CAJ - Ushio: Value Trap With Limited Scope For Growth

Summary

- Ushio is a cash and asset-rich business specializing in applied light sources in a wide array of sectors, with semiconductors being a core market.

- Recent trading is weak due to inventory corrections, increasing cost of parts and components, and a strengthening Japanese yen.

- The shares appear cheap trading on PBR 0.8x but with characteristics of an ex-growth business with limited earnings potential, we rate the shares as neutral.

Investment thesis

Ushio (UHOIF) is a niche market leader in legacy lighting technologies and a second-tier supplier to the semiconductor industry. Recent trading is weak with an inventory correction, and there appears to be no major secular growth driver for the business. With the shares trading on PBR 0.8x, we rate the shares as neutral and view them as a value trap.

Quick primer

Established in 1964, Ushio is an industrial company specializing in applied light sources (UV, visible and infrared) for use in markets such as semiconductors/flat panel display manufacturing, and lighting bulbs and components for projectors and illuminations. The core geographic market is Asia making up around 50% of total sales, followed by Japan making up around 25%. Key competitors include light source companies such as Signify (PHPPY), Hamamatsu Photonics (HPHTF), ams-OSRAM (AMSSY), and front-end SPE LCD scanner manufacturers such as Canon (CAJ) and Nikon (NINOY). It is a market leader in niche markets, such as a 65% share of cinema projector lamps and an 80% share in halogen lamps used in photocopiers.

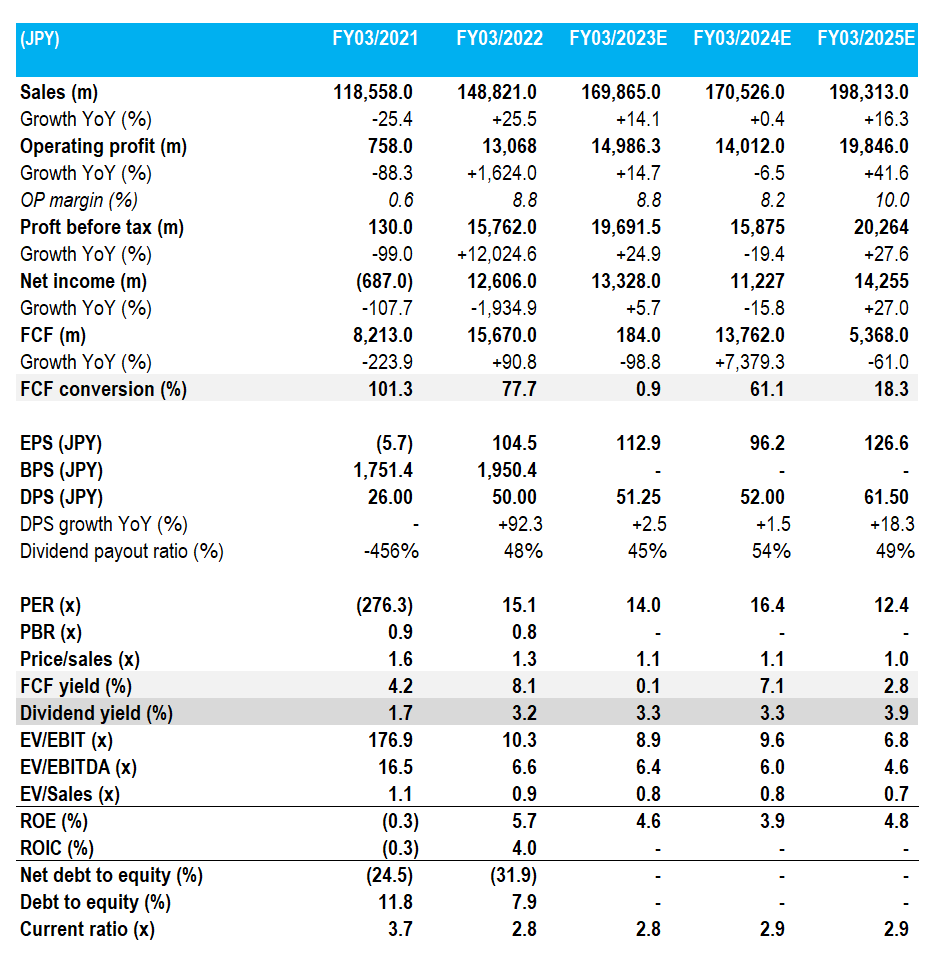

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

{kind=link}

Our objectives

The pandemic impacted Ushio significantly but it made a significant recovery into FY3/2022. Although some supply chain issues persist and China demand remains lackluster for cinema projector bulbs, we want to assess the medium-term outlook for the business.

Recent trading points to short-term difficulties

Q1-3 FY3/2023 results were steady with sales growth at 17% YoY partly driven by a weak Japanese yen, and operating profit growth of 25% YoY. However, the company lowered its FY3/2023 profit guidance due to expected weakness in the LCD and semiconductor industries; FY operating profit guidance was lowered from JPY17.0 billion/USD130 million to JPY 15.0 billion/USD115 million (a reduction of 11%). Demand for UV lamps used in SPEs for both memory and logic devices is expected to weaken as inventory adjustments occur - it would appear customers are over-stocked as they initially faced potential supply chain problems. However, there is also a demand-side issue and the company expects a soft semiconductor market until the end of H1 FY3/2024. Demand for cinema lamps in the Chinese market has also been weaker than expected with the 'zero COVID-19' policy, but a delayed recovery is in progress.

Increasing costs for parts and materials are being mitigated in part by the standardization of components and optimizing selling prices, but management concedes that in the short term profitability in Q4 FY3/2023 will decline.

Ushio operates in the mainstream technology arena for semiconductors, supplying non-leading edge components and equipment. It has made some advances in the EUV (extreme UV) market with light sources for mask inspection systems (not for the scanners in the fabs supplied by ASML ( ASML )). Despite expectations that this will be a long-term driver for the business, there are some concerns that there is pricing pressure from customers as well as a relative lack of competitiveness that could result in lowered expectations for the business in the forthcoming company's medium-term plan.

With a slowdown currently in progress, we can see this being reflected in consensus forecasts (please see Key Financials table above), with flat sales YoY and dampened operating profit margins YoY for FY3/2024.

Track record is a red flag

In order to be competitive in the semiconductor industry, sufficient capital must be allocated to R&D spend and capex. For the last six years, R&D spending has averaged 6.7% of sales, which is not a large amount to compete toe-to-toe with the market leaders. Capex spending has been 4.6% of sales which also looks on the low side. Overall, capital allocation looks conservative, as the business appears not to have a true world-beating technology to fully invest into. Capital intensity has increased from 1.8x in FY3/2017 to 2.2x in FY3/2022, illustrating that the company is becoming less efficient at generating revenues from its asset base.

The track record of the company is not stellar, with the 5-year CAGR for sales growth at -2.9%, EPS growth at 13.7%, and book value per share at 3.2% YoY. Free cash flow generation is patchy and the average FCF conversion stands at 37% which is at a relatively low level.

Valuations

Ushio trades at price to book below 1.0x and has 36% of market capitalization as net cash. However, we can see that this is a sub-standard business with low single-digit ROE, a price-to-sales ratio close to 1.0x which denote an ex-growth business, limited FCF generation, and a prospective dividend yield of 3.3% which is not exactly compelling.

Risks

Upside risk comes from a major uplift in semiconductor demand into H2 FY2024, which will have a positive knock-on effect for most suppliers in the industry.

The company may revisit its shareholder returns policy and allocate more cash to dividends and buybacks.

Downside risk comes from Ushio's continued ex-growth status as its core activities remain in legacy technologies such as halogen lamps and LCD manufacturing.

Management may commence taking high-risk decisions in order to drive growth into the business, which may result in high costs with limited returns.

Conclusion

The shares appear cheap on its PBR multiple of 0.8x but Ushio looks more like a value trap than a business capable of initiating positive dynamic change. Currently, we cannot see any proactive measures from the management that will improve its earnings trajectory, bar a short-term recovery in China-related demand, and the usual supply and demand rebalancing in the semiconductor market. With most of the current bad news priced in, we rate the shares as neutral.

For further details see:

Ushio: Value Trap With Limited Scope For Growth