UTG - UTG: From Bad To Worse

2023-11-02 12:21:20 ET

Summary

- Reaves Utility Income Trust has seen a negative performance and a 10% drop in price return, indicating an increased risk given the reliance on capital gains to fund the dividend.

- The concentration in energy stocks, reliance on external leverage, and unsustainable distribution policy pose significant risks to UTG's dividend sustainability.

- The current macro environment, with elevated interest rates and debt-saturated balance sheets of CapEx intensive businesses that are owned by UTG, further increases the risk for UTG to rely on capital gains.

About 3 months ago I published an analysis of Reaves Utility Income Trust ( UTG ) arguing that the Fund's seemingly attractive dividend yield is at risk.

It was a combination of three factors, which together constituted a significant risk for the sustainability of UTG's dividend and its more than a decade prestige of delivering growing distributions.

First was the concentration in energy stocks, which at that time had already started to assume a negative performance trajectory.

Second was the reliance on external leverage, which made the declines more tangible. The leverage itself was subject to a potentially unfavourable repricing, thereby weakening the prospects of net cash generation.

Third was the inherently unsustainable distribution policy, which heavily relied on capital gains component to make the dividends (distributions) consistent.

{kind=link}

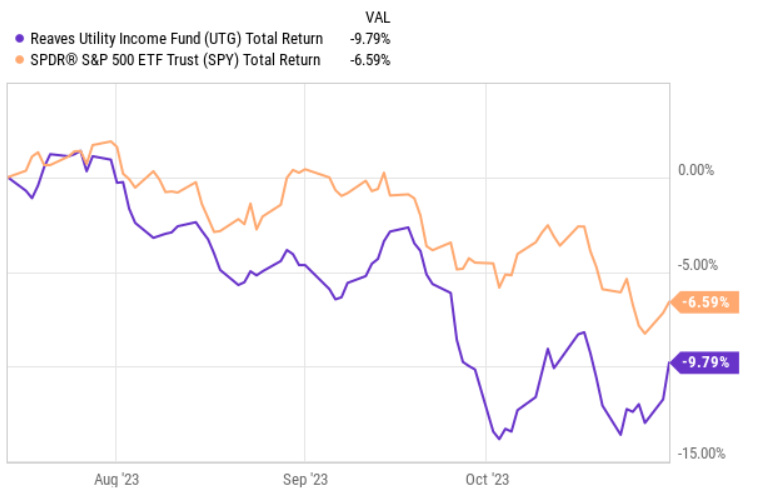

In this 3-month period, UTG has registered a negative 9.8% performance unperforming the S&P 500 by ~ 300 basis points. On a price return basis, the Fund is down by 11%.

It seems that the market is slowly recognizing the underlying risk in UTG. While ~11% drop is nothing major and some investors could view this as an interesting buying opportunity, the truth is that the risk profile of UTG has gone from bad to worse.

Let me explain why this is the case.

Thesis updated

Historically, UTG has funded its dividend both from net income (i.e., received dividends from the portfolio investments) and capital gains. Capital gains component just as in the YTD figures below has assumed a more dominant role in funding of UTG dividends.

REAVES UTILITY INCOME FUND SECTION 19(a) NOTICE

Now the question is whether UTG will enjoy the same luxury of consistently growing portfolio holding values that could be used to accommodate the ~9% yielding dividend.

{kind=link}

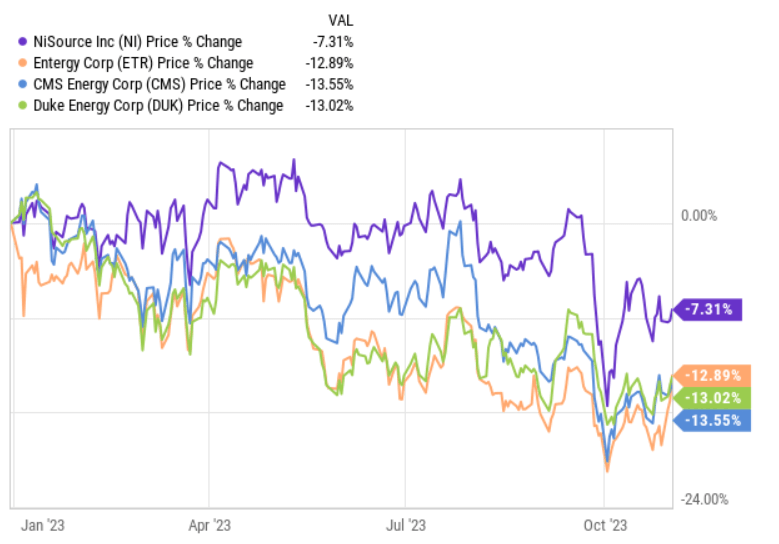

On a YTD basis most of the top UTG's holdings are down and the drivers of this correction seem more structural and potentially long-lasting.

The key problem within UTG's holdings is that almost all of the portfolio constituencies are CapEx intensive businesses, which require notable streams of external financing. Against the backdrop of higher interest rates, CapEx intensive businesses are set to suffer from pressured margins due to more elevated interest costs. The problem is not only related to incremental debt financing but also to the repricing of the existing debt, which per definition is not low for utilities, telcos and infrastructure companies.

Another problem that stems from the "higher for longer" scenario is that there is an unfavourable pressure on the valuations, which is more pronounced for UTG investments because of some inherent similarities to fixed income securities (or cash flow characteristics).

REAVES UTILITY INCOME FUND SEMI-ANNUAL REPORT

{kind=link}

Moreover, we have to consider that UTG has taken an external financing to enhance the underlying yield of its investments. This strategy has worked nicely during low interest rate environment and when the prices have consistently ticked higher.

Yet, now the magnified effects impact the results on the opposite side.

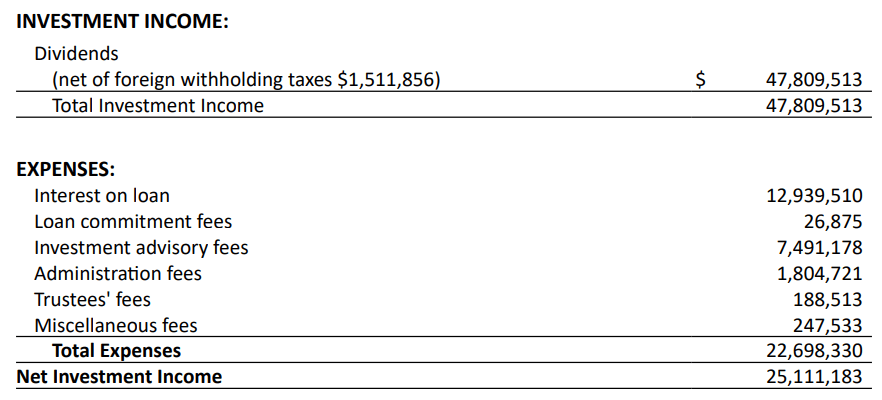

Currently, UTG has borrowed ca. $0.5 billion at a weighted average rate of 4.99% . There are some hedged attached to this funding, but these are of a short-term nature. On a go forward basis we should see additional headwinds from this as the debt gets slightly repriced to market levels.

In the latest report UTG's interest cost payments consumed ~27% of the investment income. This is significant especially in the context of a structural reliance to further capital gains to fund the dividend (i.e., increasing the reliance on capital gains).

Upside risks

Granted, the entire thesis update revolves around higher interest rates, which intensify the aforementioned risk exposures.

At the same time, if the interest rates revert back to historical levels or even assume a trajectory of a gradual normalization, most of UTG's positions would be subject to favourable repricing. This, in turn, would provide UTG with more capital gains from which to fund the dividends. Also, it would effectively neutralize any further risks that are associated with external leverage as the debt service costs would remain stable or even decrease.

Bottom line

It is critical to underscore that I am not plotting a short sale thesis for UTG. Instead, my goal is to highlight some of the risks, which are not directly observable from the first glance.

Some investors might get the feeling that UTG is an extremely resilient Fund and that its remarkable dividend history is a clear testament of that. UTG also holds an exposure towards some of the most (commonly deemed) defensive sectors of the economy, thus creating an impression that the dividends should be safe.

In my opinion, we have entered a different macro environment, where what has worked in the past might very likely not do the thing now.

The systematic risk in UTG's case has increased due to the elevated interest rates and the bias of the portfolio companies towards a debt saturated balance sheets. On a UTG-specific level, the risks are magnified due to the reliance on external leverage and seemingly unsustainable dividend policy. Namely, the sustainability of its dividends depend on the future capital appreciation of the underlying portfolio companies.

For me, this does not sound like a right strategy even though historically the markets have gone nowhere but up.

In my humble opinion, UTG is not the right vehicle for investors, who want to have a reliable stream of dividends in their portfolios. Of course, the probability is still there that UTG will continue to service its existing distribution level, especially if the interest rates decrease. However, at this moment, the overall odds are stacked against it.

For further details see:

UTG: From Bad To Worse