CMCSA - UTG: Not Worth The Risk

2023-11-06 08:00:00 ET

Summary

- Reaves Utility Income Trust is a cross-sector fund focused on dividend-producing stocks in Utilities, Telecom, Cable, REITs, and Rail Transport.

- The fund has outperformed sector-focused ETFs and has a well-diversified portfolio.

- However, the fund has high leverage and increasing capex, which may impact cash flow and dividend payout capacity.

Summary

The Reaves Utility Income Trust ( UTG ) is an interesting closed end fund, with a cross sector focus on dividend producing stocks in Utilities, Telecom, Cable, REITs, and Rail Transport. While REITs are designed to produce dividends, the other sectors are considered high dividend payers due to the low growth, low capex, and high free cash flow business model i.e., mature companies, they payout this excess cash to shareholders in leu of EPS growth.

I see two key drivers for the fund. The first is positive, the potential for lower risk-free rates. The second is a major risk driver, dividend cuts at electric utilities, which is highlighted in a recent article.

XLU: Higher Rates Hurt (NYSEARCA:XLU)I have a preference for pure REIT ETFs as seen in this article: SCHH ETF: Speculative Buy On Fed Pivot

Performance

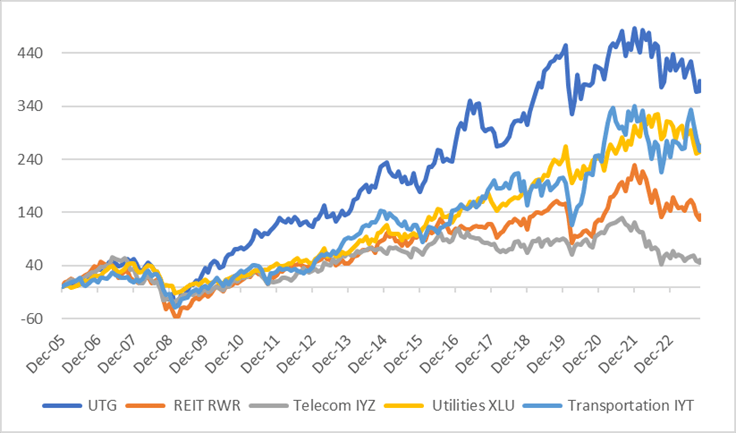

UTG has substantially outperformed the sector focused ETFs, which suggests that this combination of assets has worked well in the past. Since the start of the recent tightening cycle the utility sector has been resilient up until just recently as long-term bond yields pushed to 5%.

UTG Performance Since Inception (Created by author with data from Capital IQ)

{kind=link}

UTG Performance vs Comps (Created by author with data from Capital IQ)

Portfolio Overview

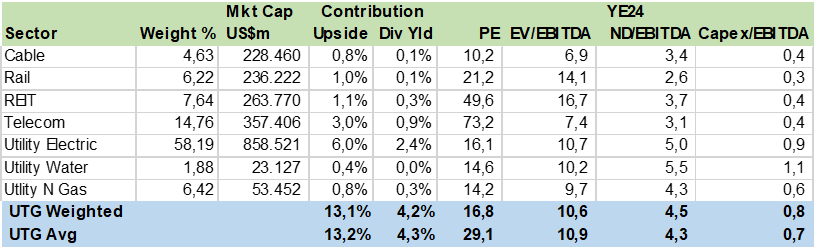

The UTG consists of 48 stocks, about 58% of the fund is in the Electric Utility sector followed by 15% in Telecom with the average weight at 2.2% suggesting this a well-diversified portfolio. I used consensus estimates on 99% of the AUM to run a series of metrics to better evaluate the fund. In the table below I calculated potential upside of 13% and a 4% dividend yield with consensus price targets and DPS (dividend per share) for YE24.

What struck me as worrisome is the leverage indicator. The fund has a ND (net debt) to EBITDA ratio of 4.5x with the utility sector at 5x. In addition, a good measure of free cash flow potential is capex to EBITDA i.e., how much is a company investing as a percentage of it cash generation. Here again the Electric utility sector stood out on the negative side with 90% of EBITDA going to capex.

UTG Consensus Sector Breakdown (Created by author with data from Capital IQ)

{kind=link}

UTG Consensus Price Target (Created by author with data from Capital IQ)

{kind=link}

Leverage Is A Risk

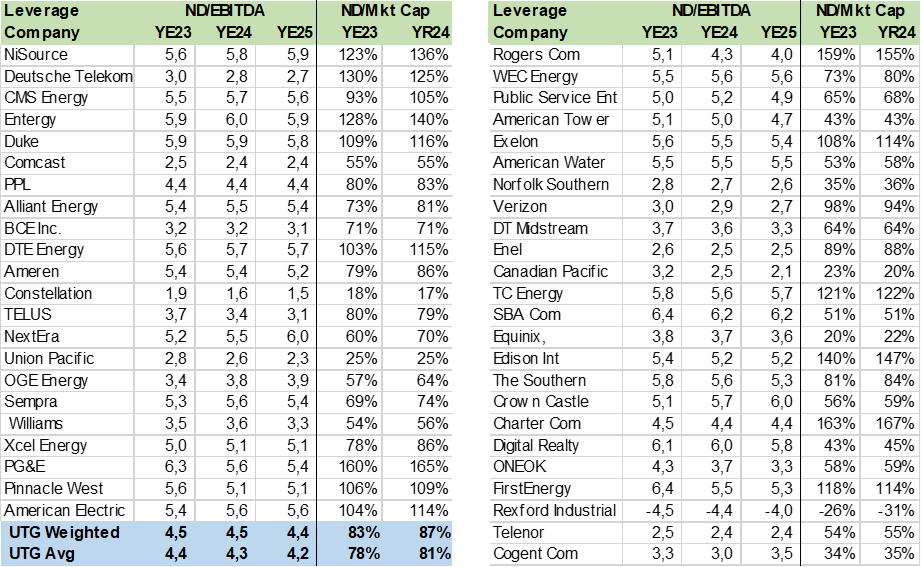

Leverage was not a problem when the cost of debt was 2% or 3%. However, with corporate bond rates at 6%-10%, the debt cost may become a problem. Companies will need to roll over debt or seek more funding at higher levels and this may start to impact cash flow and perhaps the ability to fund capex and dividends.

In the table below I calculated two leverage metrics using consensus estimates. UTG has not only a high ND/EBITDA but that ND is slated to reach 87% of market cap in YE24. This makes the stocks highly susceptible to the cost of money. Of notice is Charter Communications ( CHTR ), it is cutting dividends and has a 163% ND/Mkt Cap ratio. While PG&E ( PCG ) is now starting to pay dividends on declining debt.

UTG Consensus Net Debt & EBITDA (Created by author with data from Capital IQ)

{kind=link}

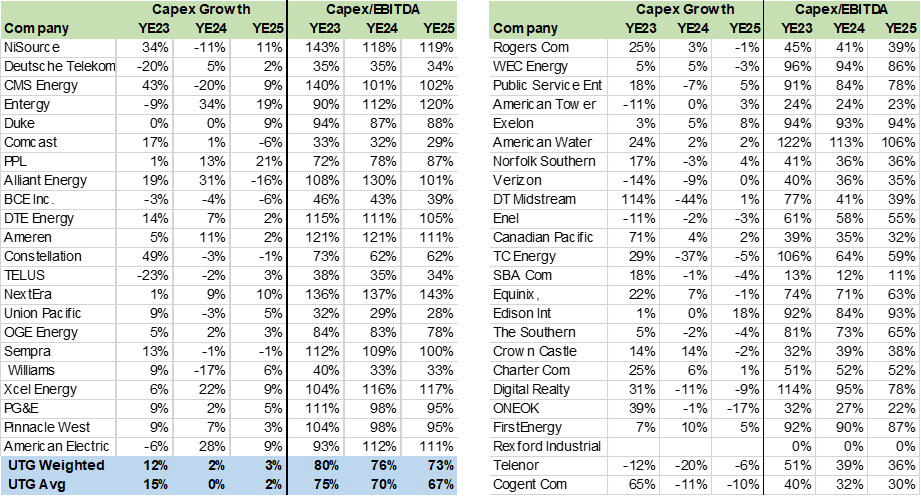

Capex On The Rise

As I mentioned at the start of this analysis, companies that pay dividends, by default, are those generating free cash flow and that generally means low capex or low required investment to maintain the business running at a slow, mature pace. The opposite is generally true, high capex to acquire or build assets, conduct research & development etc. is used to drive growth. The best companies can invest moderate amounts and achieve high and consistent growth i.e., the tech sector.

Using consensus estimates I calculated the Capex growth and more importantly the ratio of capex to EBITDA, which illustrates how much a company is using cashflow to fund investment. The market average is 45% , the lower the ratio means more EBITDA is available for dividends or share buy backs. According to the consensus, the fund is running a Capex/EBITDA of 76% with the Utilities at 90% on average. In my view, this may risk dividend payout capacity and impact the value of the fund. NextEra ( NEE ) stands out for capex spending at near 140% of EBITDA, while Comcast ( CMCSA ) and Telenor ( OTCPK:TELNF ) are below 36%. REITS are by structure low capex/EBITDA business models.

UTG Consensus CAPEX (Created by author with data from Capital IQ)

{kind=link}

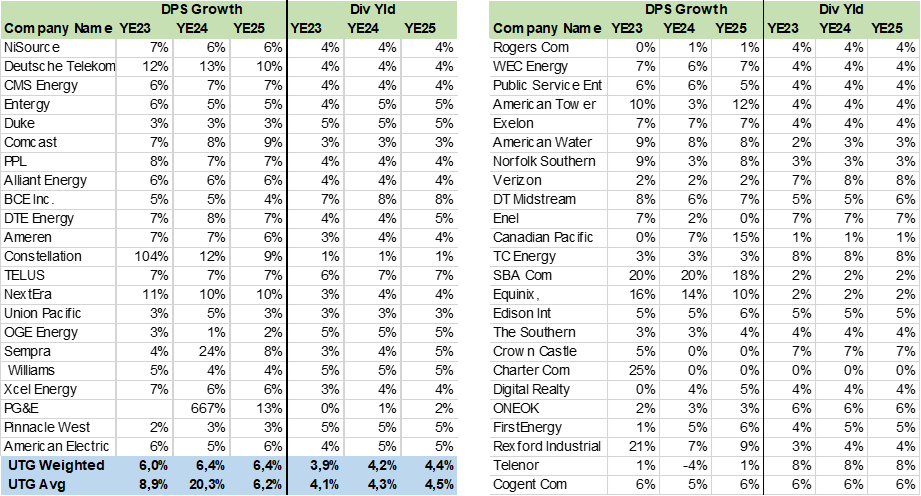

Dividends Inching Up

Using consensus estimates I calculated the funds DPS growth of 6.4% and a 4.2% dividend yield for YE24. In my view, this is not a great result and more indicative of the challenges the electric utility sector may have due to low free cashflow, and high capex needs. Verizon ( VZ ), Enel ( OTCPK:ENLAY ), Crown Castle ( CCI ) and BCE ( BCE ) are a few that stand out with over 7% Yields.

UTG Consensus Dividends (Created by author with data from Capital IQ)

{kind=link}

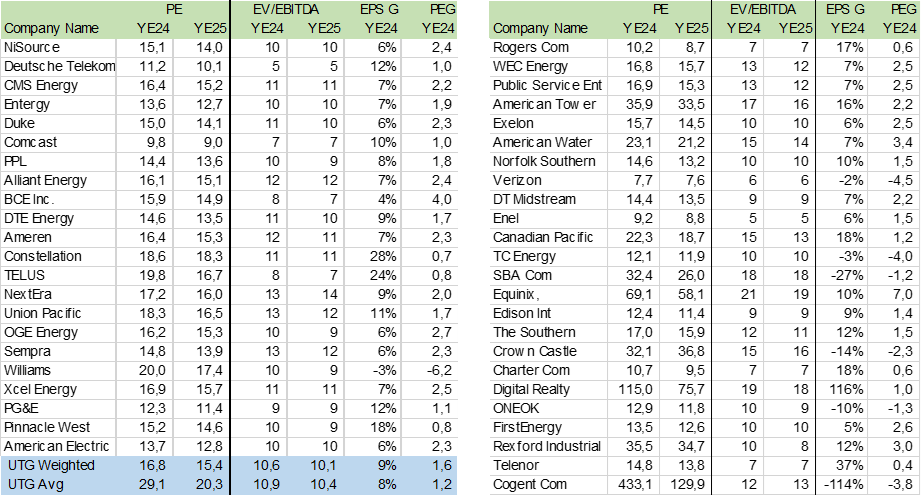

Valuation

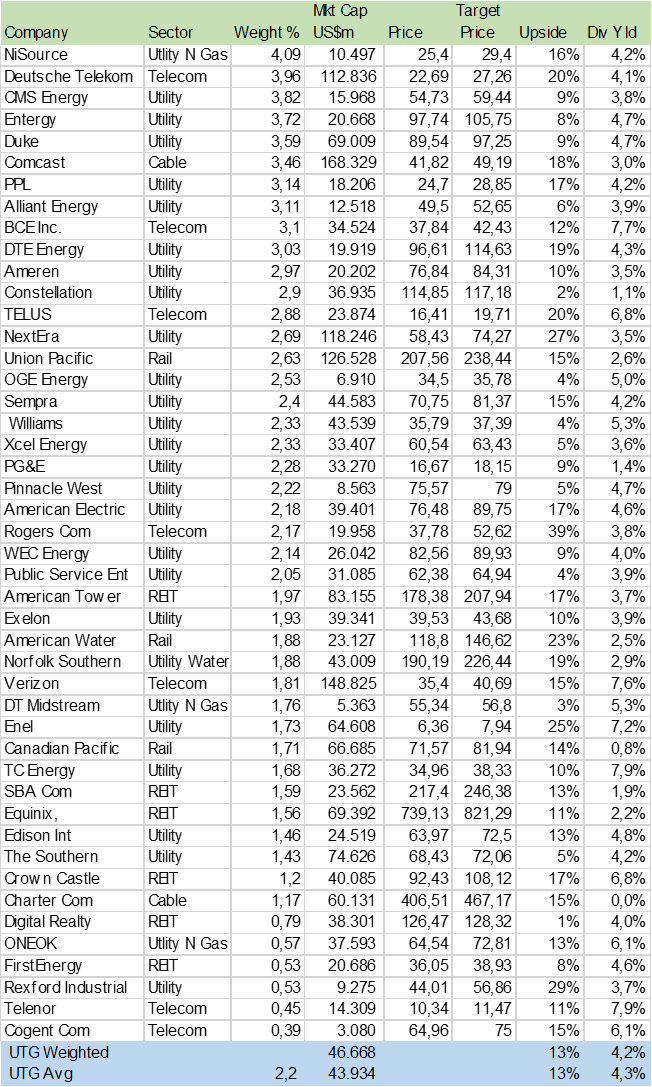

This is a tough fund to value given the sector mix, in particular the REITs that require a P/FFO metric. On consensus estimates I calculated the forward PE and EV/EBITDA for the portfolio and compared it to EPS growth to derive a PEG ratio. Here I excluded the REITs and some stocks with negative EPS growth. The conclusion is that this fund is not terribly expensive at 1.6x PEG or 16.8x PE YE24 but neither is it a value portfolio, which would require a PEG under 1x. Favorable outliers are Deutsche Telekom ( OTCQX:DTEGY ), Rogers ( RCI ), Constellation ( CEG ) and Pinnacle West ( PNW ).

UTG Consensus Valuation (Created by author with data from Capital IQ)

{kind=link}

Conclusion

I rate UTG a hold. While its track record is impressive, I find the electric utility sector at risk of reducing dividends as 90% of EBITDA is used to fund capex while it is increasing debt at higher rates that may squeeze free cash flow. At the same time the UTG's capital upside and dividend yield do not compensate for this risk, especial in a higher rate world.

For further details see:

UTG: Not Worth The Risk