XLC - UTG: Steady Distribution For The Long-Term Investor

Summary

- UTG underperformed XLU, a common benchmark applied to this actively managed closed-end fund.

- However, UTG is much more than XLU, so the lag here isn't too concerning for me in the longer term.

- Especially when investing in UTG, it is more about the distribution than shorter-term results.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 2nd, 2023.

Reaves Utility Income Fund ( UTG ) didn't have a banner year in 2022. Nor did most other investments. In fact, UTG had outperformed most fixed-income and the broader market as measured by the S&P 500 Index.

However, when compared to something like the SPDR Utilities Select Sector ETF ( XLU ), results might seem discouraging. Being an actively managed closed-end fund allows UTG to be much more than just a basic utility index fund though.

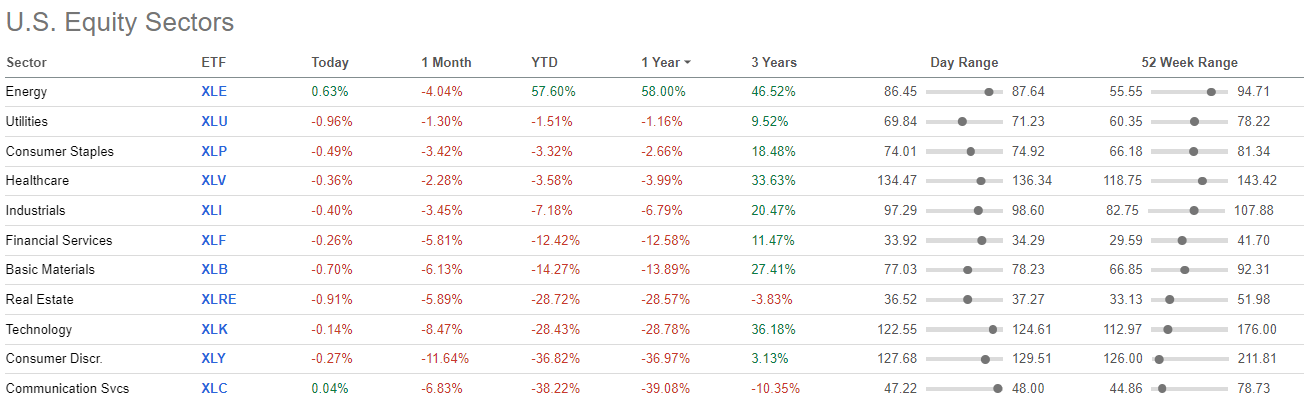

In this case, it seems relatively straightforward why UTG underperformed with its allocations towards communication services and real estate, primarily a big laggard for the year. Communication services were the biggest underperformer through 2022, as measured by the SPDR Communication Services ETF ( XLC ). Real Estate, as measured by the SPDR Real Estate ETF ( XLRE ), was down nearly 29%.

{kind=link}

Throw on leverage to selections that underperform, and you get even more underperformance. Yet, I don't think the shorter-term results for UTG should be the main factor in deciding whether to hold this fund. It seems much more appealing when considering it as an income play with longer-term potential. Given the current circumstance, I don't believe that distribution is going anywhere.

Trading at a slight discount at this time can indicate that it isn't over or undervalued either. In fact, a discount in the last few years is quite rare for UTG, so an argument could be made that it is tilting into the potential add-worthy territory. That would be the other deciding factor for adding or selling a CEF.

The Basics

- 1-Year Z-score: 0.17

- Premium: 0.43%

- Distribution Yield: 7.53%

- Expense Ratio: 1.04%

- Leverage: 18.49%

- Managed Assets: $2.433.8 billion

- Structure: Perpetual

UTG's strategy is to "invest at least 80% of its total assets in dividend-paying common and preferred stocks and debt instruments of companies within the utility industry." While they leave the door open for greater diversification across asset types, they primarily and consistently focus on equities. This can be positive as equities generally provide greater returns for the risks taken over the longer term.

The fund carries a moderate amount of leverage, but any leverage can impact the fund positively or negatively. The upside is boosted, but so is the downside when things aren't going well, such as in 2022. This is one of the stumbles that the fund had in 2020, they weren't forced to deleverage, but they did. Therefore, when things came back, rallying strongly and with a vengeance, they had less capital invested in rebounding.

By the end of 2021, they added back all their leverage and then some. In fact, now, at the end of their fiscal 2022, they are carrying $500 million on their credit line—the highest in their history. Unfortunately, at least in the short term, it looks like it might have been another bad-timing call. They've to leverage up while catching the downdraft of 2022. Longer-term, these added assets could mean stronger results in a rebound. The big question is when that rebound takes place.

That isn't the only problem with leverage, though, as higher interest rates mean higher interest expenses. They borrow at SOFR plus 0.65%. As of writing this, SOFR is at 4.30% , meaning that UTG is paying 4.95%. Anything that they invest in that doesn't return this amount meant it was a drag on performance. With rates only expected to continue to rise, these costs will climb.

Performance - A Small Discount

As I mentioned at the opening of the article, if we compare XLU and UTG, XLU has done much better this year. However, I outlined the main points on why that happened to be the case above.

Another benchmark that investors like to compare UTG to is Cohen & Steers Infrastructure Fund ( UTF ). This is another solid choice in the CEF space. And in fact, UTF has outperformed UTG for another year. This is starting to become a trend; UTG hasn't, on a total NAV return basis, beaten UTF since 2017. That being said, UTF still didn't beat out XLU, either.

YCharts

This was for similar reasons, positioning and leverage being the main factors. UTF is also a diverse fund that invests much more outside XLU's focus. XLU only invests in U.S.-based utilities. Both UTG and UTF can invest globally - although UTG normally holds fairly limited exposure outside of the U.S.

Over the last several years, UTG's discount/premium has often shown a premium. This has flipped a bit lately as the fund returns back to a briefly. A discount wasn't all that unusual going back to before 2019. Combining this average over the last decade, we get an average discount of 2.67% - putting the fund at a slightly elevated valuation compared to that today.

Distribution - The Main Focus

The managers realize that most investors in a CEF concentrate on the distribution. In this case, they've been able to deliver tremendously, and they aren't afraid to mention this.

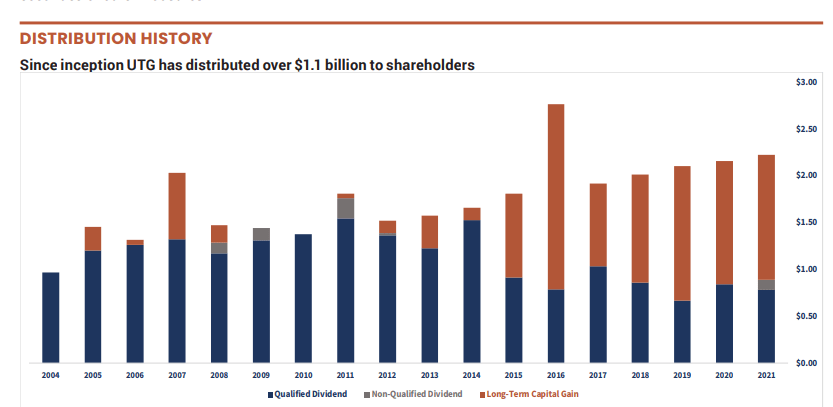

Since the Fund’s first distribution in April 2004, distributions to shareholders have totaled over $1 billion consisting of divided income and realized capital gains with no returns of capital.

The monthly distribution has been increased on 12 occasions from the initial monthly amount of $0.0967 per share to the current amount of $0.19 per share, representing a cumulative increase of 96.48%. The Trustees of the Fund regularly review the amount of the monthly distribution.

As of their latest fact sheet, they've distributed $1.1 billion to shareholders. With a couple more payouts since then, this would now be a bit higher.

{kind=link}

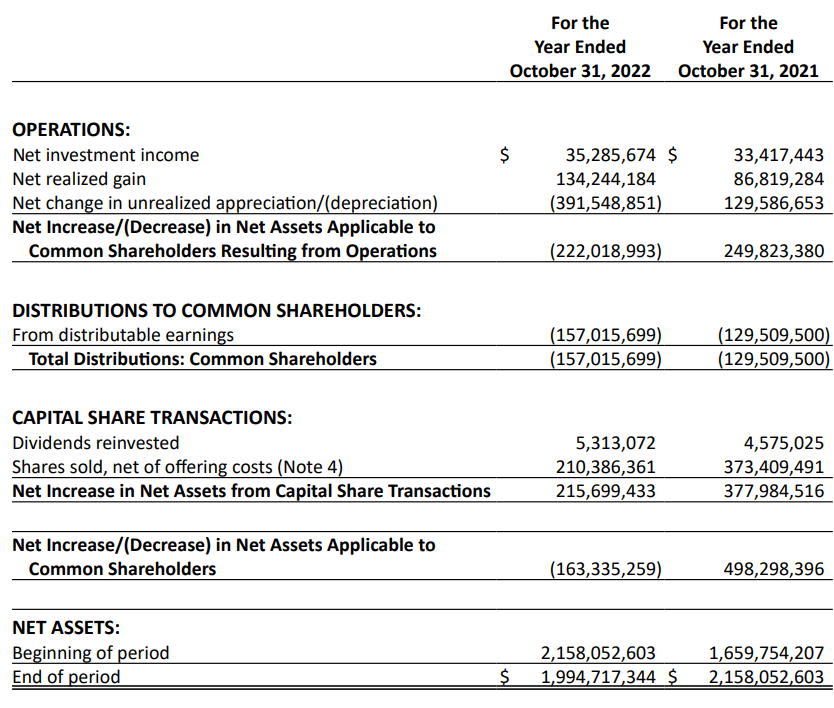

The majority of their distribution has come from capital gains, as shown above. This isn't atypical for an equity-focused fund. In their last annual report, they once again secured enough between net investment income and realized gains to 'cover' their distribution.

{kind=link}

Albeit, we can't completely ignore the unrealized appreciation in the portfolio. Having too many years in a row of such sizeable losses would definitely pressure the fund. At a distribution rate of 7.53% and a NAV rate of 7.56%, combined with the committed focus on payouts for shareholders, I don't think we are anywhere near worrying about a cut.

UTG's Portfolio

At the end of September, they listed nearly 65% in utilities, with the remainder elsewhere. This is where we can see that communication services and real estate made up meaningful allocations of the fund.

UTG Top Sector Allocations (Reaves)

In our last update that showed the industry allocation at the end of April 2022, REITs were an even larger ~16% of the portfolio. Diversified telecommunication services were around a similar weighting coming in at 16.4%.

On the other side of lagging performance, we also see that energy was in the portfolio. At a weighting of just 2.1%, that wasn't enough to move the needle for the fund. The energy sector was the top-performing sector for the year and the only green sector.

UTG has held a fairly narrow portfolio. This hasn't changed, with the latest update of their full holdings list showing 41 names. Their top ten holdings generally bring up a significant weighting in the fund. As of the latest reporting, it represents 43.60% of the fund.

Important to note the full holding list was data from the end of September; however, they list their top ten holdings as of the end of November. There could have been some small changes since then, but as an actively managed fund, every day could bring a change.

{kind=link}

When looking at these names and their performance over the last year, we can see that both TELUS ( TU ) and BCE ( BCE ) were the weaker performers. Do you know what these two names have in common? That's right; both stocks are in the communication services sector. The sector that was the worst performing in 2022 directly highlights why UTG lagged behind something like XLU.

YCharts

Of course, we also have NextEra Energy ( NEE ) which really put up a weak showing, along with Alliant Energy ( LNT ). Both of these are utility names that should have done fairly well.

For both of these, though, they had outperformed the broader utility sector over the longer term. NEE had significantly outperformed as it was a play on renewables, specifically. LNT is also working on renewable ambitions . While I'm a holder of NEE directly, it's hard not to feel it is still stretched at a forward P/E of 29x.

YCharts

Conclusion

UTG beat the broader market in 2022 thanks to its heavier allocation to utilities. However, if compared to a pure utility index fund such as XLU, it has underperformed. It also underperformed UTF once again, a trend going back to 2017 in terms of total NAV return performance being weaker. On the other hand, it's been a great income play as they've focused on delivering a growing distribution to shareholders. That can still make it a worthwhile longer-term holding for me. While they rely on capital gains to fund their distribution, it doesn't appear we are at any danger level for a distribution cut.

For further details see:

UTG: Steady Distribution For The Long-Term Investor