life expectancy. Fundamentally, Europe is struggling to decide between shutting down (or extending) its older nuclear plants and achieving its emission reduction goals, making the outlook for nuclear demand vague.

Still, it should be noted that, despite popular views, nuclear is one of the most expensive power sources per KWH due to high capital investment and labor overhead costs, both of which are rising with inflation, resulting in cost overruns and delays in developing projects. Investors should understand that fact as it may upset the long-term feasibility of nuclear over cheaper sources like wind and natural gas. To me, it is generally unlikely that fission nuclear fuel will be the primary long-term power source; however, it will likely remain a significant secondary source indefinitely.

Even then, in the case of a shortage, which appears likely amid rising demand and falling supply, raw uranium prices may still temporarily rise considerably. Total uranium production has declined by around 17% over the past decade, with production accounting for just 74% of demand in 2022 . The remainder usually comes from secondary sources, primarily decommissioned nuclear warheads. One new issue now is that Russia, and potentially the US, are likely not decommissioning warheads, at least at the same rate. Both countries are no longer offering data on decommissioning programs , with both possibly restarting nuclear test programs. At the same time, most global uranium miners struggle to bring production back to pre-COVID levels. They may not do so for years as Cameco and others race to buy uranium on the market to meet their contract obligations.

What are Uranium Miners Worth Today?

After tremendous growth this year, the uranium price rally shows no signs of slowing. See below:

{kind=link}

Uranium is extremely expensive today compared to its pre-COVID price but is not yet at the same price it was in 2007. The 2007 rally is similar to today, triggered by speculation surrounding demand growth, reductions in weapons-grade uranium, and popular views regarding a nuclear power renaissance. Further, the major Cameco Cigar Lake mine flooded , causing a substantial temporary supply cut that created a shortage. Still, the rally turned out to be a bubble as nuclear project planning crashed in 2008 and halted after the 2011 Fukushima disaster. Today, I believe the uranium rally is better protected by improved fundamentals, primarily the inability of significant miners to increase production to meet demand. Secondarily, because most uranium is mined in central Asia and Africa, there is great geopolitical risk in uranium supply chains amid the rising number of conflicts (and rumors of such ).

Still, uranium miners are very expensive today despite the rising uranium price. One of the few profitable uranium miners, Cameco, trades at a forward "P/E" of about 70X today. URNM's overall weighted average "P/E" is around 38X today. Almost all of the ETF's earnings come from Kazatomprom, which trades at a "P/E" of around 11.7X today . For the most part, most North American uranium miners are not profitable today and are not expected to be over the next year despite higher prices ( 1 , 2 , 3 ). I believe uranium mining is too expensive outside of developing countries due to environmental regulatory needs and higher labor and capital costs. Of course, if we see uranium prices over $100 to $200, then that will undoubtedly change; however, production levels will likely rise proportionally, although over a matter of years.

The Bottom Line

Overall, I believe the fundamentals of uranium itself are solid today. The combination of falling supply, rising demand, and high geopolitical risks regarding the supply chain all point toward a potentially much higher uranium price. However, most of the uranium mining stocks in URNM appear overvalued today. The breakeven is about $90/lbs in developed countries, but that figure is rising with inflation and interest rates. Further, once uranium becomes the US, many mines are waiting on standby to increase supply as needed. Thus, while we could see uranium rise into the $100-$300/lbs range for months, I expect production would ramp up to meet demand in the case of a shortage, and many are already restarting today.

I believe uranium is the best investment as a speculative trade today. One potential way to do this is by buying the Sprott Physical Uranium Trust ( U.UN:CA ), which trades on the Canadian market and is ~15% of URNM's holdings. Another decent uranium investment is certainly Kazatomprom due to its vast size and low valuation, but that requires exchanges where KAP securities are listed, such as its London exchange GDR . Likely, Kazatomprom's low valuation stems from its lack of international investment exposure.

Besides those two, and possibly Cameco, I am not too fond of the junior uranium miners because I believe their valuations are too extended compared to their potential long-term profitability. Fundamentally, I do not think uranium demand is strong enough, nor the supply low enough, to make the US a major long-term uranium exporter, as many currently hope. Accordingly, I am neutral on URNM and believe it is generally a good time to take profits today. Once uranium hits breakeven levels, junior miner investors may be upset by the low earnings yields likely seen by those firms.

For further details see:

URNM: Uranium Miner Bull Market Peaking As Valuations Stretch