UTMD - Utah Medical Products: Recycling Capital Well Long-Term Gains On The Table

2023-04-19 04:29:48 ET

Summary

- Utah Medical is a long-term compounder that was unfazed by the last two market cycles in 2002, 2008 and 2020.

- The company has strong business economics with a capital-light model that generates attractive economic profits.

- It has averaged 30% return on its capital invested since FY'18.

- I see the firm trading fairly at 48x forward earnings and believe it is on correct trajectory to hit this.

- Net-net, reiterate buy.

Investment Summary

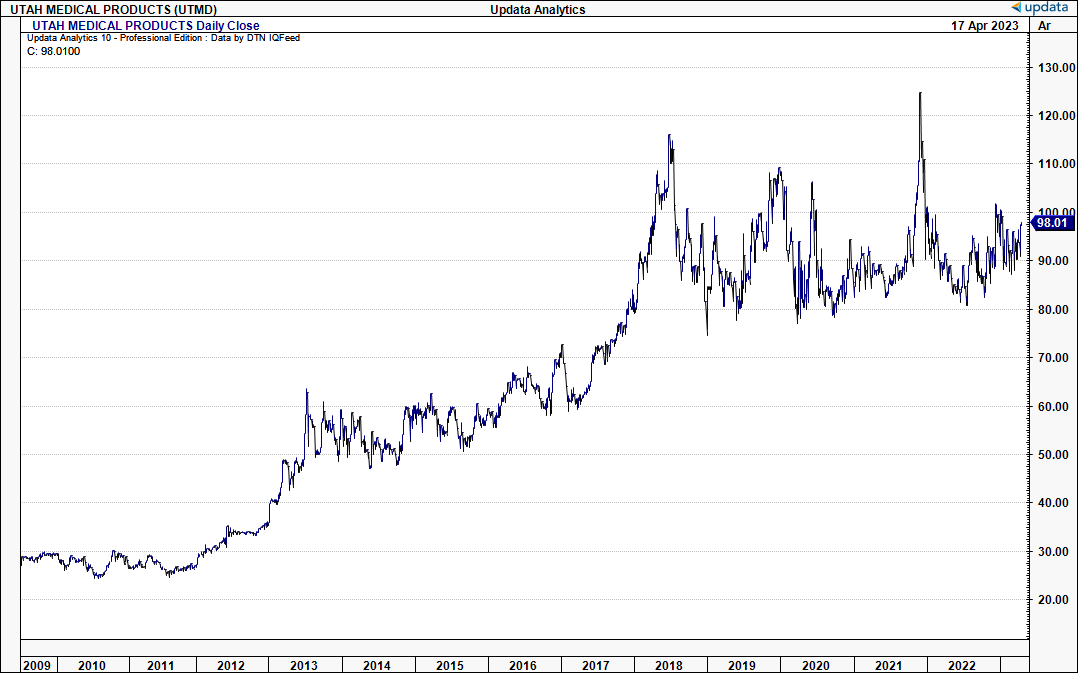

As shares continue to murmur along, I firmly believe there is long-term value to be obtained for Utah Medical Products, Inc. ( UTMD ) for equity-focused investors looking to create wealth over the long-term. Whilst history doesn't predict future results, UTMD has been a defensive compounder exhibiting a strong trend line of support for a lifespan. A $50,000 investment in UTMD in the year 2000 will now be worth $820,000 - a 1,540% total return, and impressive equity line as seen below [total return in Figure 1a, 2,460% return]. Investors have been treated to a 12-13% CAGR over this time.

As a reminder, UTMD is a vertically integrated medical manufacturing company. It manufactures a broad product offering in locations across Utah, Ireland, Australia, England, Canada. The firm is currently advancing into new product areas, including neonatal ICU, cervical/uterine disease, labour and delivery. It is partly achieving this by augmenting its current products. Here's an extremely valuable point: The average employment tenure with the UTMD [186 global full-time employees] is 13 years. In Utah, 1/5th of full-time employees have been with the firm for >30 years. This tells me more of the stability in operations - a feature that attracts me here. I had touched on this in my last UTMD publication .

For those exuding patience, I believe UTMD is a highly selective position that will continue to compound shareholder returns into the years to come. It was completely unaffected through the last two major market cycles - the dot.com bubble, and the '08/09 financial crises and offers defensive characteristics to equity positioning. This is appealing given the current climate. The following additional points are relevant to the investment debate:

- The firm generates stable, predictable long-term cash flow and earnings that continue to grow without discrepancy.

- Maintenance and growth CapEx is less than 1-2% of sales.

- It runs a capital-light, highly profitable business model that recycles capital exceptionally well and generates 30-40% return on capital investments.

- Gross and net margins are superb at 62% and 31%, respectively.

- Pays a respectable dividend each year, and repurchased $2.5Bn of stock in FY'22.

- This is a stock that has re-rated over $63/share in 10-years with just an additional $12mm and $5.1mm in revenue and earnings growth since FY'13, respectively.

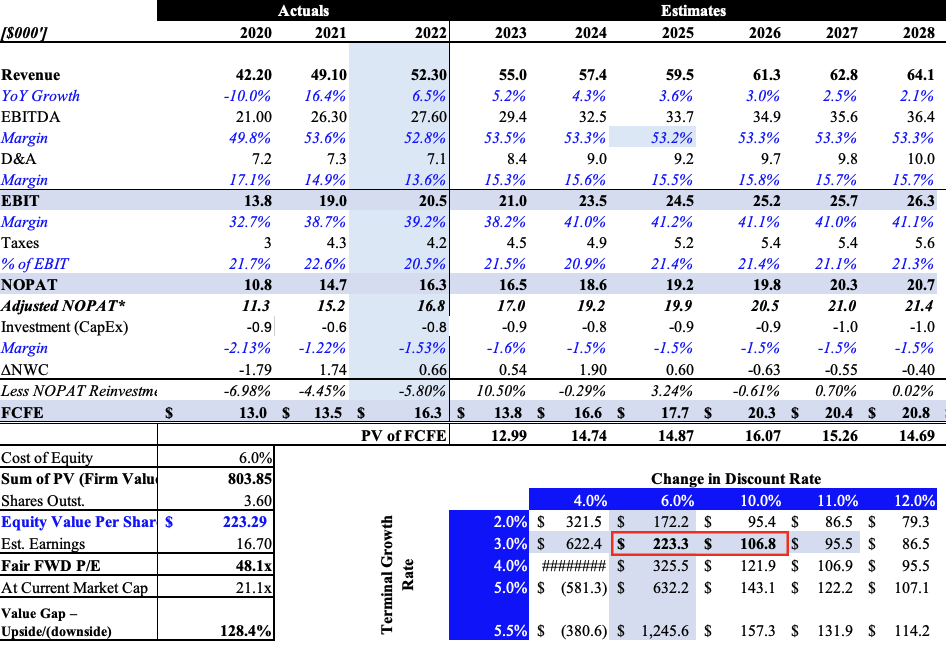

That in mind, I believe UTMD can capture 13-14% return on equity this year and generate $16.5mm in NOPAT to throw c.$14mm off to shareholders this year [dividends included]. My numbers have UTMD to compound earnings into FY'25E and reduce its capital requirements whilst increasing capital productivity. Net-net, I reiterate UTMD stock as a buy.

Fig. 1

{kind=link}

Fig. 1a

UTMD: an undercovered compounder

Understanding the investment debate here requires detailed knowledge of the key facts. Looking over a long-term horizon, I believe UTMD can unlock tremendous shareholder growth, and here are the details why.

One, UTMD is a business that needs to be examined in terms of profitability, and the cash it can throw off to shareholders (dividends included). This isn't a high-growing name, rather a mature value-proposition with attractive business economics. The outcome lies in the company's ability to generate and effectively manage surplus capital. Thankfully, management are entirely transparent on this in the 10-K:

"Management plans to utilize cash not needed to support normal operations in one or a combination of the following:

1) in general, to continue to invest at opportune times in ways that will enhance future profitability; 2) to make additional investments in new technology and/or processes; and/or 3) to acquire a product line or company that will augment revenue and EPS growth and better utilize UTMD's existing infrastructure.

If there are no better strategic uses for UTMD's cash, the Company will continue to return cash to stockholders in the form of dividends and share repurchases when the stock appears undervalued."

I can't help but notice management's focus on providing bold and constructive uses of capital from this language. Further evidence includes:

- Cash dividends + repurchases came to $5.7mm or 34% of reported earnings in FY'22. This was down from $11mm/78% if earnings the year prior.

- In FY'21, it returned $3.14 in cash to shareholders via dividends. I firmly believe this is a level the firm will return to over time.

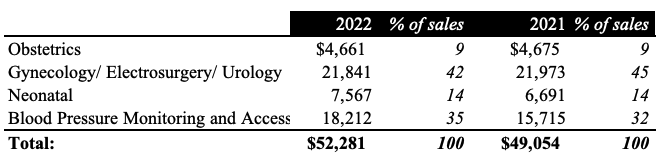

In that vein, it's important to understand what numbers we are dealing with. FY'22 U.S. sales came in 430bps higher YoY to ~$32mn, and contributed 61% of the top-line. Growth was underscored by upsides in Filshie Clip sales growth of ~14% YoY. Globally, neonatal and blood pressure/access segments grew substantially from FY'21 and contributed 14% and 35% of sales, respectively. It clipped $52mm in total revenues for the year.

Fig. 2

{kind=link}

Two, looking ahead, I believe UTMD can generate ~5% YoY growth in turnover to $55mm on gross profit margin of 62% in FY'23. On this, I expect operating leverage of ~0.48x and operating income growth of 2% this year. My numbers also bake in a higher than average COGS and OpEx to factor in the sticky manufacturing inflation. On this point, management have raised unit prices again in FY'23, whereas it expects demand to remain stable, contributing to my growth assumptions.

Three, as mentioned, UTMD has recycled capital effectively to generate substantial shareholder value. For example:

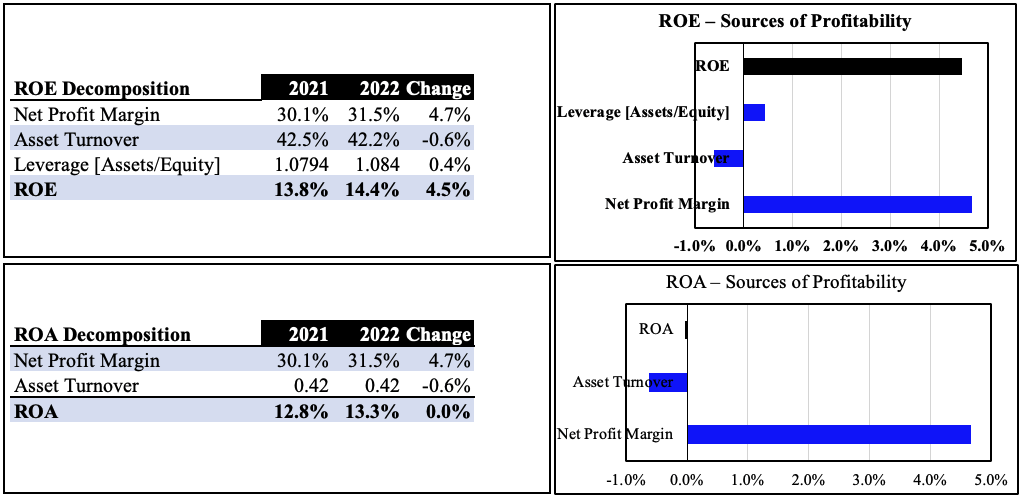

- Shareholder ROEs have remained in a 14-15% range sine FY'18, 15% in FY'22 before dividends [Figure 3].

- ROE driven by net profit margin versus leverage. Together, these are strong returns to equity holders.

- The providers of UTMD's capital have seen return on assets hover at 12-14% in the same time, 13% in FY'22.

- This, whilst its total capital base (equity + LT debt) has stretched up from $104mm to $120mm in that period.

- Equity holders have gained another $4 in book value per share, and claim an impressive $31 in book value/share at the time of writing.

Looking to my numbers a 14% ROE and 12% ROA for FY'23 is a fair range in my opinion. It wouldn't be unreasonable to observe it shifting higher to ~16% and 14% in FY'24, creating a further $2 in book value/share.

Fig. 3

{kind=link}

Four, UTMD has capital-light business economics allowing it to run a lean model to deliver economic profits to shareholders. I didn't call it an undercover compounder for no reason. Consider this:

- UTMD runs a handful of facilities with the bulk of its manufacturing located at Utah and Ireland.

- The invested capital base is very low to generate ~$4.60 in earnings per share last year. Keep in mind, this is off just $55mm in turnover. Earnings are therefore ~30% of revenues and this is very attractive value at 4.6% forward earnings yield.

- Net working capital requirements are ~$10mm to generate these numbers, with ~$0.5-$1.5mm additional NWC density each year to hit growth.

- The firm requires less than $1mm in maintenance/growth CapEx in order to grow its top-line or operating income.

- I envision this to continue, and my numbers forecast similar changes in NWC and CapEx.

You can see the invested capital turnover shifting up from FY'19 as a reflection of the capital efficiency, combined with ~30% NOPAT margin.

Fig. 4

Data: Author, UTMD 10-K

Five, it is comforting to see the capital is highly productive as well. Why? Because UTMD has generated persistently high rates of return over the cash it reinvests back into the business. It has averaged 30% ROIC since FY'18/19 and increased annual returns from 15% to 30% in that time [Figure 5]. Economic profit on this has trailed closely, signifying the compounding mechanics UTMD has in place.

The most attractive investment characteristic that I value above all is a firm's ability to allocate surplus capital at incrementally higher rates of return. There is no more valuable business my estimation. A 30% average return on new capital explains why shareholders receive ~$4.60 in earnings and $31 in book value/share - the company can throw off respectable rates of cash to its shareholders and so the earnings power is very attractive. Since FY'20 investors have seen their free cash flows convert at 91-120% of reported earnings (before dividends) and I expect this to remain on trend into FY'26 [Figure 6]. This is indulging for three reasons:

- The average 30% return provides adequate liquidity to fund growth investments and continue dividends, buybacks.

- That means it doesn't have to reinvest most of its profits to generate future growth - therefore, they are distributed to equity holders.

- This creates a consistent stream of cash flows with a high present value, well above UTMD's current market price.

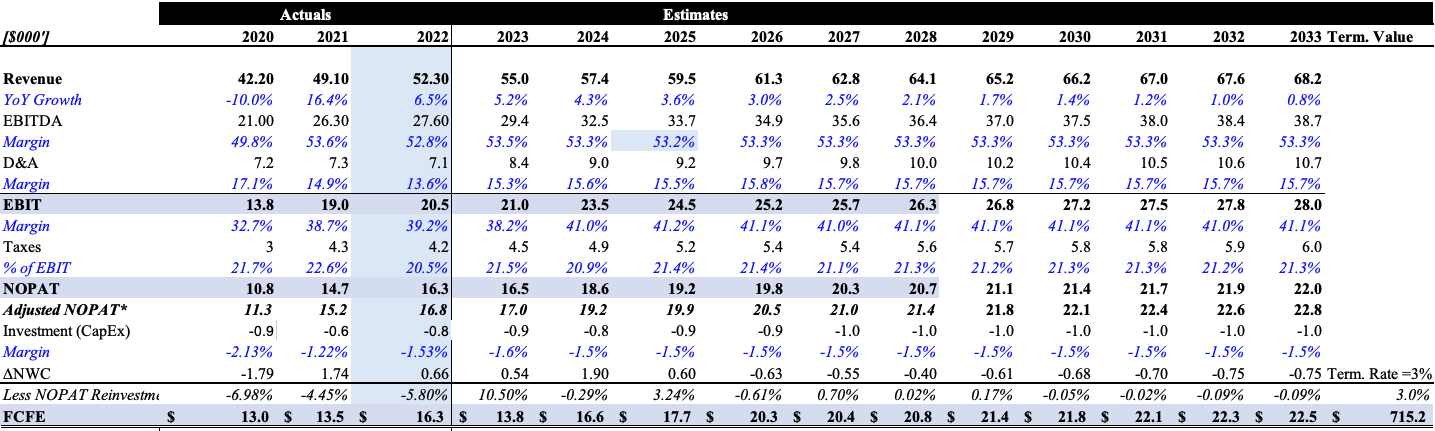

This underpins the bedrock of my investment thesis here. My numbers have UTMD to generate another c.28-30% return its capital investments in FY'23, verging on 35% in FY'24. At a 7% cost of capital (UTMD current WACC) the economic profitability is extremely valuable to shareholders in my opinion. Given these numbers, I believe UTMD can throw off $13.2mm to its shareholders this year, growing this number at a sustained rate into FY'28.

Fig. 5

Data: Author, UTMD 10-K

Fig. 6

Data: Author, UTMD 10-K

Valuation and conclusion

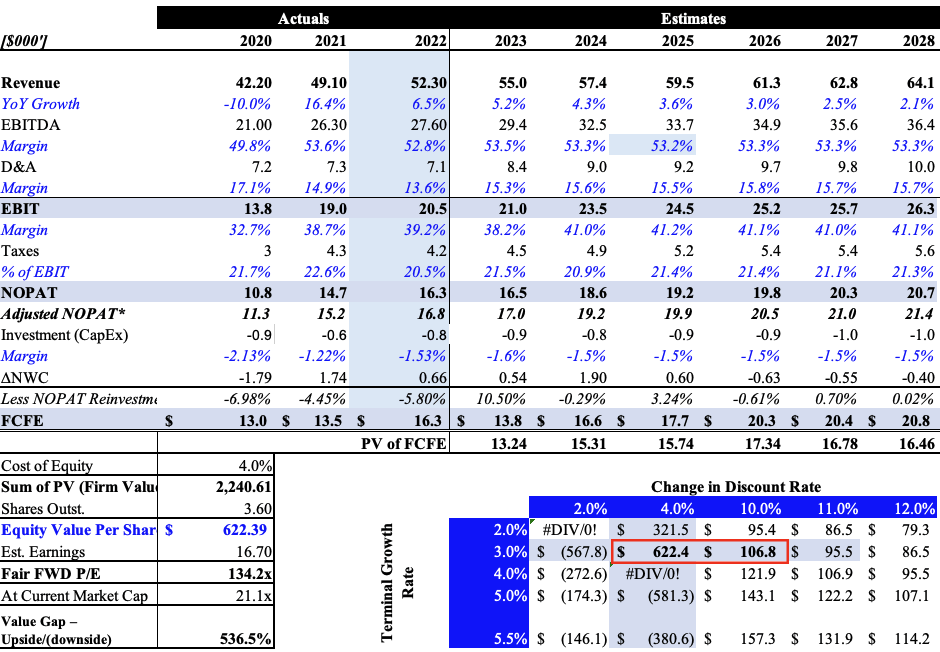

With shares priced at 21x trailing earnings I believe this does UTMD a great disservice. After all of the positive points raised so far, an informed appraisal of valuing UTMD is justified. My numbers call UTMD to generate $16.5mm in NOPAT this year on $29mm in core EBITDA, and this could increase at a fairly linear rate if the company continues on its current run rate.

Looking out to FY'28 to avoid forecasting risk, I've made 2 scenarios, with a 4% and 6% discount rate respectively, over the cash UTMD can generate for shareholders over this time. My conclusions on the firm's valuation are as follows:

- Discounting at 4% values the company at 134x my FY'23 earnings estimates, on a market cap of $2.2Bn.

- The market has UTMD valued at 21x my forward earnings estimates.

- Adding 200bps more risk to the outlook, the firm is valued at 48x forward earnings estimates.

- This reigns in to $223-$623 per share, and I don't believe this is unreasonable given the long-term range I am looking at UTMD over.

- The former is a 12% CAGR over 7 years, completely in the realms of possibility in my opinion.

Therefore, this supports my buy thesis and I am reaffirming the buy call on UTMD after these additional findings.

Fig. 7

{kind=link}

Fig. 8

{kind=link}

Fig. 9

{kind=link}

For further details see:

Utah Medical Products: Recycling Capital Well, Long-Term Gains On The Table