USFR - USFR: Adjusting Our Outlook

Summary

- Floating rate securities have rewarded investors; not only with higher income but by also protecting them from losses on their invested capital.

- Interest rates are looking like they are nearing a top, at least in the short-term.

- It might be time for investors to redeploy some of their USFR holdings back out the curve and look at longer duration funds.

In late May 2022 we highlighted why we thought investors should pay more attention to their cash holdings and how to deploy their cash in a dramatically changing rate environment. For nearly a decade many had just grown comfortable putting their cash in short to intermediate duration bond funds and ignoring money market funds and the risk that they were exposing their cash by ignoring duration and duration/interest rate risk. We revisited the idea in late September 2022 and highlighted how the WisdomTree Floating Rate Treasury ETF ( USFR ) had dramatically increased its monthly payout, and explained how we thought that there was further room for the payout to increase.

Today, investors are getting $0.183/share monthly (as of December 2022) which is well above the $0.029/share each month that they were receiving back in May 2022. Even more important, the units have maintained their NAV and provided stability - much like we believed they would.

So What Are Our Thoughts Today?

We are less bullish on the WisdomTree Floating Rate Treasury ETF these days, and have adjusted our strategy to take this into account. We still really like the fund for portfolios' cash/cash equivalents allocations but no longer believe it is the best bet for the short duration allocations within one's portfolio.

Markets and the Fed are taking a breather. We should know in a month or two exactly how much more work is required on the Fed's side which will then tell us whether rates head lower, trend sideways for a while longer, or head higher. (Bloomberg)

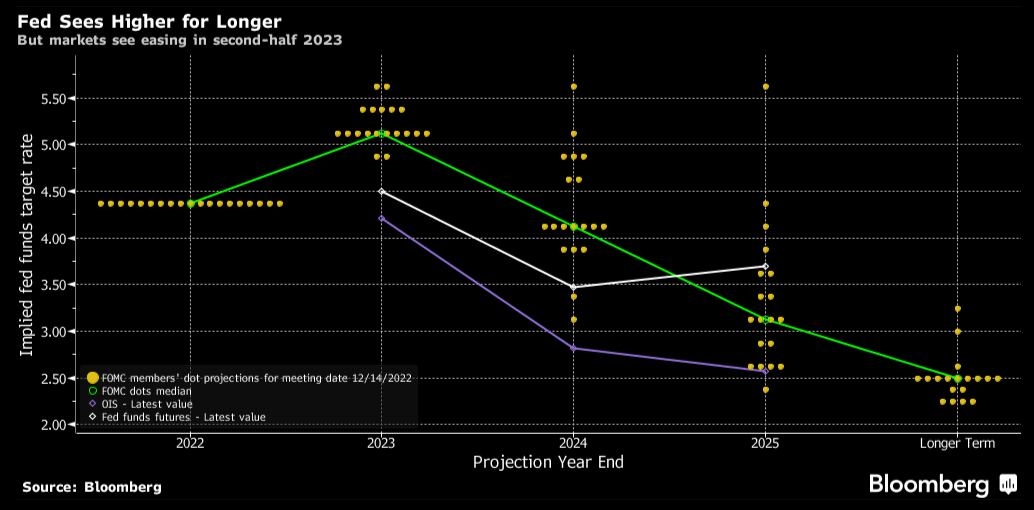

Simply put, it seems less likely that one would be 'fighting the Fed' by venturing further out the yield curve now as the market currently seems to be questioning the Fed's posturing and talking points as it relates to further rate hikes. Yes, there will be further rate hikes, but based off of future rates it certainly seems that the market expects smaller rate hikes in 2023 and even a move to cut rates later in the year. The chart above shows this change in market sentiment occurring in late October and early November 2022. Since then, rates have trended lower, and importantly across various maturity ranges on the yield curve, as inflation data has cooled a bit and more and more economic data seems to indicate that the risk of recession is only increasing.

It seems that the market and the Fed both agree that rates are going lower. The only question is the timing of such a move and how quickly and how sharply the Fed will adjust. (Bloomberg)

{kind=link}

Rates are headed lower, even the Fed acknowledges this when various members speak and when they issue all members' expectations on rates via the 'dot plot'. Sure, a spike in inflation could alter these plans but the market and the Federal Reserve both seem to agree that rates in 2024 will be lower than rates in 2023 and that is why we think that investors might be well served to begin rotating, however gradually, into longer duration fixed income instruments.

The WisdomTree Floating Rate Treasury ETF should continue to pay out a decent yield as the Fed continues to raise rates, but we do get the feeling that we are closer to the ceiling on how much higher rates can reset to than some may believe. So while short-term rates can continue higher, looking further out the curve we think that most of the price damage to bonds (in the 5-year and in maturity range) has already been done - which is what we were trying to help investors avoid by using the WisdomTree Floating Rate Treasury ETF.

So What Is The Trade?

We still very much like the idea of utilizing the WisdomTree Floating Rate Treasury ETF in place of money market funds and longer dated bond funds to park cash. However, we do think that it is time for investors to begin to look at ETFs that have longer durations and to begin to redeploy capital that is allocated for fixed income away from floating rate debt and back into securities that can deliver a combination of yield and capital gains. While 2022 was all about capital preservation for us, we think that 2023 is going to be about rotating back into duration assets in order to position ahead of 2024 - which we believe could be the year when significant total return can be realized from fixed income securities which have recently been issued (due to higher coupons which generate decent income and rates heading lower which could help bond prices increase).

In order to avoid potential losses, we think this allocation adjustment should be done orderly and methodically - meaning one should choose where they want their risk to be on the curve and stick to that plan. We currently do not want to go too far past the 5 year maturity range and have been utilizing the 1-2 year maturity range most recently to match cash to known outflows (rather than utilizing floating rate securities) in order to lock in rates and, in some cases, create tax benefits.

Final Thoughts

While some might think that this is something of a contrarian bet, we disagree and instead would frame it as positioning ahead of the move. The nearly 40 year bull market in fixed income has come to an end, but just like when the move started, this will be a multi-year, multi-move change. Rates can, and will, move both ways no matter the type of market we are in, so it is important to position for that while also allocating capital in an efficient manner. Sticking to the roughly 5 year and in maturity area should insulate investors' portfolios, and making that move methodically over 2023 should enable investors to average into decent positions.

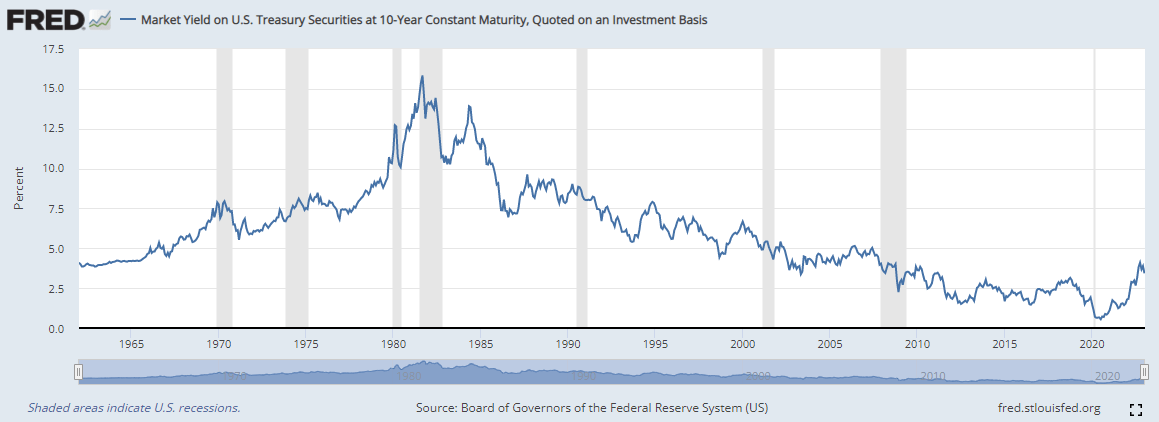

The bull market in US Treasuries is over, but even if we continue to trade sideways, current yields appear to be attractive - at least on a historical basis. (Board of Governors of the US Federal Reserve System)

{kind=link}

The graph above shows that the bull market in the 10-year US Treasury certainly appears to have ended, but importantly it also highlights that current rates are above recent high water markets for rates going back a decade. So while this is not a contrarian bet, one can take some solace in the fact that even if early, current rates are still historically impressive when compared to rates over the past decade.

While there are a few short-duration ETFs that make sense here, we also think that investors would do well to own individual securities - that way one can control the duration risk, coupon and yield within their portfolio. Liquidity has been pretty good in the 2-year and in portion of the curve and we have also seen some certificates of deposit, CDs, in the last 30 days which had attractive rates that made sense. For the investor who is looking to lock in attractive rates and rebuild their fixed income portfolio, there are a number of plays available.

For further details see:

USFR: Adjusting Our Outlook