USDP - USD Partners: Distributions Could Be Suspended In The Coming Months

Summary

- Despite what seemed like a positive start to 2022, it was not coming together as expected for USD Partners following the second quarter.

- They saw important contracts end without having already lined up new ones, thereby leaving a sizeable hole in their financial performance.

- On the surface, the third quarter actually appeared solid but this was due to very large derivative settlements that effectively saved the day.

- Without this boost, they cannot afford their distributions and risk breaching their credit facility covenant following the end of 2022.

- Most disappointingly, there was seemingly no progress in securing new contracts during the third quarter and thus I believe that downgrading to a sell rating is now appropriate.

Introduction

Early in 2022, it appeared USD Partners ( USDP ) would see an uneventful year but disappointingly, it was not coming together as expected following the second quarter with contracts ending without new ones already lined up, as my previous article discussed. After their seemingly non-existent progress during the third quarter, even more disappointingly, it now appears their distributions could be suspended in the coming months, as discussed within this follow-up analysis.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

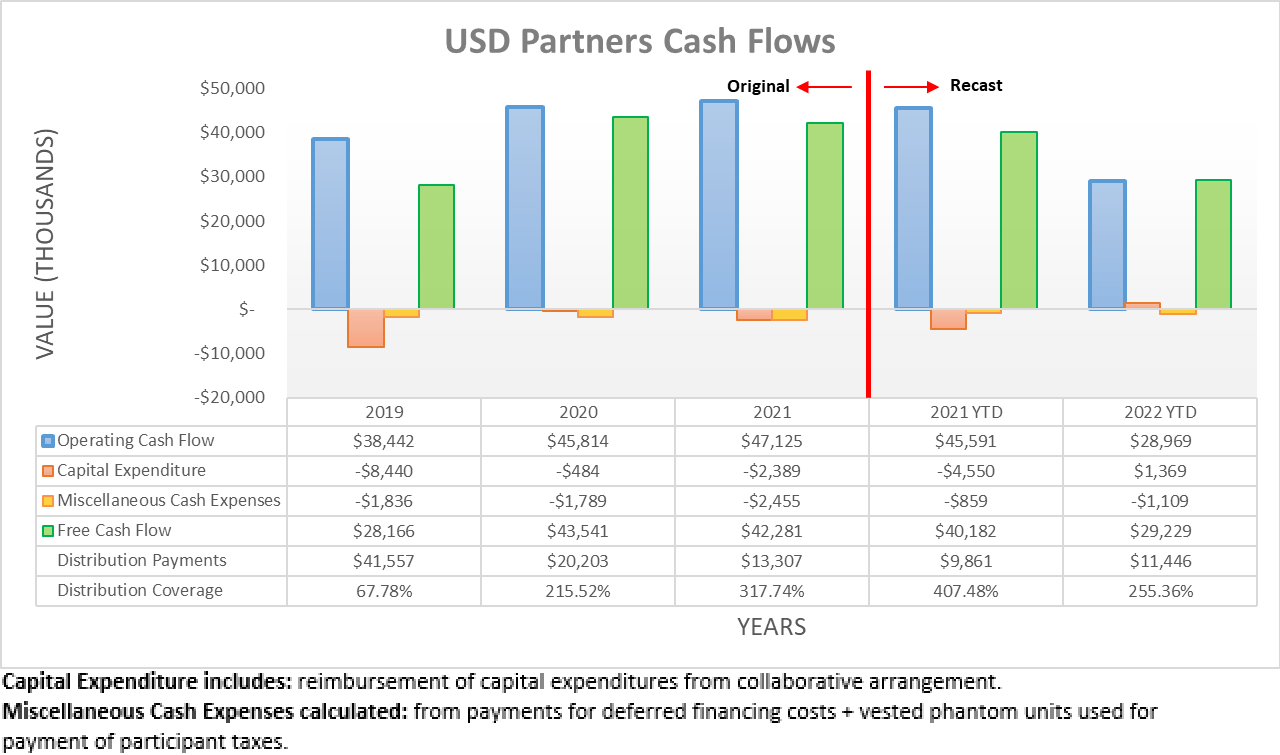

As a reminder, after their Hardisty South Terminal acquisition during the second quarter of 2022, their financial statements were recast as the acquisition represented a business combination between entities under common control. When presenting data within this analysis, their historical results for full-year 2021 and earlier have been left original with the one exception of cash flow performance graph, whereby their results for the first nine months of 2021 were recast to aid the comparison with their latest results.

Following their weaker-than-expected cash flow performance during the second quarter of 2022, it could be said that hopes were not too high upon opening their results for the third quarter. Although to my initial surprise, their operating cash flow climbed to $29m during the first nine months, up from only a mere $15.4m during the first half. Whilst far from a stellar result compared to the $45.6m they generated during the first nine months of 2021, it nevertheless appeared they were back on track, at least at first.

{kind=link}

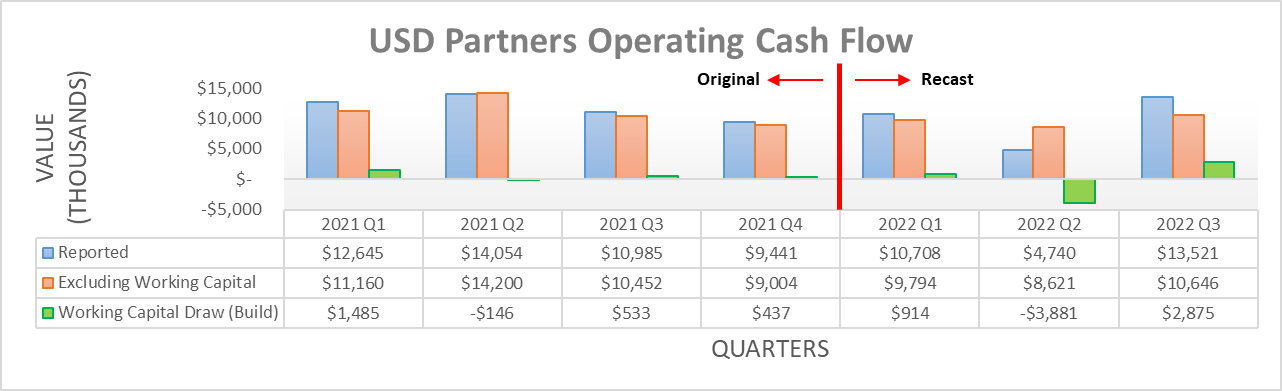

When viewed on a quarterly basis, the third quarter of 2022 actually appears to have been surprisingly good with their operating cash flow of $13.5m landing at the highest level since at least the beginning of 2021. Admittedly, this was helped along by a working capital draw, although their underlying result excluding this temporary boost was still decent at $10.6m. Whilst positive, it seemed quite odd considering their revenue was down almost 40% year-on-year during the third quarter to only $21.5m on the back of several important contracts ending during the second quarter, as discussed within my previous analysis.

After digging into their cash flow statements, the reason for this becomes evident and sadly, it is not good news for unitholders. During the third quarter of 2022, they closed out a sizeable portion of interest rate swaps, thereby seeing a $7.6m boost from derivative settlements, as interest rates have increased noticeably since initiating their contracts. If removed from their operating cash flow that excludes their working capital draw of $10.6m, it leaves what I would call their core operating cash flow at only a tiny $3m. When looking ahead into the fourth quarter, it seems unitholders can once again expect this boost as they closed out their existing interest rate swaps, as per the commentary from management included below.

"Subsequent to the quarter end, on October 12, the Partnership settled its existing interest rate swap for proceeds of approximately $9 million. The Partnership plans to use the proceeds from this settlement to pay down outstanding debt on a senior secured credit facility and fund ongoing working capital needs."

- USD Partners Q3 2022 Conference Call.

Whilst this will help once again, it does not solve anything and merely kicks the can down the road because they cannot hope to possibly fund their distribution payments without this soon-to-be-gone boost. To this point, the third quarter of 2022 saw distribution payments of $4.3m, which is well above their accompanying core operating cash flow of $3m and thus without either their working capital draw and derivative settlement, they would have needed debt funding, thereby leaving their coverage very weak even before considering their capital expenditure.

Quite possibly most disappointing of everything, their progress securing new contracts was seemingly non-existent during the third quarter of 2022. Amidst their accompanying conference call, an analyst actually pointed out that regarding their contracts "some of the language today was very, very similar on the last call", to which their response effectively confirmed, as per the commentary from management included below.

"So, regarding your first point, the discussion appears to be similar to previous calls, it is, but it is based on mental models that are consistent as to when and why the marketplace will demand our assets. And it has to do simply with the macro story and when the Canadian supply reveals itself and when that Canadian supply is sufficient to be greater than the pipe egress. So we can't predict that from a exact timing standpoint. That's impossible to do."

- USD Partners Q3 2022 Conference Call (previously linked) .

In my eyes, their commentary did not inspire confidence that new contracts were on the horizon or that any tangible progress was made during the third quarter of 2022. Rather, it seems they are taking a wait-and-see approach, which unfortunately, leaves unitholders guessing and thus as a result, opens the door for a distribution cut given their very weak coverage. Furthermore, it is particularly concerning for a long-term perspective that even these very strong near triple-digit oil prices have still not created sufficient demand for their assets. Whilst already negative, this situation actually carries even more important implications for their financial position, which could see their distributions suspended, or an even worse outcome if left unresolved.

{kind=link}

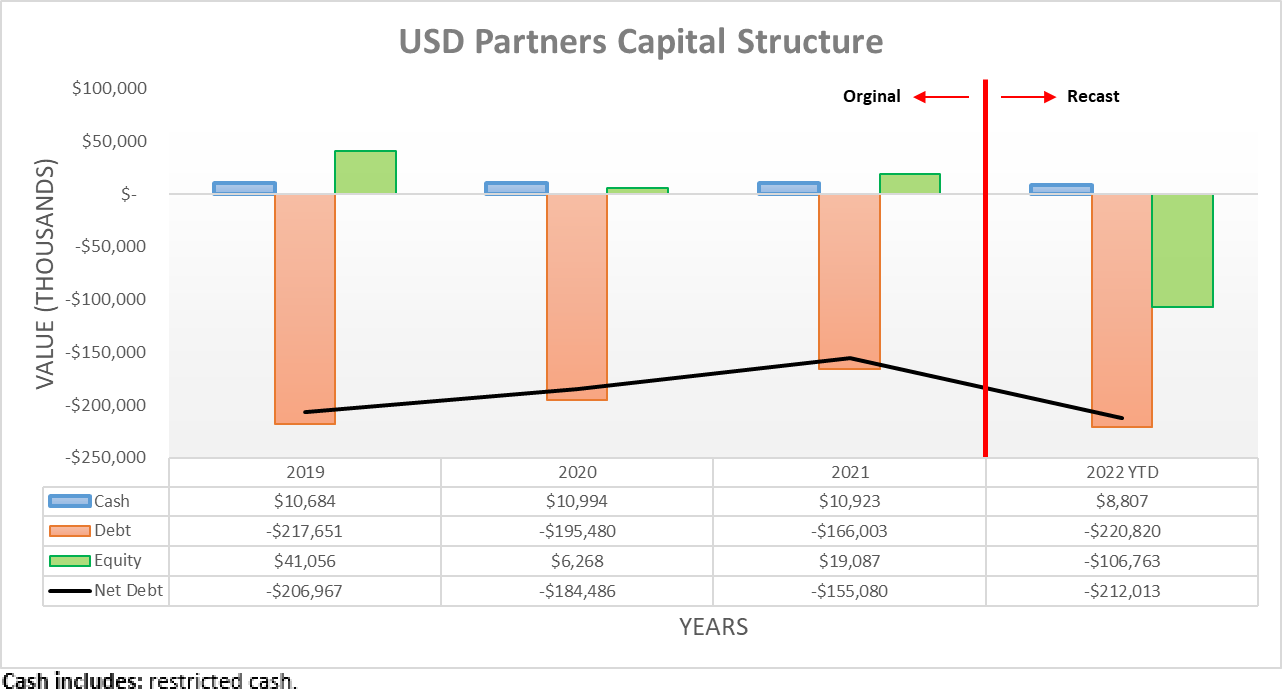

After seeing their net debt spike to $222.3m during the second quarter of 2022 on the back of their Hardisty South Terminal acquisition, it dropped slightly during the third quarter to $212m. Whilst positive, it was obviously due to their combined working capital draw and derivative settlement, which are not fundamentally driven nor repeatable perpetually into the future.

When conducting the previous analysis, it was expected their net debt would resume its downward trend as seen during 2020 and 2021, although this was contingent upon new contracts and given the seemingly non-existent progress, this is no longer the case. In light of this situation, once stripping out the cash boost from their derivative settlements, it actually now appears they are going to be funding their distribution payments with the use of debt. Whilst they appear to have bought time during the fourth quarter of 2022 by settling another $9m of derivatives, this is the last of them and thus heading into 2023, their net debt will begin marching higher, unless they quickly line up new contracts.

{kind=link}

The prospect of seeing their net debt climb even higher in 2023 is particularly concerning, firstly because their leverage is already very high, as primarily evidenced by their net debt-to-EBITDA of 5.95 and net debt-to-operating cash flow of 5.47 both sitting above the applicable threshold of 5.01 following the third quarter of 2022. Unsurprisingly, the former is noticeably higher than its previous result of 5.10 following the second quarter as their core financial performance deteriorated. Whilst the latter is modestly lower than its previous result of 6.03, this is simply due to their operating cash flow including the boost from their derivative settlement.

{kind=link}

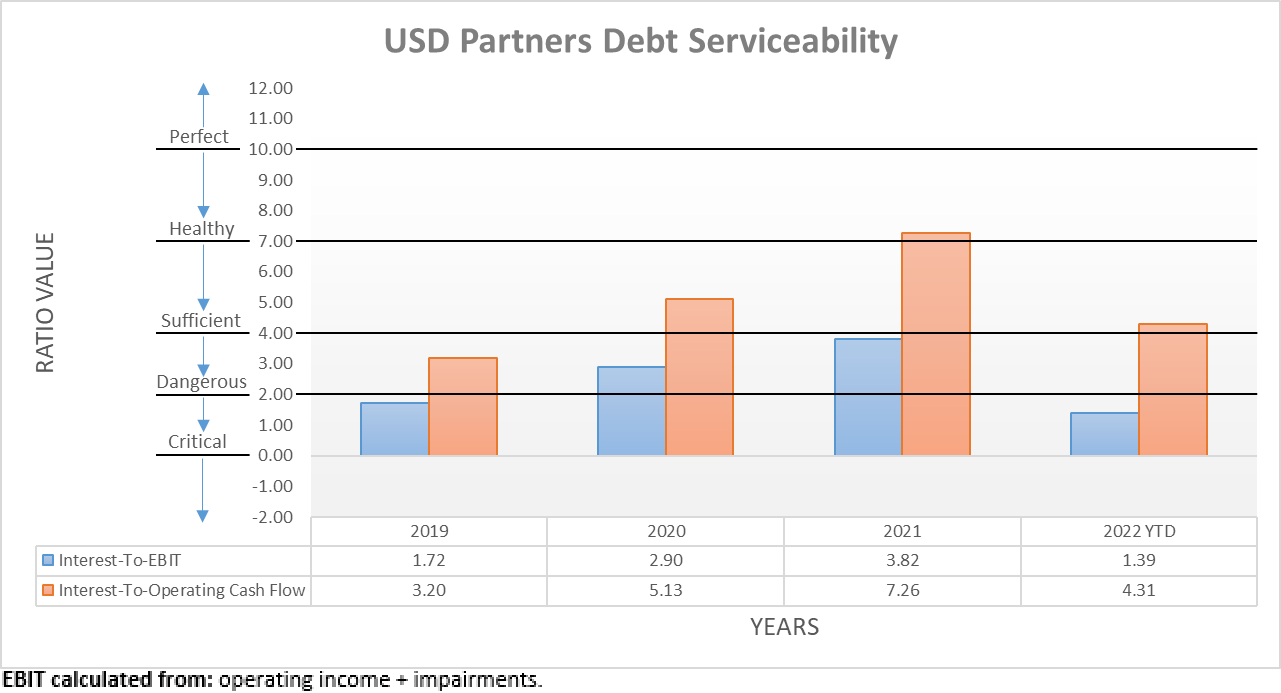

Apart from the concerns surrounding its impacts to their very high leverage, more debt is the last thing they need from a debt serviceability standpoint, which is becoming increasingly important to consider as interest rates climb rapidly. Following the third quarter of 2022, their interest coverage was already only a dangerous 1.39 when compared against their accrual-based EBIT. If compared against their cash-based operating cash flow, its result was higher at a healthy 4.31 but similar to their leverage, it was due to the boost of their derivative settlement and thus should be ignored.

{kind=link}

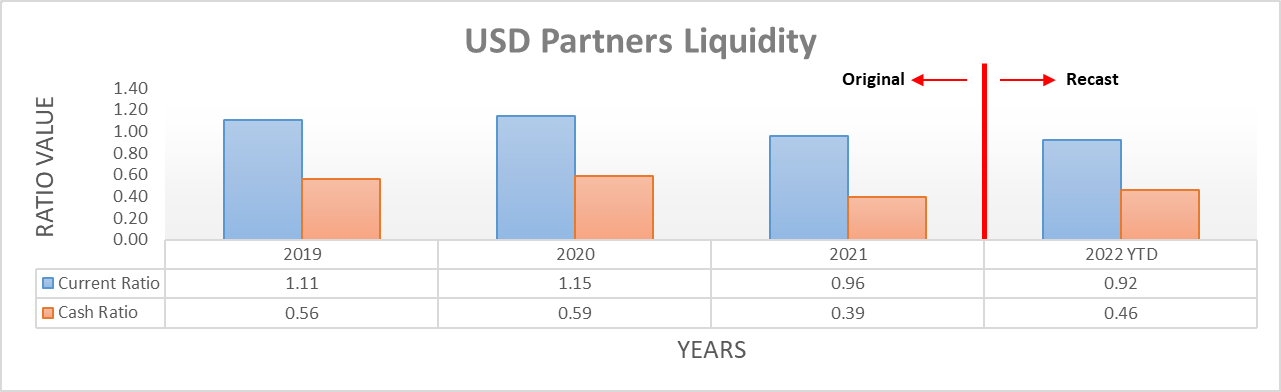

Whilst the prospects of even higher leverage and worse debt serviceability are concerning, even more critical is the impact to their liquidity, as it causes far more acute problems. On the surface, their respective current and cash ratios of 0.92 and 0.46 following the third quarter of 2022 are strong, as was the case following the second quarter that ended with respective results of 1.03 and 0.30. Although as readers of my previous article may recall, their credit facility sees a covenant whereby the limit for their leverage creates a pressing short-term hurdle, as per the quote included below.

"As a result, the Partnership's available borrowings is limited to 5.0 times its 12-month trailing consolidated EBITDA through December 31, 2022, at which point it will revert back to 4.5 times the Partnership's 12-month trailing consolidated EBITDA."

- USD Partners Third Quarter Of 2022 Results Announcement .

Following the third quarter of 2022, their total debt is $220.8m and thus requires a trailing twelve-month EBITDA of $50m at the barest minimum to stay beneath their leverage limit of 4.50 following the end of 2022. Their adjusted EBITDA was $12.3m during the third quarter, which annualizes to $49.2m and thus obviously beneath this requirement, as per their previously linked third quarter of 2022 results announcement. Since they are seemingly struggling to secure new contracts, it is quite difficult to imagine their EBITDA will materially improve during the coming quarters, thereby leaving their liquidity very weak as they risk a crisis requiring relief from their lenders.

Whilst this already leaves their outlook dubious, their adjusted EBITDA is calculated with their operating cash flow as a starting point, as per their previously linked third quarter of 2022 results announcement. This means it includes the boost from their derivative settlement and thus it was also artificially boosted by $7.6m during the third quarter of 2022. Admittedly, it appears the fourth quarter will see another $9m boost but looking into 2023, this will not continue. This leaves them skating on very thin ice as their EBITDA risks falling off a proverbial cliff in less than two months, unless they quickly secure new contracts but given management could not even provide a timeline, this does not appear probable.

It should be remembered that credit facility covenants are very serious and cannot be breached, at least not without prior approval from lenders. Since they are seemingly struggling to contract out a sizeable portion of their assets, I would be surprised to see lenders being lenient. If they go cap in hand asking for relief, it would not be surprising to see their distributions suspended, especially given their cash flow issues once excluding their derivative settlements. Worryingly, this is actually the better of the possible outcomes, as a highly dilutive equity issuance is another far worse path, or failing everything, breaching a covenant can also be a ticket to bankruptcy court.

As a side note for the purpose of clarity, their approach to calculating EBITDA differs from mine that is utilized across all articles to enhance comparability, which is detailed beneath the leverage graph included above. It should also be remembered that metrics such as EBITDA are non-GAAP, thereby meaning they can be calculated in different ways and as such, there is no one-size fits all.

Conclusion

To give credit where due, they played their hand skilfully by settling these derivatives to plug their cash flow gap during the third and fourth quarters of 2022, although this cannot last forever. The seemingly non-existent progress securing new contracts is concerning, especially given the otherwise very strong operating conditions within the oil industry. I do not take this lightly but as it stands right now, they are skating on very thin ice as they could breach their credit facility leverage covenant following the end of 2022. Not only does this leave their distributions very risky, it also risks a liquidity crisis that opens a dangerous Pandora's Box and thus, I believe that downgrading my hold rating to a sell rating is now appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from USD Partners' SEC filings , all calculated figures were performed by the author.

For further details see:

USD Partners: Distributions Could Be Suspended In The Coming Months