UTG - UTG: Valuation Normalized Attractive Risk-Reward Raising The Fund To A Buy (Rating Upgrade)

2023-10-28 07:59:53 ET

Summary

- I was previously cautious on the Reaves Utility Income Fund due to valuations.

- However, with valuations normalized, the risk/reward looks more attractive.

- The UTG fund pays an attractive 9.5% distribution yield that may appeal to long-term income investors.

The last time I wrote about the Reaves Utility Income Fund ( UTG ) was almost a year ago, when I urged investors to remain cautious, as sector valuations were still too high. Since my article, the UTG fund has declined by 17% in price and 10% in total returns, mimicing poor returns for the utility sector as a whole (Figure 1).

Figure 1 - UTG has performed poorly since my last update (Seeking Alpha)

More recently, I have upgraded my rating on the utilities sector, given better valuations. Does that mean the UTG fund deserves a buy as well?

Brief Fund Overview

The Reaves Utility Income Fund is a closed-end fund ("CEF") that primarily invests in equities and bonds of utility companies.

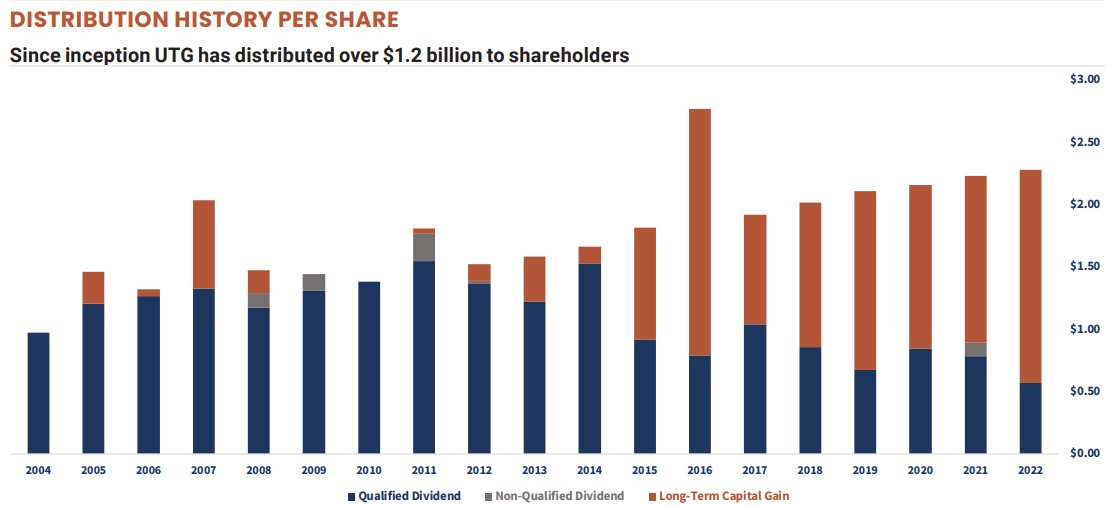

The UTG fund is a long-standing utility CEF that has been known to pay a consistent and high distribution yield through thick and thin. In fact, since inception, the UTG fund has paid more than $1.2 billion in distributions to unitholders (Figure 2).

Figure 2 - UTG has paid $1.2 billion in distributions (UTG factsheet)

{kind=link}

The UTG fund invests in a portfolio of equites and bonds of utilities and other similar companies with stable demand and cash flows. Figure 3 shows a sector breakdown of the UTG fund, showing 59% of the fund is invested in Utilities, 19.2% is invested in Telecoms, and 7.8% is invested in Real Estate.

Figure 3 - UTG sector allocation (UTF factsheet)

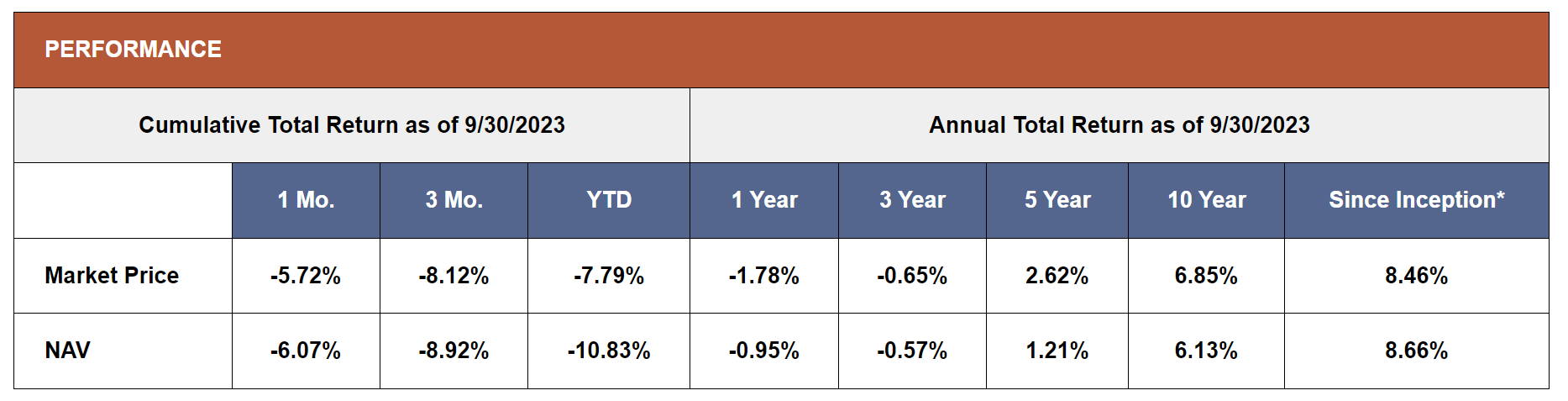

Currently, the UTG fund is set to pay a $0.19 / month distribution or an annualized forward yield of 9.5% on market price, or 9.3% on NAV (Figure 4).

Figure 4 - UTG pays a $0.19 / month distribution (Seeking Alpha)

{kind=link}

UTG's distribution is funded from a combination of income and capital gains. The proportion varies from year-to-year and is dependent on market conditions and the amount of income UTG's portfolio can generate (Figure 5).

{kind=link}

Overall, UTG's distribution appears to be well supported by the fund's long-term earnings, with the fund reporting since inception annual returns of 8.5% compared to its distribution yield of 9.3% of NAV (Figure 6).

Figure 6 - UTG has delivered solid long-term returns (utilityincomefund.com)

{kind=link}

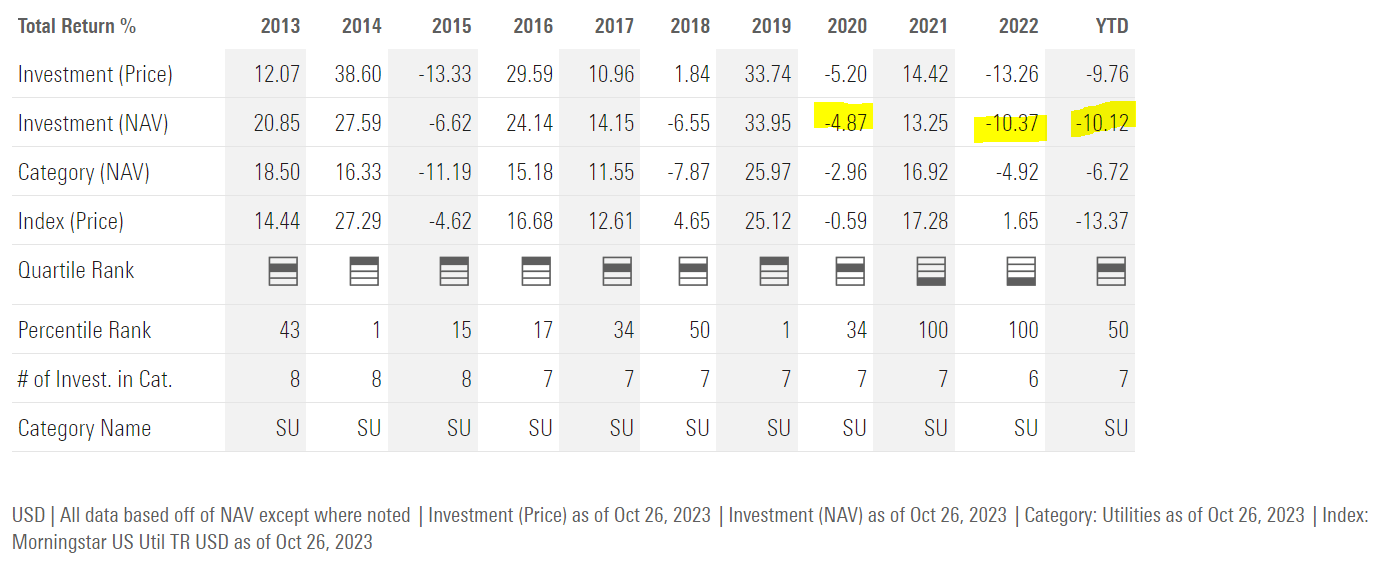

However, performance has been poor the last few years, so the UTG fund has been harvesting NAV to fund its distribution yield (Figure 7).

Figure 7 - But short term performance has been poor (morningstar.com)

{kind=link}

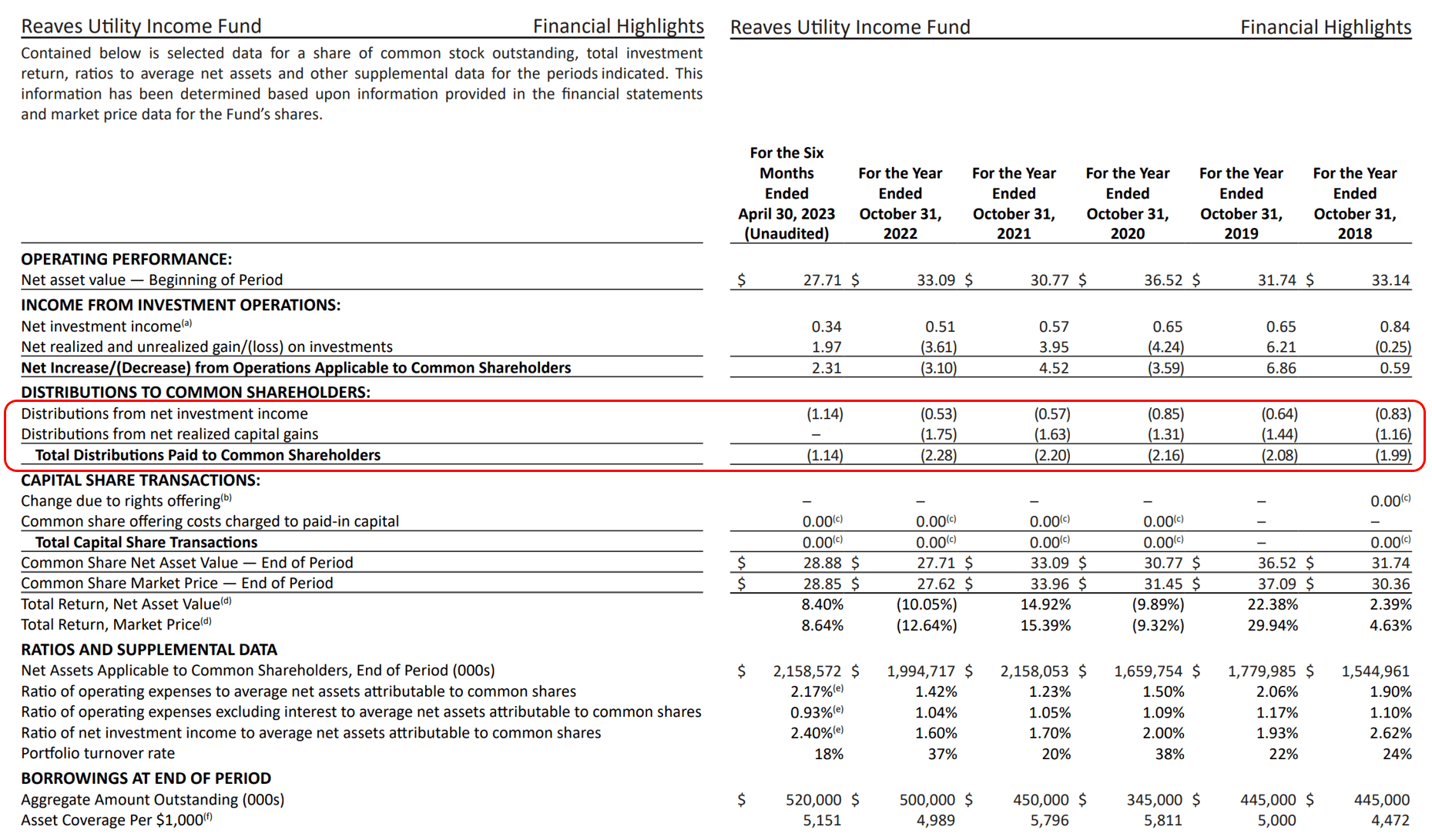

The UTG fund employs leverage to enhance its returns, and has outstanding borrowings of $520 million against $2.1 billion in equity or 20% effective leverage. However, most of the benefit of leverage goes to pay expenses, as the fund charges a fairly hefty 2.17% operating expense ratio for 6 months ended June 30, 2023. Expenses have been elevated due to higher debt servicing costs as interest rates have risen.

Utility Valuations Have Corrected

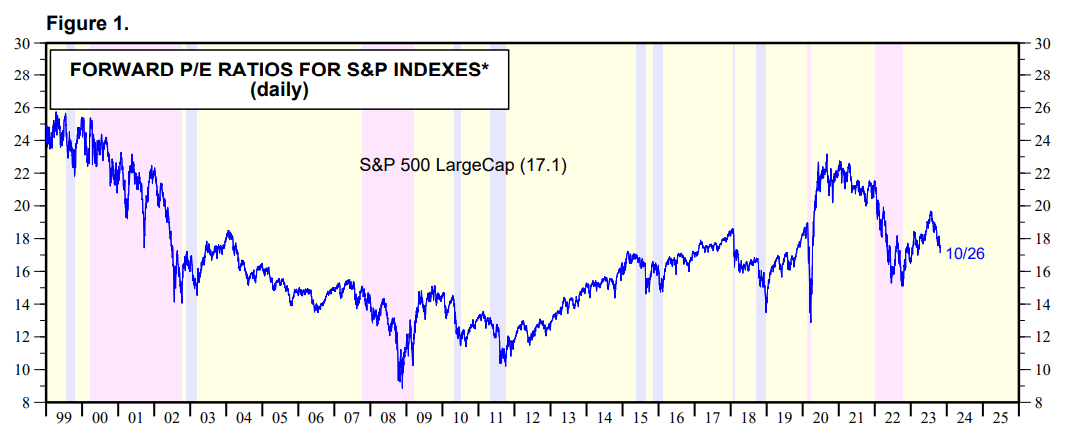

When I last covered the UTG fund, utility sector valuations were just coming off extreme levels as investors crowded into the utility sector as a safe haven against the equity bear market of 2022. Figure 8 is reproduced from my prior article, showing sector valuations peaked at over 20x Fwd P/E, but were still elevated in November 2022 at ~18x Fwd P/E.

Figure 8 - Utilities were trading at elevated multiples in late 2022 (yardeni.com)

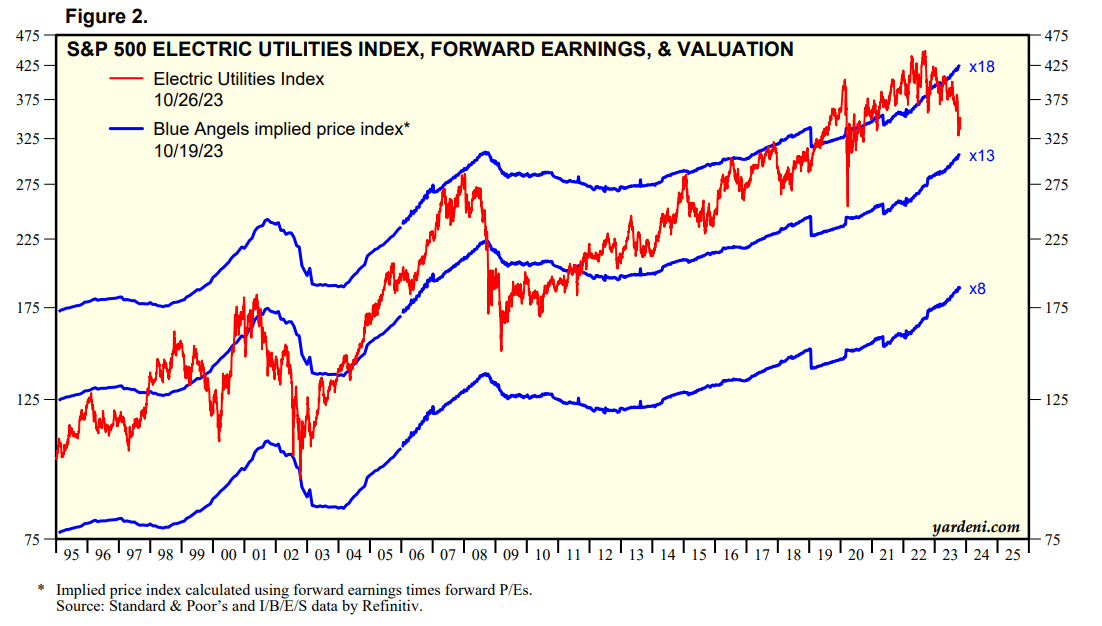

However, the valuation multiple for the utility sector has since contracted even more to ~15-16x Fwd P/E currently (Figure 9).

Figure 9 - But valuations have further corrected to 15-16x Fwd P/E (yardeni.com)

{kind=link}

Although technically, utilities are still not 'cheap' from an absolute sense, they have normalized compared to historical sector valuations of between 13-18x Fwd P/E.

Relative Valuation Screens Attractive

Furthermore, while utility sector multiples have contracted, the market's multiple has expanded from ~15x in late 2022 to ~17x currently (Figure 6).

{kind=link}

So on a relative basis, the utility sector had gone from a premium multiple to the market to a discount multiple to the market.

Has Clean Energy Bubble Burst?

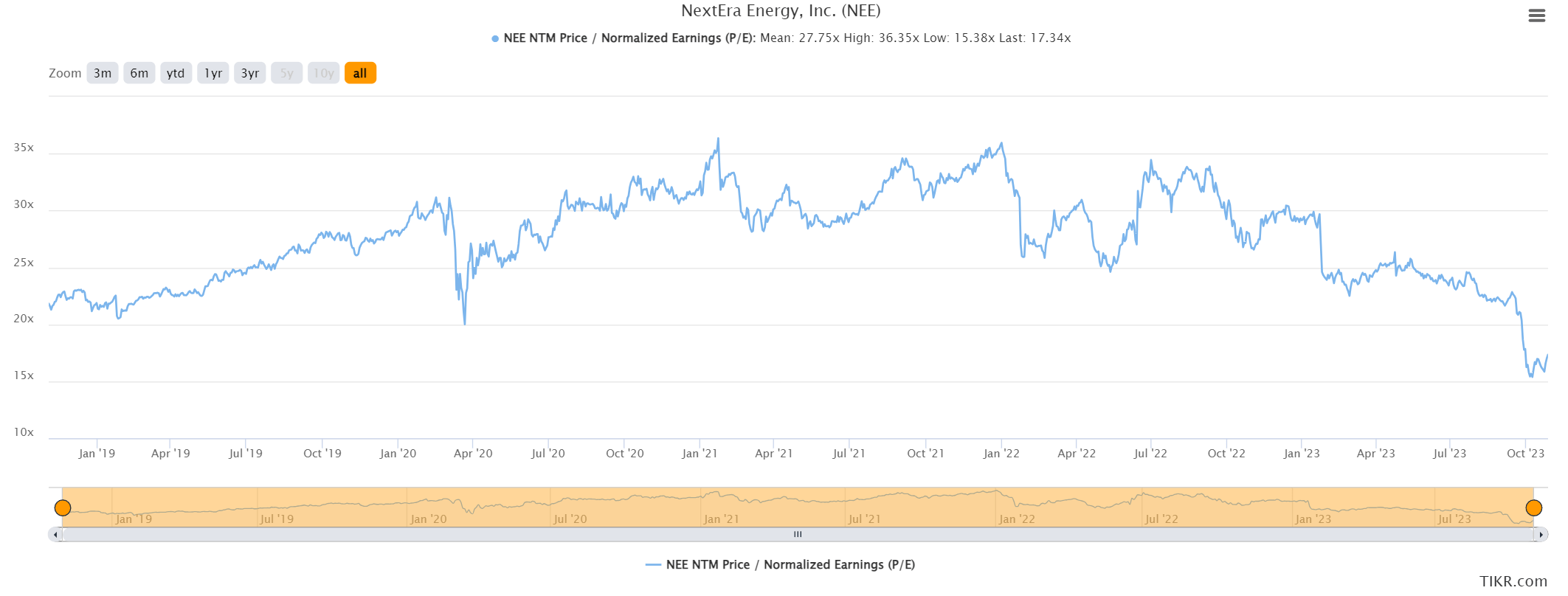

Importantly, part of the reason utility sector valuations were so high was due to a clean energy 'bubble' where utilities that were focused on clean energies like solar and wind had a seemingly zero cost of capital and were valued at ridiculous earnings multiples by the market. For example, NextEra Energy Inc. ( NEE ), a poster-child of this excess period, was trading at 35x Fwd P/E at one point in 2021/2022 (Figure 11).

Figure 11 - NEE was trading at a ridiculous 35x Fwd P/E (tikr.com)

{kind=link}

However, as interest rates have risen, leading to higher cost of debt capital, growth for clean energy utilities have been drastically reduced. This has led to a downward re-rating in high-flyers like NEE, with NextEra now trading at a much more modest 17x Fwd P/E.

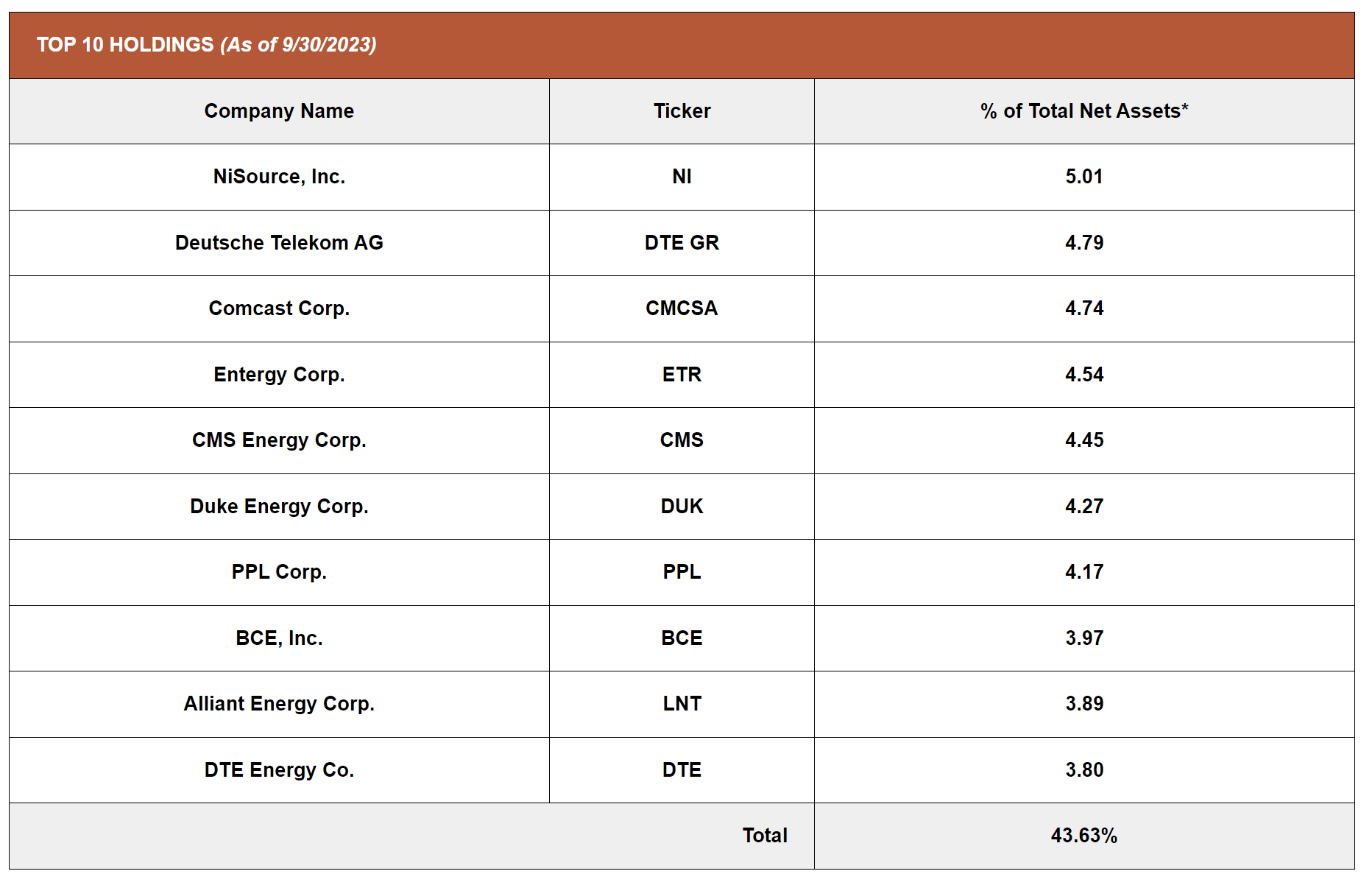

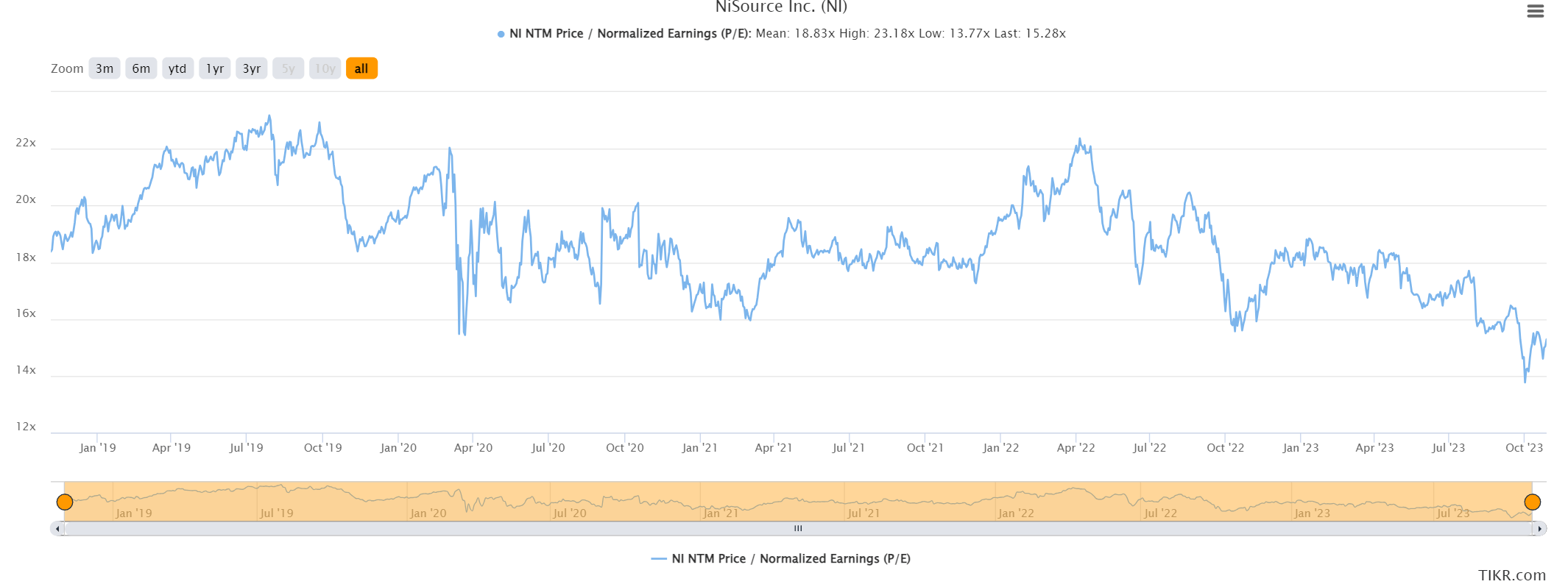

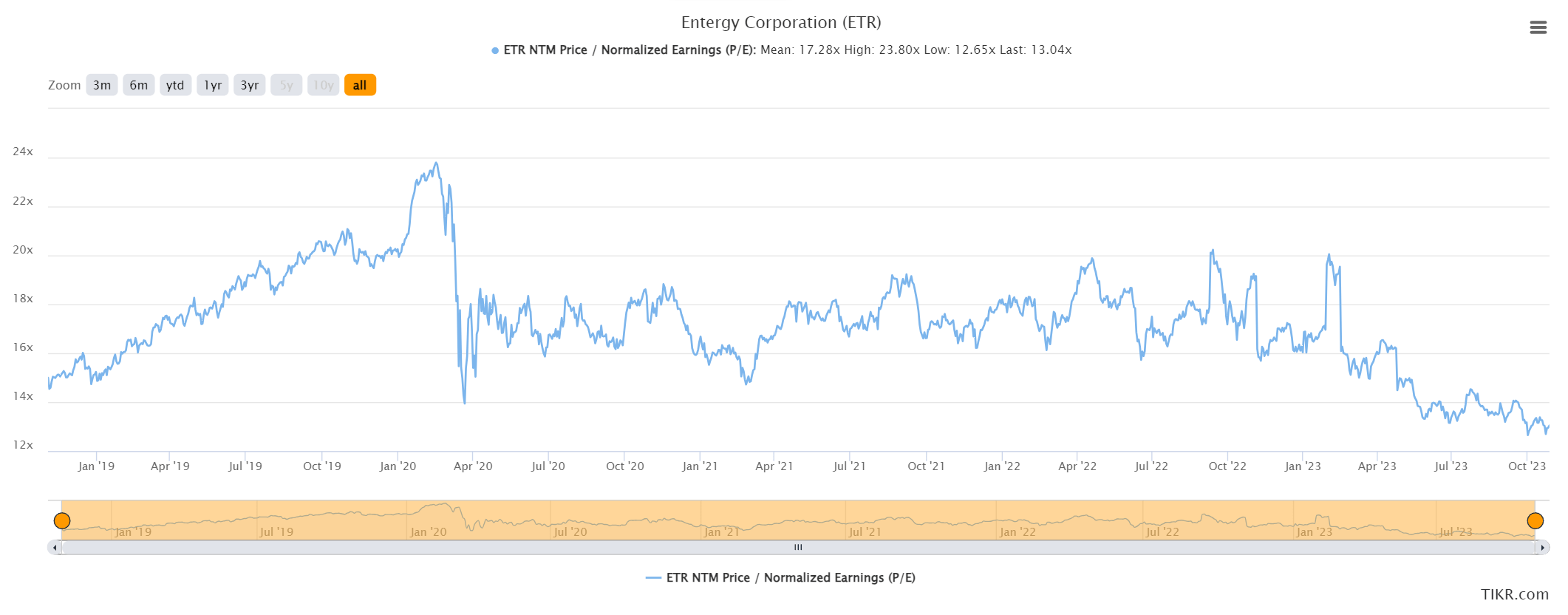

Furthermore, investors should be happy to note that while market-cap weighted ETFs and indices had a large weight in NextEra due to its market cap (NEE was a 16% weight in the XLU ETF in 2022), discretionary managers like UTG can choose not to participate in non-sensically priced stocks like NEE. Figure 12 shows the top 10 holdings of UTG, which is geared towards much more 'defensive' utilities like NiSource ( NI ) and Entergy ( ETR ).

{kind=link}

While elevated, the valuation multiples on these defensive utilities were never over-valued to the degree that NextEra was (Figure 13 and 14).

{kind=link}

{kind=link}

Upgrade To Sector Rating On Relative Valuations

As mentioned at the beginning of this article, a few weeks ago, I upgraded the utilities sector to a buy on the improving relative valuation picture I have discussed above.

My short-term timing could not have been worse, as the XLU ETF plunged by 5% on the Monday after my article was published on interest rate fears hurting long-duration utilities. However, over the following weeks, utilities have recovered nicely and has actually outperformed the S&P 500 since my article, delivering positive total returns while the markets have continued to decline (Figure 15).

Figure 15 - XLU has outperformed since recommendation (Seeking Alpha)

My bullish view on the utility sector is applicable to the UTG fund as well. While we cannot perfectly time short-term market gyrations, I believe sector valuations are now normalized enough that the risk/reward to being long utilities is attractive.

Risks To UTG

Of course, there are no guarantees with investing. The biggest risk I see to utilities is if the whole market continues to correct / enter a bear market. In that case, utility funds like UTG will inevitably suffer alongside the market.

However, given attractive relative valuations and stable business fundamentals, I expect utilities to outperform in that scenario.

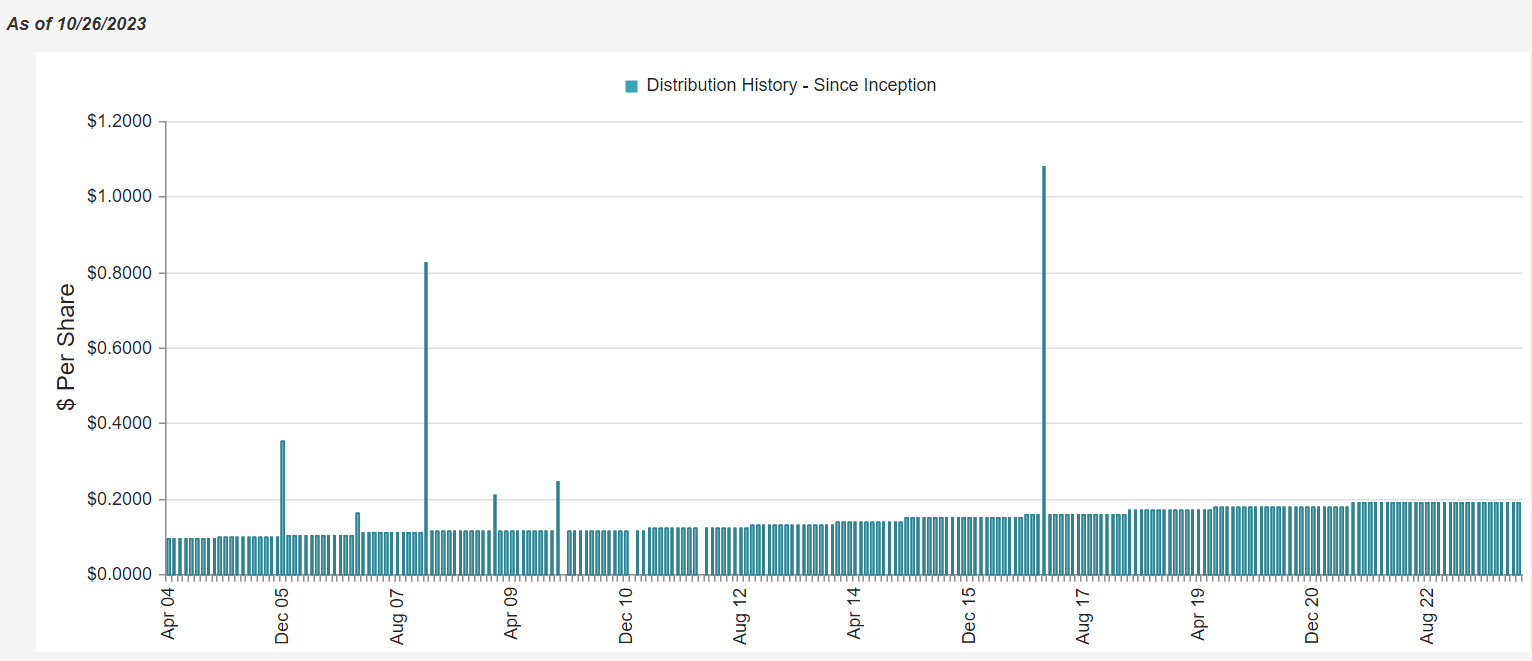

A risk specific to UTG is if the fund suffers a second negative year in a row and 3rd in 4 years, will the UTG fund have to revisit its distribution policy and potentially cut its distribution? Historically, the UTG fund has never cut its distribution, even during the depths of the Great Financial Crisis and COVID-pandemic. So if it does cut its distribution, investors should expect a large decline in UTG's share price (Figure 16).

Figure 16 - UTG has never cut its distribution (cefconnect.com)

{kind=link}

Conclusion

In summary, I believe the risk/reward for the Reaves Utility Income Fund has now shifted into attractive territory as sector valuations have normalized. The fund pays an attractive 9.5% yield.

However, investors need to be aware that 2023 could be UTG's 3rd negative year in 4, and the fund may have to revisit its distribution policies given its declining NAV.

I am raising my rating on the UTG fund to a buy .

For further details see:

UTG: Valuation Normalized, Attractive Risk-Reward Raising The Fund To A Buy (Rating Upgrade)