USFR - USFR: Skate To Where The Puck Is

2024-01-21 05:09:01 ET

Summary

- The Federal Reserve is expected to make three rate cuts in 2024, shifting to an easier monetary policy.

- Treasury bill yields closely follow Fed Funds policy rates, so the income from the USFR ETF will decrease as rates are cut.

- To protect against rate cuts, investors may want to consider lengthening the duration of their 'cash' holdings with 2-year treasury funds.

In my most recent article on the WisdomTree Floating Rate Treasury Fund ETF ( USFR ) written in early November, I noted the Federal Reserve was pausing its policy rate increases, which suggest policy rates may be peaking.

My suspicions were confirmed at the December FOMC meeting when Fed Chair Jerome Powell said that interest rates were "likely at or near the peak rate for this cycle" during his press conference. Furthermore, the December Summary of Economic Projections ("SEP") from the Fed showed that the FOMC Committee were forecasting Fed Funds rate to decline by 80 bps from a 2023 median forecast of 5.4% to 4.6% at the end of 2024 (Figure 1).

Figure 1 - December Summary of Economic Projections (federalreserve.gov)

So not only were the Fed no longer holding onto their 'Higher For Longer' tighter monetary policies, they were pivoting to a 'Soft Landing' easy monetary policy.

The reasoning the Fed gave was that if inflation continued to decline towards 2%, but the Fed kept policy rates steady, then that would effectively be tightening monetary policy, as real interest rates (nominal less inflation) would increase. The Fed therefore needs a few 'insurance cuts' to avoid over-tightening the economy into a recession.

T-Bill Yields Follow Fed Funds Rates

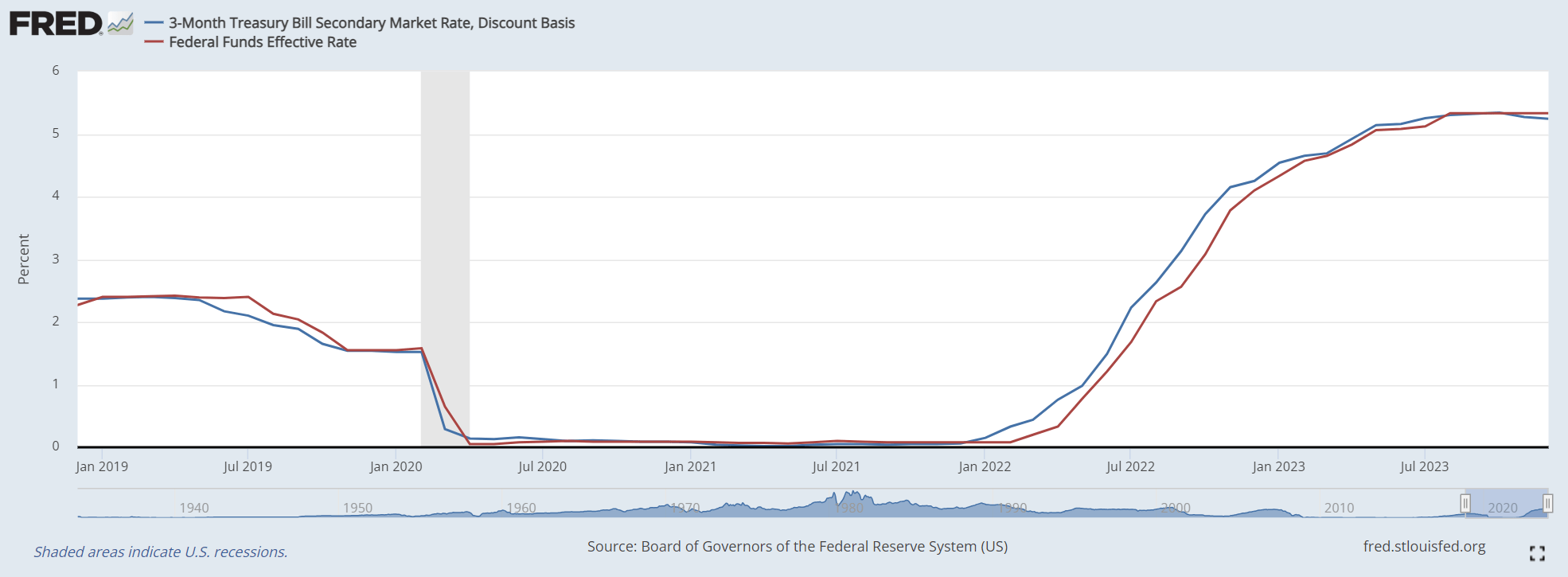

As I have written in prior articles, the reason investors in the USFR ETF should pay close attention to the Federal Reserve is because treasury bill yields closely follow Fed Funds policy rates (Figure 2).

Figure 2 - 3 month treasury bill yields follow Fed Funds rates (St. Louis Fed)

{kind=link}

Since the USFR ETF holds floating rate treasury bonds that pay interest tied to the 3-month treasury bill yield, if the Fed starts to cut Fed Funds rates in 2024, then the income that USFR investors receive will also be heading lower in the coming year (Figure 3).

Figure 3 - USFR holds floating rate treasury bonds (wisdomtree.com)

{kind=link}

With interest rate cuts seemingly a sure thing according to consensus, the key questions that remain are when will the first cut occur, and how much will the Fed cut in 2024?

March, May, Or Sometime Later?

With respect to the timing, markets seem to have gotten a little too optimistic and is currently in the process of walking back expectations that the Fed will start cutting interest rates as early as March (Figure 4).

Figure 4 - Fed Funds rate probability (January 18, 2024) (CME)

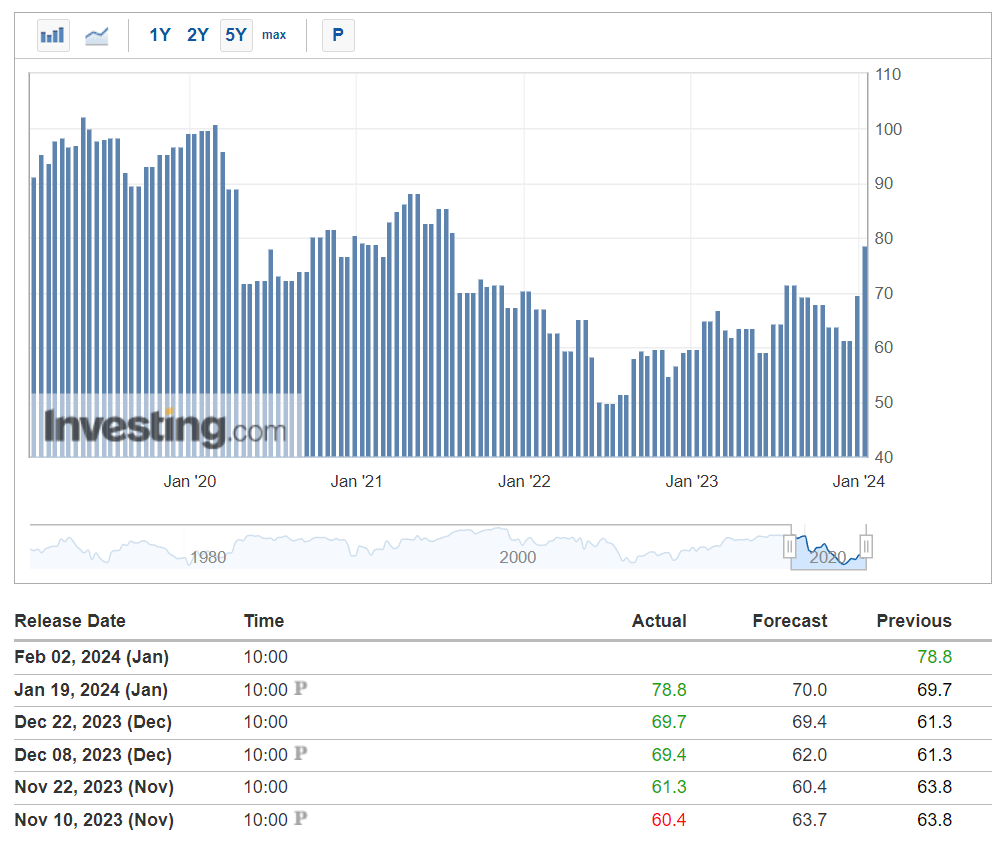

In fact, recent comments from Fed governors Chris Waller and Raphael Bostic seem to be pushing back against the idea of a March rate cut, as economic data has been surprisingly strong and the December CPI inflation report surprised to the upside (Figure 5).

Figure 5 - December CPI inflation surprised to upside (investing.com)

Nevertheless, from my perspective, as long as inflation does not make a surprise U-turn and surge back toward 2022 levels, it is a safe bet that the Fed will make a few 'insurance cuts' in the coming months.

Also, given that the U.S. will be holding a general election in early November, I believe the Fed will want to avoid the appearance of aiding the incumbent Biden administration by cutting interest rates late in the Fall, directly leading up to the election. Hence, if the Fed were to cut rates, I believe they will most likely cut in the Summer.

Leaning Towards 3 Rather Than 6 Cuts

With regards to the number of cuts, I am personally leaning towards 3 rather than the 6 cuts the markets have been pricing in. This is because economic data have simply been too strong to argue for anything more than basic 'insurance cuts'.

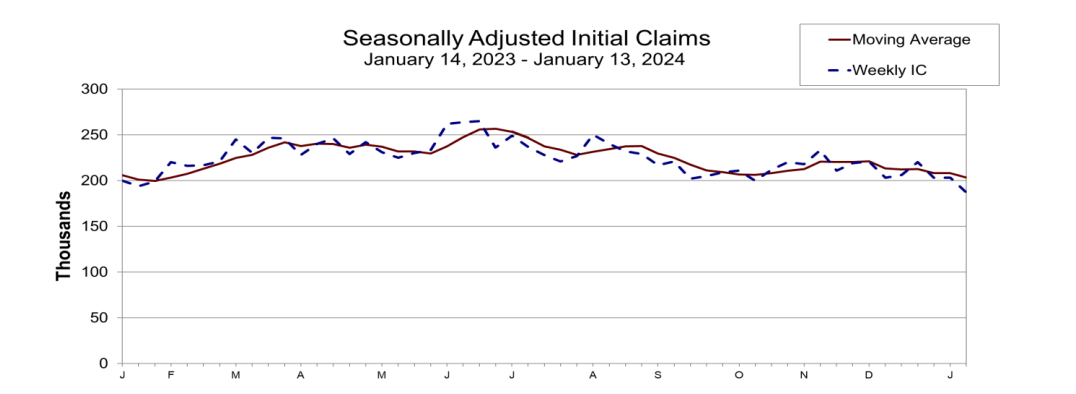

For example, the latest initial jobless claims report of 187,000 was much stronger than consensus expectations of 207,000 and was the lowest in over a year, suggesting the labour market remains robust (Figure 6).

Figure 6 - Initial jobless claims were surprisingly low (US Department of Labor)

{kind=link}

Similarly, consumer sentiment surged to a multi-year high in January, dispelling fears that American consumers were suffering (Figure 7).

Figure 7 - Consumer sentiment surged to multi-year highs (investing.com)

{kind=link}

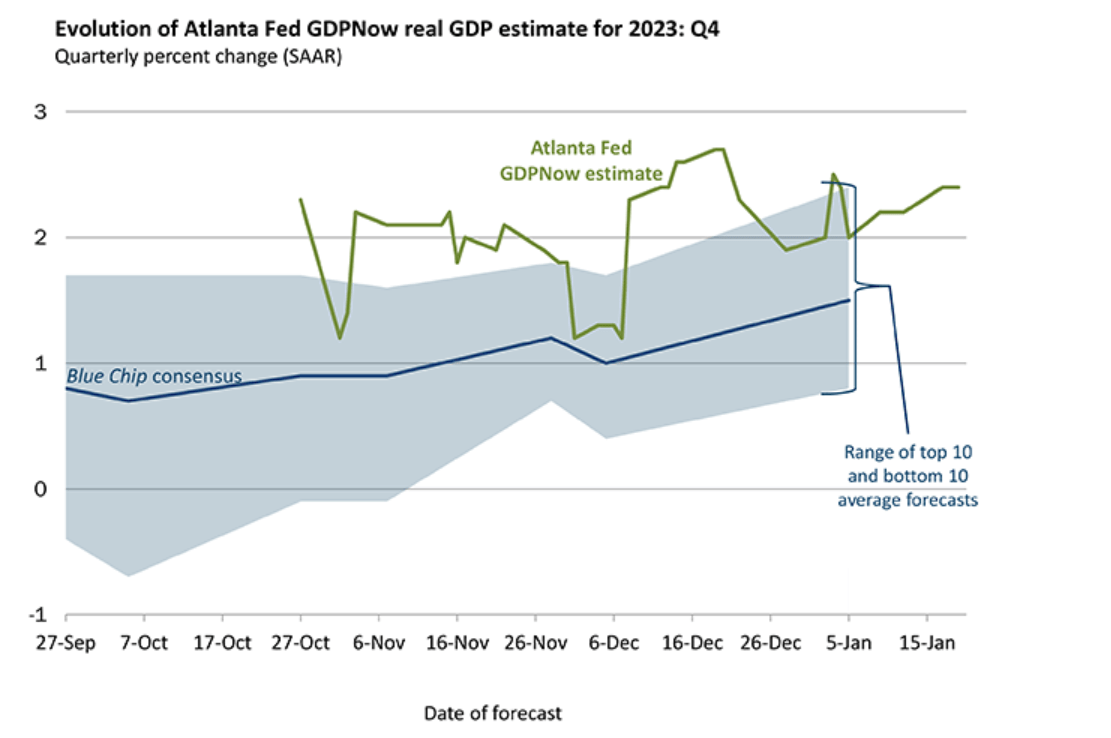

Finally, real time estimates from the Atlanta Fed showed the American economy still growing at a robust 2.4% YoY in Q4 (Figure 8).

Figure 8 - Real time GDP forecast still suggest robust growth (Atlanta Fed)

{kind=link}

Simply put, the recession fears from 2023 seem to be long forgotten, and the economy appears to be on a glide path towards a 'soft landing'. In a 'soft landing' scenario, the Fed will not need to cut policy rates six times.

Downside Scenarios For USFR

However, in the event I am wrong and the economy slows down more rapidly in the coming months, there are obviously downside risks to Fed Funds rates, as the Fed will likely have to cut interest rates more aggressively. This could explain the market's expectations for 6 rate cuts in 2024, as many on Wall Street still expect a recession in the coming quarters.

Furthermore, assuming inflation does return to ~2%, there may be scope for the Fed to cut interest rates even more in 2025 and 2026, as shown in the SEP in Figure 1. The Fed currently expects Fed Funds Rates of 3.6% at the end of 2025 and 2.9% at the end of 2026.

If everything develops as the Fed expects, then USFR holders should expect their distributions to further decline in 2025 and 2026.

Consider Lengthening Duration Of 'Cash'

To protect against this decline in forward distribution yield, investors should consider lengthening the duration of their 'cash' holdings. For me personally, I have decided to shift a portion of my cash, currently held in the USFR ETF and the iShares 0-3 Month Treasury Bond ETF ( SGOV ), into the Simplify Short Term Treasury Futures Strategy ETF ( TUA ).

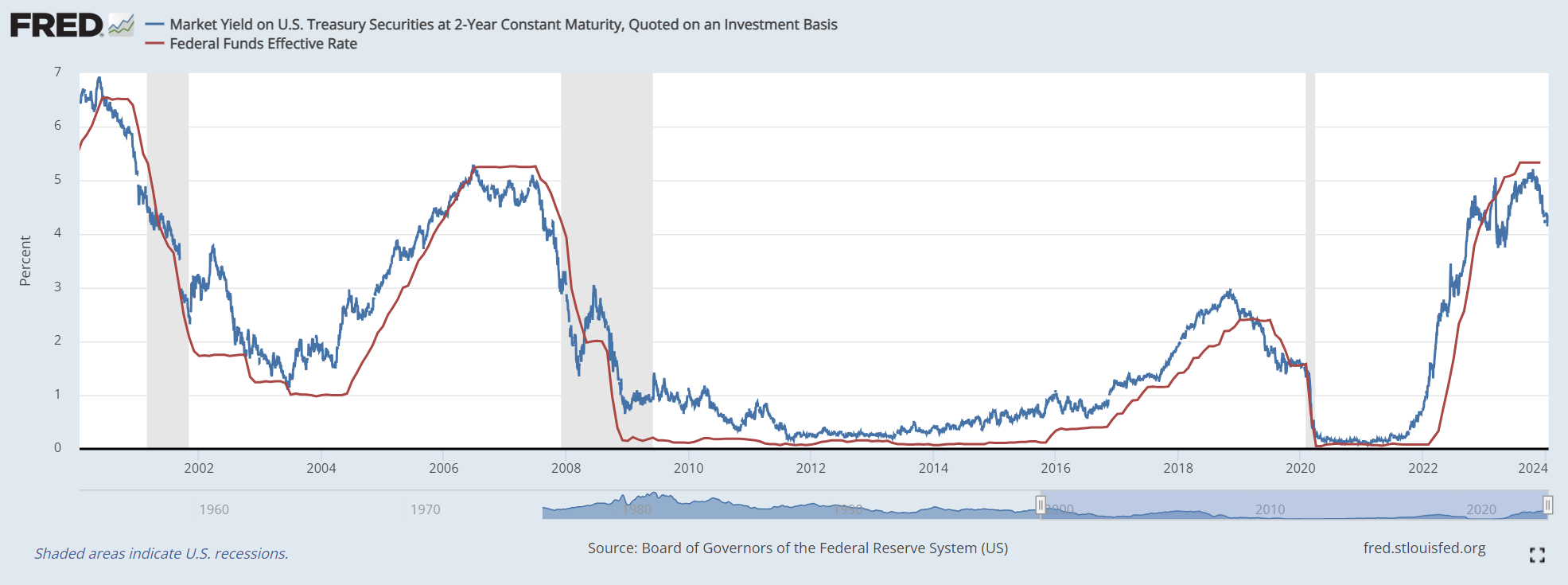

The TUA ETF is a levered bet on 2 year treasury bond futures, with collateral held in treasury bills to earn additional yield. It is designed to benefit when the 2 year yield declines, which typically leads actual Fed rate actions (Figure 9).

Figure 9 - 2 year leads Fed Funds (St. Louis Fed)

{kind=link}

By investing in the TUA, I am hoping to 'lock-in' the still attractive 2-year yield, while the dust settles on the economy.

If the Fed is correct and inflation declines while the economy holds up, Fed Funds rate should be ~3.6% at the end of 2025, lower than the current 2-year yield, which should provide modest capital gains on the TUA. In an adverse scenario where the economy weakens, and the Fed has to cut faster, the TUA ETF should do even better as 2 year yields will decline significantly.

However, lengthening the duration of cash does bring some risks. For example, if inflation returns and the Fed must hold policy rates steady for longer or even return to hiking policy rates, then the TUA will underperform.

Conclusion

In my prior article, I warned investors should keep an eye on the exit on the USFR ETF, as the Fed may be nearing the end of its hiking cycle. I believe that time has come, as the Fed has pivoted away from their 'higher for longer' stance to an easier 'soft landing' policy, with 3 rate cuts forecasted for 2024.

As the Fed cuts policy rates in the coming months, forward distribution yields on the USFR ETF will decline, since USFR's distribution is tied to 3 month treasury bills yields which track policy rates.

I am personally lengthening the duration of some of my cash holdings out of the USFR and equivalent funds and into 2 year treasury funds, to 'lock-in' current 2 year yields and to take advantage of expected policy rate cuts.

For further details see:

USFR: Skate To Where The Puck Is