REG - Urstadt Biddle Properties Being Acquired By Regency Centers: Sell Or Stay?

2023-05-19 08:00:00 ET

Summary

- I cover some of the details of the stock-for-stock acquisition of Urstadt Biddle Properties by Regency Centers.

- The combined REIT will continue to be a blue-chip retail real estate operator with high-quality assets and a strong balance sheet.

- I discuss reasons to sell and reasons to stay in UBA and become a REG shareholder when the deal closes.

- Lastly, I give my own plan of action.

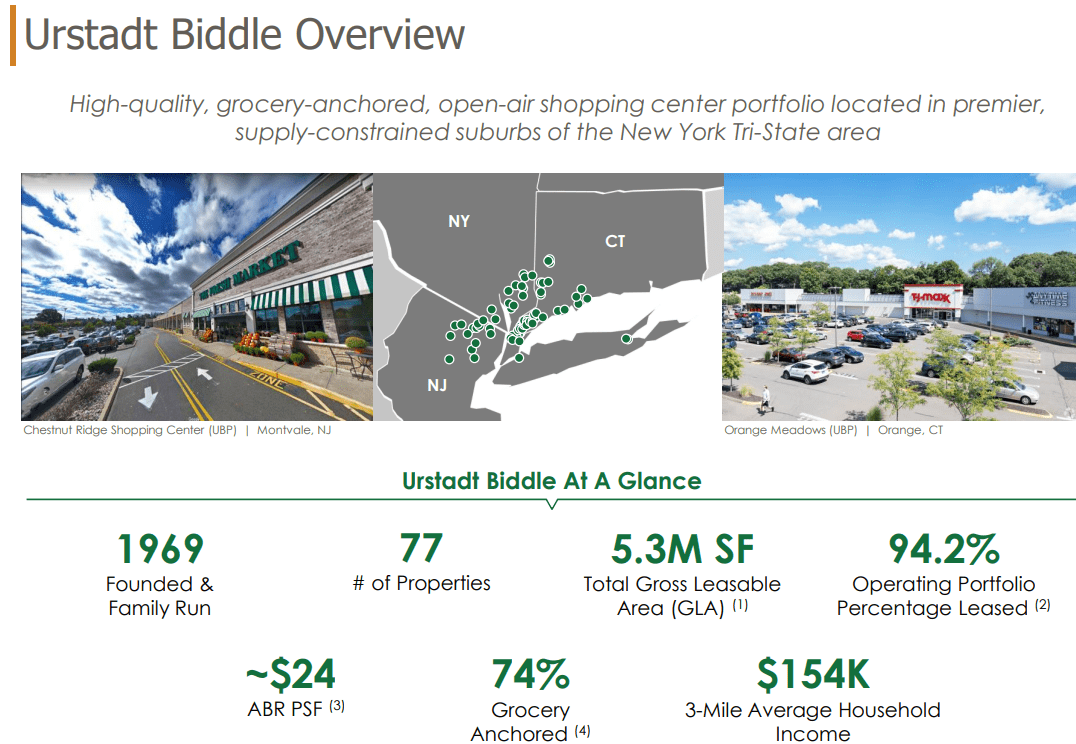

Urstadt Biddle Properties ( UBA , UBP ) is being acquired by its larger peer, Regency Centers ( REG ) .

Both are real estate investment trusts ("REITs") primarily focused on grocery-anchored retail shopping centers. While REG has a nationwide footprint, UBA is concentrated entirely in the New York tri-state area in suburbs around New York City.

{kind=link}

As Lisa Palmer, President & CEO of REG, said in the deal announcement press release :

Both companies have a successful track record of owning and operating best-in-class grocery-anchored neighborhood and community centers in premier suburban trade areas, and we look forward to the synergies and growth opportunities that this transaction will offer to the combined shareholder base.

The acquisition is a 100% stock-for-stock transaction. Both classes of Urstadt Biddle common stock, UBA and UBP, will be exchanged for 0.347 shares of REG upon deal closing. Given REG's current (as of this writing) share price of $58.56, this values UBA and UBP at $20.32 per share, a ~20% premium above the previous day's closing price for UBA and a 32.5% premium above the previous day's closing price for UBP.

This values the whole Urstadt Biddle business at about $800 million in equity value and $1.4 billion in enterprise value.

Upon completion of the deal, REG shareholders will own 93% of the combined business, while UBA/UBP shareholders will own 7%.

The deal is expected to close in late Q3 or early Q4 2023, which would put the closing date in the September-October timeframe.

At the acquisition price, UBA trades at a 4.9% dividend yield, while REG trades at a 4.4% dividend yield. Since its a stock-for-stock deal, those yields can shift, but that spread will likely be maintained.

In what follows, we'll take a brief look at the transaction and what the combined REIT will look like, then move to a discussion of whether UBA shareholders should sell or hold and become REG shareholders when the deal closes. I'll finish with my plan of action.

The Deal

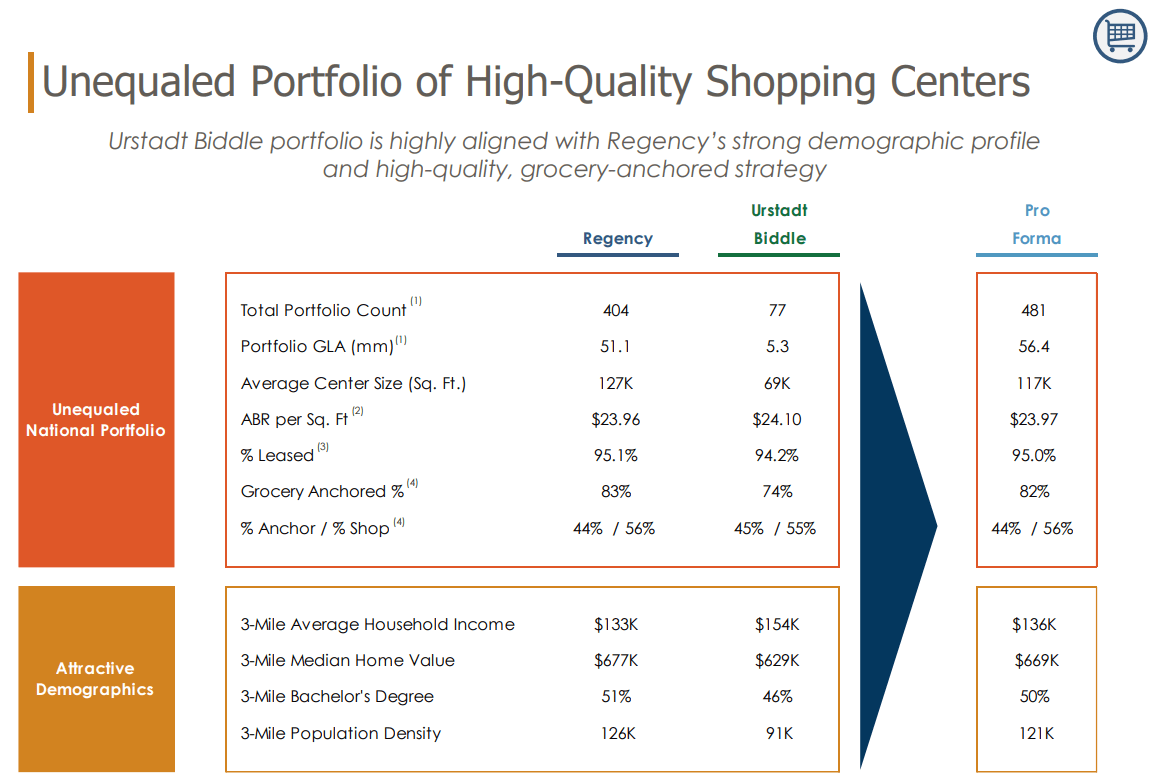

When the metrics for each REIT are laid out and compared side to side, it's easy to see why these REITs' management teams saw a combination as being sensible and worthwhile.

While UBA's average property size (69K square feet) is smaller than REG's (127K SF), they both focus on the same basic types of centers and tenants.

{kind=link}

While REG has a little more grocery-anchored NOI than UBA, they are both among the highest in their retail REIT peer group. Adding UBA's 74% of NOI from grocery-anchored centers to REG's 83% only causes the combined REIT's grocery-anchored NOI share to drop to 82%.

What's more, each REIT boasts a strong demographic profile, with high average household income, education level, and population density in the immediate trade area.

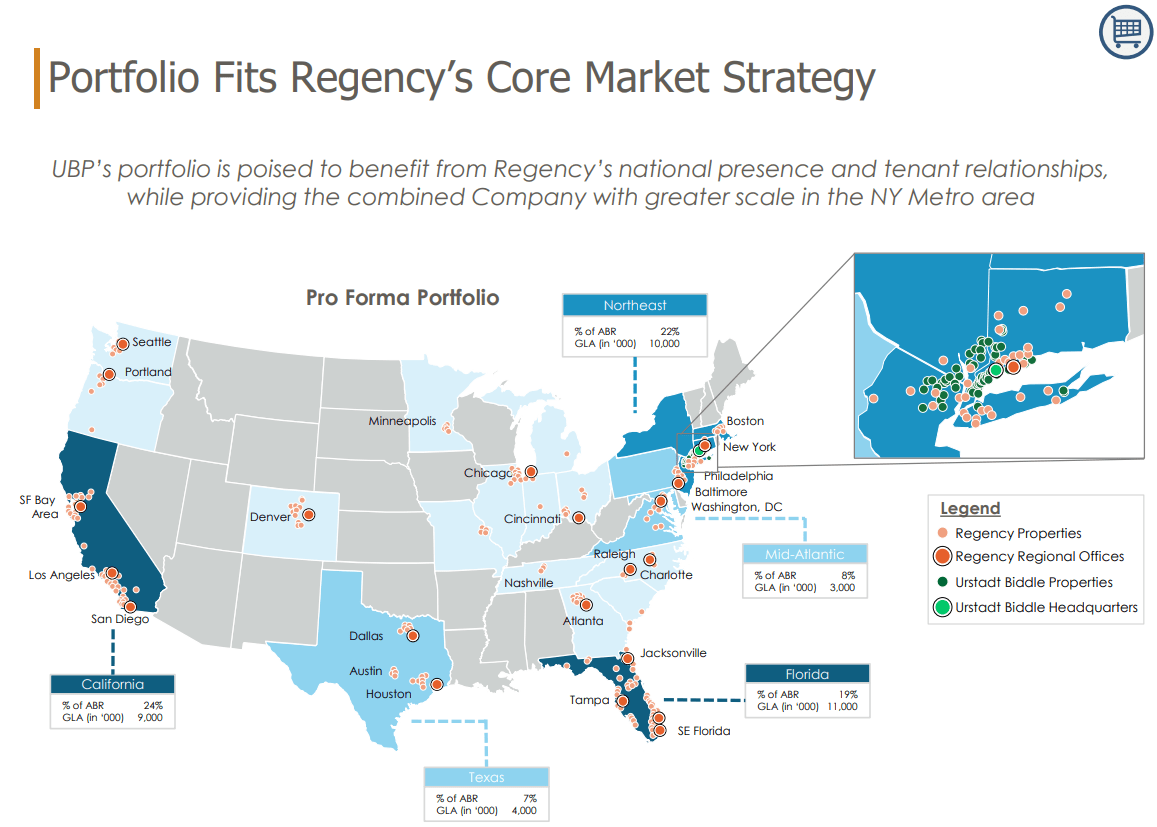

Turning to the combined REIT's geographic footprint, we find UBA's tri-state area portfolio to be a nice bolt-on acquisition for REG's existing footprint in the Northeast.

{kind=link}

REG has a heavy presence in all four corners of the US, as well as significant and growing exposure to fast-growing areas in Texas, Colorado, and the Carolinas. Of course, even in the more "challenged" areas that are suffering population declines like San Francisco and Chicago, REG's centers are still located in the best and most desirable areas that are unlikely to see material declines in tenant demand.

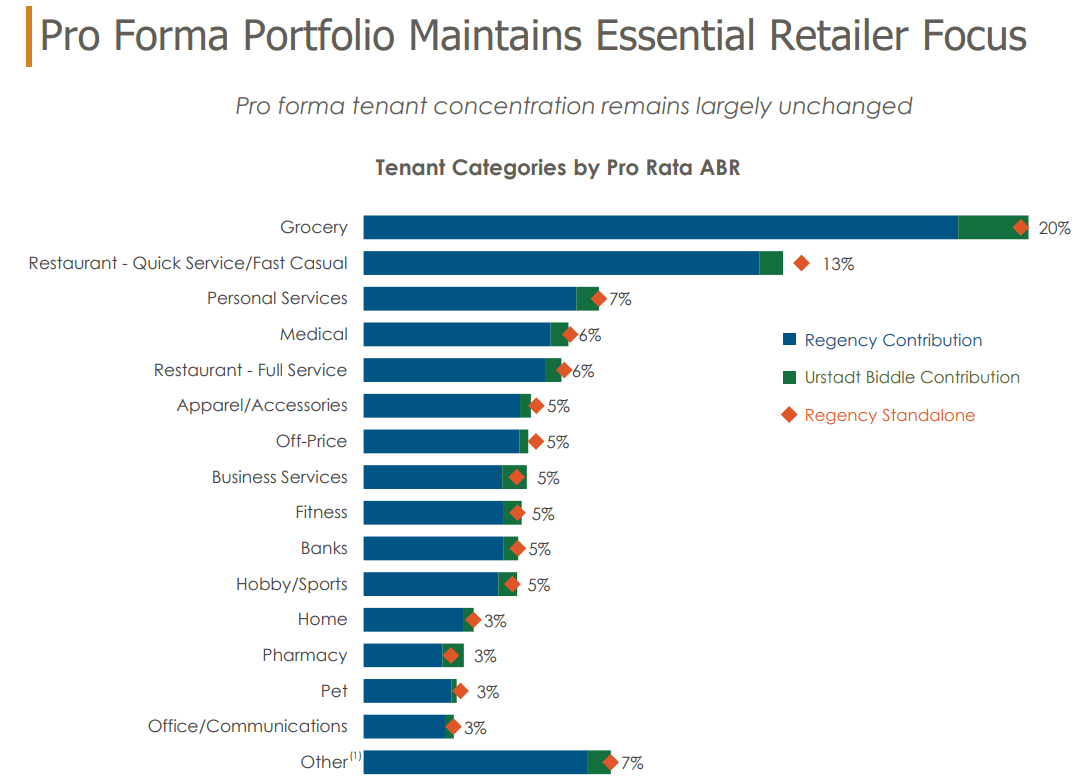

Speaking of tenants, the combination with UBA maintains REG's heavy focus on essential retailers, especially grocers that make up 20% of rent and QSRs/fast casual restaurants that account for another 13% of rent.

{kind=link}

Unsurprisingly, 6 of the combined REIT's top 10 tenants will be grocers, led by Albertsons ( ACI ).

{kind=link}

If the pending merger deal with The Kroger ( KR ) ends up closing, then the combined REIT's top tenant will account for 5.8% of rent and enjoy an investment grade credit rating. As it stands, Albertson's/Safeway is the combined REIT's only non-IG (or IG-equivalent) tenant.

In short, the combined REIT (i.e. the new REG after acquiring UBA) is set to maintain and perhaps slightly boost REG's status as a blue-chip retail REIT with a high-quality portfolio and strong balance sheet operated by a top-notch management team.

Reasons To Sell UBA And Take The Cash

Why might shareholders choose to sell UBA (or UBP) shares, take the cash, and move on? There are a few reasons I can think of:

- Since UBA offers a higher dividend yield than REG, shareholders will effectively get a dividend reduction equivalent to 50 basis points of yield once their ownership transfers from UBA to REG.

- There are some solid, high-quality REITs currently offering similar or higher dividend yields as UBA now does.

- Non-US holders of UBA could be subject to capital gains tax from the transaction.

The primary reason one would consider selling, in my estimation, concerns dividend income. That ~50 basis point drop in yield could be enough for income-oriented investors to consider selling and reinvesting into one or a few of the many high-quality REITs offering higher dividend yields today.

I'll give my thoughts on this below.

Reasons To Hold UBA And Become A REG Shareholder

At the same time, there are many reasons why UBA shareholders might not want to sell and instead hang onto their shares and become REG shareholders when the deal closes. Here are several:

- The transaction is a non-taxable stock-for-stock deal, which means UBA/UBP shareholders will not have to pay any capital gains taxes. That could be a big deal for those who purchased big tranches of UBA shares at under $10 during the COVID-19 pandemic.

- REG's management team is top-notch, highly focused on owning and maintaining quality properties, and long-tenured at the company.

{kind=link}

- REG is getting a good deal by acquiring UBA at about 13x FFO by using its shares valued at around 14.3x FFO. The deal is expected to be immediately accretive to core operating earnings (aka core FFO per share).

Increasing scale provides increased benefits. REG will be able to not only cut ~$9 million in G&A costs, but also use its extensive leasing platform and scale to increase occupancy and efficiency of UBA's portfolio.

{kind=link}

REG's cost of capital advantage (BBB+, Baa1 credit ratings) should allow the combined REIT to refinance UBA's debt at favorable rates and terms.

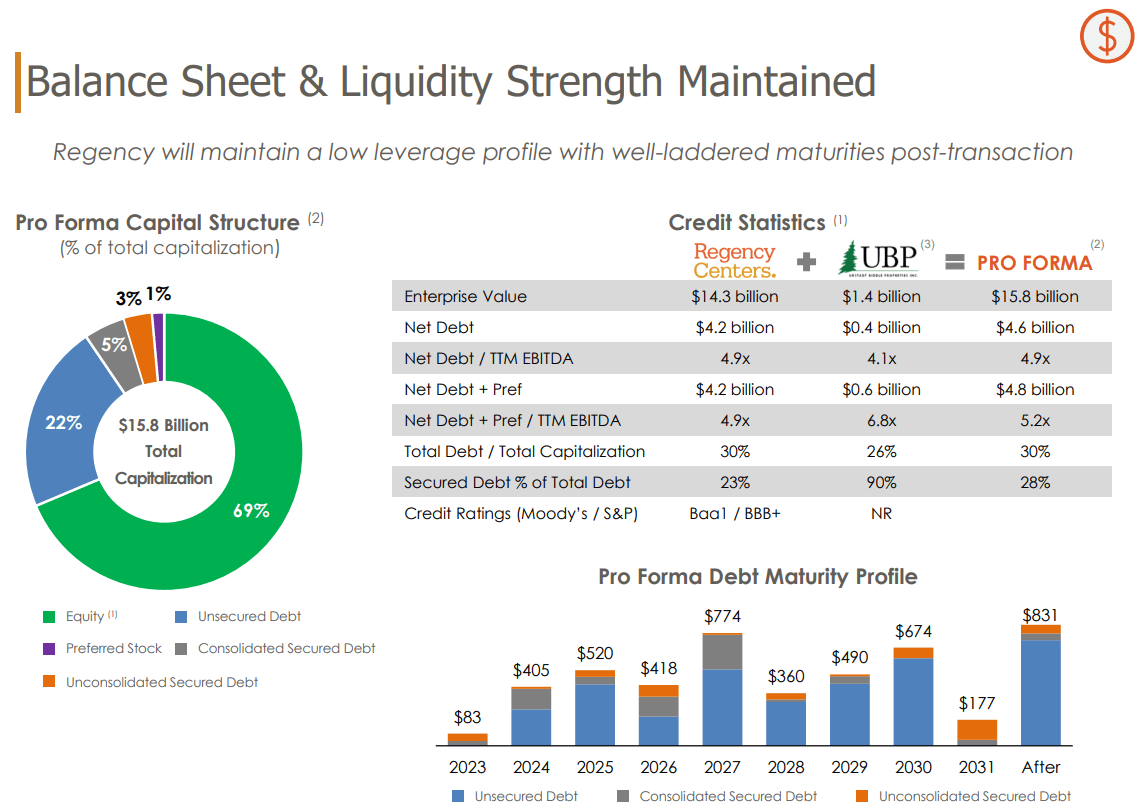

The combined REIT will still enjoy a net debt to EBITDA ratio on the low end of REG's target 5x to 5.5x range.

{kind=link}

Considering only debt, the combined REIT will maintain REG's current 4.9x net debt to EBITDA ratio. Including UBA's preferred equity, that metric jumps to 5.2x.

Upon deal closing, I could see REG choosing at some point to redeem UBA's preferred stocks, especially the 6.25% Series H ( UBP.PH ) shares as they feature a coupon yield well above REG's ~5.5% acquisition cap rates. Of course, cap rates for high-quality, grocery-anchored retail centers have climbed up to around 6% at this point, but if the pricing environment and interest rates drop back down, then UBP.PH is an obvious way that REG can lower its cost of capital.

It's less obvious to me whether management will also decide to redeem UBA's 5.875% Series K preferreds ( UBP.PK ), as the coupon yield is lower. Hence the discrepancy in price between UBP.PH, currently at over $24, and UBP.PK, which currently sits around $23.

My Take

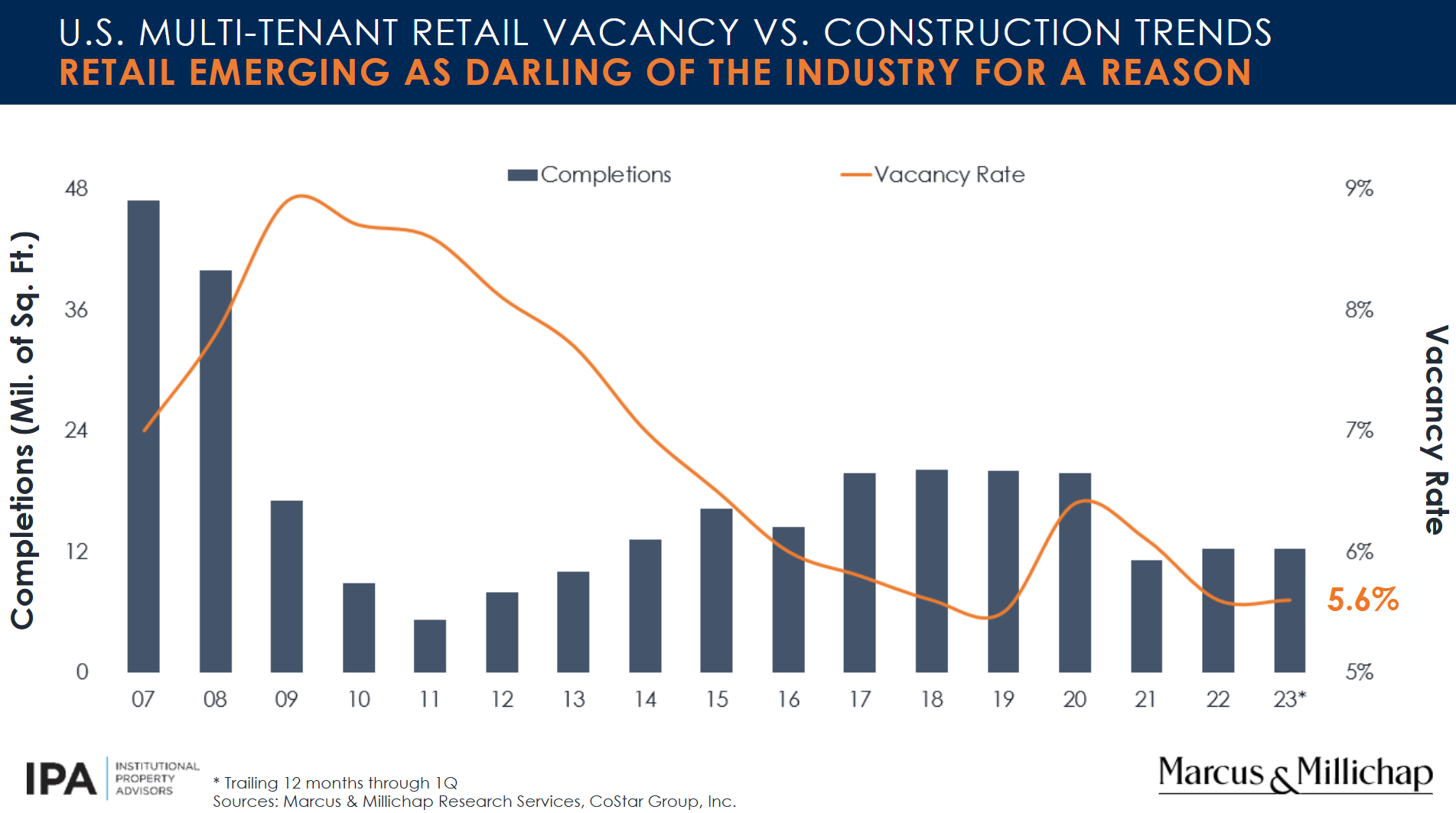

I want to continue owning retail real estate. The supply-demand balance of this sector of CRE looks very favorable to retail landlords right now. Vacancy rates are low, and completions of new retail space remains muted following COVID-19.

{kind=link}

Banks and developers are scared to touch retail real estate, and yet there are lots of signs that the "retail apocalypse" of the second half of the 2010s reached its zenith in 2020, during the COVID lockdown period, and has since reversed course.

And grocery-anchored shopping centers are the strongest and most recession-resistant form of multi-tenant retail real estate.

I do want to keep a sizable position in REG. But UBA is a large position in my portfolio, so the effective dividend reduction will bite into my total portfolio income a bit.

To offset this, I have decided to sell up to 40% of my UBA shares and reinvest the proceeds into stocks of equal or greater quality and higher yields in order to offset the slightly lower dividends from REG.

Here are some of the higher-yielding stocks I'm considering as destinations for the proceeds (comparing this to UBA's current ~5% dividend yield):

| Assets |

| Dividend Yield |

| Crown Castle ( CCI ) |

| Telecommunications towers, small cells, and fiber |

| 5.55% |

| W. P. Carey ( WPC ) |

| Industrial, European retail, single-tenant office, and self-storage facilities |

| 6.25% |

| National Storage Affiliates ( NSA ) |

| Primarily Sunbelt, primarily secondary & tertiary market self-storage facilities |

| 5.95% |

| NextEra Energy Partners ( NEP ) |

| Wind, solar, and battery storage facilities (renewable energy), sponsored by parent company NextEra Energy Inc. ( NEE ) |

| 5.7% |

| Hannon Armstrong Sustainable Infrastructure ( HASI ) |

| Senior-secured loans & preferred equity investments in renewable energy and green infrastructure projects |

| 6.2% |

| Whitestone REIT ( WSR ) |

| Sunbelt, primarily non -grocery-anchored retail shopping centers |

| 5.6% |

| Main Street Capital ( MAIN ) |

| Senior-secured loans & equity investments in lower middle-market companies |

| 6.9% |

| Kinder Morgan ( KMI ) |

| Natural gas pipeline & midstream infrastructure assets, including Gulf Coast export terminals |

| 6.9% |

The average dividend yield of these 8 stocks is 6.1%.

Assuming 60% of my UBA shares go into the (currently) 4.5%-yielding REG and 40% goes evenly into the names above, I'll end up with a weighted average yield of about 5.15% -- above UBA's current dividend yield of ~5%.

This is my current plan of action, but I have not decided when to sell the 40% of my UBA shares for reinvestment. Since it's a stock-for-stock deal, UBA shares should see further upside if REG's share price also rebounds from here. But if REG & UBA see higher stock prices, the higher-yielding stocks above may likewise rise in price, making it a wash.

Benediction

Urstadt Biddle Properties has existed for over 50 years, controlled and largely owned by the same family ever since. I trust that since Willing Biddle, CEO of UBA who married into the Urstadt family (his wife is the founder of UBA's daughter, if memory serves), has given his blessing over the deal, it was the best decision for all shareholders.

Over the years, I've owned all forms of common and preferred equity currently available to investors: UBA, UBP, UBP.PH, and UBP.PK, and I've done well in all of them to varying degrees. Through their prudent stewardship, the Urstadt and Biddle families have blessed my own family, and for that, I am grateful.

Congratulations, fellow shareholders, on a successful investment!

For further details see:

Urstadt Biddle Properties Being Acquired By Regency Centers: Sell Or Stay?