USDP - USD Partners: I Fear Something Bad Might Be Coming

Summary

- USD Partners suffered a considerable setback during 2022 as several important contracts expired with no tangible progress replacing these so far.

- Whilst their operating cash flow looked surprisingly good during the fourth quarter of 2022, this was due to derivative settlements.

- These are now mostly done and thus, I expect their upcoming operating cash flow to fall off a cliff with a distribution cut or possibly even suspension looking likely.

- Even worse, they need to refinance the entirety of their debt before November or face bankruptcy.

- Either way, I fear something bad might be coming and thus, I believe that maintaining my sell rating is appropriate.

Introduction

Following the seemingly non-existent progress USD Partners ( USDP ) was making lining up new contracts back in late 2022, it appeared their distributions could be suspended, as my previous article warned. Whilst they subsequently surprised by maintaining their distributions, their fundamentals continued deteriorating and I see various warning signs flashing and thus as a result, I fear something bad might be coming.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

As a reminder, after their Hardisty South Terminal acquisition during the second quarter of 2022, their financial statements were recast as the acquisition represented a business combination between entities under common control. When presenting data within this analysis, their historical results for 2021 and earlier have been left original, whereas their results for 2022 are obviously recast.

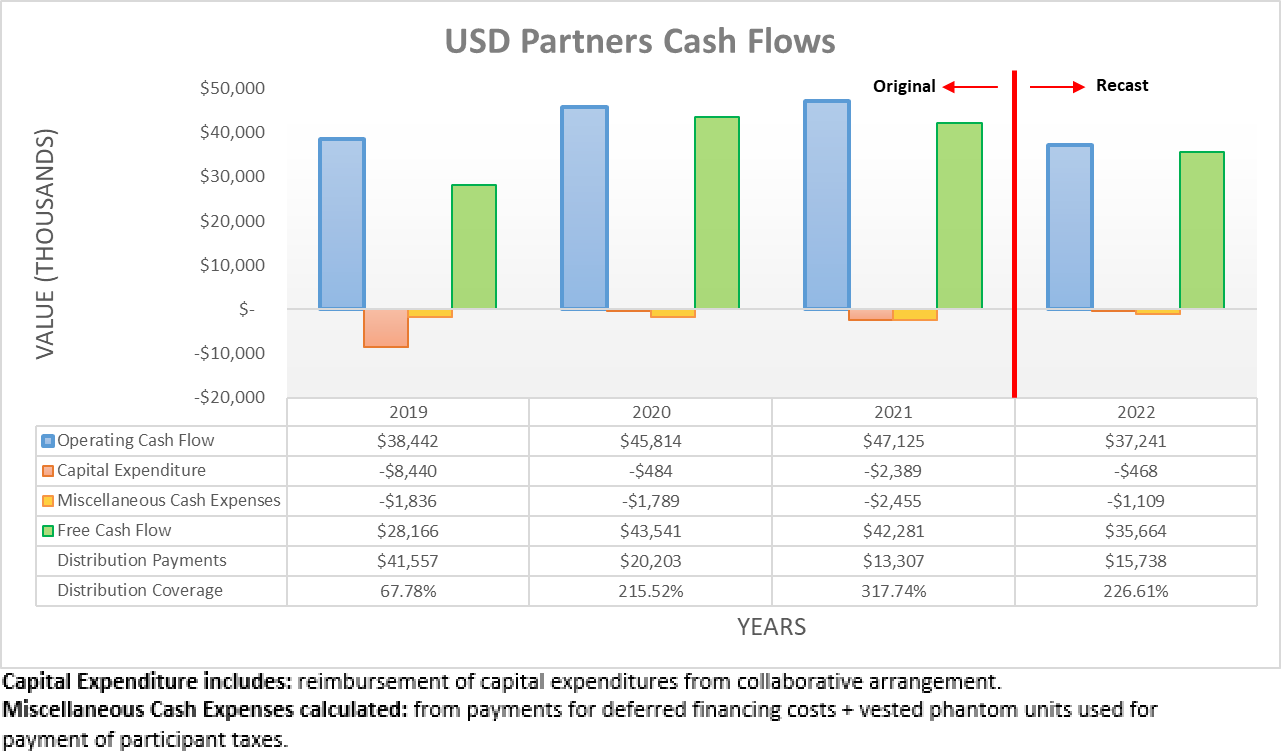

In the lead-up to the release of results for the fourth quarter of 2022, their cash flow performance was high on the list of priorities to review following my previous analysis flagging their cash generation as an area of concern. Once opened, it showed their operating cash flow ended the year at $37.2m and thus modestly above the $29m they generated during the first nine months.

{kind=link}

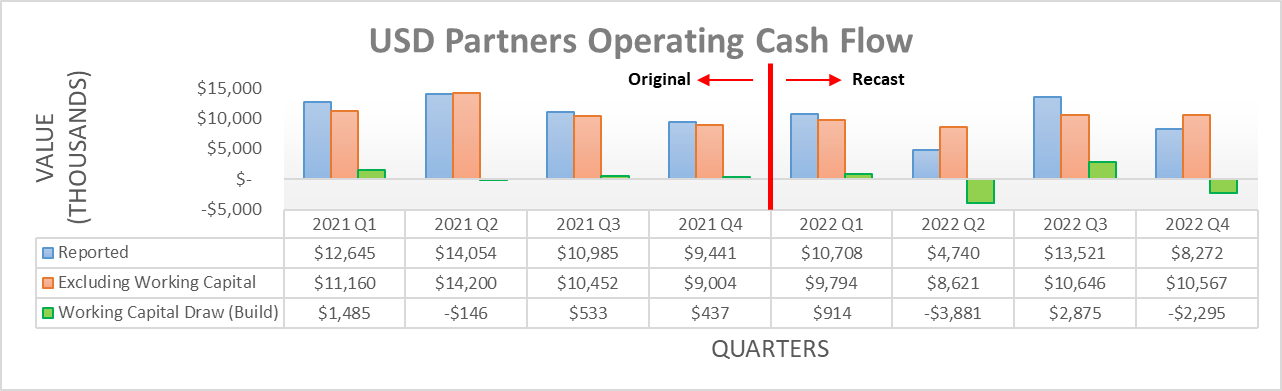

If viewing their operating cash flow on a quarterly basis and excluding working capital movements, it appears surprisingly good with an underlying result of $10.6m during the fourth quarter of 2022, which is either better or if not, roughly on par with most of their previous results in recent history since at least the beginning of 2021. That said, as readers of my previous analysis may recall, there is not good news for unitholders lurking deeper beneath the surface.

Similar to the third quarter of 2022, their operating cash flow during the fourth quarter saw a sizeable portion of interest rate swaps closed out. As a result, this saw another $8.8m boost via the settlement of derivative contracts recorded on their cash flow statement. If removed from their underlying operating cash flow of $10.6m, it leaves what I would call their core operating cash flow at only a tiny $1.8m and thus even less than the $3m they saw during the third quarter, as per my previously linked article. Very worryingly, this shows their assets are struggling to generate cash following the loss of important contracts as outlined within my earlier article . Despite it now being around six months later, they have still made no tangible signs of progress replacing these contracts with only generalized statements, as per the commentary from management included below.

“With Canadian storage utilization levels currently at the high end of the historical averages and the industry’s current expectations around growth in Canadian oil sands production in 2023 and 2024, we are focused on renewing, extending, or replacing agreements that expired during 2022 and those that are set to expire this year.”

-USDP Partners Fourth Quarter Of 2022 Results Announcement .

Whilst these contracts are still front and center on their minds, their language does not indicate anything is about to change with no tangible signs of new contracts forthcoming. If anything, it is actually looking worse as they mentioned more are set to expire during 2023 and thus if the ones from 2022 are proving difficult to replace, the last thing they need is even more spare capacity idled.

The settlement of derivative contracts essentially saved the day thus far, although they appear to be effectively running out. These are accounted for within their current and non-current assets on their balance sheet, which are collectively down to only $3.3m following the fourth quarter of 2022. Unless something changes quickly, I expect to see their operating cash flow fall off a cliff during the first and second quarters of 2023, thereby making a large distribution cut very likely, if not even a suspension given their subsequently discussed liquidity pressures that already saw their sponsor elect to forego their latest quarterly distribution, as per the commentary from management included below.

“ …in order to support the Partnership’s current liquidity position during this recontracting cycle, our Sponsor decided to waive its right to the fourth quarter distribution on its 17.3 million units without impacting the distribution to the remaining unitholders…”

-USDP Partners Fourth Quarter Of 2022 Results Announcement (previously linked) .

It is rare to see a sponsor electing to waive their right to distributions, as a significant part of the poor reputation that Masted Limited Partnerships endure stems from the actions of their sponsors that favor themselves at the expense of minority unitholders. Whilst only my subjective view, I nevertheless feel the way they speak about their distributions is lining up a cut or suspension for all of their unitholders quite soon, as per the commentary from management included below.

“The Partnership’s board determined to keep the distribution unchanged from the prior quarter and to evaluate the distribution on a quarterly basis going forward and will take into consideration updated commercial progress, including the Partnership’s ability to renew, extend or replace its customer agreements at the Hardisty and Stroud Terminals, current market conditions, and management’s expectations regarding future performance.”

-USDP Partners Fourth Quarter Of 2022 Results Announcement (previously linked) .

{kind=link}

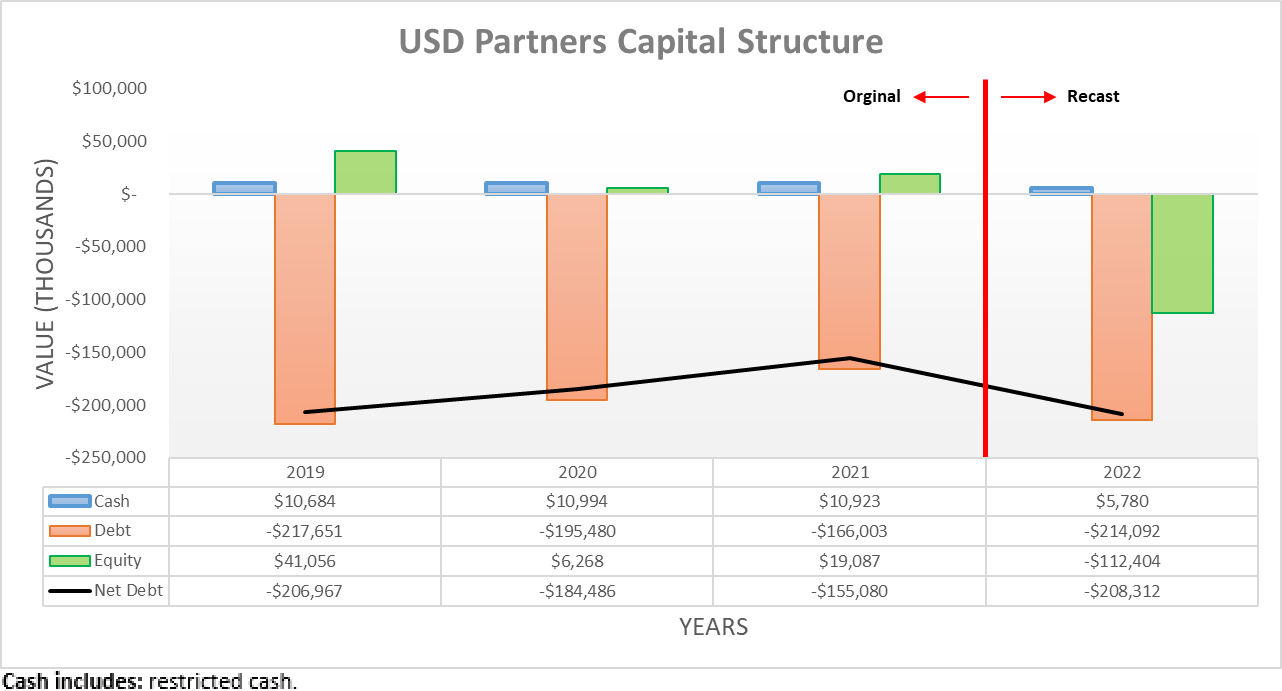

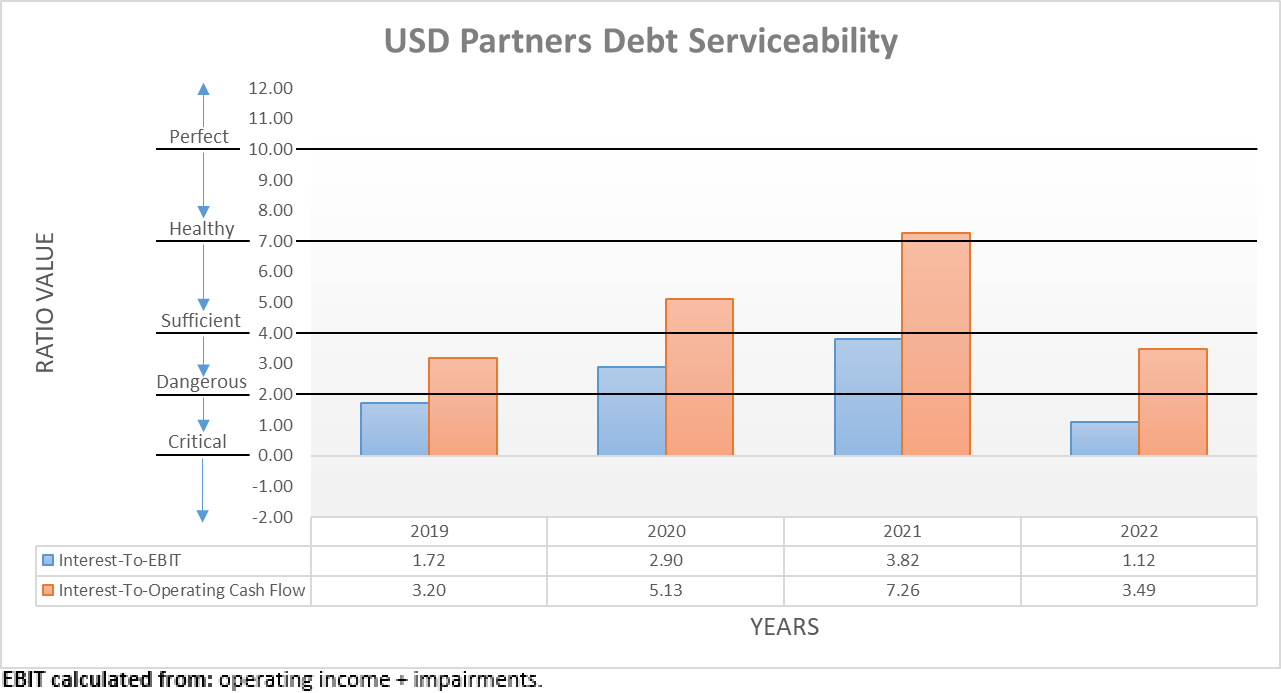

Thanks to the boost from their derivative settlements during the fourth quarter of 2022, their net debt dropped slightly to $208.3m versus its previous level of $212m following the third quarter. Since they appear to be effectively out of derivatives, this means their net debt is very likely to begin climbing during 2023, unless they quickly make progress on new contracts or suspend their distributions, the latter of which seems far more likely right now. Since there was only a small change on this front since conducting the previous analysis, it would be redundant to reassess their leverage or debt serviceability in detail, especially as neither are the primary topics right now.

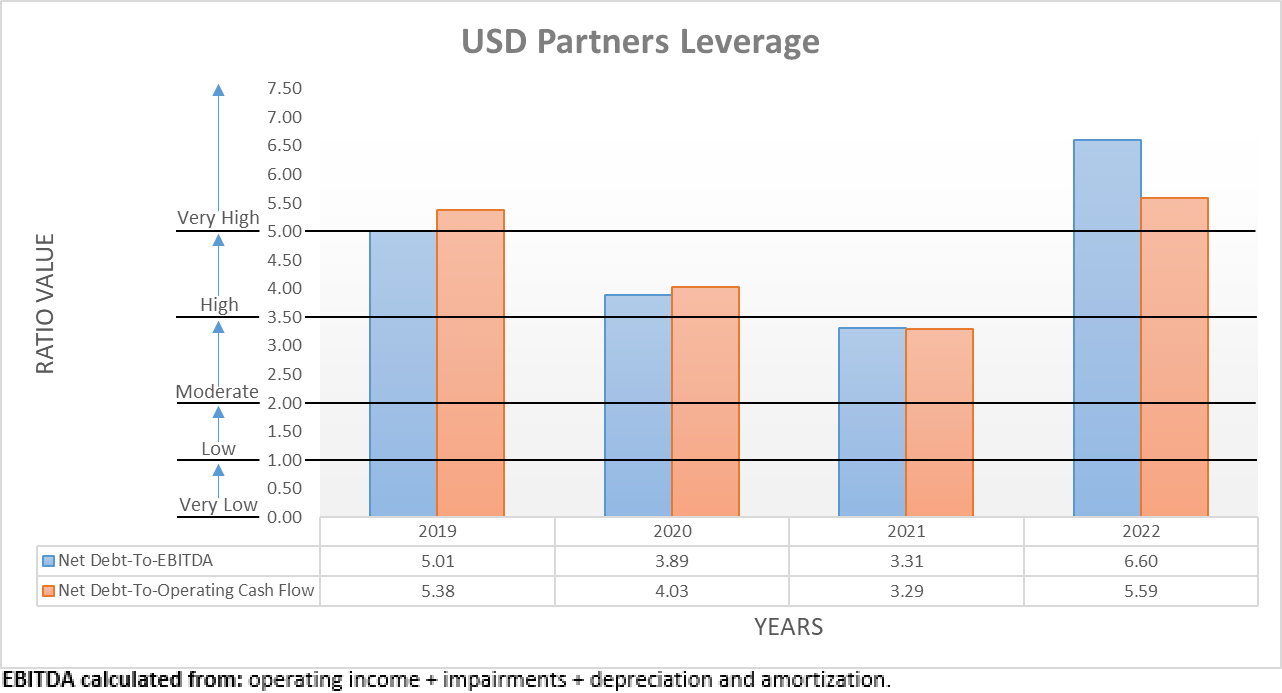

The two relevant graphs are still included below to provide context for any new readers, which shows their leverage is once again very high, quite unsurprisingly. To this point, their net debt-to-EBITDA of 6.60 and net debt-to-operating cash flow of 5.59 are both materially above the applicable threshold of 5.01. Concurrently, their debt serviceability remains dangerous with interest coverage of only 1.12 when compared against their EBIT and whilst a comparison against their operating cash flow sees a sufficient result of 3.49, I prefer to judge on the worse side. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

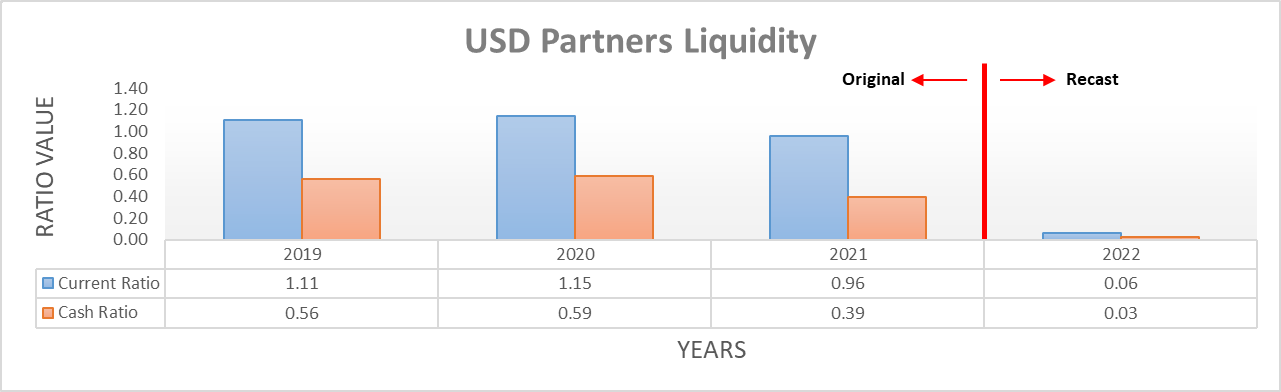

When conducting their previous analysis, their very weak liquidity was also flagged as an area of concern and thus even more critical than other issues. This is now more easily evident following the fourth quarter of 2022 with their current and cash ratios both plunging to respective results of 0.06 and 0.03 versus their previous respective results of 0.92 and 0.46 following the third quarter, which stems from their credit facility maturing in November 2023 and thus as a result, now being accounted for within their current liabilities. Worryingly, this holds the entirety of their $214.1m of debt and therefore absent of refinancing, they have no choice but to file for bankruptcy since repayment is out of the question, nor an equity issuance given their market capitalization of approximately $113m is far too low to facilitate such a bold move. At least one good development was their lenders waiving their need to comply with their credit facility covenant and thus removing the more immediate threat to their ability to remain a going concern, as per the commentary from management included below.

“In January 2023, the Partnership entered into an amendment to its senior secured credit facility. Among other things, the amendment provides the Partnership with relief from compliance with the senior secured credit facility’s maximum consolidated leverage ratio and minimum consolidated interest coverage ratio through the senior secured credit facility’s current maturity date…”

-USDP Partners Fourth Quarter Of 2022 Results Announcement (previously linked) .

Conclusion

I am not necessarily saying that bankruptcy will happen but at the same time, I must say that the outlook is very concerning and sadly, it is a real possibility. Not only do they face the entirety of their debt maturing in 2023 but just as bad, their assets are also struggling to generate cash following the loss of important contracts in 2022, which they have seemingly made no tangible progress replacing after more than half a year, not to mention they see more contracts ending during 2023.

Even if their lenders are friendly despite their poor fundamentals and refinance their credit facility without imposing onerous terms, I struggle to see their distributions surviving much into the future past this point, simply due to the lack of cash generation without derivative settlements. This means that either way, I fear something bad might be coming and thus, I believe that maintaining my sell rating on USDP stock is appropriate despite their unit price sliding lower in recent weeks.

Notes: Unless specified otherwise, all figures in this article were taken from USD Partners’ SEC filings , all calculated figures were performed by the author.

For further details see:

USD Partners: I Fear Something Bad Might Be Coming