UTG - UTG: 8.3% Dividend At Risk

2023-07-06 11:58:27 ET

Summary

- The Reaves Utility Income Trust is underperforming due to falling energy prices and rising interest rates, which are affecting its high-dividend-yielding investments in the utility industry.

- UTG's external leverage strategy, which has increased from 16% in 2020 to 24% in 2023, is magnifying capital depreciation and increasing exposure to struggling utility equities.

- UTG's distribution policy is unsustainable as it relies heavily on capital gains to maintain dividends, despite falling stock values; this puts the current 8.3% yield at risk.

Reaves Utility Income Trust ( UTG ) is a closed-end fund with an investment objective to provide attractive after-tax return stemming mainly from tax-advantaged dividends.

UTG seeks to invest at least 80% of its assets in high dividend-yielding common and preferred stocks and fixed income instruments of companies exposed to the utility industry. The Management also holds the option to employ leverage with an intent to enhance the dividend yield.

{kind=link}

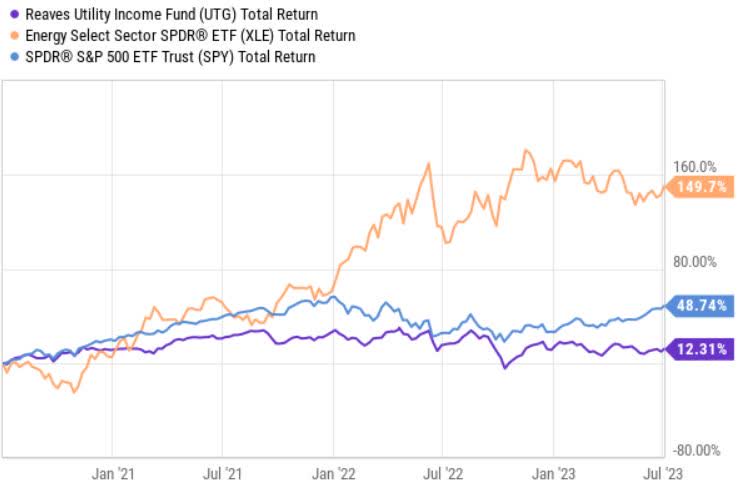

The recent performance of UTG on a total return basis has been rather weak. Since the FED switched gears from stimulative to restrictive monetary policy in early 2022, UTG's performance has been flat yielding significantly lower results compared to the SPDR S&P 500 ETF Trust ( SPY ) and its benchmark the Energy Select Sector SPDR ETF ( XLE ).

{kind=link}

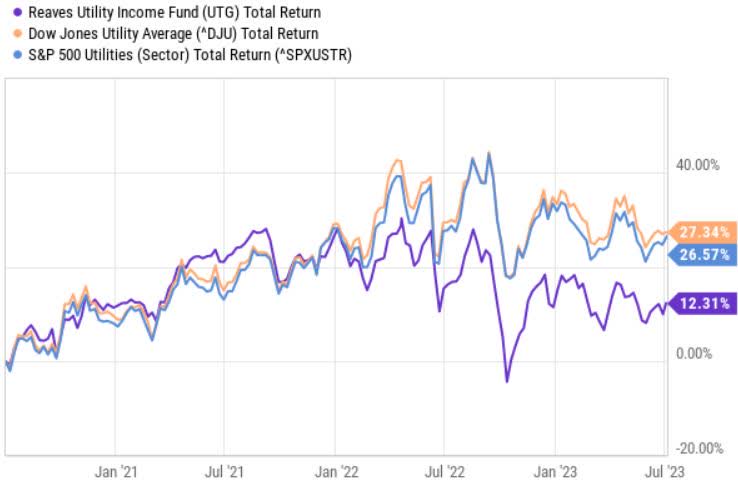

The underperformance is still there if we compare UTG to some popular indices, which carry more pronounced factor exposures towards utility segment.

3 reasons why UTG's dividend is at risk

Considering UTG's investment objective and high yielding dividend, the CEF is naturally being viewed as a dividend stock that is mostly preferred by dividend-seeking investors. So, below, I will outline the key elements that have a high potential for imposing serious headwinds for UTG's ability to maintain the current dividend and keep its dividend track-record clean.

{kind=link}

#1 High concentration towards falling energy prices

As of now Q1, 2023, UTG had roughly 65% of portfolio invested in utility and energy segments. Looking at the Top 10 holdings, we can clearly see that there is a notable skew towards energy factor / risk.

Reaves Asset Management

Entergy Corporation ( ETR ), Xcel Energy ( XEL ), Ameren Corporation ( AEE ), Alliant Energy ( LNT ), Duke Energy ( DUK ), DTE Energy Company ( DTE ), NiSource Inc. ( NI ) and NextEra Energy, Inc. ( NEE ) are all energy utility stocks, which in the past year have experienced negative share price performance.

The energy prices have gone down sharply, putting a pressure on the future earnings for majority of UTG's top holdings.

{kind=link}

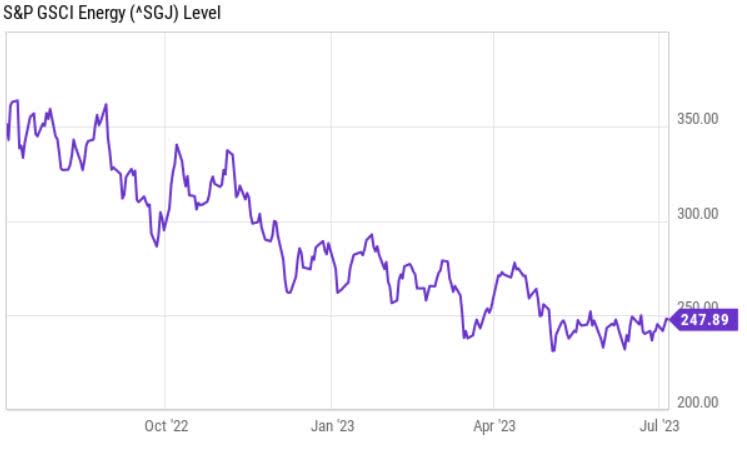

Looking at the investment performance in the energy commodity market, we can see a notable deterioration of financial prospects. Granted, the utility names included in the UTG's portfolio do not perfectly correlate with the dynamics in the energy commodity markets as these companies have relatively diverse set of business activities they perform (e.g., not only energy generation, but also distribution, storage etc.). Furthermore, some of the energy sales are underpinned by tariff and State compensation mechanisms guaranteeing certain profitability levels. Yet, the weakening of energy markets does put a downward pressure on the current profits; essentially resulting in totally understandable convergence to a more normalized levels of energy prices.

Moreover, most of the utility names are highly leveraged due to the constant need for sizeable maintenance CapEx and ambitious targets to expand in the renewable energy space. High leverage is also justified by the stable and predictable streams of income stemming from regulated and inherently defensive business activities (e.g., energy transmission, distribution and sale).

The notion of high indebtedness in conjunction with surging interest rates creates an additional impediment for future earnings stability.

#2 External leverage magnifying the capital depreciation

Historically, UTG has applied external leverage to enhance the yield potential from its portfolio. UTG's leverage was ca. 24% of net assets on April 30, 2023 - mainly constituting of a credit agreement based on SOFR plus 0.65% with a weighted average interest cost of 4.99%.

Starting from 2020, UTG has increased its reliance on additional leverage from ~16% in 2020 to ~24% in 2023.

We can also see how UTG is becoming more aggressive in maintaining the dividends by allocating most of its capital in equity instruments, while the mandate allows the Management to consider preferred and fixed income alternatives. Currently, UTG holds less than 1% in preferred stocks and fixed income instruments. This means that all of the assumed external leverage has been directed towards increasing the exposure to, primarily, utility equities.

Nevertheless, if we look at the underlying yield levels offered by the key equity exposures - utility, telco and REIT -, it is evident that on an unlevered basis their dividends do not support the current yield of 8.3%. The average unlevered dividend yield of utility, telco and REIT stocks is around 4%, 7% and 4%, respectively.

Yet, even if we factor in the 25% leverage (including the corresponding costs of financing), 8.3% yield does not seem to be fully warranted by the underlying cash flows as the spread between the current yield and the blended average of levered yields is too wide.

Finally, the presence of external leverage does not only provide an opportunity to boost the yield potential, but also magnifies the downside risk. Against the backdrop of falling energy prices, structural headwinds for utility stocks and what we already have seen on the stock price performance front, it is clear that UTG's chances to service dividends via realizing capital gains are diminishing.

#3 Unsustainable distribution policy

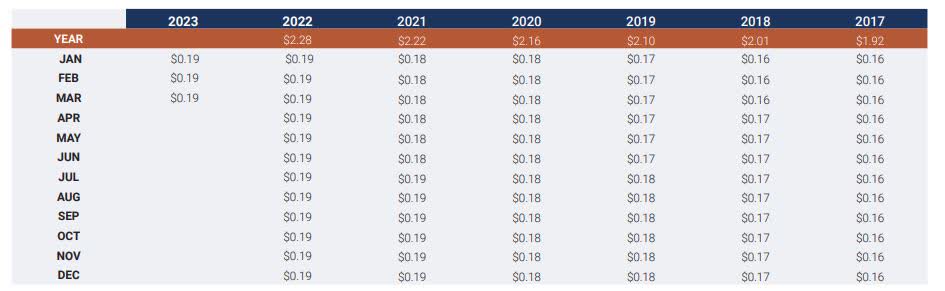

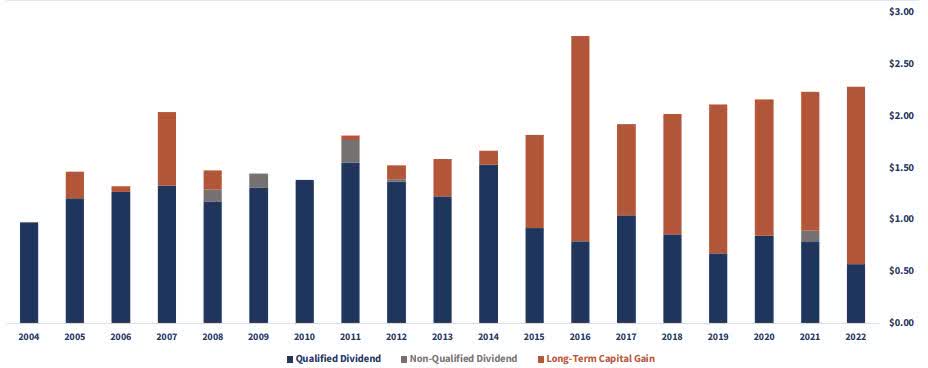

Historically, UTG has managed to deliver growing dividends in a very stable and predictable fashion. The distributions have been supported from two sources - dividend income from the investments and realized capital gains.

{kind=link}

In theory, there is nothing wrong about servicing dividends through a realization of capital gains component. However, this strategy is sustainable and prudent only under scenario in which the underlying investments increase in value, otherwise there is a risk of tapping into existing NAV (including the unrealized losses) to sponsor distributions.

In UTG's case, we can see how the Fund has been relying more and more on the capital gains element to comply with its dividend policy. On a YTD basis, UTG has distributed roughly 66% of its capital via the capital gains component, which is despite the fact that the underlying stock values have fallen.

Again, given that the structural dynamics indicate unfavourable ride for UTG's investments going forward (certainly, relative to the period when energy prices were skyrocketing), the current dividend policy is clearly at risk.

The bottom line

UTG is facing notable headwinds, mainly via decreased energy prices and surging interest costs, which make the external financing more expensive and impair the financial prospects of the highly leveraged utility, telco and REIT investments.

Considering that the UTG's dividend coverage is mostly based on divestments of stock that have experienced capital appreciation, the current 8.3% yield is at risk.

For further details see:

UTG: 8.3% Dividend At Risk