USNA - USANA Health Sciences: Dipping Revenues But It Could Improve

Summary

- USNA has endured declines in revenue, net income, and free cash flow over the past two years.

- Recent acquisitions and a robust balance sheet offer the potential for a change in the company's fortunes.

- At present, my assessment of USNA is that it's a hold, as it's currently trading at close to my estimate of its fair value.

USANA Health Sciences, Inc. (USNA) experienced significant benefits during the pandemic as a major chunk of their sales comes from dietary supplements, which saw a surge in demand. The company reached its highest revenue in 2021 and 2022. The recent acquisitions of Rise Bar and Oola have added to USNA's portfolio. However, the post-pandemic dip in revenue and declining cash flow is a concern. Additionally, the company is facing rising costs of sales due to inflation, which is affecting its profitability. Based on these factors, I would give USNA an initial rating of hold.

About the Company

USANA is a company that produces high-quality nutritional supplements, healthy foods, and personal care products. These products fall under the categories of optimizers, nutritional supplements, food, skincare, and others. The company has more than 500,000 customers and operates in 24 countries, with the majority of its sales coming from Asia, particularly China, as well as some sales from America and Europe. That's why it places a significant emphasis on its operations in China.

Industry Outlook

According to Statista, the beauty and personal care industry is expected to experience a compound annual growth rate ((CAGR)) of 4% until 2027. This is justified given the growing global population and rising disposable income of Chinese consumers. All of these factors mean a bigger market with better demand for this industry.

Fortune Business Insights predicts growth of about 9% for the dietary supplements industry from this year through 2028. The significant and far-reaching impact of the COVID-19 pandemic has led to an increase in demand for dietary supplements across all regions, as the fear of the virus has made people more health-conscious and focused on their intake of nutrients.

While many companies experienced a backlash during the pandemic, companies like USNA have seen a greater demand in pandemic years as 80% of its sales comes from nutritional supplements.

Recent Performance

USNA experienced unprecedented growth during the pandemic, with revenues reaching new heights in 2020 and 2021, totaling almost $1150M and $1200M , respectively. This was largely attributed to the heightened demand for nutritional supplements and healthy foods as people sought to maintain their health in the face of the COVID-19 virus.

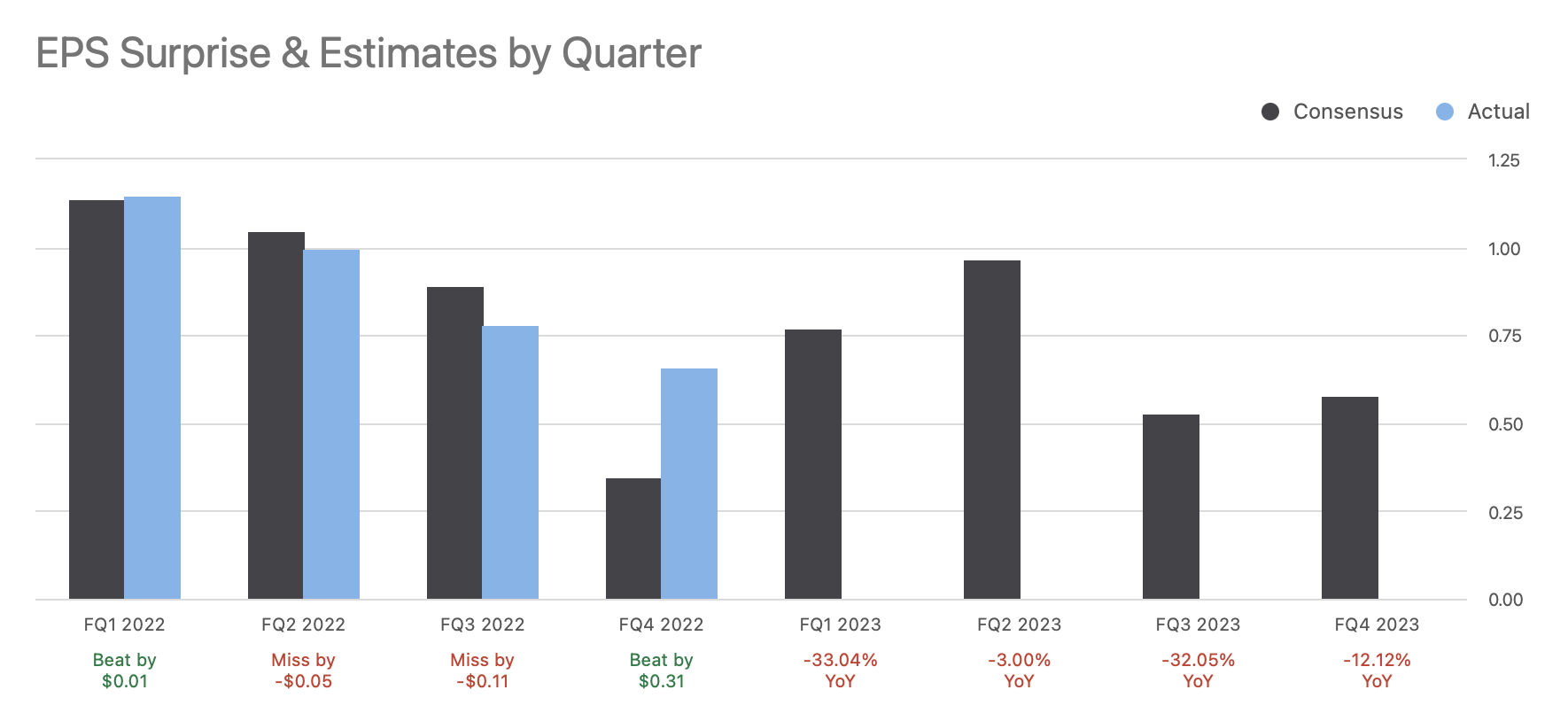

However, as the situation improved and the fear of the virus subsided, the company saw a decline in sales, with a 17% drop in 2021. Each quarter, the company recorded decreasing sales and lower earnings for its shareholders. With the company posting negative results, the market had low expectations for the final quarter. But the company defied these expectations and delivered powerhouse results. A surge in demand during the final two weeks of the quarter led to an incredible 90% upside surprise in earnings per share ((EPS)), comfortably exceeding market expectations.

Strengths

In contrast to the income statement, which displays a decrease in revenues and a shrinkage of net income by more than 40% in just one year, USNA's balance sheet still demonstrates a strong financial position. The company is debt-free, which is far from typical in at a time when the small-cap stock market is heavily populated with so-called "zombie companies" - i.e., those that can only survive by continuing to incur debt. That USNA's full income can be utilized for the benefit of shareholders without the need for long-term debt payments provides shareholders with significant return potential.

Furthermore, the company's short-term or day-to-day financial well-being is robust. With a current ratio of 2.7x and a cash ratio of 2.0x, USNA appears to be highly liquid in the short term. This eliminates the concern of investors about potential short-term obligations that could arise at any time.

USNA has never issued dividends, but instead implements what I think is a superior approach to reward its investors: a share repurchase policy. Over the past 12 months, the company has invested over $62 million in its share repurchase program. This reflects management's confidence in the company, and suggests that they still view the shares as undervalued. The share repurchase system not only boosts EPS, but also saves a significant amount of taxes that the company would otherwise have to pay if it were to hand out dividends.

{kind=link}

Weaknesses

One of the significant issues I observe regarding USNA is its reliance on doing business in China, which is currently causing difficulties for the company's growth. The COVID-19 crisis in China and its stringent lockdown measures are affecting USNA, as a large portion of its sales comes from this region. Any alteration in the policies by the Chinese government directly affects USNA's sales. This was evident in 2021 when the lockdowns in China resulted in a 16% decline in USNA's revenue.

Another thing that concerns me is escalating inflation and growing interest rates. Unlike service companies, USNA is heavily reliant on raw materials for its product manufacturing. This growing cost of sales and operating expenses is a source of worry for USNA. The operating income as a percentage of revenue has been decreasing over the past two years and has dropped to as low as 10% for the company.

Another aspect contributing to its weakness is the decreasing un-levered free cash flows (UFCF). UFCF represents the amount of cash a company has before considering its financial obligations and shows the amount of cash available for the company's expansion. The reduction in USNA's UFCF indicates a risk to its future growth as the company has less cash each year. This decrease not only reduces the overall enterprise value, but also makes it challenging for management to secure capital and pursue other opportunities in the future.

When evaluating a company's performance, it's important to not only consider its internal factors and growth, but also how it compares to its industry and competitors. By comparing a company to similar firms, you can get a better understanding of its ability to outperform its competition and provide better returns for its investors. The forward-looking revenue growth for USNA's peers Medifast ( MED ), Herbalife Nutrition ( HLF ), and The Beauty Health Company ( SKIN ) is estimated at 16%, -10%, and 57%, respectively. However, USNA is far behind at -16%. Additionally, when compared to the industry as a whole, the forward-looking EBITDA growth of the sector median is 5%, while USNA is struggling at -10%. This suggests that USNA might have difficulty surpassing its peers and could struggle to keep pace with them.

Looking Forward

There are two factors that could potentially increase USNA's revenues in the near future:

- The recent acquisition of Rise Bar and Oola: Rise Bar produces protein bars and Oola provides a personal development framework. These acquisitions took place in November 2022, facilitating potential revenue growth that will be reflected during the first quarter of 2023.

- Chinese New Year and easing of lockdowns: As previously noted, USNA's revenues are heavily dependent on China. The first quarter of 2023 could be favorable for the company for a couple of reasons. The Chinese New Year, celebrated on Jan. 22, 2023, typically leads to an increase in spending. Also, the easing of lockdowns in China makes it easier for the company to supply, market, and sell its products.

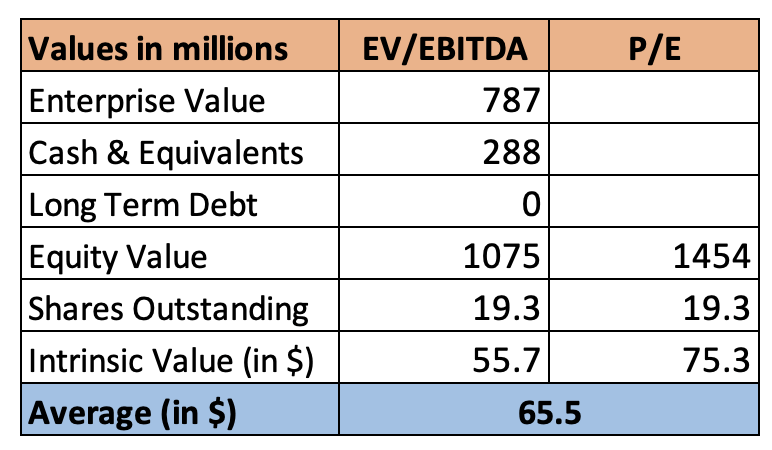

Valuation

By using the intrinsic valuation methods of EV/EBITDA and P/E multiples, I've established an average value of $65.5. The current stock price is $61.4, which suggests that the stock is close to its fair value. I utilized the following assumptions in these valuations:

- P/E Multiple - A sector median P/E multiple of 20.98x was considered compared to USNA's 17.03x.

- EV/EBITDA - A sector median EV/EBITDA multiple of 13.74 was used in comparison to USNA's 7.31.

Intrinsic Valuation (Created by author using data from Seeking Alpha)

{kind=link}

Conclusion

Several factors indicate that the company has a lot of potential. Its strong short-term liquidity, the absence of long-term debt, and an active share repurchase program demonstrate the company's solid financial position. The fact that it has recently acquired two companies and has a peak season ahead of it, I would include USNA on my watchlist.

However, the company's shrinking revenues and net income concern me. The fact that the UFCF is declining and that revenue highly depends on the policies of China raises questions about its growth. Since the current stock price is nearly equal to my estimate of its fair value, I rate USNA as a hold.

For further details see:

USANA Health Sciences: Dipping Revenues, But It Could Improve