USNA - USANA: New Digital Tools And Solid Balance Sheet Imply Undervaluation

2023-10-23 05:01:02 ET

Summary

- USANA Health Sciences has a diversified international presence, with 90% of net sales coming from international markets.

- The company has a healthy balance sheet with strong liquidity and solid asset/liability ratio.

- The launch of new digital tools and affiliate programs in 2023 is expected to drive net sales growth in the coming years.

USANA Health Sciences ( USNA ) recently delivered a clean balance sheet and an internationally proven business model already producing free cash flow even with declining net sales. In my view, the affiliate program and new digital tools designed and launched in 2023 will most likely bring net sales growth and FCF growth in the coming years. I do see risks from currency fluctuations, failed introduction of products, or M&A failures, however the company appears quite undervalued. I executed a DCF model.

USANA Health Sciences: International Operations Make The Company Quite Diversified

With production distributed internationally mainly through its own sales channels, USANA Health Sciences is a company that designs, manufactures, and markets nutritional skin care and health products in general based on extensive technological research on which the company bets on its differential in relation to competing products in the market.

Source: 10-Q

By July of the current year, the company considered having a client portfolio close to half a million internationally, which is distributed between individual clients who agree to purchase products for their personal use and clients who make the purchase for subsequent distribution in markets and retail stores.

As of July 1, 2023, we had approximately 487,000 active Customers worldwide. Source: 10-Q

Also, as stated in its latest quarterly report for the month of July 2023, the company's net sales are estimated at 90% internationally and only 10% locally in the United States, which I believe offer great diversification in case of a global recession.

The operations are covered in a single business segment called direct sales, which includes different product lines, which are nutritional products, probiotics, skin care products, and food production products. By the historical record of the company's recent years, the nutritional line products are those that have had the best response in the market.

To market these products internationally, USANA has a large number of subsidiaries based in the United States and strategic countries, among which we find three subsidiaries in China, one in Hong Kong, one in South Korea, Australia, New Zealand, Thailand, Mexico, France, Singapore, and Colombia among others.

Healthy Balance Sheet

As of July 1, 2023, USANA Health Sciences reported cash and cash equivalents worth $300 million, inventories of about $61 million, and prepaid expenses and other current assets close to $25 million. The total current assets stood at $387 million, and the current ratio is more than 3x, so I believe that liquidity does not seem a problem for USANA Health Sciences.

Property and equipment stood at close to $95 million, with goodwill close to $16 million, and intangible assets worth $29 million. In sum, total assets were equal to $602 million, and the asset/liability ratio appears quite solid at close to 4x-5x.

Source: 10-Q

I am really not afraid of the list of liabilities, which include accounts payable worth $9 million, other current liabilities of $104 million, and deferred tax liabilities worth $4 million.

Source: 10-Q

Other Analysts Expect Growing FCF Margin In 2024

The figures from other financial analysts are quite beneficial. They include operating margin growth in 2024, net margin growth in 2024, and positive 2024 free cash flow. More in detail, analysts are expecting 2024 net sales close to $967 million, with 2024 EBITDA of $135 million, operating margin of 10.7%, and 2024 net income close to $69.7 million. Additionally, 2024 free cash flow would stand at $81.8 million, with 2024 FCF/net sales of about 8.45%. I took into account these figures in my financial model, so I believe that readers may want to have a look at them.

Source: S&P

Further Expansion Of The Digital Sales Capabilities And Electronic Commerce Platforms Will Most Likely Bring Net Sales Growth

At present, the company seeks to carry out a growth strategy through the inorganic scale of its sales and occasionally increasing the number of active clients on an annual basis. The development points of this strategy involve expanding its digital sales capabilities and electronic commerce platforms as well as achieving an expansion in its productive capabilities with regard to food production. Another of the key factors of this strategy is to delve deeper into the Chinese markets and achieve greater proximity to its clients within this region. Under my base case scenario, I assumed that these efforts will most likely be successful, enhance sales growth, and bring economies of scale.

Given The Current State Of The Balance Sheet, Sale Of Equity Or Debt To Finance Growth Into New Markets, Or Acquisitions Will Most Likely Bring Business Growth.

The company does not really report liabilities, and the asset/liability ratio appears quite solid. Hence, I believe that sale of equity or debt will most likely not bother investors out there. If USANA uses the new financing to acquire other small competitors or expand into new countries, I believe that we may see significant net sales growth and FCF margin expansion. In this regard, management provided the following commentary in the last quarterly report.

We might also require or seek additional financing for the purpose of expanding into new markets, growing our existing markets, mergers and acquisitions, or for other reasons. Such financing may include the use of additional debt or the sale of additional equity securities. Any financing which involves the sale of equity securities or instruments that are convertible into equity securities could result in immediate and possibly significant dilution to our existing shareholders. Source: 10-Q

Affiliate Programs Launched In 2023 Will Most Likely Have a Beneficial Effect In The Coming Years, Which May Enhance Net Sales Growth

I believe that the efforts made by USANA to design new affiliate programs will most likely have a beneficial effect on future cash flow statements. Many of these new tools were launched in 2023, so perhaps clients, partners, or employees may not really know how to use them. As soon as the new tools are up and running in 2024 and 2025, I believe that we may see net sales growth.

Affiliate program, social selling tools. The Affiliate program offers a new, simplified way for individuals and customers in these markets to share, market, sell, and earn compensation for selling our products. In 2023, we will promote this program in these markets, promote and expand the digital tools for the program, and continue to evaluate offering the program in other markets. Source: 10-k

Competitors, And Risks

The nutritional products industry has high competition, and the barriers to entry are low, resulting in a large number of participants at the international and regional level as well as retail distributors, wholesalers, and those who work through digital platforms. In any case, USANA belongs to a minority group of companies with international reach, among which we find Amway, Herbalife ( HLF ), and Nu Skin ( NUS ). They have greater resources and more pronounced brand recognition.

Due to the nature of this company's business, a large part of the risks involves the legal conditions and possible changes in this regard that exist locally in the United States and in the regional markets in which it distributes its products. Particularly, as mentioned before, due to the strategy aimed at the Chinese markets, we must consider that there are a large number of legal risks due to the high regulation of commerce by the government of this country. In addition, the expansion of its clientele in this country could be an incorrect move, and may cause the company to incur serious and unnecessary operating costs.

The last factor that we must consider as a risk arising from the current growth strategy is the acquisition strategy and particularly to the two businesses acquired by USANA in 2022, which are the ones that the company is currently trying to grow. In the same way, the inability to achieve this as well as a misinterpretation of market trends could generate operational consequences in the general structure of the company.

My Financial Model

My DCF model is based on previous cash flow statements and the previous assumptions. I assumed conservative net income growth, D&A growth, no losses on sale of property and equipment, loss on impairment on other assets, and stable capex. As a result, I obtained growing FCF at a conservative path.

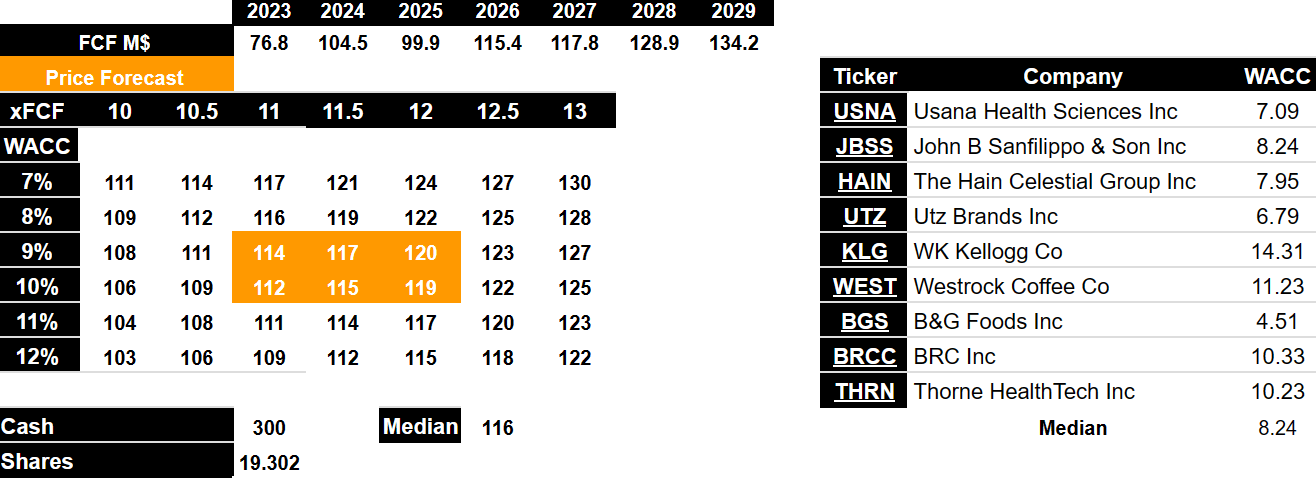

In particular, I obtained 2029 net earnings of $76 million, 2029 depreciation and amortization close to $12 million, 2029 right-of-use asset amortization worth $4 million, and equity-based compensation expenses close to $9 million.

Besides, with changes in inventories worth $171 million, changes in prepaid expenses and other assets of $1 million, and changes in accounts payable of about -$27 million, 2029 CFO would be $140 million. Finally, if we also take into consideration capex of -$7 million, 2029 FCF would be $134 million.

Source: Malak

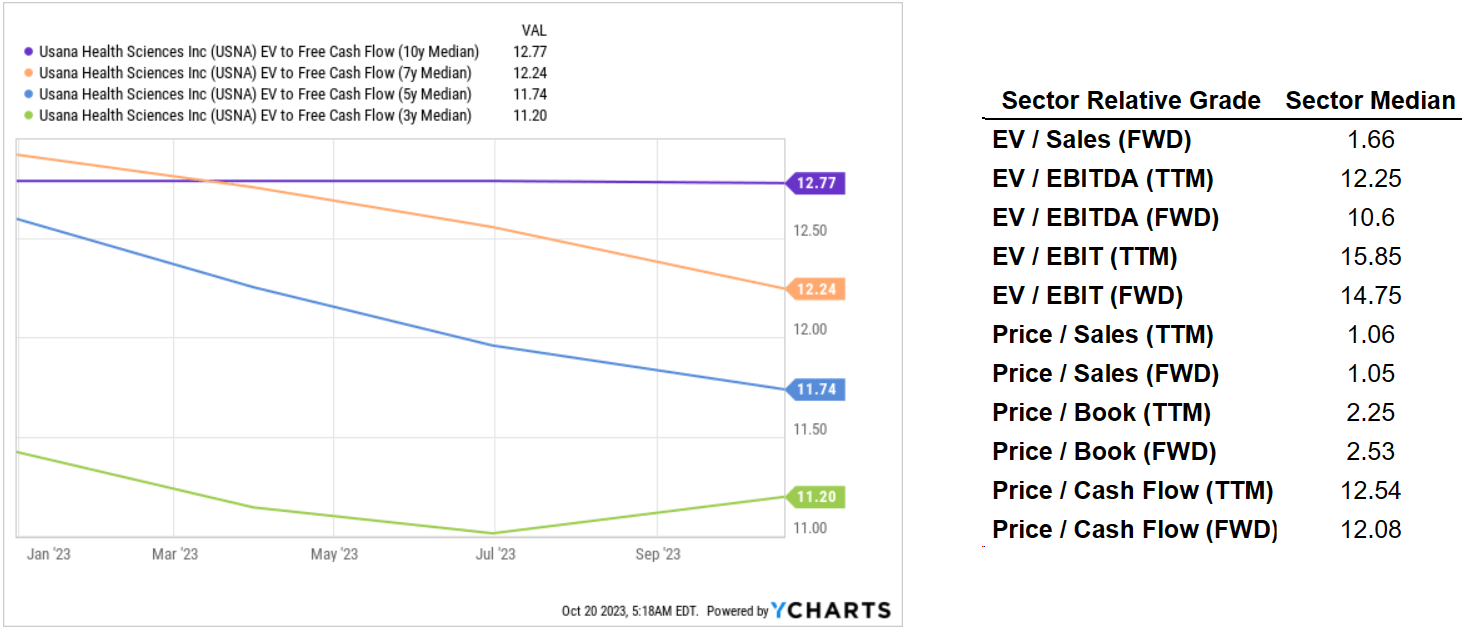

According to figures offered by Seeking Alpha and previous EV/FCF multiples, I assumed that a valuation between 10x and 13x would be conservative. Note that the EV/EBITDA in the sector is close to 10x-12x, and previous EV/10 Years Median is about 12.7x.

Source: Seeking Alpha And Ycharts

{kind=link}

Now, with a WACC of about 7%-12% and FCFs ranging from $76 million to $134 million, the implied price forecast would be close to $103-$130 with a median price of $116 per share.

{kind=link}

I also obtained a range of internal rate of return close to 11%-18% with a median close to 13%-14%. I really cannot say whether other analysts could use better or worse figures than me. However, I do not expect their figures to be far from that of mine. In my view, USANA Health Sciences does appear cheap.

Source: Malak

Conclusion

Equipped with a healthy balance sheet, and currently developing new digital tools capabilities and an affiliate program, USANA Health Sciences could show some business growth coming from 2024. In my view, the company’s financial stability will most likely allow it to sell equity or debt to finance either acquisitions or expansion into new territories. Even after suffering declines in sales driven by currency fluctuations, management proved that it can deliver somewhat stable free cash flow. With this in mind and taking into account risks from competitors or failed introduction of products, USANA Health does look undervalued.

For further details see:

USANA: New Digital Tools And Solid Balance Sheet Imply Undervaluation