USCI - USCI: Expensive Commodities ETF Better Alternatives Exist

2024-01-04 18:29:58 ET

Summary

- The United States Commodity Index Fund is an ETF that aims to replicate the SummerHaven Dynamic Commodity Index.

- The index selection methodology is based on backwardation, but it does not directly address the underlying risk factor and propensity for the commodity to rise or decrease in price.

- USCI has comparable returns to its peers but with worse risk/reward metrics and the highest expense ratio in its category.

- The selection process for the underlying risk factors occurs each month, with each contract being equally weighted.

Thesis

The United States Commodity Index Fund, LP ETF ( USCI ) is a commodities exchange-traded fund. The vehicle aims to replicate the SummerHaven Dynamic Commodity Index, which is a market index investing in commodities futures:

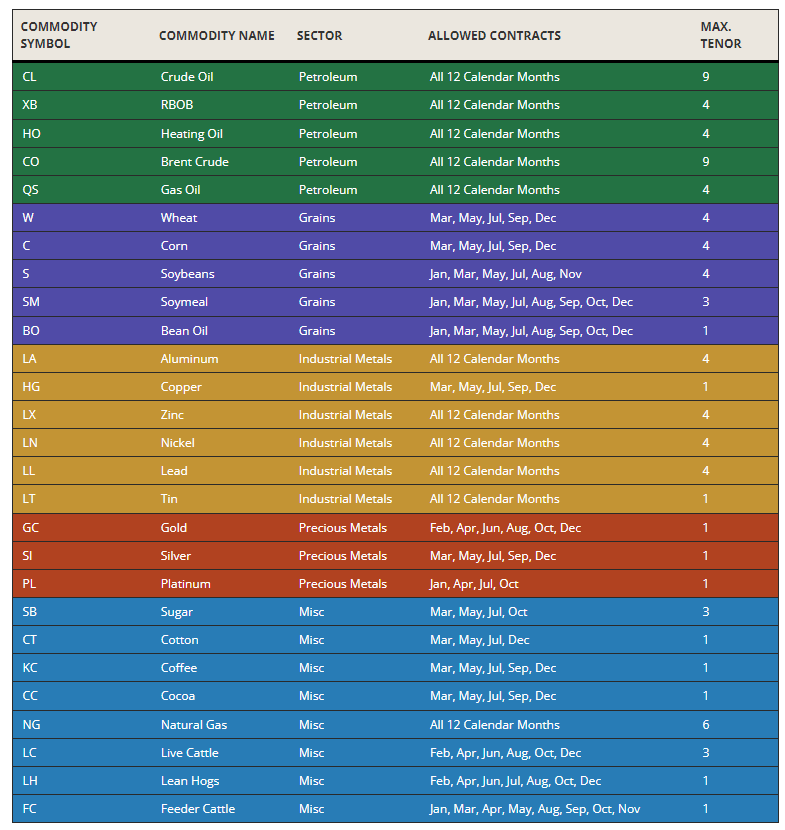

The SummerHaven Dynamic Commodity Index Total Return is an index designed to reflect the performance of a portfolio of 14 commodity futures. The index is reformulated each month from 27 possible futures contracts. The 14 selected contracts are equally weighted and represent five sectors: petroleum (e.g., crude oil, heating oil, etc.), precious metals (e.g., gold, silver, platinum), industrial metals (e.g., zinc, nickel, aluminum, copper, etc.), grains (e.g., wheat, corn, soybeans, etc.), and non-primary sector (e.g., sugar, cotton, coffee, cocoa, natural gas, live cattle, lean hogs, feeder cattle).

What is very particular about this index and hence the ETF, is the selection methodology which is based on backwardation. Backwardation references a market state when the current price, or spot price, of an underlying asset is higher than prices trading in the futures market. There are various reasons for this shape of the curve for a particular commodity, factors that can affect backwardation ranging from supply shortages to a potential recession.

What is important to keep in mind though is that the backwardation methodology works towards addressing the negative price action from rolling futures, thus helping the fund with its carry. When the fund rolls into a new future contract, when in backwardation, it will do so at a more advantageous price. The fallacy with this methodology though is that it does not address the underlying risk factor and propensity for the underlying commodity to rise or decrease in price, in our view.

The fund's historic performance falls within the same one exhibited by its peers, but with worse risk/reward metrics. Furthermore, USCI has the highest expense ratio from the analyzed population, with an expense ratio that rivals the more structured CEF vehicles.

Comparable returns, high expense ratio

The fund has a longer-term total return comparable with its peer group:

As we can see from the above table courtesy of YCharts, USCI does not outperform its peer group on a 5-year time-frame, and in fact, lags the low volatility Direxion Auspice Broad Commodity Strategy ETF ( COM ) and the better-known peer Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF ( PDBC ).

From a risk metrics perspective, USCI also lags:

Risk Metrics (Author)

We can see the ETF exposing the largest maximum drawdown from the cohort on the contemplated time frame, all while clipping an expense ratio which is almost double the one charged by PDBC. Such a high expense ratio, which is comparable with the CEF space, should only be charged by an ETF which employs an active strategy that outperforms. This is not the case here. In fact, USCI is the riskiest investment from the cohort, with the largest maximum drawdown and the lowest Sharpe ratio. Why would a retail investor want to pay a high fee for a poor risk-adjusted performance?

For a retail investor who does not like volatility, COM is the best choice, a fund which we covered here . PDBC on the other hand is an institutional investor darling, with a $4.6 billion AUM and ample liquidity. We covered PDBC here .

While USCI does optimize the rolling strategy for a futures fund via its systematic backwardation approach, its longer-term performance and analytics do not justify its fees and investing in this name versus its competitors.

Index construction

The SummerHaven Dynamic Commodity Index is an interesting one, aiming to capture almost the entire commodities universe via its composition:

{kind=link}

27 contracts are initially contemplated, with SDCI selecting only 14, taking into account the ones with the greatest backwardation. The selection process occurs each month, with each contract being equally weighted and representing the five sectors outlined above. We find it strange that the index quants have included Natural Gas in the 'Other' category rather than include it with the petroleum products, since natural gas is a by-product of oil extraction, and there is a fairly good long-term correlation between the prices of oil and natural gas, although shorter time-frame divergences can indeed occur.

The index requires at least one component from each of the four commodity sectors as outlined in the above table ('Precious Metals', 'Industrial Metals', 'Petroleum', and 'Grains'). If a sector isn't represented after selecting the 14 commodities, the commodity with the highest backwardation among the commodities of the omitted sector is substituted for the commodity with the lowest backwardation among the 14 selected commodities. By taking this approach the index composition does not consistently exclude any of the large four sectors.

Commodities are bottoming

From an allocation standpoint there are several indicators that are pointing toward a bottoming process in commodities:

Commodities vs Bonds (BofA)

The investor community is severely underweight commodities on a historic time frame and when compared to the Commodities/Bonds ratio. Peak pessimism and allocations usually mark the beginning of a bottoming process.

From a fundamental standpoint, if the base case scenario is a soft landing and a significant amount of Fed cuts in 2024, then why is the commodities market pricing in a recession? If a true soft landing scenario does materialize then commodities should follow stocks higher, and the investor community will allocate more capital to this sector. There is currently a disconnect between allocations to commodities and allocations to equities that will need to be solved.

Conclusion

USCI is a commodities exchange-traded fund. The vehicle aims to replicate the SummerHaven Dynamic Commodity Index, which is a rules-based index that chooses the contracts with the highest backwardation. While this methodology helps to mitigate the futures roll effect, we do not think it is an accurate predictor for the actual performance in the underlying risk factor, with USCI having performed in line with its peers from a total return perspective. What is surprising though is that USCI has the worst risk/reward analytics from the cohort and an expense ratio which is almost double the one exhibited by PDBC. While we are overall bullish commodities here, we do not think USCI is the appropriate vehicle to allocate new capital. Existing shareholders are best served to hold, while new money would do well to look at COM or PDBC.

For further details see:

USCI: Expensive Commodities ETF, Better Alternatives Exist