USFR - USFR And SGOV: Fed Suggest 5% Yields Until End Of 2024

2023-09-22 11:44:47 ET

Summary

- Owning treasury bills and floating rate treasury bond funds can provide attractive risk-free yields in uncertain economic times.

- The recent "hawkish pause" by the Federal Reserve has positive implications for SGOV and USFR. Fed Officials are forecasting 5%+ yields until the end of 2024.

- If they do end up cutting interest rates, that will be because the economy weakens. In that case, SGOV and USFR give investors a 'real option' to buy cheap assets.

I have been an advocate for owning treasury bills and floating rate treasury bond funds like the WisdomTree Floating Rate Treasury Fund ETF ( USFR ) and the iShares 0-3 Month Treasury Bond ETF ( SGOV ) for the better part of this year, as earning 5% risk-free yields is very attractive in light of the uncertain macroeconomic environment.

However, the one drawback from owning these floating rate securities is the unpredictable nature of short-term interest rates. How high will the Federal Reserve raise its short-term Fed Funds rate, and how long will they keep Fed Funds rates elevated are two key questions keeping T-bill owners up at night?

Recently, at the September FOMC meeting, the Federal Reserve decided to keep its Fed Funds rate steady at 5.25%. However, analysts considered this a 'hawkish pause'. What does a hawkish pause mean, and what are the implications for SGOV and USFR?

Brief Fund Overviews

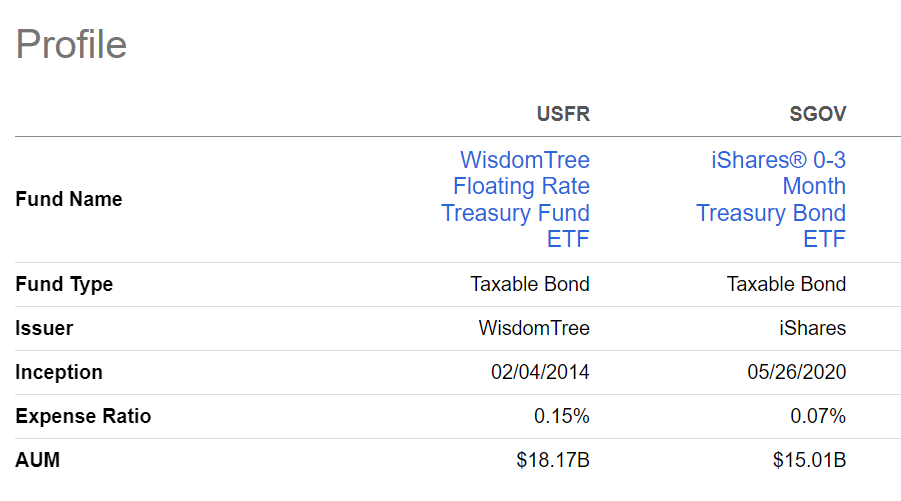

First, for those still warming up to treasury bills as a viable investment asset class, let me introduce my two favorite holdings in this space (Figure 1). In terms of lowest cost, we have the iShares 0-3 Month Treasury Bond ETF ("SGOV"), which simply owns 3-month treasury bills and rolls them at maturity and charges a 0.07% expense ratio (fee waiver until June 2024, then reset to 0.13%). In contrast, the WisdomTree Floating Rate Treasury Fund ETF ("USFR") owns floating rate treasury bonds that typically have 1 to 2-year maturities and pay the prevailing 3-month treasury bill rate every quarter (Figure 1). USFR charges a 0.15% expense ratio.

Figure 1 - USFR and SGOV are low-cost ways to earn treasury bill yields (Seeking Alpha)

{kind=link}

Both SGOV and USFR invest in securities backed by the U.S. government, so they are generally considered to be default risk-free. Furthermore, as their interest payments reset quarterly or are based on prevailing treasury bill yields, they also have nearly zero duration risk. Basically, both funds can be considered 'near cash' investments.

In terms of yields, the SGOV has a 30D SEC yield of 5.32% and its latest monthly distribution annualizes to 5.14%. USFR has a 30D SEC yield of 5.37% and its latest distribution annualizes to 5.35%.

Markets Interpret Fed Pause As Hawkish

As mentioned briefly at the beginning of this article, the Federal Reserve decided to keep its Fed Funds rate steady at the recent September FOMC, the second meeting in a row where the Fed has kept interest rates steady. However, many pundits considered the Fed's September actions to be a ' hawkish pause ', and equities and bonds tumbled as a result. What does a 'hawkish pause' mean, and what are the implications for SGOV and USFR?

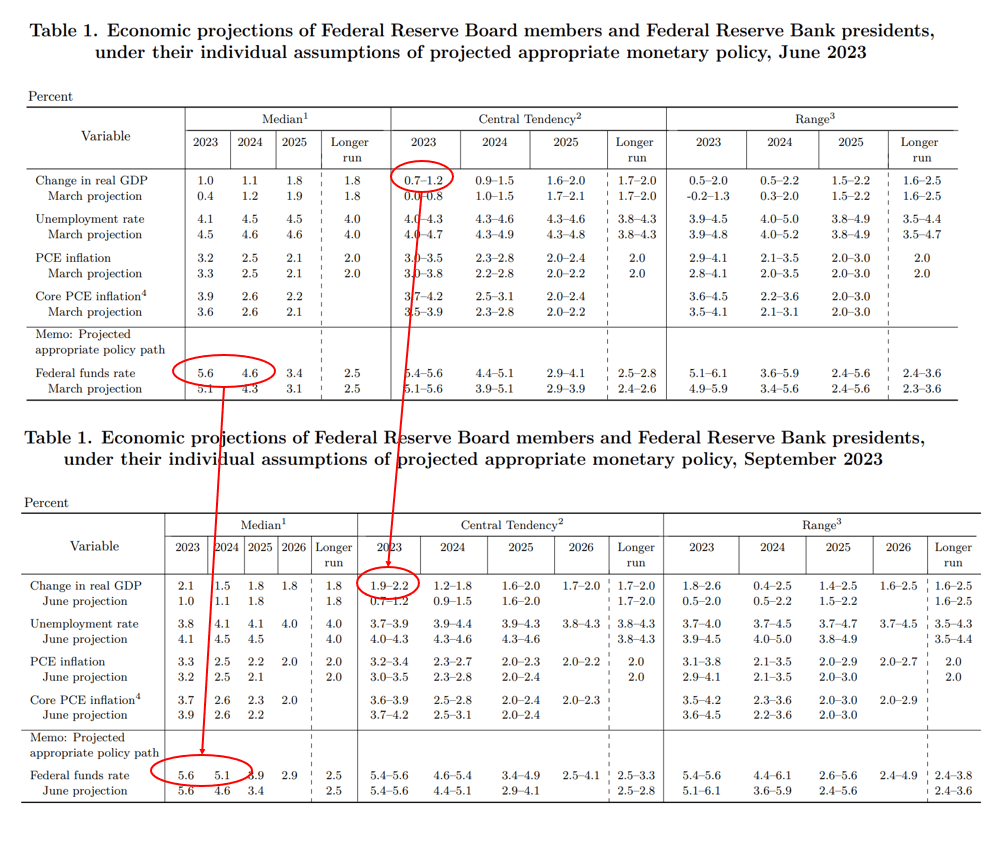

Although the Federal Reserve kept its Fed Funds rate steady, in its Summary of Economic Projections , Fed officials maintained their median forecast for a 2023 year-end Fed Funds rate of 5.6% compared to the current 5.25-5.50% range. This means the Federal Reserve is still open to raising interest rates one more time before the year is over (Figure 2).

Figure 2 - Comparison between June and September SEP (Author created)

{kind=link}

Furthermore, the Fed raised its forecasts for the 2024 median Fed Funds rate from 4.6% to 5.1%, effectively pricing out two interest rate cuts. Finally, Fed officials also raised their estimates for economic growth, with 2023 estimates now a solid 1.9-2.2% GDP growth. This means the Fed is likely no longer as concerned about the economy and is less likely to cut interest rates, in my view.

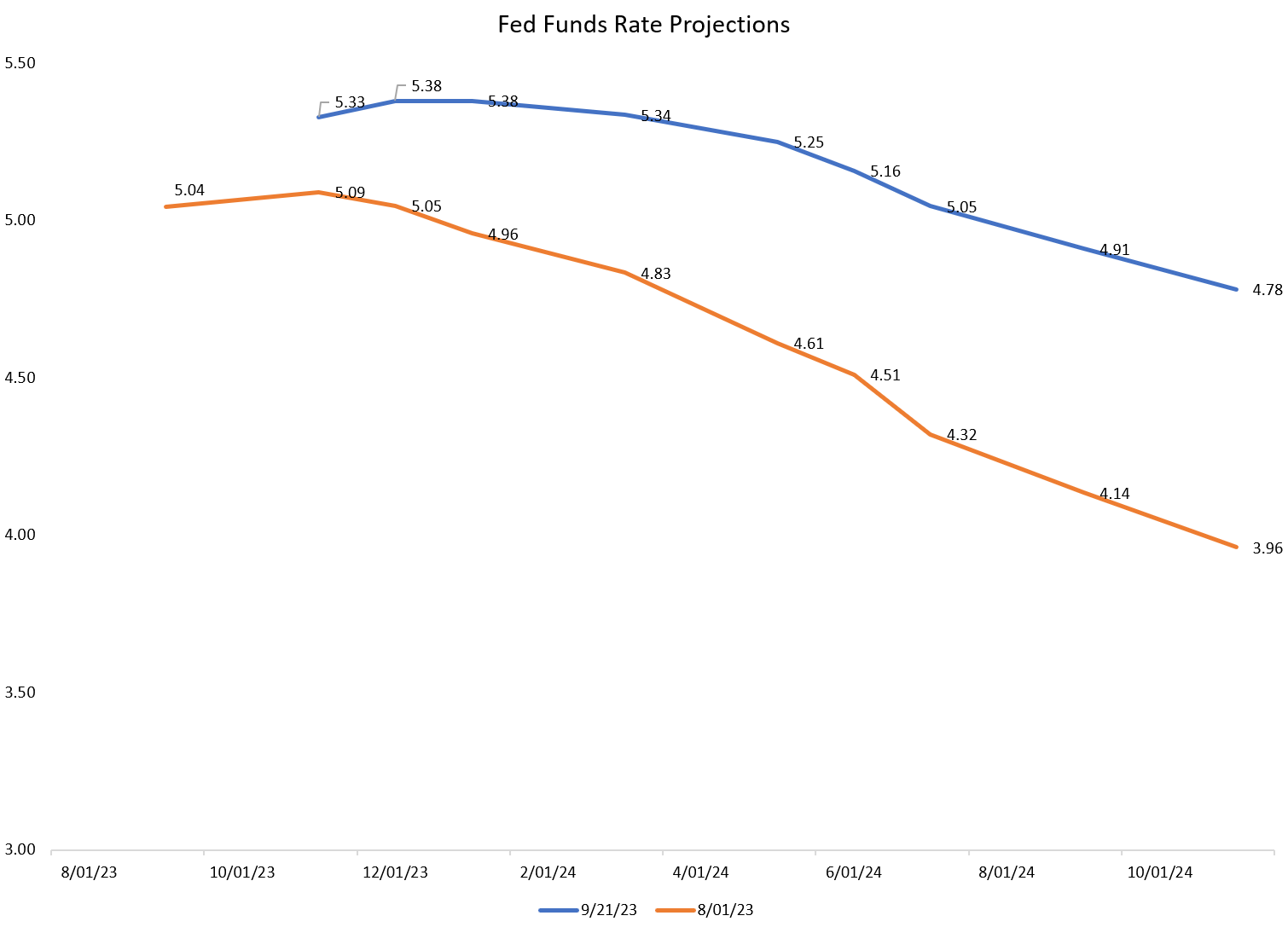

The immediate impact of the Fed's decision was a repricing of interest rate policy by fixed income traders. As recently as early August, traders were expecting the Federal Reserve to begin cutting interest rates by the end of 2023, and by the end of 2024, they expect the Fed to have cut interest rates by more than 4 times or a total of 109 bps to 3.96% (Figure 3).

Figure 3 - Traders have dramatically reduced Fed rate cut expectations (Author created with data from CME)

{kind=link}

However, after the updated SEP forecasts, traders have pushed out their Fed interest rate cut expectations to mid-2024, and their 2024 year-end forecasts have been raised to 4.78%, pricing in only 2 rate cuts instead of 4.

Readers should note that the market's expectation for 2024 year-end Fed Funds rates of 4.78% is still 32 bps lower than Fed officials' median forecast. I believe this suggests the market is still more dovish than the Fed.

Higher For Longer For One More Year

While Chairman Powell stressed that the Summary of Economic Projections is only the FOMC committee's best efforts forecast at a point in time and does not represent a prescription for how monetary policy is going to be implemented, the SEP does give analysts and investors a glimpse into what Fed officials are thinking.

My interpretation of the SEP is that barring a sharp deceleration in the economy, the Fed is very likely to maintain its restrictive monetary policies 'higher for much longer'.

With respect to SGOV and USFR, this also implies that high short-term interest rates are here to stay for at least another year unless the economy worsens materially in the coming months.

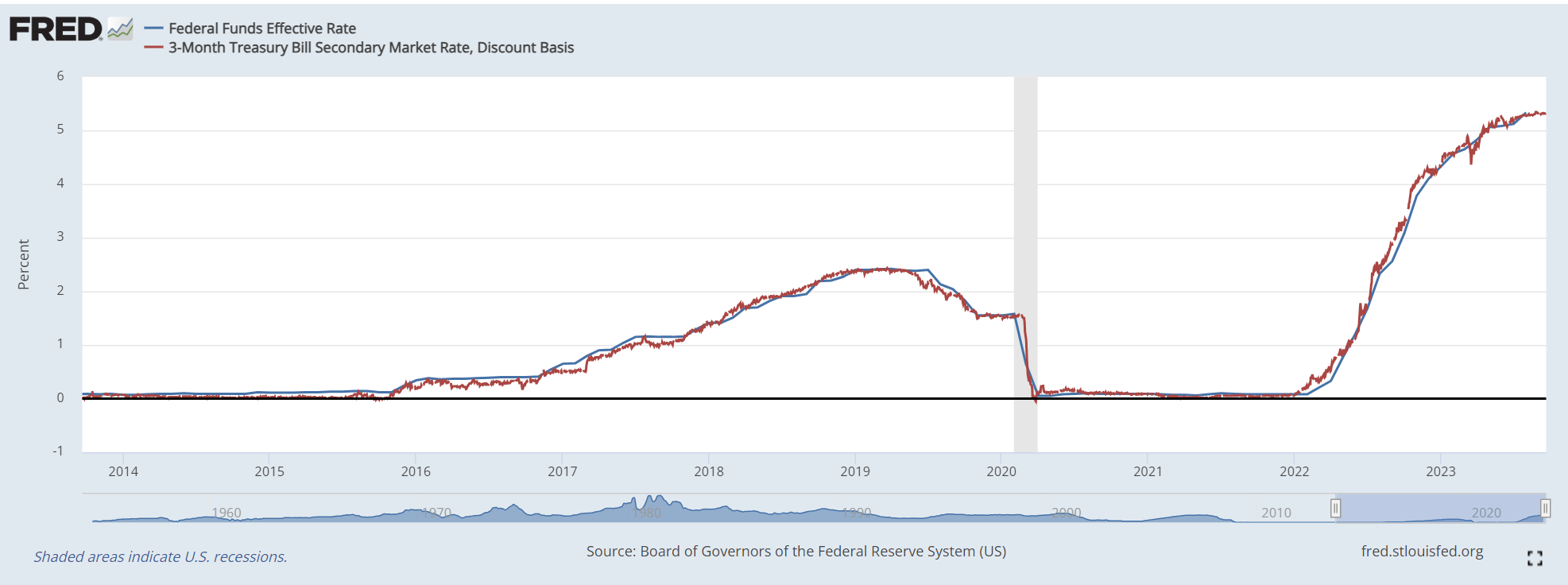

If we take the Fed officials at their word, they expect the Fed Funds rate to be 5.1% at the end of 2024. Since 3-month treasuries trade basically the same as the Fed Funds rate, this means I'm expecting SGOV and USFR to continue earning 5%+ for all of 2024 (Figure 4).

Figure 4 - Fed Funds rate and 3-month treasuries are essentially identical (St. Louis Fed)

{kind=link}

Risk To SGOV/USFR

The biggest risk to SGOV and USFR is if the economy worsens suddenly, then the Federal Reserve may decide to cut interest rates far sooner than what they are forecasting right now. However, if that were to happen, then I expect a high allocation to SGOV and USFR will come in handy as investors can sell their 'cash' holdings and use the proceeds to buy assets at much lower valuations. Cash is a real option.

Conclusion

The biggest worry for floating rate treasury yields is how long the current era of high short-term interest rates will last. The most recent FOMC meeting gave us a glimpse of how long Fed officials expect Fed Funds rates to stay elevated.

If we take Fed officials at their word, the Fed Funds rate is expected to be 5.1% at the end of 2024, which means SGOV and USFR can continue to earn 5%+ yields for the next year. I continue to rate both SGOV and USFR a buy.

For further details see:

USFR And SGOV: Fed Suggest 5% Yields Until End Of 2024