URTH - URTH: Expect Negative Long-Term Real Returns On Global Stocks

Summary

- The high weighting of overvalued U.S. stocks, the strong likelihood of profit margin mean reversion, and the weak growth outlook, suggest the URTH is unlikely to keep pace with inflation.

- The ETF has exposure to international developed markets yet the outperformance of U.S. stocks over the past decade has raised the U.S.' weighting in the ETF to 68%.

- As borrowing costs continue to rise globally, this poses another risk to long-term URTH returns, should investors require higher returns on equities to compensate for rising bond yields.

For long-term focused investors, the iShares MSCI World ETF ( URTH ) has become an increasingly popular option. Inflows into the ETF have soared, doubling since 2019 to reach USD16bn. The ETF has exposure to international developed markets. However, the outperformance of U.S. stocks over the past decade has raised the U.S. weighting in the ETF to 68%. With U.S. stocks significantly more expensive than most of the rest of the world, URTH is likely to perform poorly as growth slows and profit margins decline. Over the next decade, URTH is unlikely to keep up with inflation.

{kind=link}

The URTH ETF

The URTH ETF is heavily weighted towards U.S. stocks, which make up 68% of the index, thanks to their sustained outperformance over recent years. The top 10 stocks, which make up around 15% of the index, are all U.S. companies, and while they have some exposure to international markets, this is clearly a U.S.-centric ETF despite having exposure to other developed market countries. Japan is the second-highest weighted country with just 6% of total assets, followed by the U.K., which has 4%.

In terms of sector exposure, the dominance of U.S. stocks means that the breakdown looks similar to the S&P500, with Information Technology commanding a 22% share, followed by Health Care (15%) and Financials (14%). The fund charges a 0.24% expense fee, which is on the high side compared to many world ETFs such as the Vanguard Total World Stock ETF ( VT ) which charges just 0.07%. This despite the VT's higher number of stock holdings and exposure to Emerging Markets.

10-Year Forecast Still Suggests Negative Real Returns

Long-term equity market returns can be broken down into three parts; the dividend yield, expected growth in dividends, and any change in the dividend yield reflecting the valuation that investors are willing to pay for stocks. The current dividend yield on the MSCI World is 2.3%, and dividends have grown at a pace of 4.6% annualized over the past decade. If the dividend yield remains at current levels and dividends continue to grow at 4.6% per year, the URTH should be expected to return 6.6% annually over the long term. In real terms, with 10-year breakeven inflation expectations currently at 2.3%, this translates to 4.3% annual real returns.

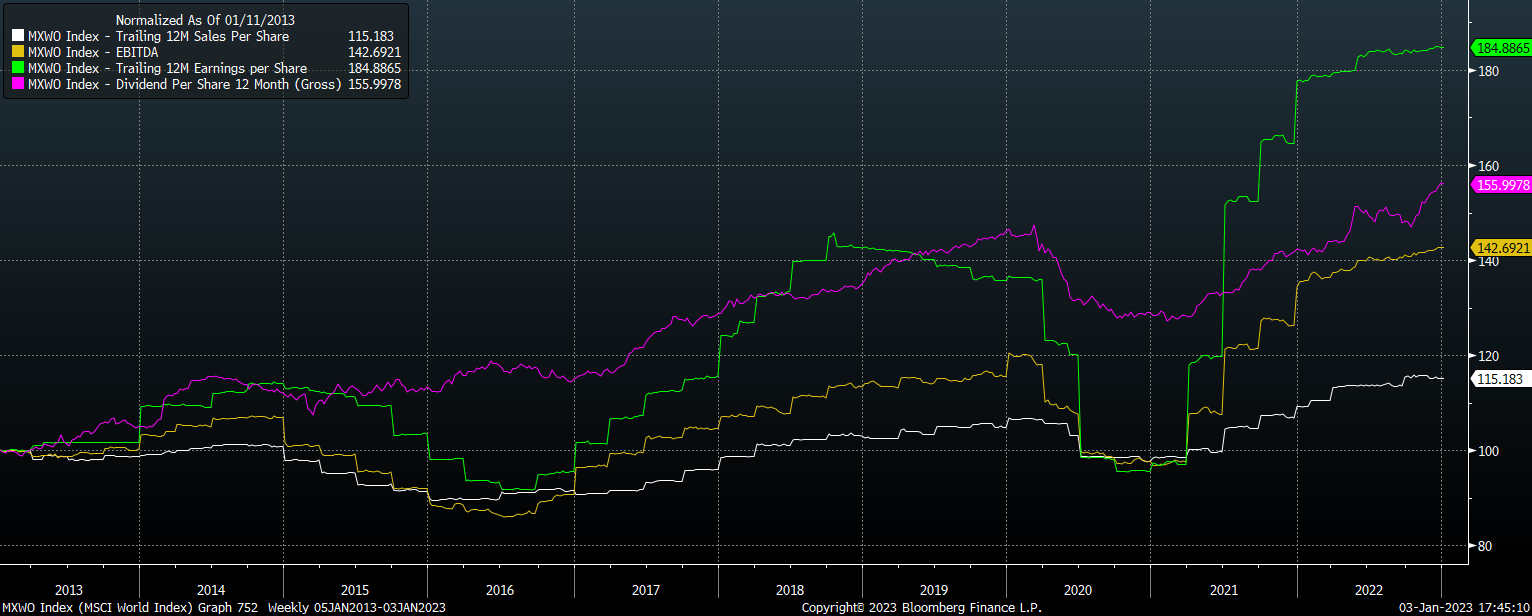

However, this is likely to be overly optimistic when other factors are taken into account. For instance, while dividends have grown by 4.6% over the past decade, sales have only risen by 1.4% annually. Dividends have grown significantly faster than sales over the period thanks to rising profit margins, which have been driven largely by falling interest costs, tax costs, and depreciation expenses. With these costs now appearing to have bottomed out, I think it is fair to expect profit margins to fall sharply over the coming years, and for dividend growth to be constrained by sales growth.

MSCI World Sales, EBITDA, EPS, Dividends, Rebased (Bloomberg)

{kind=link}

There are two implications of this. Firstly, sales growth over the past decade has averaged 1.4% annually. If we assume that this pace of growth continues and dividends keep pace, this would bring real annual total returns on the URTH down to 1.1% (2.3% dividend yield + 1.1% dividend growth - 2.3% inflation).

Secondly, there is potential for dividend payouts to decline from their current elevated level relative to sales. While the current dividend payout ratio (dividends as a share of current earnings) is historically low at 39%, compared to a long-term average of 46%, dividends are elevated relative to every other metric, even EBITDA. Dividend payments are currently 21% of EBITDA, which is around 25% higher than its long-term average. If dividends return to their long-term average share of EBITDA over the next decade, this would act as a 2% drag on annual returns, putting total annual real returns on the URTH at -0.9%.

Of course, there is the possibility that profit margins will remain elevated for years to come, which would allow companies to continue paying out elevated dividends for years to come. There is also the potential for sales to rise much faster than they have over the past decade, should global growth recover. However, the risks appear to the downside, particularly as borrowing costs continue to rise globally. This poses another risk to long-term URTH returns. Should investors require higher returns on equities due to the rising yields on bonds, the effect on returns could be devastating. A 1 percentage point rise in the required dividend yield on the MSCI World by 2033 would be enough to knock 3.5% annually off of 10-year returns, reducing total annualized real returns to -4.4%.

{kind=link}

Summary

Investors in the URTH risk overestimating the long-term returns likely from international equity benchmarks. The high weighting of overvalued U.S. stocks, the strong likelihood of profit margin mean reversion, and the weak outlook for global growth, suggest the URTH is unlikely to keep pace with inflation over the next decade, particularly after fees are taken into account.

For further details see:

URTH: Expect Negative Long-Term Real Returns On Global Stocks