URTH - URTH: Developed Markets Are At The Goldilocks Interlude

2023-07-09 08:49:16 ET

Summary

- The iShares MSCI World ETF provides exposure to developed markets, not the entire world, and its share price has been trending higher since October last year.

- The ETF's performance is largely correlated to the U.S. market due to its significant U.S. asset base, with tech stocks like Apple, Microsoft, and Nvidia driving growth.

- Despite a Goldilocks-style growth, there are risks to developed markets from tight monetary policies and U.S-China decoupling, and a correction in the ETF's value appears imminent.

- There could be a 10% correction.

First, unlike what its name suggests, the iShares MSCI World ETF ( URTH ) does not provide equity exposure to the whole world, but only to developed markets as I will elaborate on later. Despite its widely fluctuating path, the share price has been trending higher since October last year as charted below.

Therefore my objective with this thesis is to understand the underlying reasons as well as formulate the most likely outcome for the rest of the year. For this purpose, I will take inspiration from the Goldilocks economy , a term used for depicting an ideal economic situation where there is neither not much expansion nor contraction.

A Goldilocks-like environment

Looking into the rear mirror, more specifically from December 2016 to December 2017, it was one of the periods of the Goldilocks screenplay. Global economic growth was stronger than expected, with inflation present as well, but it was a declining trend, not only in the U.S. as pictured below but in Europe as well. This all played in a macroeconomic context characterized by central banks' cautiousness, and noteworthily, the absence of geopolitical incidents. As to the financial markets, the stock market including URTH recorded good performances, unlike bonds, which is the case today too.

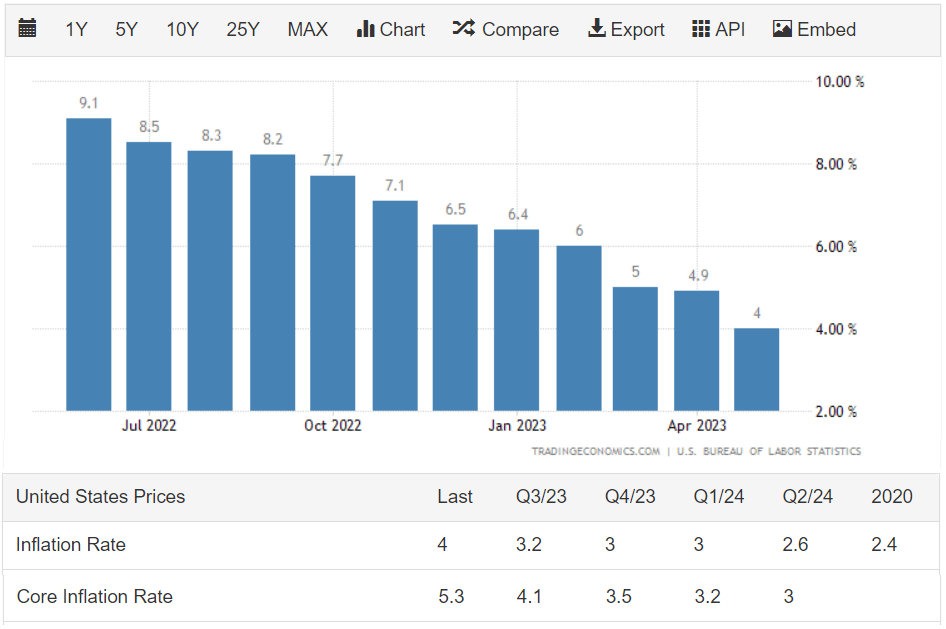

Presently, the main ingredient for Goldilocks is the downtrend in inflation as pictured below and this has brought relief to market participants, as the aggressive pace at which interest rates were hiked since March last year has not broken down the economy.

Inflation trending downwards (tradingeconomics.com)

{kind=link}

To this end, there were fears of systemic risks during the banking turmoil some three months back which tormented regional banks as high-interest rates caused the value of their long-duration bonds to plummet. Two factors that restored confidence in the system were the Fed coming up promptly with lending instruments aimed at alleviating liquidity concerns, and a pause in the cycle of raising rates.

Looking further, the last reading shows core inflation at 5.3%. However, bear in mind the Fed's target rate for inflation is 2% , which is still far away. Therefore, according to the last FOMC (Federal Open Market Committee) meeting, interest rates may still have to be raised further as, despite such a high degree of monetary policy tightness the U.S. economy has been remarkably resilient as seen by its ability to sustainably add jobs.

To put things into perspective, this is not a rapidly growing economy, but has not contracted either as many were anticipating since the end of last year, and is still humming, similar to Goldilocks-style growth, despite an inflation rate of 4%.

URTH's Holdings and Correlation to the S&P 500

As a result, not only has the stock market been sparred, but the S&P 500 has rallied by more than 20% since October as charted in orange. Looking closer, URTH’s price performance in blue has been largely correlated to the U.S broader market.

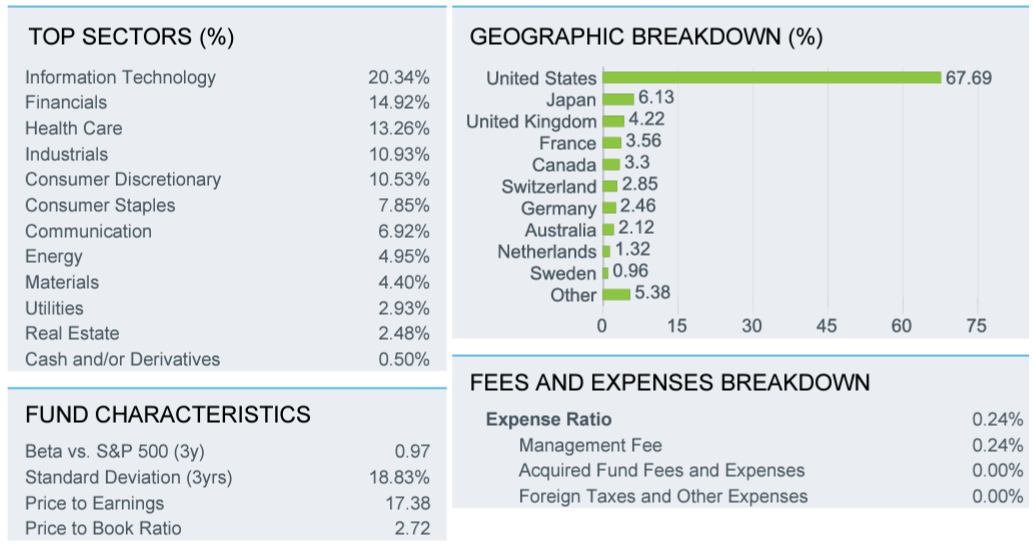

The reason is that 67.69% of its assets are U.S. based, or it is predominantly skewed towards American stocks, followed by Japan at 6.13% as illustrated below. On top, URTH which tracks the MSCI World Index dedicates 20.34% of its weight to the IT sector including stocks like Apple (NASDAQ: AAPL ), Microsoft (NASDAQ: MSFT ), and Nvidia (NASDAQ: NVDA ). These tech stocks have been climbing to new highs due to the four trillion dollars of opportunities now emerging in Generative AI, thereby largely offsetting the pains seen by the financial, healthcare, and energy sectors.

URTH Sector Exposure and Fund Characteristics (www.ishares.com)

{kind=link}

To get further insights into what is to come, I look at some of the comments made by the Fed's Chairman Jerome Powell during the last FOMC meeting. His main argument was centered on economic resiliency together with the need for tight monetary policy to control inflation, implying additional rate raises. Later, speaking in Portugal on June 28, Mr. Powell again reiterated that while monetary policy is tight, it may not be restrictive enough and has not been in force for long enough, to get inflation under control.

Thus, after raising rates three times by 25 basis points this year, and pausing in June, the Fed could hike by another 50 basis point hike this year, and, if past performance repeats itself, could be bad for URTH, in the same way as last year when suffered from a downside (orange chart) when Fed fund rates were raised (blue chart).

In addition, there is also the possibility of an economic slowdown hitting the stocks of developed markets.

Possibility of a Mild Economic Slowdown

In this respect, Mr. Powell has mentioned the lag between the time interest rates are applied till the full effects of tightening occur with the main factor to watch out for including bank credit availability. Now, according to veteran fund manager Richard Woolnough, this can take up to 18 months and according to the timing of rate hikes, the full effects should only be seen in the second half of 2023, possibly in the form of a mild "economic slowdown" according to economists consulted in June.

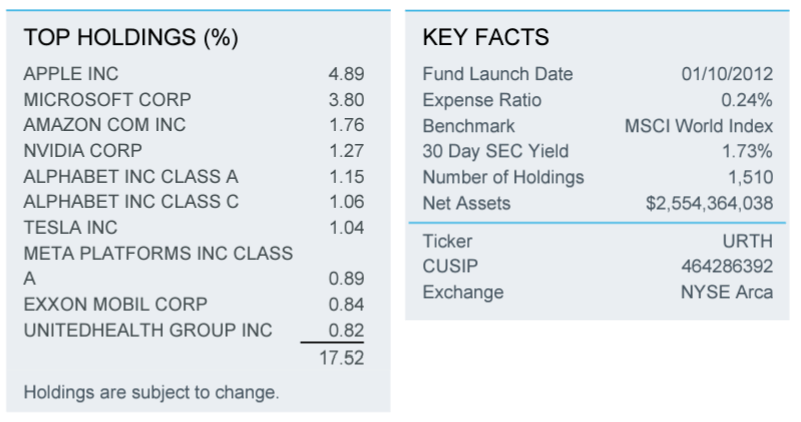

Consequently, investors should be aware that despite all their artificial intelligence prowess, URTH's main tech holdings (as pictured below), could be impacted by lower consumer spending and a fall in advertising revenues. Detailing further, the ETF holds a total of 1,510 stocks, charges fees of 0.24%, and pays 1.73% of dividend yields (30-Day SEC yield).

Top Holdings (www.ishares.com)

{kind=link}

Furthermore, with more than 20% of its assets dedicated to Europe, URTH should not be spared from volatility impacting the old continent where the Central Banks also have the same inflation-reduction mandate as the Fed which leaves Japan as the only country where the Goldilocks effect should persist. The reason is its 3.2% inflation remains well below America and Europe, and while other central banks have been juggling with interest rates, the Bank of Japan has been coolly maintaining its key interest rate at - 0.1% since 2016.

However, with most of the attention concentrated on the Fed, the European Central Bank, and the Bank of England (to a lesser extent), many seem to have forgotten the world’s second-largest economy. For this matter, China’s post-Covid recovery is far from strong with the PMI (Purchasing Managers Index) well below expected. Now, with the PBOC (People's Bank of China) not having the same inflation-fighting constraints as the West, it has more room for stimulus, but one has to be patient while geopolitical tensions with the U.S. are starting to complicate things. Thus, the latest curbs on exports of semiconductor-making metals like Gallium and Germanium by Chinese authorities could be in retaliation to the U.S. Commerce Department possibly restricting Chinese companies' accessibility to intelligent cloud services.

Now, restrictions to the free flow of goods have the potential to disrupt semiconductor and solar panels supply chains or make components dearer, thereby contributing to high inflation. Worst, China's move could also backfire as the West recalibrates its supply chain away to Vietnam or India, in turn hurting the economic recovery of the world's largest metal exporter (2020 figures). Detailing the China-related risks further, as the most industrialized nation, the country is a large producer of goods and consumer of raw materials, and, as such, any weakness could reverberate negatively across both developed and emerging markets.

Be Ready for a Correction

Therefore, there are risks to the economies of developed markets, not only from their own central banks' pursuing tight monetary policies but also from U.S-China decoupling, or reducing their economic independence.

Moreover, the latest U.S. labor market data indicate that 209K jobs were added in June, or the fewest since Dec 2020, but wage growth continues to remain strong. This means that workers have more disposable income to buy goods and services, in turn sustaining high demand. Now, higher demand rhythms with elevated prices, in turn contributing to a higher consumer price index. Also, job creation figures for April and May show that higher borrowing costs are starting to grind businesses' appetite for growth.

Thus, when looking at the data in its globality, it shows that while the Fed’s action is impacting growth, the labor market's tightness implies that expectations for a raise in interest rates remain intact. Consequently, the take for investors is that despite inflation trending lower as seen earlier, there is no room for complacency from the U.S. central bank and that one should not entertain false hopes for Goldilocks to continue as if everything is OK.

To further support my pessimistic outlook, contrarily to the 2016-2017 period, there is a war in Europe that lingers on and any escalation to neighboring countries could bring the conflict nearer to URTH’s developed markets. Also, there are geopolitical risks around Taiwan which could adversely impact supply chains in case of tit-for-tats reactions to restrictive measures imposed by either side.

Looking at the price performance, after its upside, the ETF has reached a price-to-earnings multiple of 17.44x , compared to 12.62x for the Vanguard FTSE Developed Markets ETF ( VEA ). Well, their holdings differ, but, a comparison of their valuations shows that the iShares ETF is 38.2% overvalued which is unsustainable in view of the risks I have mentioned. Thus, an above 10% correction as in January 2018 (chart below) after the 2016-2017 Goldilocks episode cannot be excluded.

In conclusion, after seeing an above-20% Goldilocks-style upside, the ETF is currently at the interlude which means that it is not the time to be complacent and that a correction appears imminent. On top, of this time around, there is no shortage of geopolitical ingredients which could adversely impact stocks in sharp contrast with seven years ago.

For further details see:

URTH: Developed Markets Are At The Goldilocks Interlude