SGOV - USFR: Keeping An Eye On The Exit (Downgrade To Hold)

2023-11-08 17:57:20 ET

Summary

- The Federal Reserve has paused its rate hikes, indicating that short-term interest rates may have peaked.

- Market expectations suggest the first rate cut may occur in mid-2024, with three cuts expected by the end of 2024.

- I plan to switch treasury bill holdings into 2-year notes in anticipation of possible economic weakness and a cut in Fed Funds rates.

As someone who holds roughly 30% of my investment portfolio in floating rate treasury securities like the WisdomTree Floating Rate Treasury Fund ETF ( USFR ) and the iShares 0-3 Month Treasury Bond ETF ( SGOV ), I pay close attention to macroeconomic news, especially those that concern the Federal Reserve and the setting of short-term interest rates.

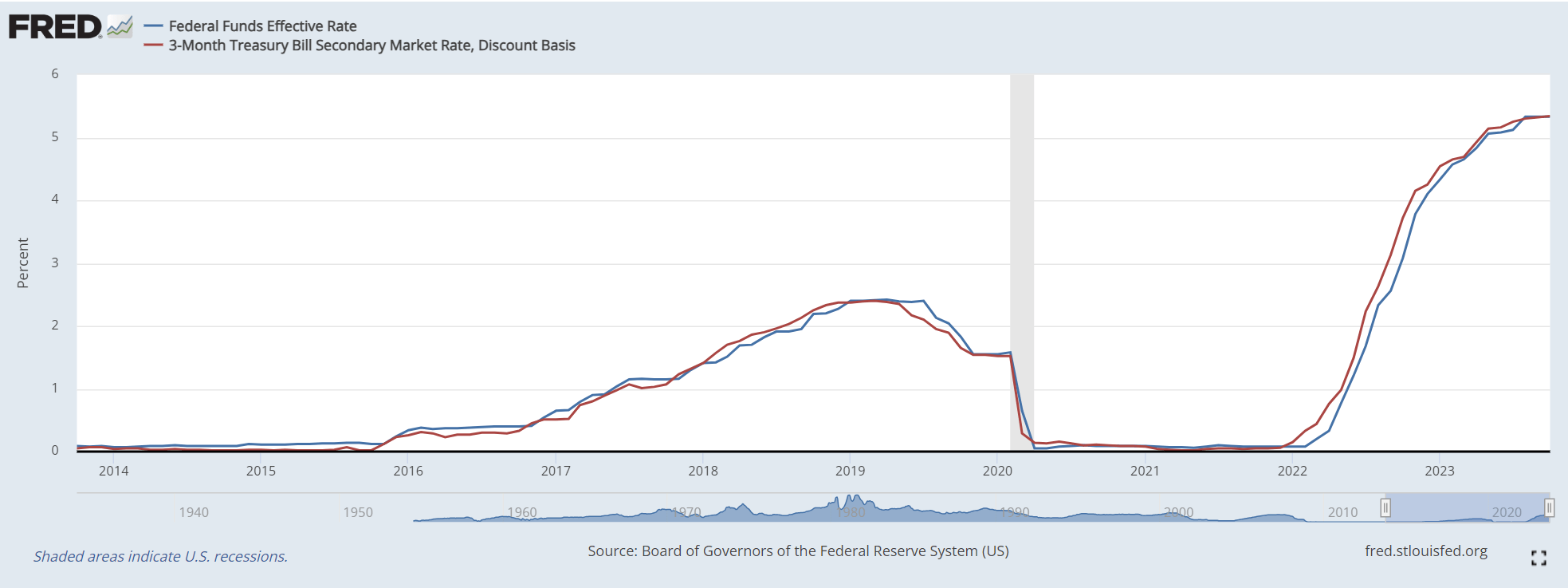

In prior articles, I have shown that the short-term Fed Funds rate set by the Federal Reserve is directly related to short-term 3-month treasury yields on which SGOV and USFR are based (Figure 1). That is why it is critically important for floating-rate investors like myself to monitor macroeconomic developments.

Figure 1 - Fed Funds rate is directly linked to 3 month treasury bill rates (St. Louis Fed)

{kind=link}

In my most recent article on SGOV and USFR, published after the September FOMC meeting, I noted that the Fed's September Summary of Economic Projections ("SEP") suggested the Fed may hold interest rates 'higher for longer' until the end of 2024.

So far, my thesis has held true, as the Fed kept the short-term Fed Funds rate steady at the recent November FOMC meeting. However, as a Fed pause was well-telegraphed, the details on future policy decisions are what really matters.

Dovish Pause?

When asked whether a hypothetical pause at the upcoming December would mean interest rates have peaked, Chair Powell took pains to reiterate that "the idea that would-- difficult to raise again after stopping for a meeting or two, it's just not right. I mean the Committee will always do what it thinks is appropriate at the time. And again, we haven't made any decisions at all about December." (source: November FOMC press conference transcript )

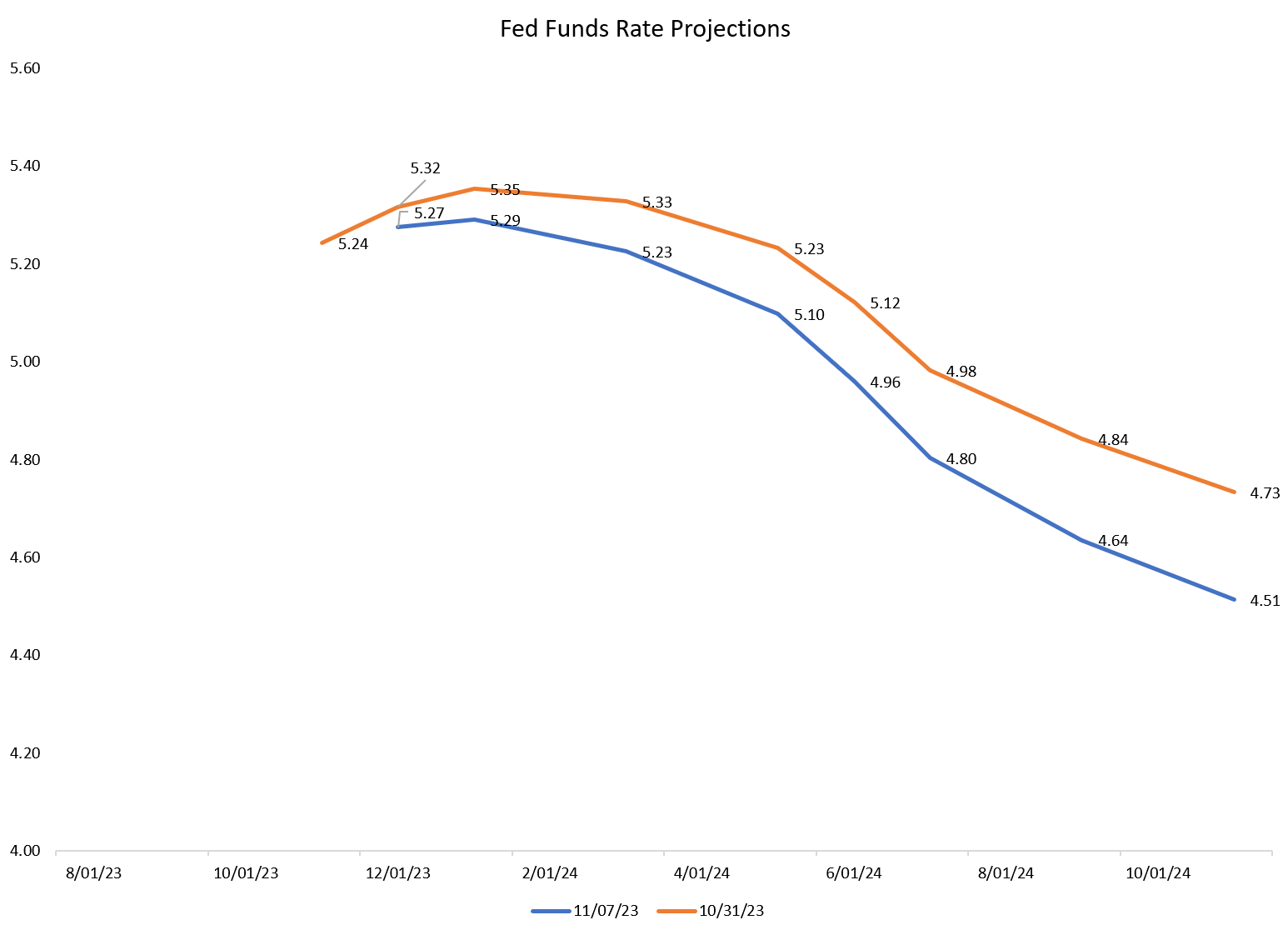

However, despite repeated attempts by Chair Powell to sound hawkish in the press conference with quotes like the one above and "the Committee is not thinking about rate cuts right now at all" , financial markets interpreted the latest FOMC decision as dovish . Traders brought forward their first rate cut estimate by a month to May 2024 and lowered their year-end 2024 Fed Funds rate estimate by 22 bps to 4.51% (Figure 2).

Figure 2 - Traders interpreted the FOMC meeting as dovish (Author created with data from CME)

{kind=link}

What else was said in the press conference that led to the dovish interpretation? I believe Chair Powell's answers to some of the questions may have led to the dovish interpretation.

First, Chair Powell noted that the efficacy of the Summary of Economic Projections "decays over the three-month period between that meeting and the next meeting" , so whatever hawkish projections the FOMC committee made in September may no longer apply as the situation may have changed.

Furthermore, when pressed by Bloomberg's Michael McKee on whether each meeting going forward was 'live', Chair Powell seemed reluctant to accept that characterization and said that "you're close to the end of the cycle". These 'slip of the tongue' dovish statements negated most of his explicitly hawkish language in my view.

Jobs Report Shows Normalizing Labor Market

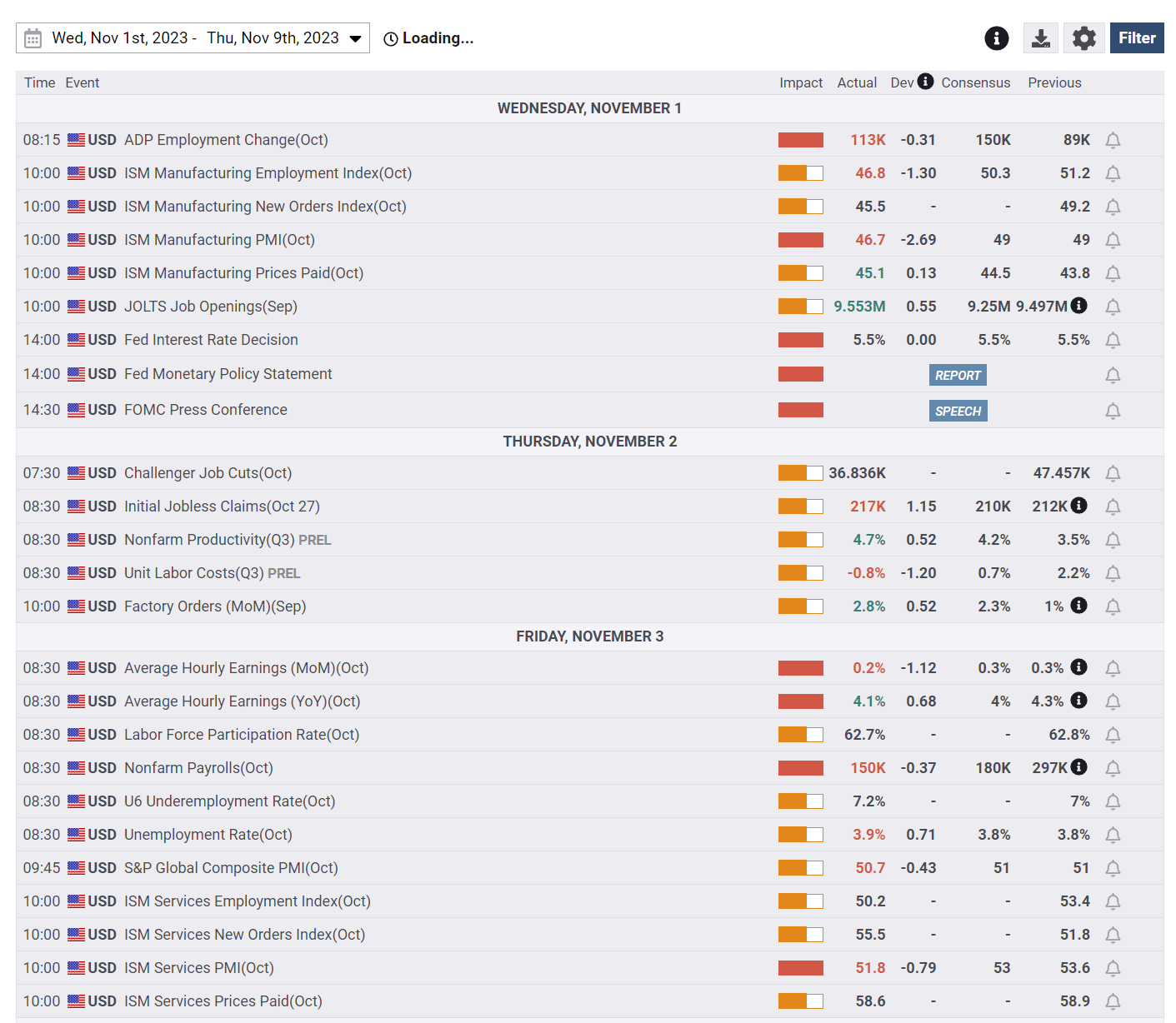

Another reason investors have turned more dovish in recent days is that macroeconomic data has come in softer than expected, which suggests monetary policy is near a sufficiently restrictive level. For example, on the same day as the FOMC meeting, the ISM Manufacturing PMI came in at 46.7, missing estimates of 49 (Figure 3).

Figure 3 - Macroeconomic data has come in softer (fxstreet.com)

{kind=link}

Most importantly, the Nonfarm Payrolls report on Friday, November 3rd came in significantly weaker than expected at 150k vs. 180k estimated and 297k last month. Unemployment also rose to 3.9%.

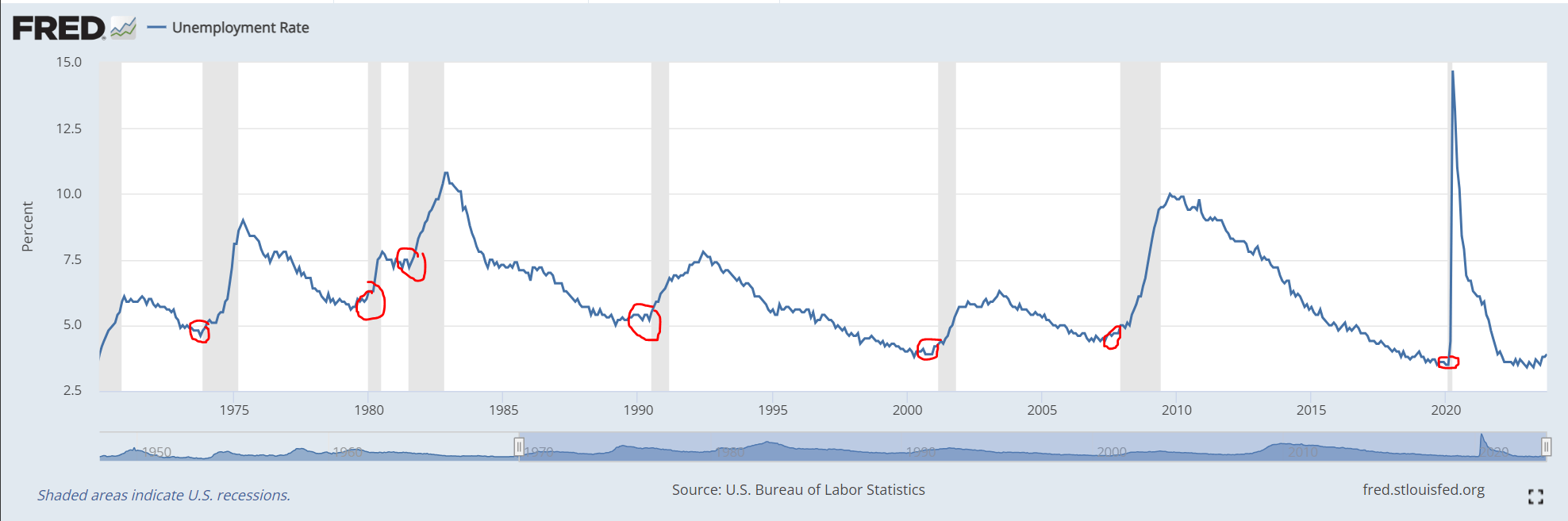

Relative to the cycle low unemployment rate of 3.4% from January 2023, the unemployment rate has now increased by 0.5% to 3.9%. While still low by historical standards, a rising unemployment rate suggests labor markets are normalizing and hence there may be less need/desire by the FOMC to raise interest rates further.

In fact, some macro analysts are pointing to the rising trend in the unemployment rate as an ominous precursor to a coming recession. Historically, a persistent rise in unemployment is a coincident/leading indicator to recessions (Figure 4).

Figure 4 - Rising unemployment leads to recessions (St. Louis Fed)

{kind=link}

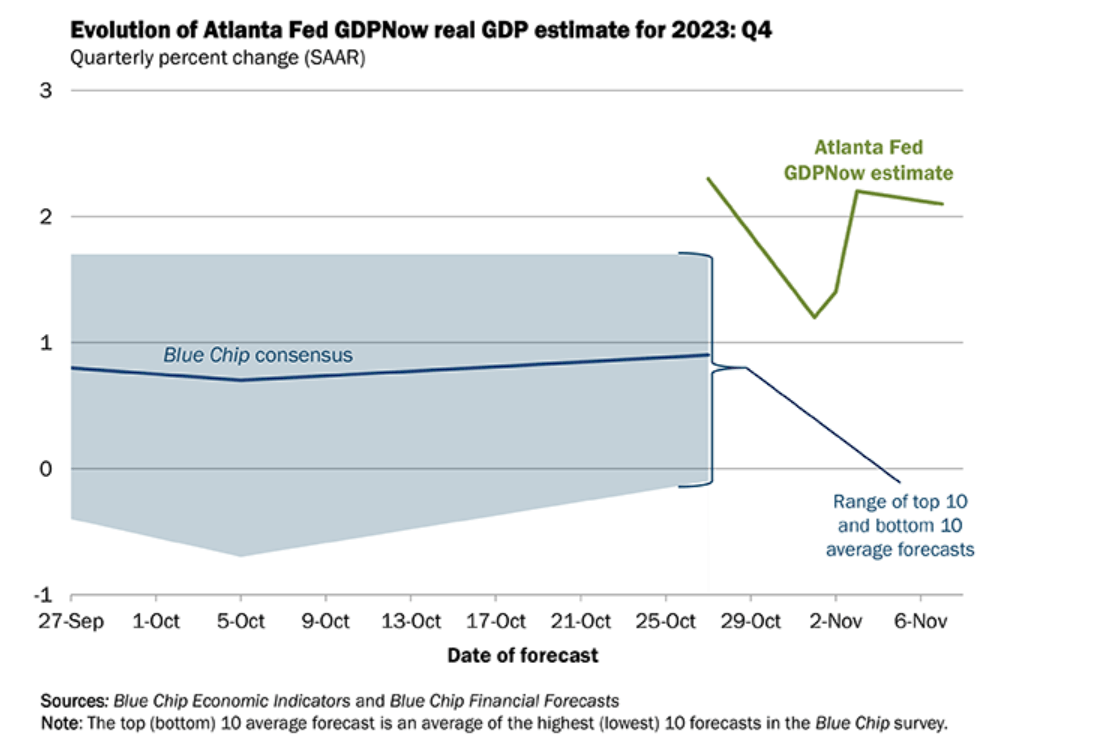

GDP Slowing But Still Positive For Now

While I am concerned about a weakening economy, real-time forecasts from the Atlanta Fed's GDPNow tool suggest the American economy is still growing, albeit at a slower pace than Q3's blistering 4.9% annual pace (Figure 5).

Figure 5 - GDPNow forecasting ~2% growth in Q4 (Atlanta Fed)

{kind=link}

So for now, it may be premature to worry about an imminent recession and the Fed cutting interest rates to boost economic growth. However, when the Fed starts cutting interest rates to support a weakening economy, they usually don't just cut once.

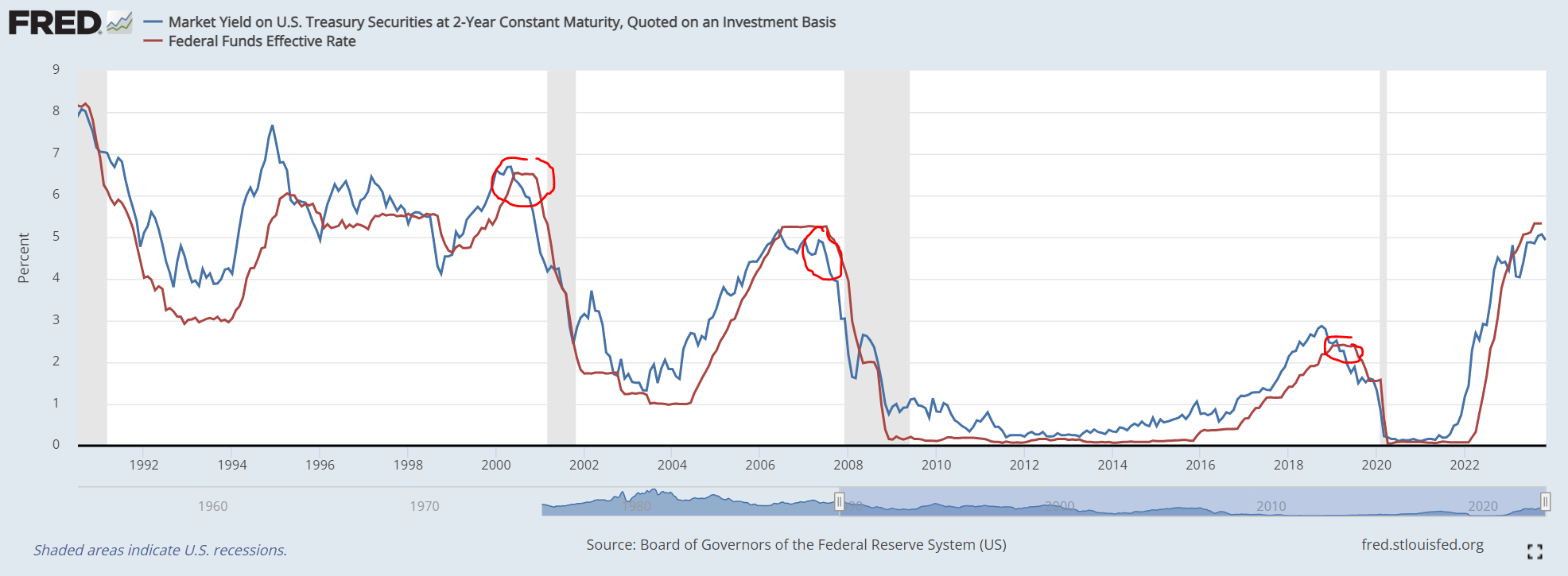

2-Year Yield May Provide Some Clues On End Of 'Higher For Longer'

Historically, the 2-year yield has front-run the Fed in anticipating rate cuts (Figure 6). If the 2-year yield starts to decline rapidly, that will most likely signal some near-term economic troubles requiring the Fed to cut interest rates, and hence 3-month treasury yields.

{kind=link}

My plan is to gradually switch my treasury bill holdings into 2-year notes and funds in the coming months, ahead of an expected decline in 2-year yields, in order to lock in the current high yields for an extended period of time while retaining the optionality of holding 'near-cash' assets.

Conclusion

The Federal Reserve recently paused its rate hikes for a second FOMC meeting in a row. This suggests we are near the end of the current rate hike cycle and that short-term interest rates may have 'peaked'.

The next step to consider is when the Fed may cut interest rates in the future. Currently, the market expects the first rate cut in mid-2024, with 3 cuts expected by the end of 2024.

I believe floating-rate treasury funds like USFR and SGOV are still a good choice for the next few months, although their yields are expected to decrease once the Fed cuts interest rates.

I am personally looking to gradually switch my treasury bill holdings into 2-year notes over the next few months ahead of possible economic weakness and a cut in Fed Funds rates. I am downgrading USFR to a hold .

For further details see:

USFR: Keeping An Eye On The Exit (Downgrade To Hold)