UTG - UTG: Top-Notch Infrastructure CEF To Benefit From Lower Interest Rates

Summary

- UTG has "utility" in its name and holds a portfolio of mostly utilities, but in truth it is more of a general infrastructure fund.

- The closed-end fund has a strong track record of steadily growing distributions since its inception in 2004, without a single dividend cut blemish.

- The biggest headwind is rising interest rates, because UTG is about 25% leveraged.

- During periods of low/falling interest rates, UTG outperforms. But during periods of high/rising interest rates, the CEF struggles.

The Reaves Utility Income Fund ( UTG ) is a lightly leveraged closed-end fund that invests in utility and telecommunications "businesses that grow cash flows and dividend payments more quickly than sector averages and faster than long-term inflation."

The fund began on February 24th, 2004, almost 19 years ago exactly as I write this. Since then, the fund has returned just shy of 10% annually, on average, while tracking closely with unleveraged utility index - the SPDR Utilities Select Sector ETF ( XLU ):

But UTG isn't simply a leveraged version of a market cap-weighted utility index. Rather, it is an actively managed fund that is split roughly 60/40 between utilities and other sectors, such as communications, real estate, industrials, and energy.

Rather than strictly utilities, one can think of UTG as an essential infrastructure fund.

As of the end of 2022, total net assets stood at $2.1 billion as well as $500 million in debt, representing leverage of about 24%. That's up from about 21% leverage the year prior.

While Reaves hand-picks stocks based on their appreciation potential as well as their cash flow and dividend growth profiles, the primary source of returns for UTG is the high-yielding distribution, which comes from both leveraged dividend income and realized capital gains.

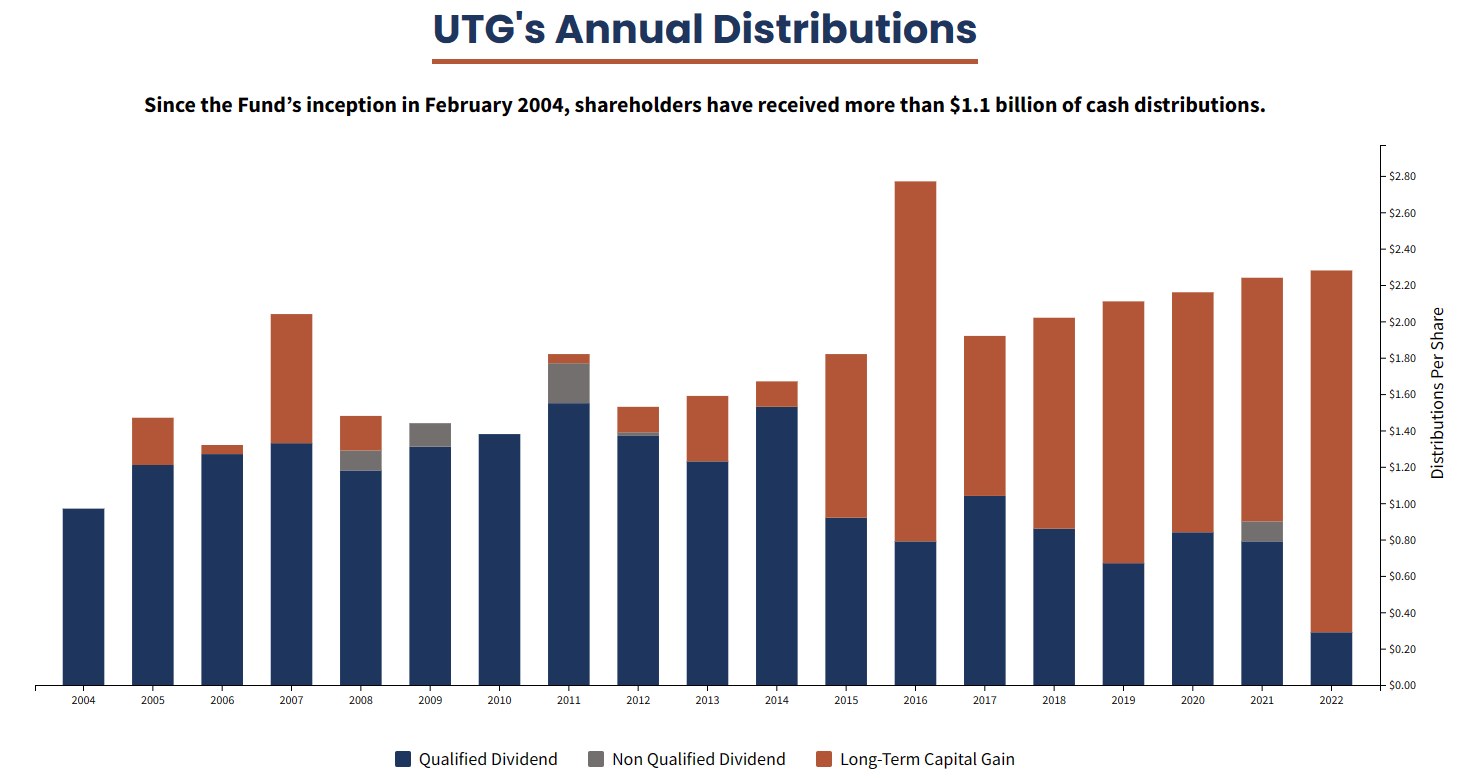

Since inception of the fund in 2004, UTG has returned over $1 billion in distributions to shareholders and has not cut or reduced its regular monthly distribution once, even though the Great Recession of 2008-2009. In fact, the regular distribution has increased by a total of 90%, or about 4.75% annually, since 2004.

The biggest risk to UTG's performance is rising interest rates. Since the fund is leveraged, growing interest expenses create a drag on net investment income. And this is on top of the negative effect higher interest rates have on the fund's underlying holdings, which themselves employ a significant amount of leverage.

To be clear, UTG's distribution does not appear to be in imminent danger, even amid elevated interest rates. But for multiple reasons, UTG is a bet on lower interest rates. Since I am of the view that interest rates will fall sometime in the next year or so, I think now is the perfect time to be buying UTG and its 7.9% distribution yield.

Review of a Year of Underperformance

UTG underperformed in 2022 because of rising interest rates. Full stop.

Much more could be said, of course, but that simple statement sums up the situation pretty well.

The first reason why higher interest rates weigh on UTG's performance is because its underlying holdings tend to utilize a fair amount of debt in their own operations.

Infrastructure is inherently capital intensive. Utilities, telecommunications companies, landlords, railroad companies, and midstream energy companies all use significant leverage in order to fund their ongoing capital expenditures.

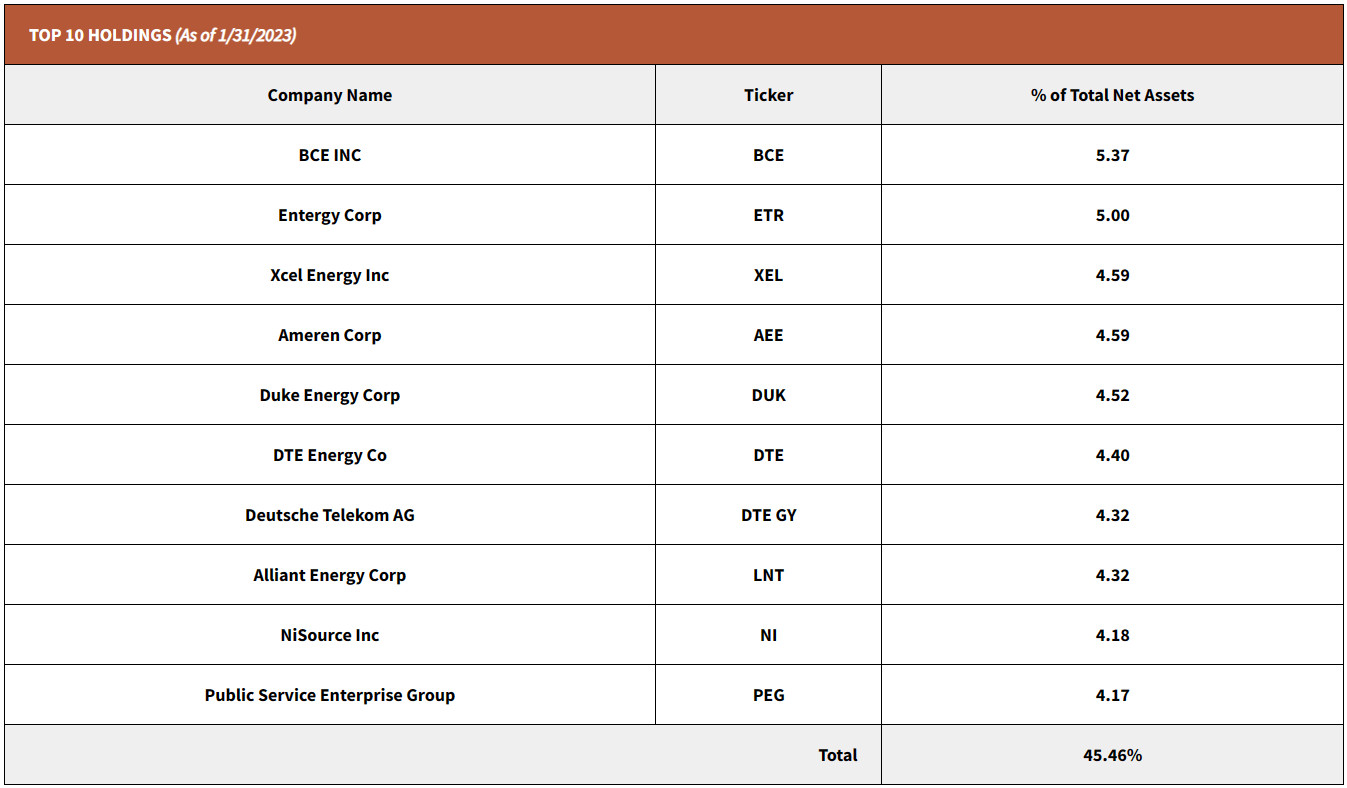

UTG Fact Sheet

You'll notice from the above chart that utilities actually only make up a little over 60% of UTG's portfolio. Sometimes that number is higher, sometimes lower. But the point is that UTG targets infrastructure broadly rather than utilities specifically .

Two of UTG's top ten holdings are telecommunications companies, one Canadian and one European, while the remaining 8 are utilities.

{kind=link}

The focus on utilities is a strength for UTG, because recently enacted federal legislation in the form of the "Inflation Reduction Act" provides a long runway of tax credits for utilities to make investments in the lower-carbon power generation assets that they were largely going to do anyway.

Here's management's commentary on recent federal legislation from the shareholder letter in the fiscal 2022 annual report :

[T]he passage of the Inflation Reduction Act (IRA) in August was a significant event that remains, in our view, underappreciated by most investors. This legislation provides a wide array of incentives to utilities to transition more rapidly away from fossil fuel generation, especially coal. Among them: enhanced and expanded tax credits for new development of renewable generation and electric storage, new tax credits to support existing nuclear generation and the development of new nuclear technology and the production of hydrogen, as well as new incentives for industrial and transportation electrification. These incentives will meaningfully lower the cost of new investments for utilities in these emerging technologies. Additionally, increase in power usage should help by spreading the cost of new investment across more energy sales.

This tailwind for electric utilities makes UTG's ~60% exposure to utilities a strong base to provide steady, consistent returns for the portfolio.

On top of that solid base of utilities, UTG also has a significant (~17%) exposure to communications companies. As of the end of 2022, UTG owned 7 communications stocks:

| Communications Company |

| % of Portfolio (12/31/22) |

| BCE Inc. ( BCE ) |

| 5.15% |

| Deutsche Telekom ( OTCQX:DTEGY ) |

| 3.81% |

| TELUS Corp. ( TU ) |

| 3.78% |

| Comcast Corp. ( CMCSA ) |

| 3.33% |

| Verizon Communications ( VZ ) |

| 2.75% |

| Rogers Communications ( RCI ) |

| 1.56% |

| Charter Communications ( CHTR ) |

| 1.14% |

Here's management's commentary on UTG's communications holdings from the 2022 shareholder letter:

In communications infrastructure, where the Fund's investments are concentrated in cable, data centers, towers, and traditional telecom, returns were negative and were largely responsible for the Fund's overall decline. Two factors contributed to the results. First, rising interest rates negatively impacted companies structured at Real Estate Investment Trusts (REITs) such as our tower and data center investments. While there was little fundamental business deterioration for these companies, valuation multiples fell as investors shifted funds to lower duration assets. Another factor was the prospect of increased competition in the U.S. broadband space. More operators are building fiber and fixed wireless networks to compete with cable, at the same time as cable companies are more aggressively competing in wireless telephony. While competition is certainly becoming more acute, we continue to believe our investments have the potential to outgrow their respective industries and inflation. More importantly, we do not see material risk to the expected cash flows underpinning share repurchase or dividend income contribution from the space.

You'll notice that these comments extend beyond companies categorized in the "communications" sector and to real estate investment trusts ("REITs") that own cell towers and data centers.

Here are UTG's other non-utility holdings:

| Other Non-Utility Company |

| Sector |

| % of Portfolio (12/31/22) |

| Canadian Pacific Railway ( CP ) |

| Industrial |

| 3.33% |

| Union Pacific ( UNP ) |

| Industrial |

| 2.89% |

| SBA Communications ( SBAC ) |

| REIT |

| 2.42% |

| Williams Companies ( WMB ) |

| Midstream Energy |

| 2.35% |

| Norfolk Southern Corp. ( NSC ) |

| Industrial |

| 2.17% |

| Crown Castle ( CCI ) |

| REIT |

| 2.02% |

| TC Energy Corp. ( TRP ) |

| Midstream Energy |

| 1.90% |

| Digital Realty Trust ( DLR ) |

| REIT |

| 1.80% |

| Equinix ( EQIX ) |

| REIT |

| 1.75% |

| DT Midstream ( DTM ) |

| Midstream Energy |

| 0.93% |

| Rexford Industrial ( REXR ) |

| REIT |

| 0.59% |

Rounding out the list of holdings are three railroad companies, three midstream energy companies, and one industrial/warehouse REIT - Rexford Industrial ( REXR ). It appears that REXR was purchased sometime in the fourth quarter of calendar year 2022, during which time the fast-growing REIT traded at an opportunistic price in the low $50s. I like this addition, as it adds a low-yielding but high-growth income stream to the portfolio of mostly high-yielding but low-growth holdings.

The second and probably more substantial reason why higher interest rates weigh on UTG's performance is because the CEF uses leverage to juice higher returns.

UTG's total debt increased from $450 million at 10/31/21 to $500 million at 10/31/22. Presumably, this additional debt was added to make opportunistic purchases.

The fund's floating interest rate formula is SOFR plus 0.65%. Given the current SOFR of 4.55%, UTG's interest rate on debt sits at 5.2%. And each time the Fed raises rates further, the SOFR and UTG's borrowing rate will rise accordingly.

For the fiscal year ending 10/31/22, UTG's interest expense amounted to $8.49 million (12.7% of total investment income), compared to $3.60 million (6.3% of total investment income) in fiscal 2021.

In other words, as a share of investment income, UTG's interest expense doubled from 2021 to 2022. That ate into net investment income.

Despite total investment income increasing by 16% year-over-year from fiscal 2021 to fiscal 2022, net investment income grew only 5.6%.

Now, NII plus net realized gains of $169.5 million in fiscal 2022 did surge from $120.4 million in fiscal 2021, largely because utility stocks performed well and allowed management to take some gains. But this isn't recurring income. You can only take a capital gain once.

Admittedly, though, UTG does have substantial accumulated unrealized capital gains, which explains how the share of distributions categorized as long-term capital gains has increased over time.

{kind=link}

The above chart is a bit noisy, making it look like UTG's distribution fluctuates because of occasional supplemental payouts. But the regular monthly distribution has only grown without a single cut since 2004.

That is an impressive track record for a leveraged fund, if you ask me!

Buy Today Or Wait?

UTG's net asset value per share as of 2/17/23 stood at $28.96, while the stock price as of the afternoon of 2/21/23 had sunk to $28.75. NAV per share surely fell on the 21st as well, so the fund probably still bears a slight premium to NAV, as is its historical precedent.

The current annualized distribution of $2.28 represents a dividend yield of 7.9% on UTG's price of $28.75.

That is obviously an attractive yield for a fund with a strong history of both strong total returns and steady distribution growth. But is now a good time to buy? Or is there more downside potential in the face of rising interest rates?

I would actually answer yes to both. Outside of the initial COVID-19 market selloff, UTG's stock price has not been this low since the December 2018 market plunge. Correspondingly, the dividend yield based on the regular monthly dividend has not been this high since then. So, now certainly doesn't seem like a bad time to be accumulating shares.

At the same time, the Fed seems intent on their policy rate at least another few times, implying that UTG's borrowing rate will go another 50 basis points higher to about 5.7%. That is a substantial headwind that likely spells no distribution increases this year and perhaps further downside in UTG's stock price.

I leave it to you, dear reader, to decide for yourself about timing. But on dips like today's (on February 21st, with the market down 2%+ as of this writing), I am buying shares.

Bottom Line

UTG is a well-managed fund offering a way to gain exposure to utility sector tailwinds and telecommunications cash flows while offering a high-yielding distribution and potential capital appreciation. But make no mistake: it is vulnerable to higher interest rates.

My macroeconomic outlook is that the Fed's policy rate (and perhaps interest rates more broadly) will go a little higher from here before falling steadily in the coming years. If this outlook proves accurate, then UTG should produce very strong returns from the two tailwinds of falling interest rates and beneficial government fiscal policy.

For further details see:

UTG: Top-Notch Infrastructure CEF To Benefit From Lower Interest Rates