USFD - US Foods Holding: Risky Until Proven Otherwise

2023-08-08 04:12:07 ET

Summary

- US Foods Holding is a food distribution company that sells to various venues.

- The company has achieved stable growth in its revenues. An improving margin, that the company strives for, could make the investment a more worthy opportunity.

- USFD's valuation is high in my opinion and its high debt level poses a risk, leading to a sell rating.

US Foods Holding ( USFD ) is a company that sells food through restaurants, hospitals, nursing homes, hotels, and other venues. As the company holds a sizable amount of debt and has a trailing P/E -ratio of 30, I believe the stock is worthy of a sell-rating.

The Company

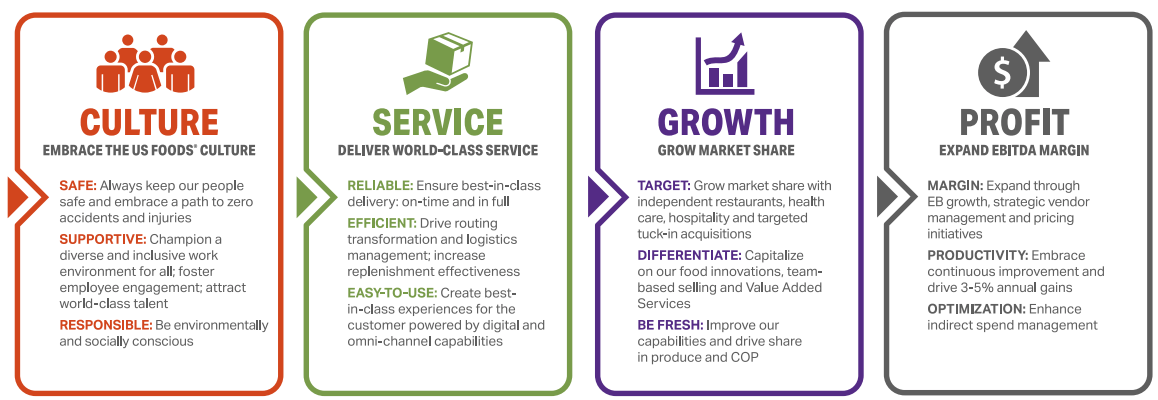

USFD provides venues with food items, as told in the thesis summary - the company's slogan is "We help you make it". The company's strategy revolves around a steadily growing market share that's achieved through fantastic service:

{kind=link}

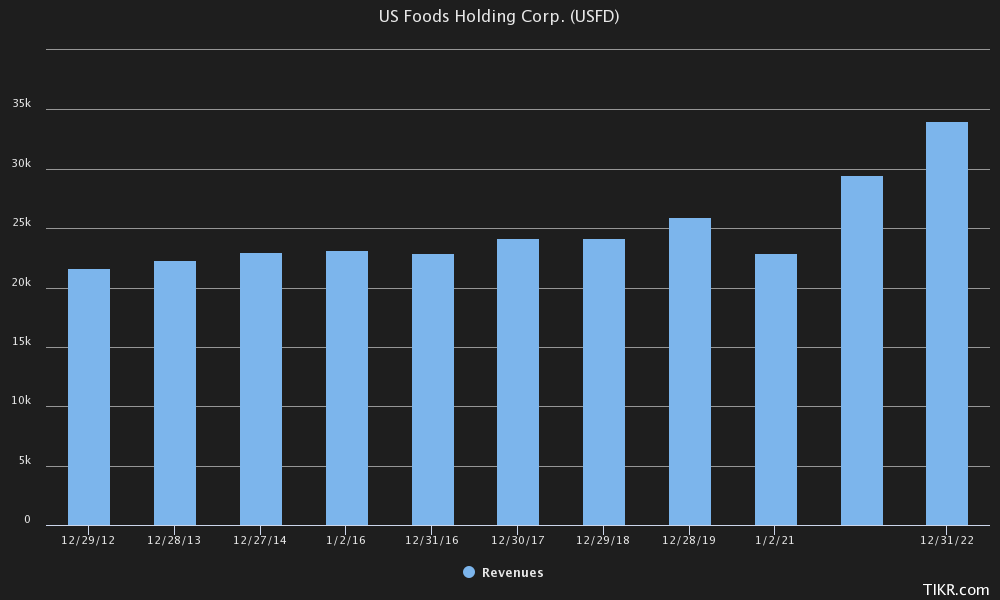

The company has achieved stable growth throughout its history.

Financials

US Foods' financials show a story about mostly stable growth, excluding the Covid-hiccup in FY21:

{kind=link}

The company's revenues have grown with a compounded annual growth rate of 4.6% for the past ten years.

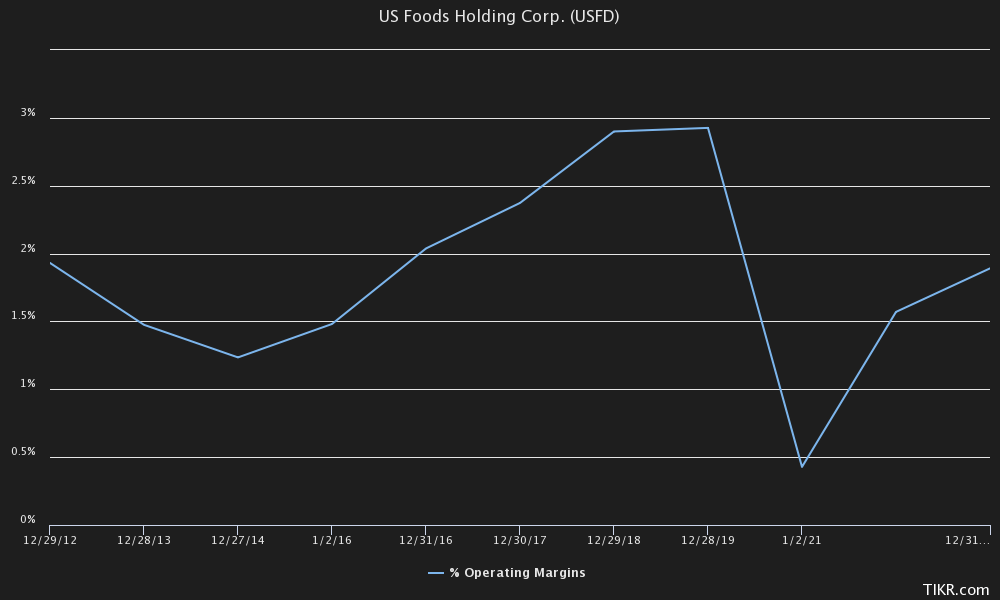

US Foods' operating margin has always been thin at around two percent:

{kind=link}

With trailing numbers, the company's margin stands at 2.3%. US Foods has plans to expand their margin through further collaborations with partners.

US Foods' balance sheet shows a risky side to the company, as they have interest-bearing debts totalling over $4.5 billion , mostly in long-term debt. To balance the debt, US Foods only has a cash balance of $292 million - the company is highly leveraged, imposing a risk to investors.

Incoming Q2 Result

USFD should report its Q2/2023 results on the 10th of August. The company is expected to have a growth in revenues of 5.3%, compared to Q1 growth of 9.5%. I believe this expectation is very reasonable, as food inflation should increase nominal revenues in the sector.

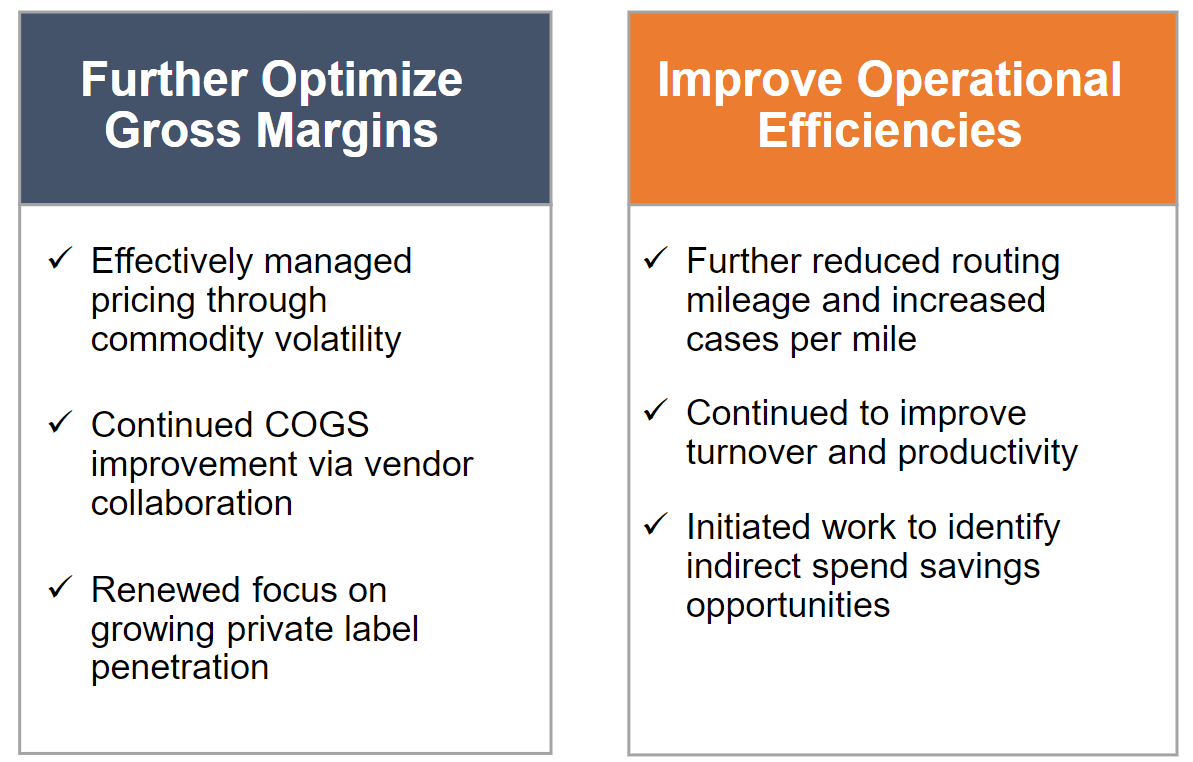

Analysts also expect an EBIT margin of 3.5% for the quarter - a quite significant jump from last year's 3.1%. The expected rise in margin is explained by US Foods' efforts to further optimize their operations, as told in the company's Q1 result presentation :

{kind=link}

The operational improvements showed promise in Q1 already, as the EBIT margin jumped to 2.8% from previous year's 1.9% - a significant improvement of 90 basis points. To sum up the incoming results, I believe the next quarter's expectations are completely reasonable from analysts.

Valuation

Finally, the cornerstone of my bearish sentiment, the company's valuation seems to price in a lot from the company. The company trades at a trailing price-to-earnings ratio of 30.25. The earning yield alone is already less than USA's 10-year bond yield of 4.04% . Of course, the expected long-term growth that I, and analysts, have in mind, add around 5% to the company's expected return for a period. With the earnings yield of 3.3% and a growth of 5%, the stock would have an expected annual return of 8.3%.

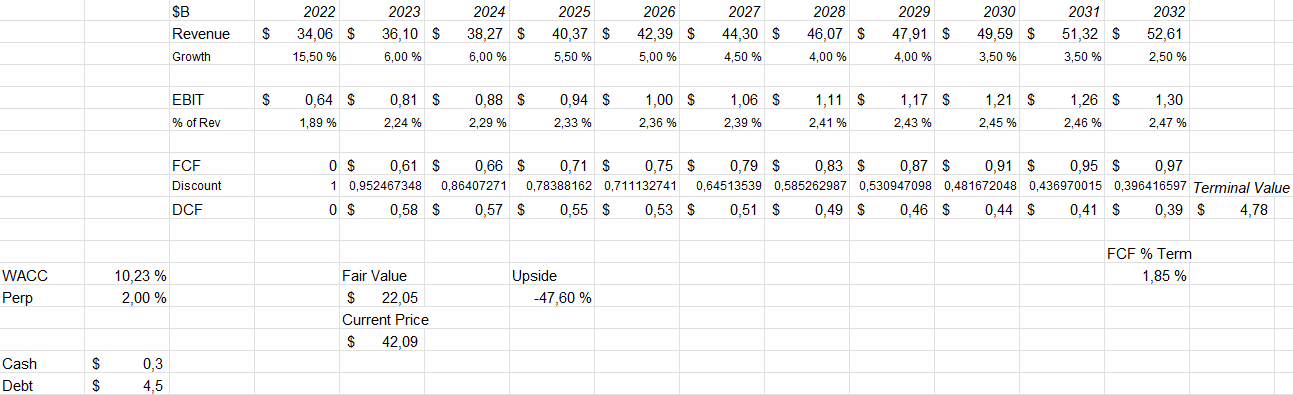

Taking evaluating the company's value further, I constructed a discounted cash flow model in my usual manner. In the expected numbers, I believe USFD will have a growth of six percent in 2023 and 2024, with the growth slowing down slowly into the terminal rate of two percent. This is coupled with a growing operating margin, as the company's EBIT margin rises from 2.24% in 2023 to 2.47% in 2032. The company should convert its earnings into free cash flow quite well, crafting the following DCF model:

{kind=link}

The estimated fair value of $22.05 is 48% below the stock's current price of $42.09 - a significant gap to the downside. The used value for the weighted average cost of capital of 10.23% is derived from a capital asset pricing model:

CAPM of USFD (Author's Calculation)

The cost of debt of 6.19% is calculated from the company's interest expenses - the company has had $281 million in interest expenses in the last twelve months, and with their amount of interest-bearing debt this amounts to the mentioned cost of debt. The company has a very high amount of debt, and I expect the amount of debt to stay quite high at a 35% debt-to-equity ratio.

I use the United States' 10-year bond yield as the risk-free rate, with the yield currently being 4.04%. The used equity ris k premium of 5.91% is Professor Aswath Damodaran's latest estimate made in July 2023. The stock has a historical beta of 1.49 according to Yahoo Finance . Finally, a small liquidity premium of 0.4% is in my opinion justified in the cost of equity, crafting a cost of equity of 13.25% and a WACC of 10.23% that's used in the DCF model.

Is The Company Cyclical?

US Foods has a beta of 1.49, which suggests the company to be quite cyclical in nature. This beta came as a surprise to me, as for example grocery stores have very low betas - for example according to TIKR, Kroger has a beta of 0.48 and my recently covered Ingles Markets has a beta of 0.67. The offering does vary from grocery chains, though, as US Foods provides food mostly to restaurant venues instead of straight to consumers. As restaurants are a more expensive way to eat, restaurant spending should be more volatile in terms of the macroeconomy than grocery stores.

Also, the company's heavy debt balance leverages its operations, making the investment more volatile for shareholders - for example in the Covid pandemic, the company's bottom line dove into negative territory because of a weakened EBIT and high interest expenses. In this sense, paying off debt would make the company a lower risk investment.

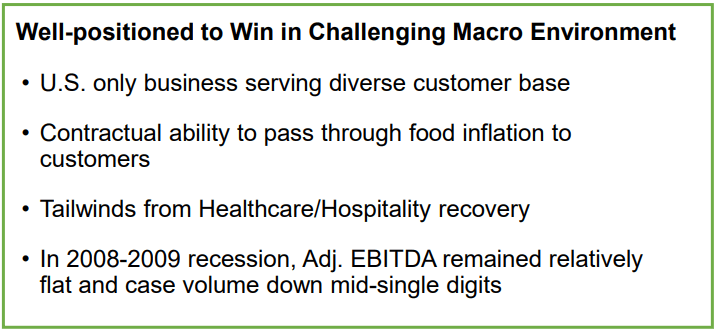

The company does make a point in its Q1 investor presentation that it can handle a turbulent macroeconomic environment:

{kind=link}

US Foods doesn't have public financial filings for the 2008-2009 period, but taking the company's words at face value, the last bullet point would be a very positive sign - a beta of 1.49 would not be justified in my opinion if the company had such strength in the recession.

Takeaway

If US Foods' operating margin doesn't jump very significantly in the coming years, I believe the stock is currently quite highly valued at $42.09. The company's risk profile is heightened by a high amount of debt, making the investment volatile. With a significant downside to fair value in my DCF model estimates, I believe it's justified to have a sell-rating for the stock.

For further details see:

US Foods Holding: Risky Until Proven Otherwise