UBA - Urstadt Biddle's Affluent Submarkets Spur Demand

2023-03-17 03:41:58 ET

Summary

- Urstadt Biddle is often overlooked due to its small size and lack of communication.

- Its portfolio is well located in low-supply submarkets.

- I think it is significantly undervalued.

Urstadt Biddle Properties ( UBA ) ( UBP ) owns a concentrated portfolio of grocery anchored shopping centers in the affluent suburbs of NYC. With this footprint, it boasts some of the best catchment area metrics among all REITs with supremely high household income. The REIT has a long track record of strong performance and I believe its business is well positioned for growth. At just over 13X AFFO I think Urstadt Biddle is significantly undervalued.

Let me begin by looking at fair value and follow with why it might be priced so cheaply despite fundamental strength.

Valuation

Grocery anchored shopping centers are in a great place fundamentally as they have a constant stream of foot traffic from grocery stores which fuels the adjacent small shops. The challenge to investing in this area is that the market seems to already know it is a great area and has assigned many of the names a high valuation.

For the most part I think the high valuation is warranted so I would not call things like Regency Centers ( REG ) overvalued, rather I see the outliers on the cheaper end as opportunistic.

Something like an RPT Realty ( RPT ) has a 10X FFO multiple and a 13X AFFO multiple making it quite cheap, but I am not convinced that it has the level of quality I am seeking. Specifically, its leverage might be too high for the current environment.

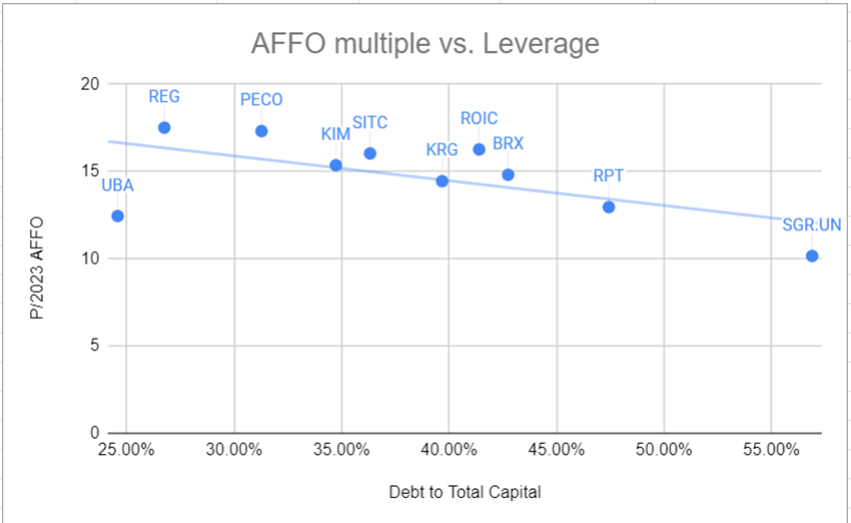

Given where interest rates are, I find it crucial to adjust raw multiples for leverage. Once this is done, I think it is clear that UBA is an outlier to the undervalued side.

{kind=link}

The REITs largely follow the pattern you would expect with higher leverage trading at lower multiples. UBA, however, has the lowest leverage yet it trades at close to the lowest multiple. This magnitude of deviation warrants further investigation and I see 2 possible explanations.

1) It is somehow lower quality/growth/safety

2) It is undervalued and should trade higher.

After studying UBA I believe its overall quality is above average in its peer set for the following reasons:

- Property locations - superior

- Leasing prospects - strong

- Balance sheet - superior

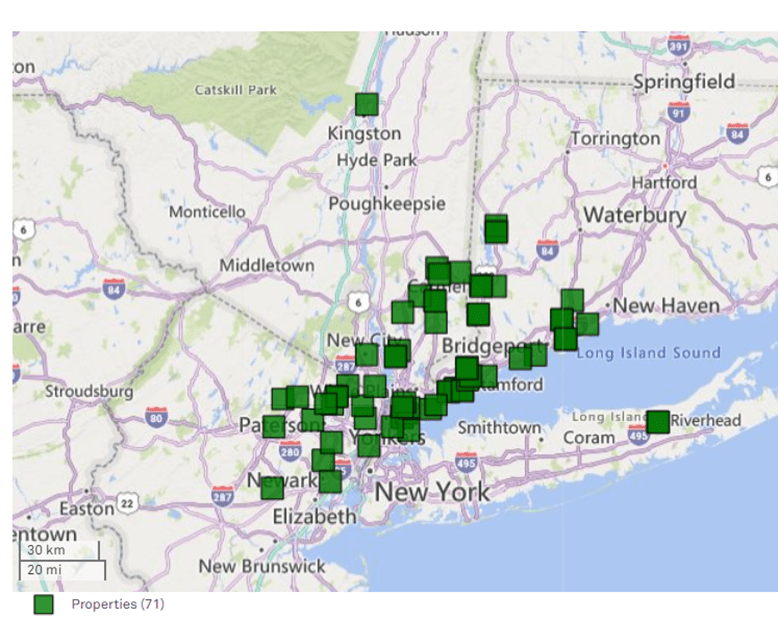

Let me elaborate a bit on each of these topics. While most REITs diversify their properties across the country, UBA is concentrated in the suburbs of NYC.

{kind=link}

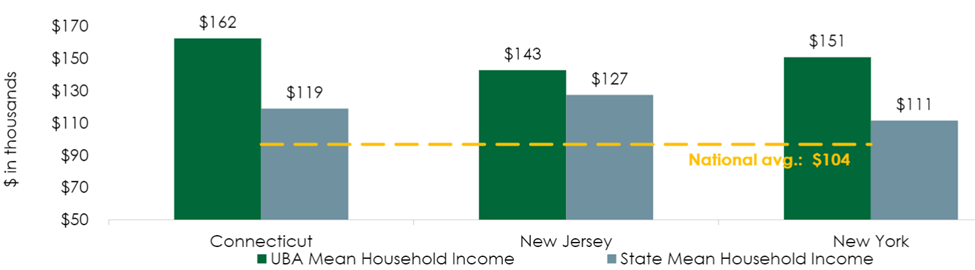

The advantage of this location is that it is remarkably high household income. These are already high income states, but UBA's specific locations are even higher with an average household income of about $150K in their catchment radii.

{kind=link}

Retailers like having access to wealthy customers, which makes UBA's locations quite desirable to rent.

Retailer openings have started to significantly outweigh store closures leading to net absorption in the space. UBA is positioned to capture the incremental demand. In its 1Q23 earnings report (period ending 1/31/23), occupancy ticked up to 94.1% as rents were renewed at 4.6% above expiring rent and new tenants paid 10.3% more than expiring. Most of the retail REITs had great leasing in this quarter, but more impressive to me is UBA's forward leasing pipeline. Per the earnings release:

Our leasing and management teams are very busy working to deliver space for our new tenants, and we have a strong pipeline of new leases that includes 69,500 square feet in the lease negotiation phase and another 124,000 square feet in the letter of intent phase."

That is almost 200,000 square feet of additional future leasing that has yet to hit the bottom line and keep in mind UBA only has 5.3 million square feet. That will be a significant jump in occupancy.

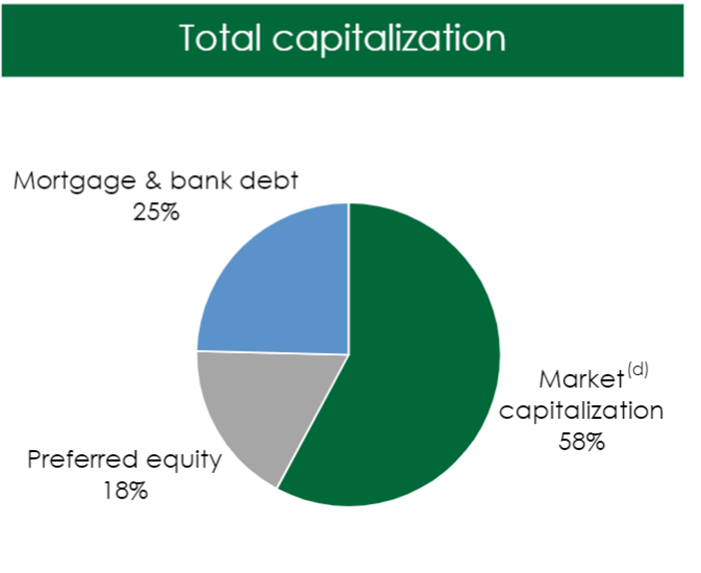

Improved revenues from new leases should filter through to the bottom line nicely as UBA has somewhat low debt and most of it is fixed rate.

{kind=link}

I think most analysts would see these same strengths when looking at UBA, so why would the company trade at such a discount to peers?

Well, I think it is mostly a matter of neutral differences that are being perceived as bad.

Factors holding UBA/UBP down in the market

I think there are 4 main factors causing it to trade well below fair value.

1) Lack of communication

2) Small size

3) Misunderstanding about population density in catchment radius

4) Dual share class structure

UBA feels like a private company that just happens to be publicly traded. They don't do earnings calls. They don't do the industry conference circuit. There is little to no schmoozing of investors or analysts of any sort.

As such, it is more difficult to get to know UBA. With fewer potential investors looking at it, there are naturally going to be fewer investors buying it. This lack of communication is compounded by its small size at a market cap of about $650 million. The sub $1B stature precludes most of the larger institutional investors from even considering it.

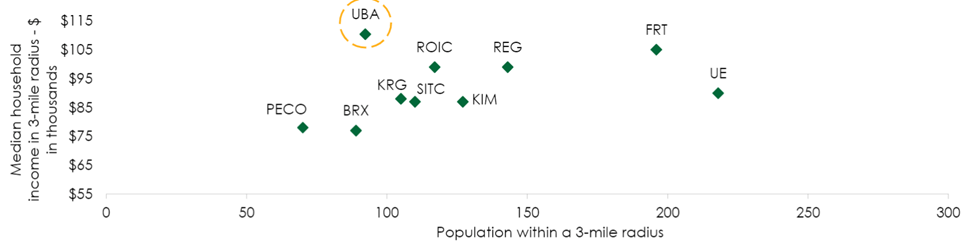

I also believe UBA is being unfairly punished for low population density in its catchment radii. It is among the lowest.

{kind=link}

This is broadly viewed as a negative, but the metric as a standalone is meaningless.

What actually matters is the ratio of population to the square feet of retail space. UBA's catchment radii has a somewhat low population, but it also has a low supply of shopping centers. All in I think that is a favorable situation because shopping centers being further apart means customers are going to be more loyal to their proximally located centers.

Finally, and this is a big one, investors really dislike weird structures and UBA's dual class structure is about as weird as it gets.

UBP is the common share

UBA is the Class A common share.

Any sort of distributions that UBP gets, UBA will get 110% of that. So on the January dividend, UBA got $0.25 per share while UBP got $0.225 per share. The 2 classes of shares will often trade at proportional prices to make their dividend yields approximately equivalent. At the time of this writing UBP is cheaper by about 0.61% after adjusting for relative payouts.

{kind=link}

Earlier this morning, UBP was cheaper by about 3% so there is quite a bit of fluctuation. In my opinion, when they are priced proportionally, UBA is the better way to go because it is significantly more liquid, but if the gap exceeds a 1% advantage for UBP I would lean toward buying UBP. It does have significantly stronger voting rights. For the 10-K wording on the differences between the 2 share classes see below:

Each share of Common Stock entitles the holder to one vote. Each share of Class A Common Stock entitles the holder to 1/20 of one vote per share. Each share of Common Stock and Class A Common Stock have identical rights with respect to dividends except that each share of Class A Common Stock will receive not less than 110% of the regular quarterly dividends paid on each share of Common Stock."

In combination, the supervoting shares and lack of communication with the public might raise concerns about management alignment with shareholders. That is probably the main reason for UBA trading at 65% of NAV.

Why it isn't actually bad

Public companies do all sorts of things for the sake of appearances that might not be the best decisions for the long term health of their companies. When so highly scrutinized there is a tendency to do what looks good rather than what is actually good. Perhaps such motivations are behind the flood of REITs into industrial real estate AFTER it became hot and prices were already prohibitively high.

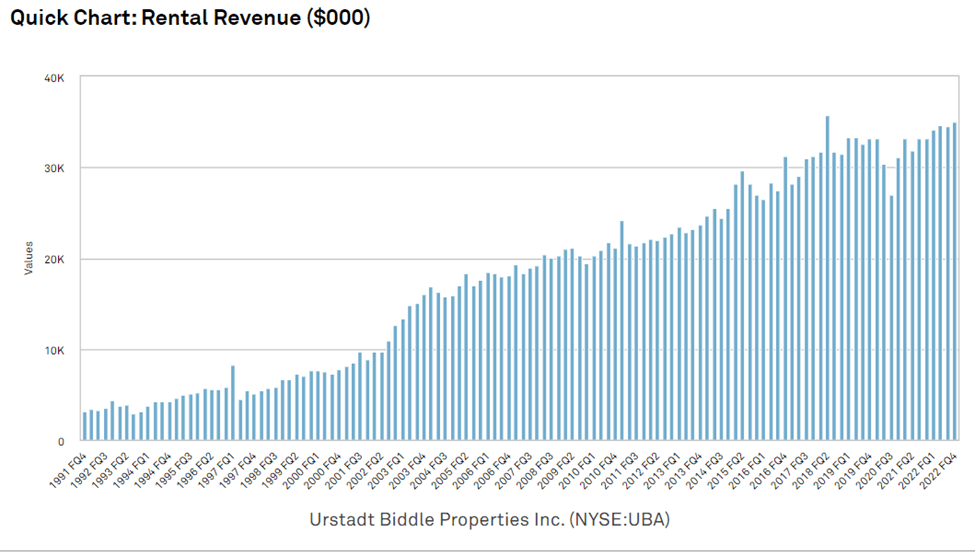

UBA operates differently. They are looking at the 30 year horizon and not caring so much about the next quarter. It has led to strong results over time in what has generally been a challenging retail environment. Revenues have been climbing steadily for over 30 years. There are hiccups for recessions and COVID, but that is a great trend.

{kind=link}

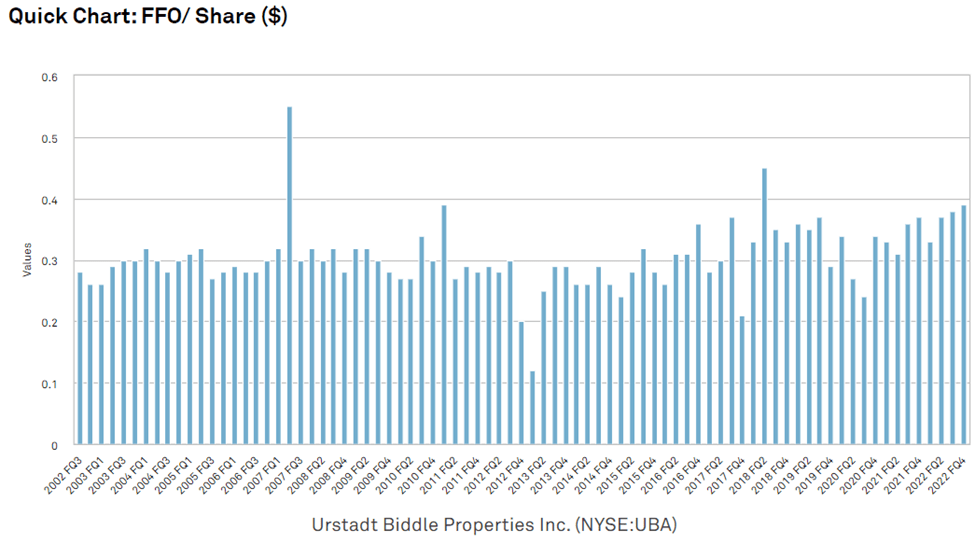

FFO/share has climbed at a slower pace, but a similar upward trajectory is noticeable.

{kind=link}

Another key difference between UBA and peers is that they are content to stay small. Despite being only $650 million in market cap they are executing a rather large share buyback.

Such a move shows clear alignment with shareholders. They are willing to shrink the company to improve value per share by buying stock back at 65% of NAV. Each share bought is immediately accretive to NAV and to FFO/share.

I have also met with UBA management and they struck me as straight forward, honest operators who really understand their submarkets.

The opacity and lack of communication is misinterpreted by the market as misalignment. I see it more as a company just buckling down and doing the work without putting on a show.

If I'm right and UBA is in fact a high quality REIT, it is deeply mispriced and quite opportunistic.

For further details see:

Urstadt Biddle's Affluent Submarkets Spur Demand