XLC - UTG: Solid Utility Fund For Income-Oriented Investors

2023-12-09 09:04:30 ET

Summary

- Reaves Utility Income Trust is a solid closed-end fund that has been able to deliver consistent distributions to its investors since its launch.

- UTG's performance has been impacted negatively by higher interest rates in more recent years, but with rates receding, it could turn into a tailwind.

- The fund's distribution has been steadily increasing, and while utility performance has been lackluster, I don't believe we are in danger territory in regard to a cut in the distribution.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Reaves Utility Income Trust ( UTG ) remains a popular closed-end fund with income investors. It's one of only several CEFs that have an inception prior to the global financial crisis that has also never reduced its distribution. That means it has gone through the GFC and Covid without significant damage. Being a fund that emphasizes utility exposure is certainly one of the key reasons for this type of results.

However, with higher interest rates, UTG faced a new threat. One that pressures utilities more acutely, and given the borrowings employed by UTG, its investment income was also pressured. Some funds hedged against higher rates, UTG wasn't one of them and that certainly is a negative mark on the management team here.

That said, rates have been receding, with the 10-Year Treasury Rate coming off of its latest highs when it was pushing ~5%. With the Fed looking about done with further rate hikes, what was a headwind could turn into a tailwind for the fund if rates recede further. For this reason, I believe that UTG remains a 'Buy,' as I did rate it earlier this year .

I think that UTG is one of the set-and-forget types of CEFs that doesn't necessarily have to be traded around. However, it would appear all other investors also view this fund favorably and trying to get this fund at a screaming bargain is tough. The fund has barely traded at any meaningful discount for an extended period of time for several years now.

The Basics

- 1-Year Z-score: 0.13

- Premium: 0.42

- Distribution Yield: 8.71%

- Expense Ratio: 0.93%

- Leverage: 21.07%

- Managed Assets: $2.467 billion

- Structure: Perpetual

UTG's investment objective is "to provide a high level of after-tax total return consisting primarily of tax-advantaged dividend income and capital appreciation." To achieve this, the fund "intends to invest at least 80% of its total assets in dividend-paying common and preferred stocks and debt instruments of companies within the utility industry."

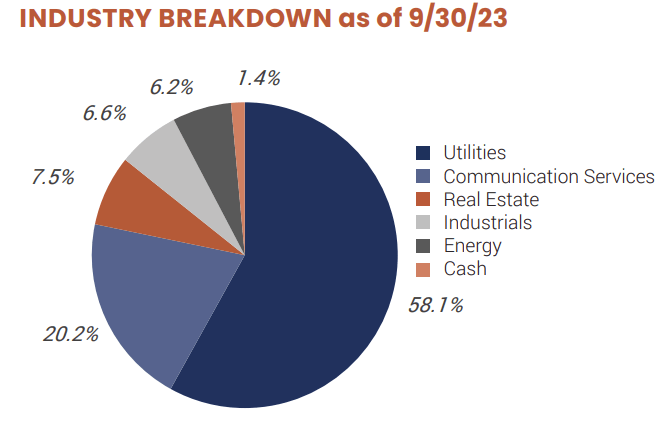

That leaves 20% outside of the utility sector. However, they are fairly liberal with what they coin as "utility," which can also include various holdings from the communication services and real estate sectors as investments. Here's a look at the overall sector breakdown as of their last fact sheet .

{kind=link}

They also leave it open for further flexibility with investing across asset classes, but really, they are almost entirely invested in equity securities.

The fund runs with leverage in the form of borrowings from a credit facility. With higher interest rates, that has seen their borrowing costs rise. Their expense ratio is fairly low for a CEF, but when including the borrowing costs, the total expense ratio comes up to 2.17%. That was as of their last semi-annual report for the six months ended April 30, 2023. The Fed has bumped up rates higher since then, so we would anticipate that would have also increased some since this last report.

Performance - Utilities Face Pressure But Valuation Remains Tight

Since the Fed began increasing interest rates, utilities overall haven't performed particularly well. In this case, UTG has underperformed since the start of 2022. As we can see below, though, it isn't as though the Utilities Select Sector SPDR ( XLU ) has had performance to boast about either during this time.

YCharts

UTG also carries some exposure to the communication services sector, the more traditional telecom companies within that space - not Meta Platforms ( META ) or Alphabet ( GOOG ) ( GOOGL ), which make up the largest allocation of the Communication Services Select Sector SPDR ( XLC ). Those two companies make up almost 49% of the ETF's weighting, which has heavily skewed the performance.

UTG has also had a sleeve of real estate exposure, which is another area of the market that has been under pressure due to higher rates. As soon as we started to see those rates ease, we started to get a rebound in both the utility and REIT space. Given the outlook is for rates to come down next year, there is a good chance that Treasury Rates could face continued pressure, and therefore, UTG could be looking to a bargain at these prices.

On the other hand, the unfortunate part about UTG is that the fund's premium has remained relatively sticky. Even despite the pressures within this space, investors seem to continue to be willing to drive the fund to trade at parity with its NAV per share. This is quite rare for a CEF, but in fact, since going back to around Covid, investors have not let UTG trade too drastically far away from its NAV per share.

YCharts

However, as we can see above, that hasn't always been the case. UTG was like most other CEFs in that it traded at discounts or premiums, and it sometimes varied wildly. For that reason, while utilities look like a bargain and could have further tailwinds driving them higher, UTG isn't a screaming buy until we see a wider discount.

One fund that did hedge its leverage was its peer, Cohen & Steers Infrastructure Fund ( UTF ), which frequently gets mentioned alongside UTG. That said, while UTF did outperform UTG since the beginning of 2022, it wasn't by any landslide outperformance. UTF had been facing the same types of pressures of higher rates impacting their underlying holdings, which also include some REIT investments and more global exposure.

YCharts

UTF runs with higher leverage, and that was likely a contributing factor to seeing it perform just about as poorly as UTG during this time. They might be hedged, but when most of what you are investing in is facing pressure, and you are investing in more of it, losses will also be higher.

Distribution - Steady

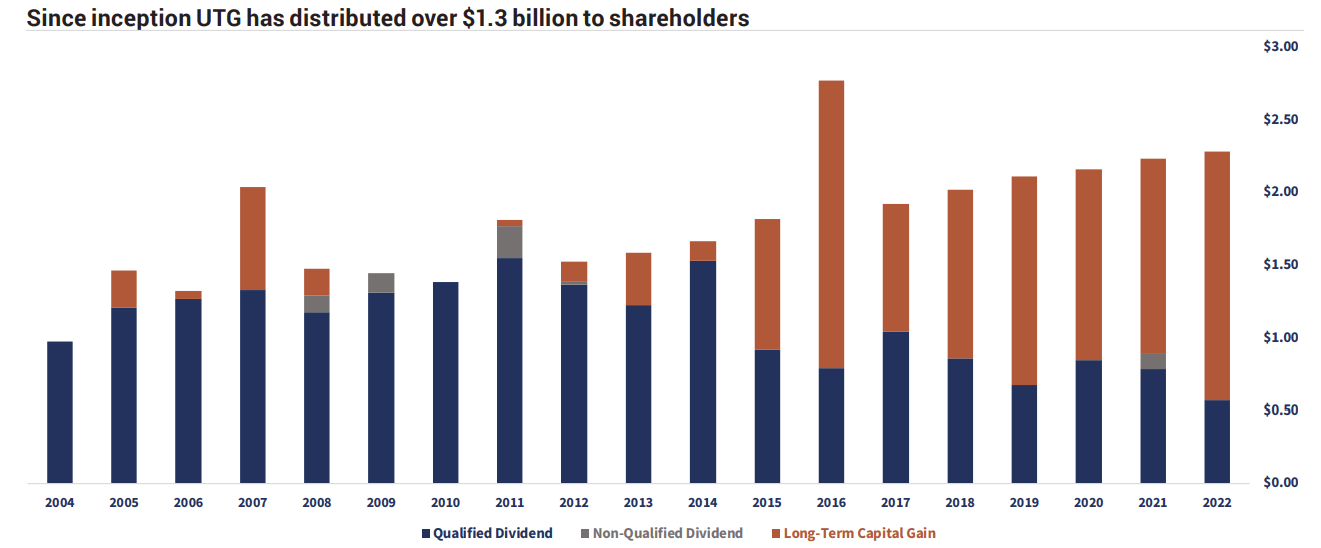

As noted at the open, UTG's distribution has been incredibly steady. Well, I guess it would be even more appropriate to call it a steady ascension, as the fund has increased on a number of occasions since its launch.

{kind=link}

The overwhelming majority of the distribution has been characterized as qualified dividends or long-term capital gains. That can make it incredibly tax-friendly if held in a taxable account.

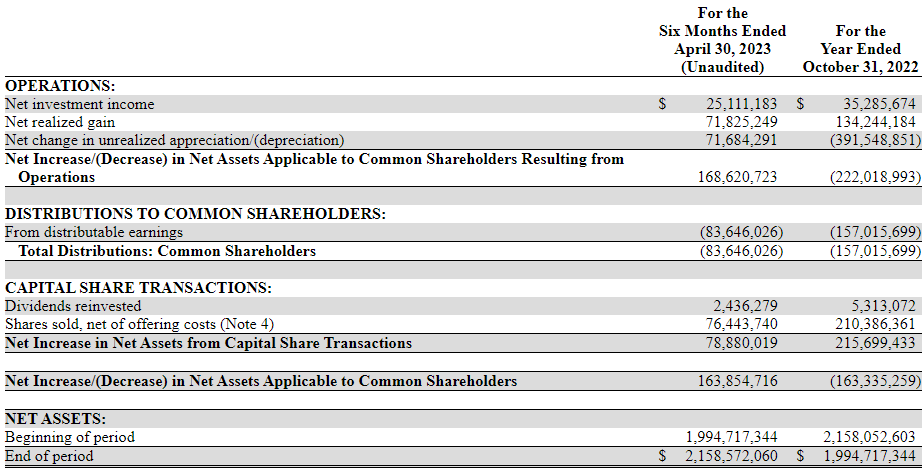

One thing that one might point out is that they have been relying more on capital gains over time, and that is quite true. However, with the latest semi-annual report - despite the rising leverage costs - we've seen that NII is looking to rise. Of course, those leverage costs meant that, relatively speaking the rise here would have been less than it otherwise would be, but seeing NII head higher is still encouraging.

{kind=link}

On a per-share basis, NII for fiscal 2022 came in at $0.51, and in this report, if it was annualized, it was on pace for $0.68 NII per share. The fiscal year-end is actually over, but CEFs have some really big leeway for reporting up-to-date information. They haven't historically released their annual report until early January of the next calendar year.

So we won't get the exact amount NII was for fiscal 2023 for a bit of time yet. However, with the anticipation of potential gains returning with lower rates and higher NII, the distribution coverage should be heading in the right direction. Given the fund's NAV rate of 8.75%, I don't think we are in danger of seeing a distribution cut either. I suspect that the management team knows that this is the main selling point of UTG. Nothing is ever guaranteed, but I would be willing to bet that they would be quite hesitant to cut their payout. At least, I believe it would take a significantly higher NAV rate with little chance of recovery. I don't believe we are in that situation where there isn't some optimism going forward, and at a sub-10% NAV rate, we aren't at precarious levels yet.

UTG's Portfolio

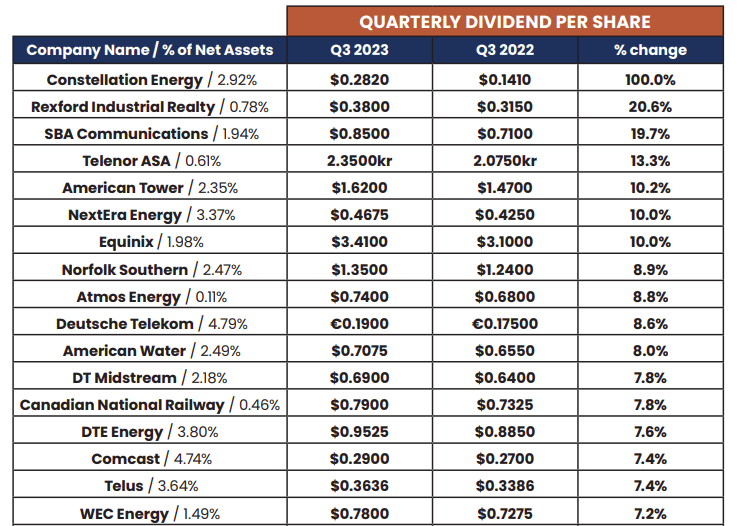

Besides portfolio changes to increase NII for the fund, one thing they've also been focusing on more recently this year has been dividend increases from their underlying holdings. They've now listed each holding for each quarter and what - if any - dividend increase there was for each position. They had a post for Q2 2023 , but the latest was for Q3 2023 .

In that press release, they noted 51 equity positions, with 48 paying dividends during the quarter. They also noted that in the last 12-month period, they saw 43 increased dividends and no reductions. Year-over-year, the weighted average increase was 7.9%.

However, they did note that Constellation Energy ( CEG ) saw a particularly large increase of 100%. CEG was spun off from Exelon ( EXC ) in early 2022, leaving it with a relatively short history, but that can certainly provide some confidence from the management team going forward. When factoring that out, the adjusted year-over-year increase was 5.6%. Here is the breakdown that they provided of those companies with the largest increases that are in UTG's portfolio.

{kind=link}

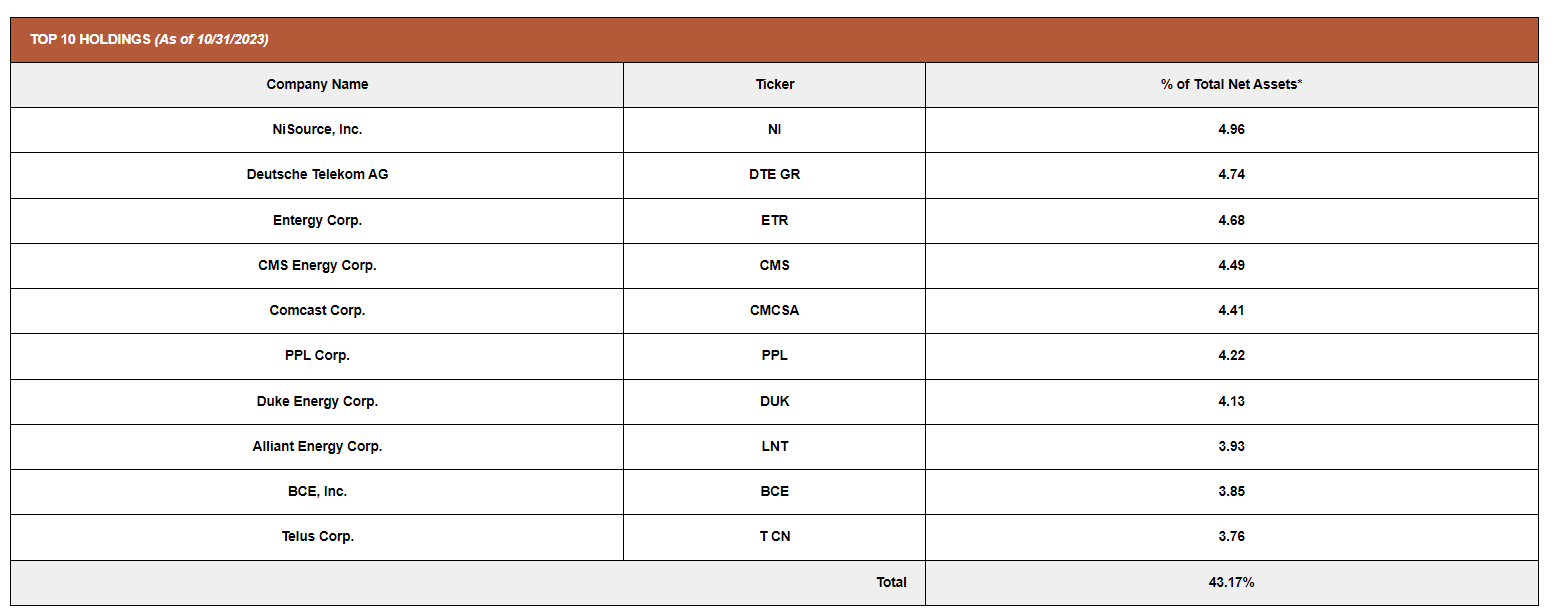

Overall, UTG doesn't carry the largest portfolio, instead concentrating more on fewer names. Their top ten holdings accounted for just over 43% of the fund's weighting. That definitely puts it on the more concentrated side, and that was similar to how the fund was positioned last year , with the top ten at that time making up 43.60%.

{kind=link}

The portfolio turnover also isn't that high here, which tends to mean that the top holdings generally stay top holdings for extended periods of time. That said, the fund's largest holding belongs to NiSource ( NI ), which wasn't positioned in the top ten last year. Additionally, Deutsche Telekom ( DTEGY ) comes in as the second largest position. That was also a new name to the top ten.

A noteworthy name to fall off the top ten list was NextEra Energy ( NEE ). NEE is a highly popular utility company that has been in the top position in most utility and infrastructure funds. However, after a tumble a couple of months ago, that has seen its dominance start to slide. NEE also is the largest position in XLU, at a weighting of ~13%, meaning that NEE is still a substantial part of the overall utility sector.

YCharts

In this case, UTG's full holding list still shows that NEE is a holding, but it has slipped rather meaningfully. NEE went from 4.58% weight to 3.37% weighting.

Conclusion

Utilities aren't going away, and neither is UTG, even as they face this new higher interest rate environment. UTG is a solid utility fund that has been able to deliver a steadily growing distribution to investors. The last several years have been tougher for the fund. That said, those higher interest rates that were a headwind could turn into a tailwind. While I believe that UTG is worth investing in, I'm also cognizant of the fact that it isn't a screaming buy. The trading near parity with its NAV doesn't justify that level of enthusiasm. Therefore, implementing a dollar-cost average approach to building up a position in this one would probably be more appropriate.

For further details see:

UTG: Solid Utility Fund For Income-Oriented Investors